Brent crude closed above $110 per barrel on 30 April 2026, marking a 54% surge since 28 February, the day military conflict with Iran began. That figure has crossed a threshold analysts had previously identified as the point where central banks would be forced to reconsider their policy trajectories. Five months ago, futures markets were pricing roughly 50 basis points of US Federal Reserve rate cuts through 2026. Those cuts have been removed entirely. For the European Central Bank (ECB) and the Bank of England, markets have shifted from pricing easing to pricing hikes. The speed and breadth of this repricing across three major central banks simultaneously represents one of the most consequential shifts in interest rate expectations in recent memory. What follows maps how that repricing is playing out across the Fed, ECB, and Bank of England, what it has done to bond yields globally, and how Morningstar Investment Management’s three fixed income scenarios help investors assess where their portfolios stand.

How a 54% oil price surge rewrote the global rate outlook

The timeline is stark. On 28 February 2026, conflict with Iran began. By early March, Brent crude had crossed $100 per barrel. As of 1 May 2026, prices remain above $110, with Brent closing at $110.61 on 30 April.

- 28 February 2026: conflict begins; oil prices begin climbing

- Early March 2026: Brent crosses $100 per barrel

- 1 May 2026: Brent trading above $110 per barrel

The persistence of these levels reflects the structural nature of the disruption. The International Energy Agency has characterised the Strait of Hormuz situation in terms that leave little room for dismissal.

The IEA Oil Market Report for March 2026 formally characterised the Strait of Hormuz situation as the largest supply disruption in oil market history, providing the analytical basis that has since shaped how central banks and sovereign debt markets have framed their response to the current price environment.

The IEA has described the ongoing Strait of Hormuz disruption as the “largest supply disruption in oil market history.”

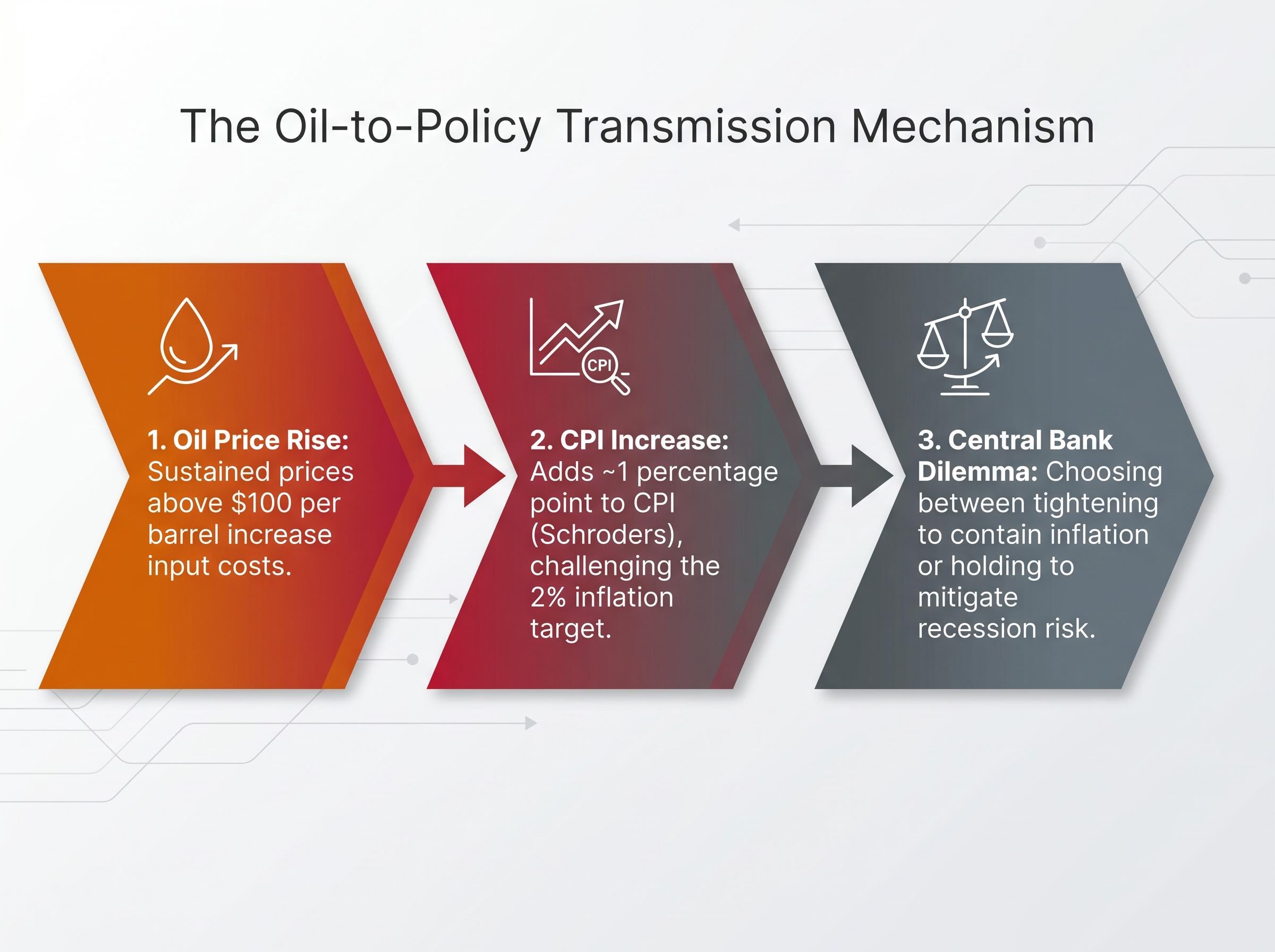

This is not a temporary spike driven by speculative positioning. Sustained oil prices above $100 add approximately 1 percentage point to consumer price index (CPI) readings, according to Schroders analysts. That single percentage point is the mechanism connecting the oil market to every central bank decision that follows. It makes easing difficult to justify politically, analytically, and institutionally, regardless of where policymakers started the year.

The recalibration of global inflation expectations extends beyond rate futures: institutional investors are simultaneously rotating into commodities, high-margin equities, and shorter-duration fixed income, while disinflationary counter-forces such as Chinese manufacturing exports and AI productivity gains create genuine uncertainty about how persistent the current CPI impulse will prove.

When big ASX news breaks, our subscribers know first

The Fed, ECB, and Bank of England: three central banks, one direction

Each of the three largest Western central banks entered 2026 with a different policy stance. Each has arrived at the same constrained position.

The Federal Reserve had 50 basis points of cuts priced into futures markets as recently as December 2025. By the end of Q1 2026, those cuts had been removed entirely. Hike scenarios, previously confined to outlier projections, are now live contingencies in several strategists’ base cases.

The Fed rate trajectory through 2027 now incorporates geopolitical risk premiums that extend well beyond the immediate conflict timeline, with sanctions on energy producers feeding into core domestic inflation metrics and industries from aviation to corporate travel absorbing margin compression that amplifies the case for a prolonged hold.

The ECB held its deposit rate at 2.0% on 19 March 2026. Futures markets now price one to two 25-basis-point hikes through the remainder of 2026. ING’s Carsten Brzeski has indicated that rate cuts are off the table, with hikes becoming more probable under a prolonged disruption scenario. Morningstar economist Grant Slade sees the ECB on hold as the base case, with a conditional late-2026 cut possible only if energy prices recede and the conflict proves short-lived.

The Bank of England has seen its expected easing cycle dismantled. Goldman Sachs now forecasts Bank Rate holding at 3.75% through 2026, revised from prior expectations of quarterly cuts beginning in July.

The convergence is the signal. Three institutions with different mandates, different inflation baselines, and different economic backdrops have all moved in the same direction. That makes this difficult to dismiss as a local anomaly or a temporary adjustment.

| Central Bank | Pre-Conflict Expectation (Dec 2025) | Current Expectation (May 2026) | Direction of Revision |

|---|---|---|---|

| US Federal Reserve | 50bps of cuts priced | Zero cuts priced; hike scenarios live | Hawkish |

| European Central Bank | Further easing expected | Hold at 2.0%; 1-2 hikes priced | Hawkish |

| Bank of England | Quarterly cuts from July 2026 | Hold at 3.75% through 2026 | Hawkish |

What central banks actually do when oil prices rise: the policy transmission explained

The assumption many investors carry is straightforward: oil rises, inflation rises, central banks raise rates. The reality is more conflicted than that.

The transmission chain works in three steps:

- Oil price rise: sustained prices above $100 per barrel feed directly into transport, manufacturing, and energy costs across the economy.

- CPI increase: those higher input costs flow into consumer prices. According to Schroders, oil above $100 adds approximately 1 percentage point to CPI, a material shift for central banks targeting 2% inflation.

- Central bank response: this is where the dilemma emerges. Policymakers must choose between raising rates to contain inflation expectations and holding steady (or even cutting) to support an economy that oil-driven cost pressures are simultaneously weakening.

Schroders analysts caution that central banks are unlikely to match the full extent of market-priced hikes, noting that recession risk remains a countervailing force that could eventually pivot policymakers back toward easing, even while oil remains elevated.

Recession risk sits at the centre of the policy dilemma: Moody’s Analytics places the 12-month US probability at 48.6%, and the four simultaneous transmission channels from reduced consumer disposable income and rising input costs through to investment pullback and Fed rate pressure create a compounding dynamic that supply-side tightening alone cannot resolve.

That tension is the core difficulty. Oil-driven inflation is a supply shock, not a demand shock. Raising rates does not produce more oil. It does, however, slow the broader economy. DWS’ Kastens has highlighted the risk of faster-than-expected tightening if inflation expectations become unanchored, drawing on the 2022 inflation surge as the most recent precedent for how quickly central banks can be forced to act when price pressures prove stickier than expected.

This is the dilemma shaping every rate decision for the remainder of 2026: tighten into a supply shock and risk recession, or hold and risk losing credibility on inflation.

Bond yields in the real world: what the repricing looks like on a screen

The policy uncertainty has already repriced bond markets in measurable terms.

US 10-year Treasury yields peaked at 4.46% on 27 March 2026, the highest level since July 2025, before settling at 4.42% as of 29 April 2026. The 30-year US mortgage rate reached 6.38% on 26 March, illustrating how the repricing transmits directly into real-economy borrowing costs.

In Europe, German 10-year Bund yields sit at approximately 2.5-2.6% in late April 2026, reflecting a market that has absorbed the ECB’s hawkish pivot and priced out the easing trajectory that prevailed at the start of the year.

The sharpest stress, however, sits in emerging market sovereign debt. The EMBI Global Diversified index, which tracks the spread between emerging market bonds and US Treasuries, has widened by approximately 150 basis points since February 2026.

Emerging market sovereign spreads have widened by approximately 150 basis points since the conflict began in February, with Turkey, Egypt, and Pakistan among the most affected.

That spread widening reflects a compounding problem: higher oil prices feed inflation in energy-importing economies, while simultaneously tightening the global financial conditions those economies depend on for refinancing.

The IMF Global Financial Stability Report for April 2026 identified commodity-importing emerging market economies as particularly exposed to the combination of portfolio debt outflows and higher expected monetary policy rates, a dynamic that maps directly onto the spread widening already recorded in Turkey, Egypt, and Pakistan.

| Market | Yield / Spread Level (Late April 2026) | Key Move Since February 2026 |

|---|---|---|

| US 10-Year Treasury | 4.42% | Peaked at 4.46% (27 March); highest since July 2025 |

| German 10-Year Bund | ~2.5-2.6% | Elevated; easing expectations removed |

| EMBI Global Diversified Spread | ~150bps wider | Broad stress across Turkey, Egypt, Pakistan |

Fixed income under pressure: how your bond portfolio holds up across possible oil outcomes

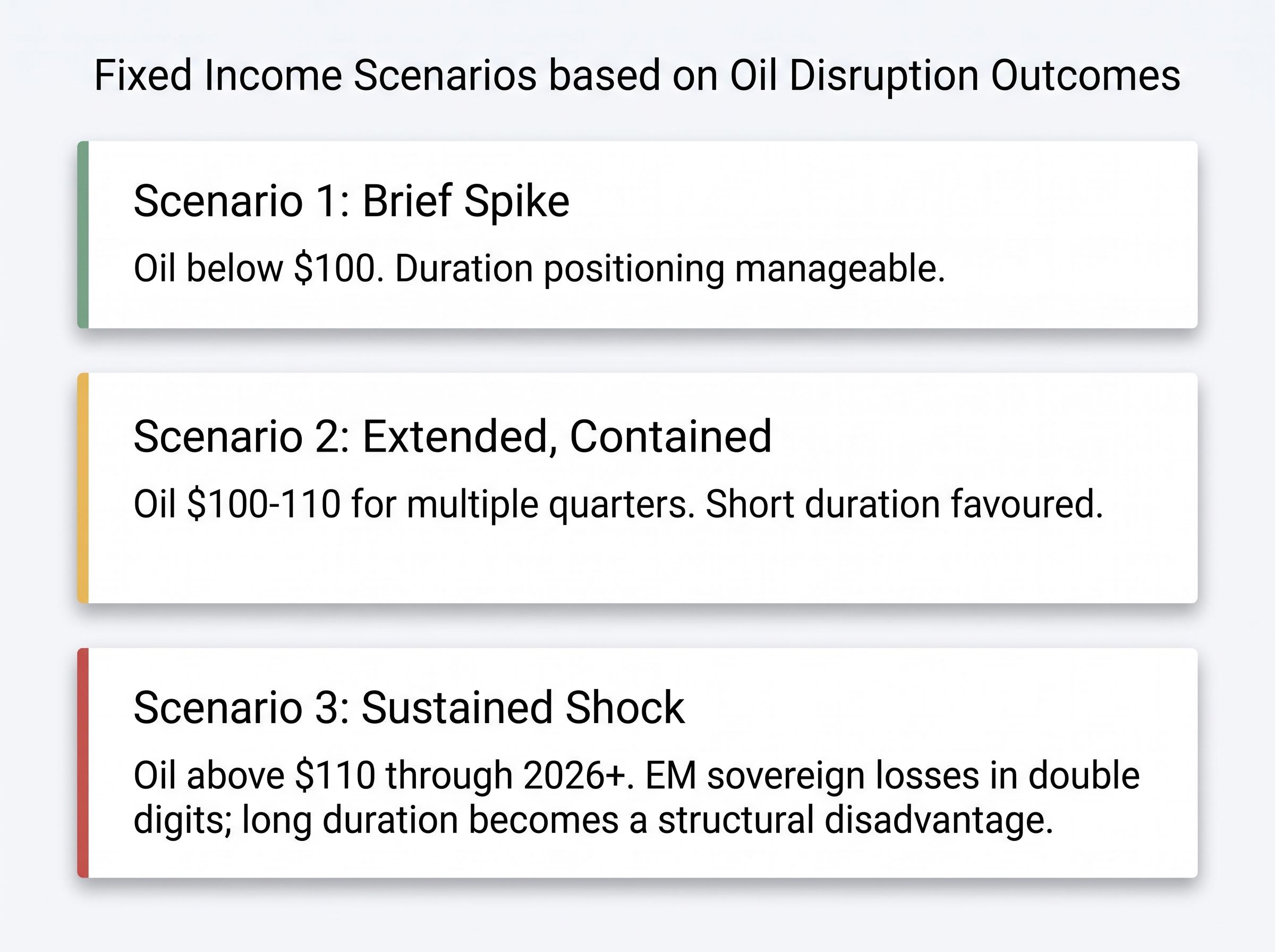

Morningstar Investment Management’s Q1 2026 Markets Observer outlines three scenarios for fixed income investors, each defined by the trajectory of the oil disruption. The range of outcomes is wide, and the asymmetry between the benign and severe cases is worth examining closely.

Scenario 1: brief spike, quick reversal. Oil prices retreat below $100 as the Strait of Hormuz disruption resolves within months. In this case, the yield repricing partially reverses, and existing bond portfolios recover much of their mark-to-market losses. Duration positioning remains broadly manageable.

Scenario 2: extended but partially contained disruption. Oil remains in the $100-110 range for multiple quarters. This is where outcomes begin to diverge sharply. Shorter-duration portfolios absorb the pressure; longer-duration holdings face sustained losses. Credit spreads widen selectively, with energy-importing sovereigns and lower-rated corporates most exposed.

Scenario 3: sustained prolonged shock. Oil remains above $110 for the remainder of 2026 or longer. Longer-duration assets become a structural disadvantage. Credit risk premiums expand broadly. Emerging market sovereign debt faces potential losses in the double-digit percentage range, according to Morningstar’s analysis. The 150 basis points of EMBI spread widening already recorded suggests elements of this scenario are partially in motion.

| Scenario | Oil Price Assumption | Key Fixed Income Impact | Portfolio Implication |

|---|---|---|---|

| 1: Brief spike | Below $100; quick resolution | Yield repricing partially reverses | Duration positioning manageable |

| 2: Extended, contained | $100-110 for multiple quarters | Outcomes diverge by duration and credit quality | Short duration favoured; selective credit stress |

| 3: Sustained shock | Above $110 through 2026+ | Broad credit premium expansion; EM sovereign losses in double digits | Longer duration becomes structural disadvantage |

Morningstar Investment Management recommends that long-horizon investors use periods of elevated volatility to review portfolio composition and rebalance where appropriate, rather than react to short-term disruptions.

Investors wanting to understand why the standard crisis playbook is underperforming in the current environment will find our full explainer on safe haven assets in a supply-shock crisis instructive; it examines why gold, government bonds, and the yen have each declined since the conflict began, which floating-rate instruments have outperformed fixed-rate alternatives, and what the 2022 rate cycle suggests about the recovery trajectory for fixed income once the hiking peak arrives.

The rate rethink is here. Whether it lasts depends on one variable.

The Iran conflict has not simply delayed rate cuts. It has restructured the interest rate expectations landscape across the three most systemically important Western central banks simultaneously. The gradual easing cycle that investors spent 2024 and early 2025 positioning for has been interrupted, and the replacement is not a pause. It is an open question between extended holds and outright hikes.

The variable that determines which of the three Morningstar scenarios ultimately plays out is singular: the duration and severity of the Strait of Hormuz supply disruption. If the blockade resolves, the repricing partially unwinds. If it persists, the dynamics already visible in emerging market spreads and elevated Treasury yields become entrenched features of the fixed income environment.

Schroders analysts caution that recession risk remains a countervailing force to sustained rate hikes, a factor that could eventually pivot central banks back toward easing even while oil remains elevated.

For investors, the actionable conclusion is not prediction. It is preparation. Reviewing portfolio duration, credit exposure, and emerging market weighting against these three scenarios provides a more durable foundation than positioning for any single outcome.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—