CBA Shares Drop 10%: a Record Fall With No Crisis to Blame

2 hrs ago

Treasury yields climbed to their highest level since June 2025 on the morning of 13 May 2026, the same day the U.S. Senate is scheduled to vote on Kevin Warsh as the next Federal Reserve Chair. The 10-year Treasury yield reached 4.42%, up 4 basis points from Friday’s close, as bond markets priced in a less accommodative monetary policy regime before the confirmation vote had even begun.

Jerome Powell’s term ends this week. Warsh, confirmed to the Fed Board of Governors on Monday 12 May in a 51-45 vote, is one Senate vote away from the top job. The policy shift on the table, a return to strict 2% inflation targeting, the potential abandonment of forward guidance, and an accelerated balance sheet reduction, represents one of the sharpest philosophical pivots at the Fed in decades. What follows covers who Warsh is, how the confirmation unfolded, what his policy philosophy means for interest rates and the balance sheet, and what investors should watch as the transition takes effect.

The first vote is already done. On 12 May 2026, the Senate confirmed Kevin Warsh to the Fed Board of Governors for a 14-year term by a margin of 51-45. Senator John Fetterman (D-PA) was the sole Democratic crossover in an otherwise party-line result.

The second vote, the one that matters for monetary policy, is expected today. The governor confirmation and the chair confirmation are procedurally distinct. Only the chair vote grants Warsh authority to set the Federal Open Market Committee (FOMC) agenda, lead press conferences, and serve as the Fed’s primary public voice.

The milestones that brought the nomination to this point:

The path was not frictionless. Senator Thom Tillis temporarily blocked advancement over a Department of Justice probe into Powell, a procedural detour that underscored how politically charged Fed personnel decisions have become. Powell’s term ends this week, making the chair vote’s timing operationally urgent.

The nomination cleared the Senate Banking Committee on 29 April 2026 in a strict party-line 13-11 vote, a milestone that triggered the first visible market reaction: Treasury yields rose, the S&P 500 was flat, and the dollar firmed, confounding the dovish relief rally some had expected.

Warsh is not a technocratic unknown arriving without a record. He was appointed to the Board of Governors in 2006 at age 35, making him the youngest Fed Governor in the institution’s history. He served through 2011, covering the full arc of the 2008 financial crisis response, from the early liquidity interventions through the first rounds of quantitative easing.

That experience shaped a specific worldview. Warsh participated in the emergency measures that stabilised the financial system, then watched those emergency tools become permanent features of Fed policy. His return to the Fed is not a reunion; it is an ideological re-entry. At his 21 April 2026 confirmation hearing before the Senate Banking Committee, Warsh laid out a philosophy that directly challenges the policy architecture of the past 15 years.

According to CFR analysis of the hearing, Warsh criticised the Fed’s drift into “political debates, climate policy,” calling for a reversion to the institution’s core statutory mandate of price stability and maximum employment.

His prior crisis-era credibility gives that critique institutional weight. Warsh is not an outsider questioning tools he never used; he is a former insider arguing those tools were kept too long and applied too broadly.

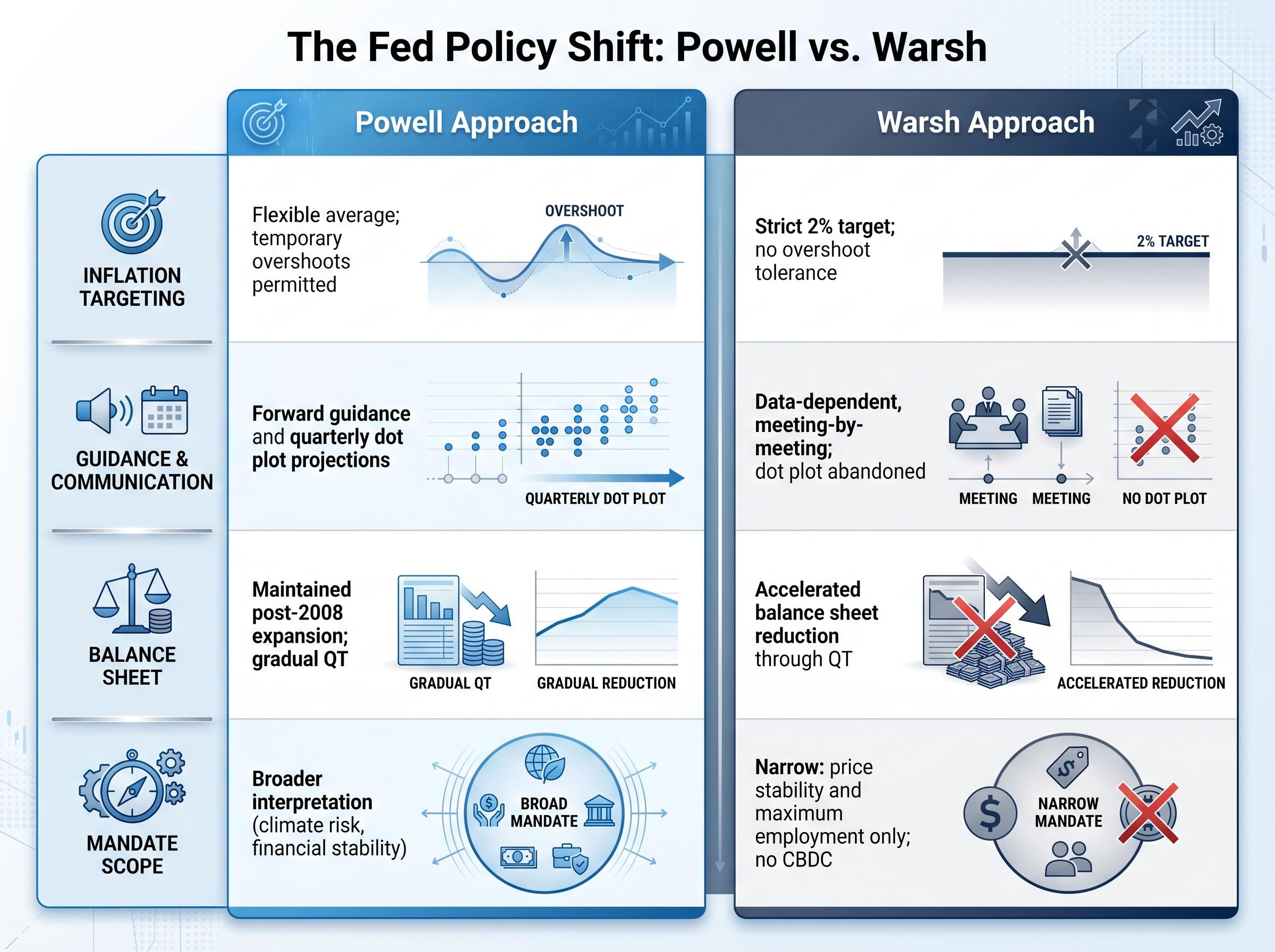

The differences between Warsh and Powell are not abstract. They translate into specific decisions about how rates are set, how the Fed communicates, and how large its balance sheet remains.

Powell adopted flexible average inflation targeting in 2020, a framework that permitted temporary overshoots above 2% to compensate for periods of undershooting. Warsh opposes this framework and favours a strict 2% target with no tolerance for deliberate overshoots.

The FOMC’s 2020 flexible average inflation targeting framework, codified in the committee’s Statement on Longer-Run Goals and Monetary Policy Strategy, formally permitted temporary inflation overshoots above 2% to compensate for prior undershooting periods, a structural accommodation that Warsh has explicitly identified as the core problem he intends to reverse.

On communication, the divergence is structural. Powell relied on the dot plot and forward guidance to telegraph the Fed’s rate intentions to bond markets. Warsh favours abandoning both tools in favour of data-dependent, meeting-by-meeting decisions, a shift that would remove one of the primary mechanisms through which markets currently price rate expectations.

Warsh has also signalled plans to shrink the balance sheet through quantitative tightening, reversing the post-2008 expansion that Powell largely maintained. He opposes central bank digital currency (CBDC) development, framing it as beyond the Fed’s statutory scope.

Investors focused on the fed funds rate may be watching the wrong variable: our deep-dive into Warsh’s balance sheet strategy examines how accelerated quantitative tightening could steepen the yield curve even during a rate-cutting cycle, with specific implications for long-duration Treasuries, REITs, utilities, and investment-grade corporate bonds.

| Policy Area | Powell Approach | Warsh Approach |

|---|---|---|

| Inflation targeting | Flexible average; temporary overshoots permitted | Strict 2% target; no overshoot tolerance |

| Guidance and dot plot | Forward guidance and quarterly dot plot projections | Data-dependent, meeting-by-meeting; dot plot abandoned |

| Balance sheet | Maintained post-2008 expansion; gradual QT | Accelerated balance sheet reduction through QT |

| Mandate scope | Broader interpretation (climate risk, financial stability) | Narrow: price stability and maximum employment only; no CBDC |

Market pricing as of 13 May reflects the transition: approximately 2.3-2.4% probability of a 25 basis point cut at the June FOMC, consistent with near-term steady rates. The removal of forward guidance alone would alter how bond markets price Fed expectations, adding uncertainty premiums to duration risk across portfolios.

All 12 FOMC voting members share equal votes on rate decisions. A Fed Governor is one of those voters, with a 14-year term and influence proportional to the quality of their arguments at the table.

The Chair is different. The role carries a separate 4-year term and a distinct set of powers:

The governor confirmation on 12 May gave Warsh a seat at the table. The chair confirmation expected today would give him control of the meeting.

Powell’s term ends this week. If Warsh is confirmed today, the June 2026 FOMC meeting, approximately six weeks away, would be his first opportunity to chair the committee.

CME FedWatch data as of 13 May shows approximately 97.7% probability of steady rates at that meeting. Cumulative Fed rate hike expectations through April 2027 reached a new peak of approximately 20 basis points on the morning of 13 May. That steady-rate consensus was built under the assumption of Powell-era continuity. Whether it survives first contact with a new chair who favours rules-based tightening is an open question.

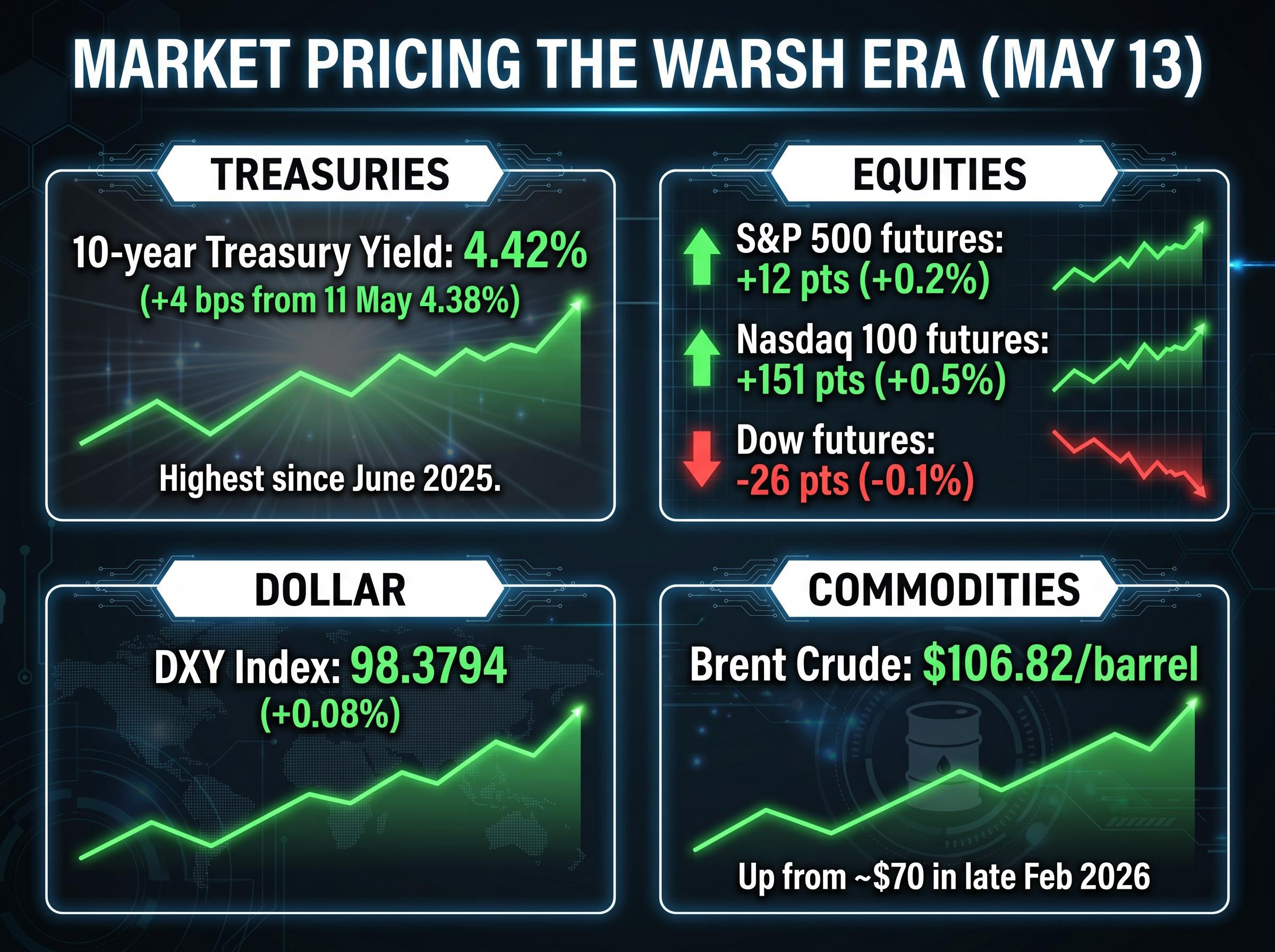

The 10-year Treasury yield at 4.42% on the morning of 13 May, up 4 basis points from the 11 May close of 4.38%, is the clearest market signal. It marks the highest level since June 2025 and reflects bond investors beginning to price in tighter financial conditions under a Warsh-led Fed.

Wolfe Research’s yield decomposition model points to a structural floor on Treasury yields that persists regardless of geopolitical resolution, attributing only 19 of the 40-basis-point surge in the 10-year yield to the Iran conflict shock, with the remaining 21 basis points tied to growth repricing and other factors that a peace deal cannot unwind.

Equities told a more nuanced story. The S&P 500 closed down 0.16% on 12 May. Futures as of 03:33 ET on 13 May were mixed: Dow futures down 26 points (0.1%), S&P 500 futures up 12 points (0.2%), and Nasdaq 100 futures up 151 points (approximately 0.5%). The pattern is consistent with uncertainty about rate trajectory rather than a directional repricing of growth.

The dollar index (DXY) edged up approximately 0.08% to 98.3794, a marginal strengthening consistent with expectations of higher U.S. real rates. Brent crude at $106.82 per barrel, up from roughly $70 pre-conflict in late February 2026, adds an inflation input that compounds the hawkish repricing.

| Asset | Level / Move | What it signals |

|---|---|---|

| 10-year Treasury yield | 4.42% (+4 bps from 11 May) | Hawkish repricing; highest since June 2025 |

| S&P 500 futures | +12 points (+0.2%) | Mixed equity sentiment; no panic, but caution visible |

| Nasdaq 100 futures | +151 points (+0.5%) | Tech resilience amid broader rate uncertainty |

| DXY (U.S. Dollar Index) | 98.3794 (+0.08%) | Marginal dollar strength on higher rate expectations |

| Brent crude | $106.82/barrel | Elevated oil adds inflation pressure to Warsh’s first policy decisions |

Cumulative rate hike expectations through April 2027 reached a new peak of approximately 20 basis points as of 13 May morning, the highest level since Warsh’s nomination was announced.

The combination of rising yields, a firmer dollar, and elevated oil prices reflects a market positioning for a less accommodative Fed. For equity investors, higher rates alongside a rules-based chair with quantitative tightening ambitions present a genuine shift in the discount rate environment.

The central paradox of this appointment is straightforward. Trump nominated Warsh partly out of frustration with Powell’s pace of rate cuts, seeking a Fed chair more amenable to lower borrowing costs. The nominee he chose, however, is a rules-based hawk whose framework could compel rate hikes if inflation persists, the opposite of what the administration sought.

The 51-45 party-line vote made the tension visible. Democrats at the 21 April hearing pressed Warsh repeatedly on Fed independence, reflecting concern that the nomination itself represented political interference. Warsh’s response was unambiguous.

During his confirmation hearing, Warsh emphasised a rules-based, apolitical approach to monetary policy, distinguishing his framework from Powell’s more discretionary style and implicitly distancing himself from the White House’s stated rate preferences.

Analysts have drawn parallels to Paul Volcker’s 1979-era appointment, when a strict inflation-targeting chair accepted short-term economic pain to break stagflation. The comparison is imperfect but instructive: if inflation reaccelerates, driven by oil at $106.82 and elevated consumer price readings, Warsh’s rules-based framework could produce rate hikes that run directly counter to the administration’s growth agenda.

The Federal Reserve History account of Volcker’s 1979 anti-inflation measures documents how the shift to targeting bank reserves drove short-term rates above 20%, produced a sharp recession, and ultimately broke the inflation spiral, establishing the historical benchmark against which rules-based monetary tightening is still measured today.

That gap between what the White House wanted and what a Warsh-led Fed might deliver is the variable that rate-sensitive portfolios will price over the next 12 months.

The accumulated context of the past week, the governor confirmation, the yield move, the hawkish policy framework, converges on a short list of specific signposts:

Rate-sensitive positions, including long-duration bonds and growth equities, face the most direct repricing risk if Warsh’s first FOMC communication signals a tighter-than-priced path.

For investors trying to model portfolio positioning across the remainder of 2026, our full explainer on the 2026 rate outlook examines what the four-way FOMC dissent means for forward guidance reliability, covers why Powell remaining on the Board as a governor complicates the transition, and identifies the specific assets, including long-duration Treasuries, REITs, and utilities, that face the sharpest repricing risk if the rate path shifts.

Kevin Warsh enters the Federal Reserve chairmanship, pending today’s vote, with a documented philosophy that leaves less room for interpretation than most incoming chairs. Strict 2% inflation targeting, scepticism of forward guidance, and a stated preference for balance sheet reduction are not campaign themes; they are operational commitments made under oath at a Senate hearing.

The Volcker comparison circulating among analysts captures the market’s core uncertainty. Volcker broke inflation at the cost of recession. Warsh may not face the same extremity, but his rules-based framework means the Fed’s response function under his leadership will be more mechanically tied to inflation data and less subject to the discretionary judgement that characterised the Powell years.

The June FOMC meeting is the first concrete test. Until then, the yield curve, the dollar, and the Fed funds futures market will price in what the Senate is about to formalise.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding Federal Reserve policy are speculative and subject to change based on economic conditions and institutional decisions.

Kevin Warsh was first appointed to the Fed Board of Governors in 2006 at age 35, making him the youngest Fed Governor in the institution's history. He served through 2011, covering the full arc of the 2008 financial crisis response, and now returns with a philosophy that challenges the policy architecture of the past 15 years.

Warsh favours a strict 2% inflation target with no tolerance for overshoots, abandoning forward guidance and the dot plot in favour of meeting-by-meeting decisions, and accelerating balance sheet reduction through quantitative tightening. This rules-based approach could produce rate hikes if inflation persists, even if the current baseline shows steady rates at the June 2026 FOMC meeting.

A Governor confirmation grants a seat and vote on the Federal Open Market Committee for a 14-year term, while a Chair confirmation grants a separate 4-year term with additional powers including agenda-setting, leading post-meeting press conferences, and serving as the Fed's primary voice before Congress. Warsh's Governor confirmation passed on 12 May 2026; the Chair vote was expected on 13 May 2026.

The 10-year Treasury yield rose to 4.42% on 13 May 2026, up 4 basis points from the prior close and the highest level since June 2025, as bond investors began pricing in tighter financial conditions under a Warsh-led Fed. Cumulative rate hike expectations through April 2027 also reached a new peak of approximately 20 basis points on the same morning.

Investors should watch Warsh's first post-confirmation public statement for signals on the pace of balance sheet reduction and whether the dot plot is removed immediately or phased out, followed closely by the June 2026 FOMC meeting, the next CPI release, and any guidance on the start date and pace of quantitative tightening.