On 12 May 2026, the ASX’s two worst-performing sectors were healthcare and technology, yet the forces destroying value in each had almost nothing in common. Budget Day created a nervous backdrop across the market, with investors rotating out of rate-sensitive and policy-exposed names ahead of the evening’s federal budget announcement. Against that positioning, CSL absorbed a second consecutive day of institutional selling as ten brokers slashed price targets and three cut ratings following Monday’s historic profit warning. Simultaneously, Life360 fell 10.9% after disclosing that a third-party anti-fraud system error had suppressed new user registrations through Q1. What follows unpacks the distinct mechanisms driving each sector’s decline, examines the full broker response to CSL’s guidance cut, and situates both stories within the broader market dynamics of the session so readers understand not just what happened but why.

A split session: materials surge while growth names take the hit

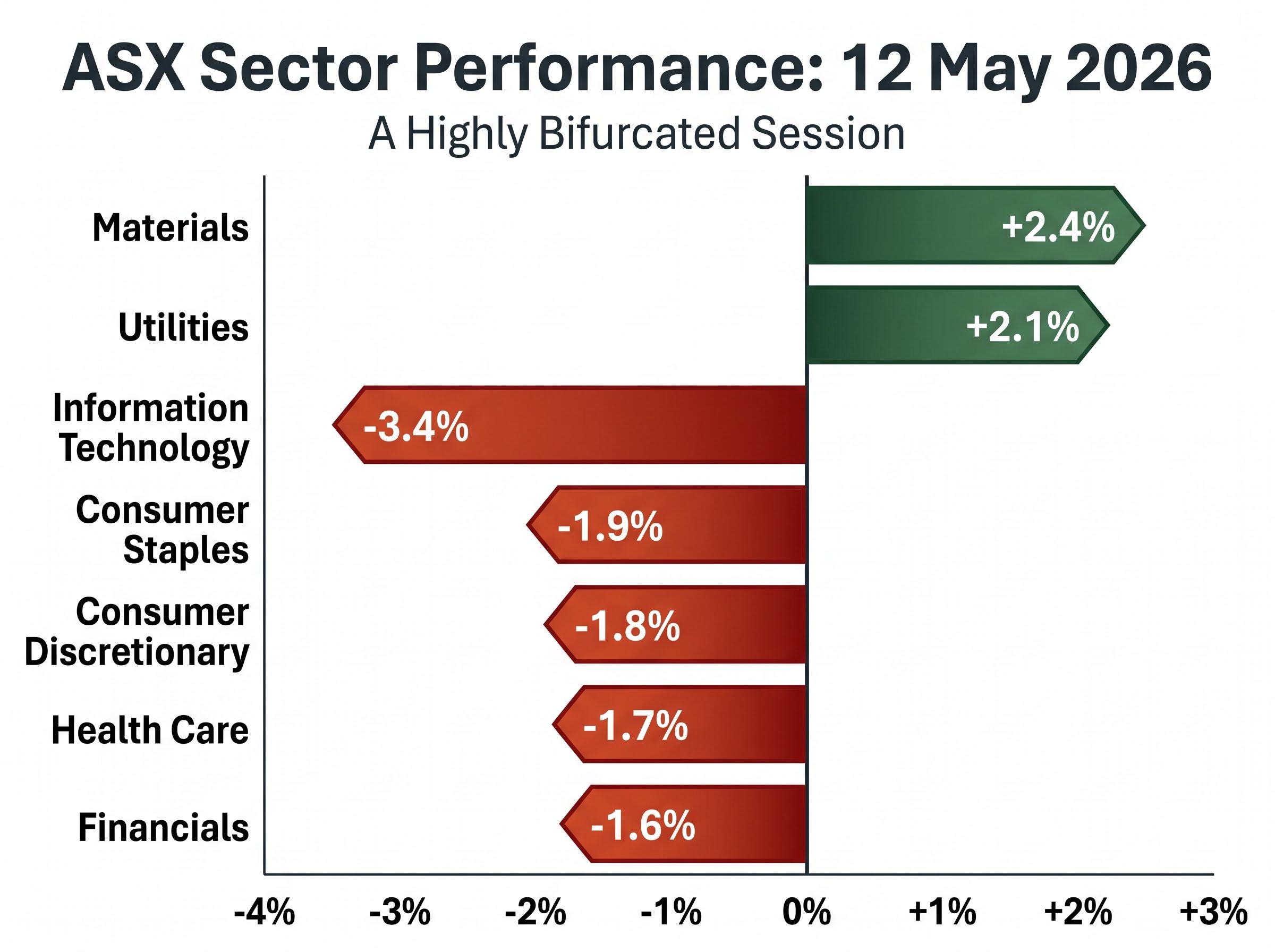

The S&P/ASX 200 closed at 8,670.7, down 31.1 points or 0.36%. That headline number is a poor summary of a highly bifurcated session.

Materials led the board higher, with the ASX Materials index (XMJ) rising 2.4% as COMEX copper futures closed at a record above US$6.45 per pound. BHP gained 2.5%, Rio Tinto added 3.1%, and South32 climbed 3.6%. Utilities followed, with the ASX Utilities index (XUJ) up 2.1% and Origin Energy rising 2.7%.

StoneX copper market analysis confirms the record-high COMEX copper print was driven by speculative positioning and a widening disconnect between physical supply conditions and futures pricing, context that helps explain why the materials sector rally carried conviction rather than reflecting a straightforward demand surge.

At the other end, the ASX Information Technology index (XIJ) fell 3.4%, the session’s worst performer, and the ASX Health Care index (XHJ) dropped 1.7%. Pre-budget investor positioning was the dominant behavioural theme: capital rotated into commodity names and real-asset-backed sectors, and out of long-duration growth stocks whose valuations are most sensitive to rising yields.

| Sector | Index Code | Session Move |

|---|---|---|

| Materials | XMJ | +2.4% |

| Utilities | XUJ | +2.1% |

| Energy | XEJ | Positive |

| Financials | XFJ | -1.6% |

| Health Care | XHJ | -1.7% |

| Consumer Staples | XSJ | -1.9% |

| Consumer Discretionary | XDJ | -1.8% |

| Information Technology | XIJ | -3.4% |

Within the S&P/ASX 300, advancing stocks trailed declining stocks 86 to 200, a breadth reading that confirms the damage was far wider than the modest headline decline suggests.

When big ASX news breaks, our subscribers know first

Why rising energy prices were punishing tech stocks before Life360 said a word

The transmission channel ran through crude oil. ICE Brent crude rose 2.2% to US$106.52 per barrel, pushing energy costs and inflation expectations higher, which in turn lifted bond yields. Higher yields increase the discount rate applied to future earnings, and that repricing hits high price-to-earnings technology names hardest.

Siteminder (ASX: SDR) and WiseTech Global (ASX: WTC) were already in downward price trends before the session opened. The macro environment simply reinforced existing weakness. The ASX Information Technology index (XIJ) fell 3.4%, the session’s worst-performing sector, before any company-specific headlines entered the picture.

Individual tech stock declines included:

- Life360 (ASX: 360): down 10.9%

- Siteminder (ASX: SDR): down 6.0%

- WiseTech Global (ASX: WTC): down 5.9%

- Catapult Sports (ASX: CAT): down 5.1%

The investor takeaway is straightforward: when energy prices rise and yields follow, the re-rating is sector-wide, not stock-specific. No individual company’s strong fundamentals can fully insulate it from that macro force.

The transmission from oil price and rate expectations to equity valuations ran faster in May 2026 than in previous cycles because central banks were simultaneously navigating a supply-shock inflation environment that constrained their ability to cut, amplifying the discount-rate sensitivity of long-duration growth stocks.

Life360’s third-party anti-fraud error and what it means for user growth guidance

Life360’s decline was a company-specific accelerant layered on top of the broader rotation. A modification to an anti-fraud system at a third-party partner incorrectly flagged legitimate user traffic, suppressing new account registrations. The error disproportionately affected Android and lower-specification devices.

The impact is not expected to fully normalise until Q3 2026, meaning user growth metrics will remain depressed through at least two more reporting periods. Life360 reduced its user growth outlook as a direct result, making this a guidance-cut event rather than a one-quarter noise item.

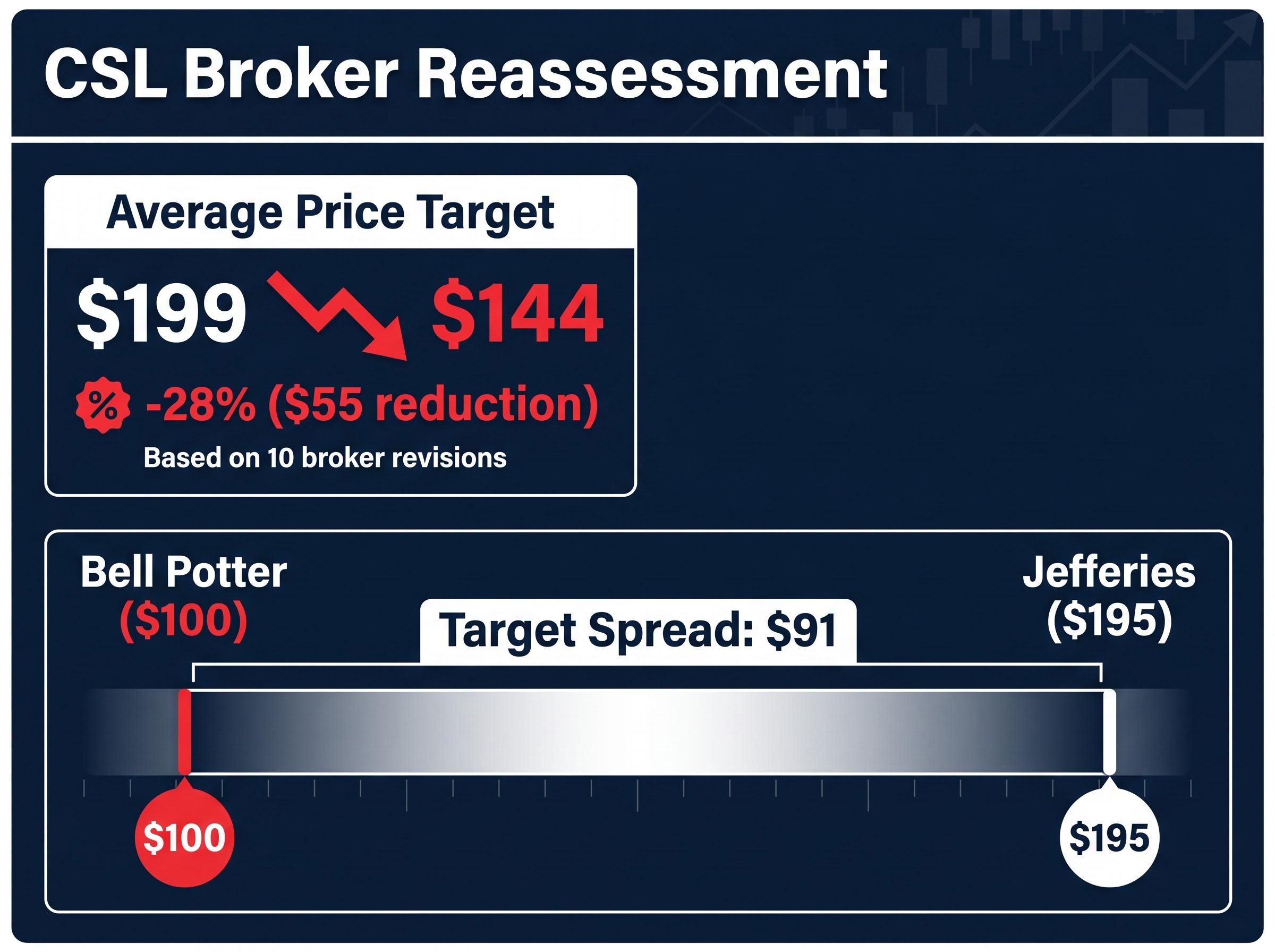

What ten brokers’ simultaneous reassessment tells you about CSL’s credibility problem

On 12 May, ten brokers revised their CSL price targets downward. Three, Citi, Jarden, and Canaccord, cut ratings from buy-equivalent to hold-equivalent. The spread between the most bearish and most bullish targets tells the story of how uncertain the earnings floor now appears.

CSL’s 16% single-day collapse on 11 May erased A$9.48 billion in market capitalisation in a single session, representing the largest single-day decline in the company’s listed history and the direct catalyst for the ten-broker reassessment that followed.

The average analyst price target fell to $144 from $199, a $55 reduction representing a 28% collapse in consensus value in a single round of revisions.

CSL fell an additional 2.2% on 12 May, compounding Monday’s historic 17-21% crash.

| Broker | Rating Action | New Price Target | Prior Price Target |

|---|---|---|---|

| Bell Potter | Retained hold | $100 | $155 |

| Citi | Downgraded to neutral | $110 | $200 |

| Macquarie | Retained neutral | $111 | $176 |

| RBC Capital Markets | Retained sector perform | $113 | $176 |

| Ord Minnett | Retained hold | $135 | $186 |

| Morgans | Retained buy | $147.59 | $241.34 |

| Morgan Stanley | Retained overweight | $166 | $198 |

| UBS | Retained buy | $175 | $205 |

| Jarden | Downgraded to neutral | $191 | $244 |

| Jefferies | Retained buy | $195 | $212 |

The $91 spread between Bell Potter’s $100 floor and Jefferies’ $195 ceiling reflects genuine analytical disagreement about whether CSL’s impairments represent a one-off reset or a structural earnings problem. That uncertainty is itself a reason valuations remain under pressure.

The anatomy of CSL’s profit warning and why the market ran out of patience

The broker cascade on 12 May was not an isolated overreaction. It was the logical endpoint of a pattern that began in mid-2024: four guidance cuts in eighteen months, each deferring the promised recovery further into the future. By the time Monday’s announcement landed, the market had run out of patience.

The specific FY26 revenue headwinds, totalling approximately US$650 million in stated pressures, break down into three categories:

- US immunoglobulin channel inventory normalisation: approximately US$300 million revenue impact. Demand grew mid-to-high single digits, but excess inventory in the distribution channel suppressed new orders.

- China albumin market contraction: approximately US$200 million impact. CSL expanded market share, but the overall market value declined.

- Middle East disruptions, slower Hemgenix uptake, and iron competition: approximately US$150 million combined impact.

The net guided revenue decline of approximately US$400 million implies meaningful offsets, but management’s public disclosures did not fully reconcile the gap. FY26 revenue guidance sits at approximately US$15.2 billion (constant currency), down from US$15.6 billion in FY25. FY26 NPATA guidance is approximately US$3.1 billion, down from US$3.3 billion in FY25.

The write-down problem and the road to FY28

On top of the revenue shortfall, CSL announced approximately US$5 billion in additional non-cash pre-tax impairments across FY26-FY27, layered on the US$1.5 billion already recorded in 1H FY26. A non-cash pre-tax impairment means the company is writing down the book value of assets (primarily CSL Vifor intangible assets and selected property, plant, and equipment) to reflect that those assets are no longer expected to generate the returns originally forecast. No cash leaves the business, but the write-down signals that prior acquisition assumptions were too optimistic.

Interim CEO Gordon Naylor’s 90-day review concluded that growth initiatives are “working,” but financial benefits have been “delayed longer than expected.” That framing captures the core credibility problem: the strategy may be sound, but the timetable keeps moving. CSL’s shares have declined more than 66% since mid-2024, and Monday’s 17-21% fall was the largest single-day decline in the company’s history.

The recovery thesis rests on US$500-550 million in annual transformation savings by FY28, targeting portfolio growth, operational savings, and capital discipline. No near-term catalyst has been identified across broker coverage.

Budget Day cross-currents: financials, consumers, and the sectors caught in policy crossfire

While CSL and the tech sector dominated headlines, the federal budget was quietly reshaping positioning across multiple other sectors.

The ASX Financials index (XFJ) fell 1.6%, driven by concern that potential changes to negative gearing and capital gains tax settings could reduce property investor mortgage demand. Property investors accounted for approximately 40% of total mortgage applications in 2025, making any policy shift a material risk to bank lending volumes. Individual financial stock declines included:

- ANZ and NAB: each down 2.1%

- CBA and Westpac: each down 1.4%

- HMC Capital: down 5.8%

- Australian Finance Group: down 5.5%

- Judo Capital: down 5.5%

- Zip Co: down 5.4%

Consumer-facing sectors also weakened, with the ASX Consumer Staples index (XSJ) down 1.9% (Coles down 2.6%, Woolworths down 1.7%) and the ASX Consumer Discretionary index (XDJ) down 1.8% (Temple and Webster down 6.0%, Lovisa down 4.8%, Guzman Y Gomez down 4.8%). Expectations of fiscal restraint in the budget sustained concern about household cost-of-living pressure.

NAB Business Conditions fell 3 points to +3 index points, the second-lowest reading since 2020. Forward orders have declined 11 cumulative points since February.

The NAB Business Conditions reading of +3 index points, its second-lowest since 2020, sits alongside per capita recession signals that predate the budget: corporate insolvencies at their highest since the 1990-91 recession, real wage declines, and consumer confidence at a 50-year low, forming a backdrop that made fiscal restraint expectations particularly damaging for consumer-facing names.

What comes next for ASX investors as the dust settles on Budget Day

Three data releases over the next three trading days will shape ASX direction:

- US April CPI (due 13 May 2026): consensus forecast +0.6% month-on-month headline, down from March’s +0.9%. A higher print would reinforce the yield pressure that hit growth stocks on 12 May.

- Australian Wage Price Index (due 14 May 2026): consensus forecast +0.8% quarter-on-quarter. A strong reading could alter RBA rate-cut expectations.

- Post-budget market reaction: the evening’s announcements on tax, spending, and housing policy settings will be digested in Tuesday’s session.

The 30-year Treasury yield threshold of 5%, flagged by Bank of America’s Michael Hartnett as a potential market deterioration trigger, sat at 4.98% on 30 April; the 13 May US CPI print now carries outsized significance as the single data release most likely to determine whether that level holds or breaks.

The S&P/ASX 200 sits below its short-term trend ribbon at 8,771-8,775. A sustained close above that band is required to neutralise downside risk toward the 8,262-8,379 support zone. For CSL, no near-term catalyst has been identified by any broker, and earnings stabilisation is not expected before FY28. Life360’s user growth normalisation is not anticipated before Q3 2026.

For investors managing exposure to CSL, Life360, or other rate-sensitive growth names, the data releases ahead will either validate or challenge the repricing the market delivered on 12 May.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A session that rewarded conviction in commodities and punished faith in growth narratives

On 12 May 2026, the market simultaneously punished two types of faith through entirely different mechanisms. CSL’s broker cascade reflected accumulated credibility damage from a specific company’s repeated execution failures across four guidance cuts in eighteen months. The technology selloff reflected a macro repricing mechanism, transmitted through crude oil and bond yields, that penalises duration regardless of company quality.

The session’s only genuine strength, in materials and utilities, reflected tangible asset backing and commodity tailwinds, not earnings growth optimism. The market rewarded what could be weighed and measured, and punished what required patience and belief.