With the question self-directed investors face right now is not whether the RBA will cut. It is whether their portfolios are positioned to capture the sectors that have historically moved first and fastest when rates fall.

With the RBA’s May 2026 meeting approaching and the cash rate at 4.10% following two consecutive hikes in February and March 2026, investors who are positioning for a future easing cycle have a narrow window to consider where historical rate cuts have rewarded early movers on the ASX. The 2025 easing cycle, which brought the cash rate to 3.60%, provides the most recent empirical reference point, and the patterns it confirmed echo longer precedents from 2019 to 2020. What follows is a framework mapping the ASX sectors with the strongest historical track records during monetary easing, explaining the mechanics driving each, and offering a practical approach for positioning ahead of confirmed cuts rather than chasing moves after the fact.

Why rate cuts move markets: the mechanics self-directed investors need to understand

Rate cuts benefit equities through multiple pathways, not just cheaper borrowing. The distinction matters because it explains why some sectors respond to a 25bp move with a 2-3% rally while others barely register.

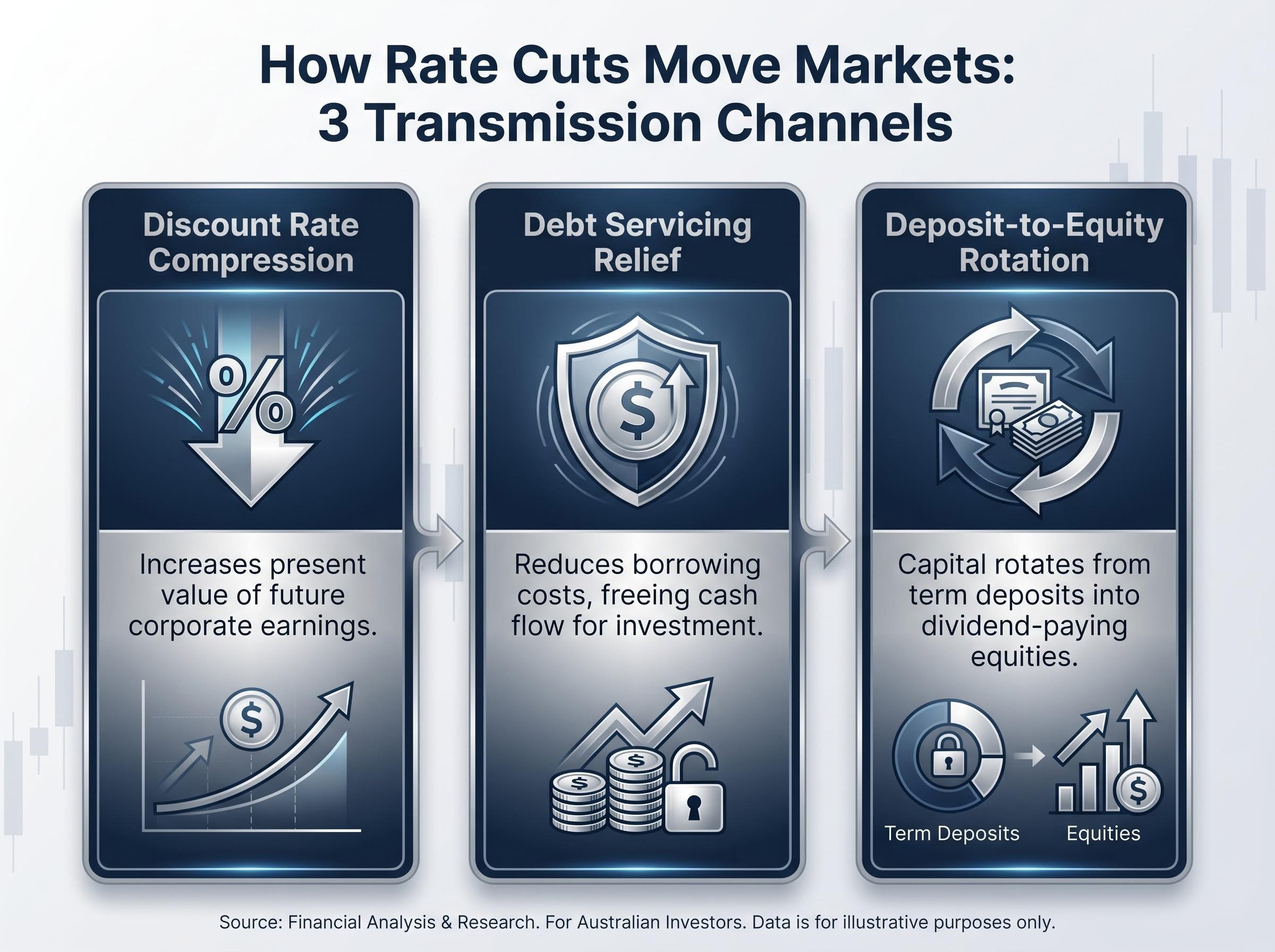

Three transmission channels do the heavy lifting:

- Discount rate compression: When the RBA cuts, the rate used to discount future corporate earnings falls. This mathematically increases the present value of those earnings and lifts equity prices, even before any operational improvement occurs.

- Debt servicing relief: Companies and consumers with variable-rate borrowings see immediate cost reductions, freeing cash flow for investment or spending.

- Deposit-to-equity rotation: As the cash rate falls, term deposit yields decline. Income-seeking investors, particularly retirees and SMSF holders, systematically rotate capital from deposits into dividend-paying equities, creating demand-side price support.

The magnitude of this effect varies by asset duration. Long-duration assets, those whose cash flows are weighted far into the future, experience the largest valuation re-rating from a given rate move. A company expected to generate most of its earnings over the next two years is less sensitive to discount rate changes than one whose value depends on earnings projected a decade out.

The discount rate mechanics that make long-duration assets so sensitive to RBA decisions are the same framework applied in dividend discount modelling, where a 25bp reduction in the required return produces a disproportionately large increase in present value for assets whose cash flows are weighted far into the future, particularly REITs, infrastructure, and ASX utilities with regulated revenue streams.

The dividend yield spread signal: The estimated ASX 200 dividend yield sits at approximately 4.5-5.5%. A cut to 3.60% would meaningfully widen the premium that dividend-paying equities offer over the risk-free cash rate, increasing their relative attractiveness to income-focused capital. This spread is the single most referenced valuation signal in easing-cycle positioning.

Without understanding these mechanics, investors risk acting on the right instinct but targeting the wrong assets.

When big ASX news breaks, our subscribers know first

REITs and infrastructure: the rate-sensitive long-duration plays

REITs and infrastructure occupy the most structurally direct position in a rate-cut thesis. The mechanics from the previous section compound here in ways that make these asset classes the logical starting point for easing-cycle positioning.

REITs: financing costs, cap rates, and yield spread widening

REITs benefit through two simultaneous channels. Lower financing costs reduce the interest expense on property debt, directly improving distributable earnings. At the same time, cap rate compression (the rate used to value commercial property) lifts underlying asset valuations, strengthening balance sheets.

- Lower debt servicing costs improve distribution capacity

- Cap rate compression increases net asset values across the portfolio

- Yield spread widening draws income-seeking capital into the sector

During the 2025 easing cycle, when the RBA cut to approximately 3.60% by August 2025, REITs were among the clearest beneficiaries. ASX-listed names such as Scentre Group (SCG.AX), Goodman Group (GMG.AX), and Dexus (DXS.AX) represent the range of exposures available within the sector. Even in the post-March 2026 tightening environment, real estate showed a relief rally when the 5-4 board split suggested hawkishness was constrained, underscoring the sector’s acute sensitivity to rate signals.

Infrastructure: long-duration cash flows and institutional re-rating

Infrastructure assets generate regulated, inflation-linked cash flows over decades. This makes them among the highest-duration assets on the ASX, with disproportionate sensitivity to discount rate changes.

- Regulated revenue streams provide stability that amplifies during easing

- Long-dated cash flow profiles mean discount rate compression has an outsized valuation effect

- Superannuation funds and institutional investors systematically increase infrastructure allocations when rates fall, adding a demand-driven valuation uplift on top of the fundamental re-rating

Historically, both REITs and infrastructure begin outperforming in the months leading up to confirmed cuts rather than after. Investors who wait for the RBA announcement may find the initial repricing has already occurred.

Technology and growth stocks: the valuation leverage play

High-growth technology companies are often described as the riskiest corner of the ASX. During rate cuts, however, they carry a structural valuation advantage over nearly every other sector. The apparent paradox resolves once the mathematics is visible.

Technology companies derive most of their valuation from earnings projected far into the future. A 25bp reduction in the discount rate applied to those distant cash flows has a proportionally larger effect on present value than the same reduction applied to a mature business generating most of its earnings in the next two to three years.

The duration effect in practice: A business whose value depends on earnings ten years out experiences a materially larger present-value uplift from discount rate compression than one whose cash flows are concentrated in near-term quarters. This is why growth stocks carry the highest beta to rate decisions on either side.

The contrast with the current tightening environment makes the dynamic clearer. After the March 2026 hike, technology was among the most pressured ASX sectors while real estate and financials rallied on constrained hawkishness. The inverse applies when cuts begin.

The contrast with the current tightening environment makes the dynamic clearer. Oil shock repricing across ASX sectors from late April 2026 illustrates how the same channels that amplify rate-cut benefits — including REIT valuations, growth stock multiples, and consumer spending capacity — can run sharply in reverse when an inflationary external shock forces the RBA to tighten rather than ease.

Zip Co (ZIP.AX) offers a contextual reference point. In April 2026, the company’s share price rose 56.8%, alongside a record quarterly EBTDA of $65.1 million (up 41.5% year-on-year) and upgraded FY2026 guidance to a minimum $260 million cash EBTDA. While company-specific recovery dynamics drove much of that move, the broader rate expectation environment shapes the backdrop for such re-ratings.

Three categories of growth stock carry different rate sensitivity profiles:

- Early-stage or unprofitable companies: Highest duration, highest sensitivity to rate moves, highest risk if cuts are delayed

- Profitable but high-growth companies: Strong rate sensitivity with a margin of safety from existing cash generation

- Mature growth companies: Moderate sensitivity, lower volatility, smaller upside from cuts

For investors willing to accept higher volatility, technology and growth stocks represent the highest-leverage expression of an RBA easing thesis.

Dividend stocks and building materials: the income rotation and housing recovery plays

The same rate-cut event that compresses discount rates also triggers a behavioural shift among income-focused investors. As the RBA cuts and term deposit rates decline, capital migrates. Retirees and SMSF holders, in particular, systematically rotate toward high-yield ASX equities when deposit returns fall below acceptable income thresholds.

This deposit-to-equity rotation creates a demand bid for dividend-paying stocks that operates independently of any fundamental valuation improvement. It is a flow-driven dynamic, and it has historically supported prices in high-yield equities during every easing cycle measured.

Building materials occupy a separate but related position. Rate cuts lower mortgage rates, which stimulates housing approvals and construction commencements. This creates direct revenue tailwinds for ASX-listed building materials companies as physical demand for their products increases.

Historical data reinforces the opportunity. Diversified financials have historically averaged +3.4% three-month returns in below-average or declining rate environments, the strongest performing sector across this metric. At a cash rate of 3.60% post-cut, with the ASX 200 dividend yield estimated at approximately 4.5-5.5%, the spread over cash would be materially wider than in the current 4.10% environment.

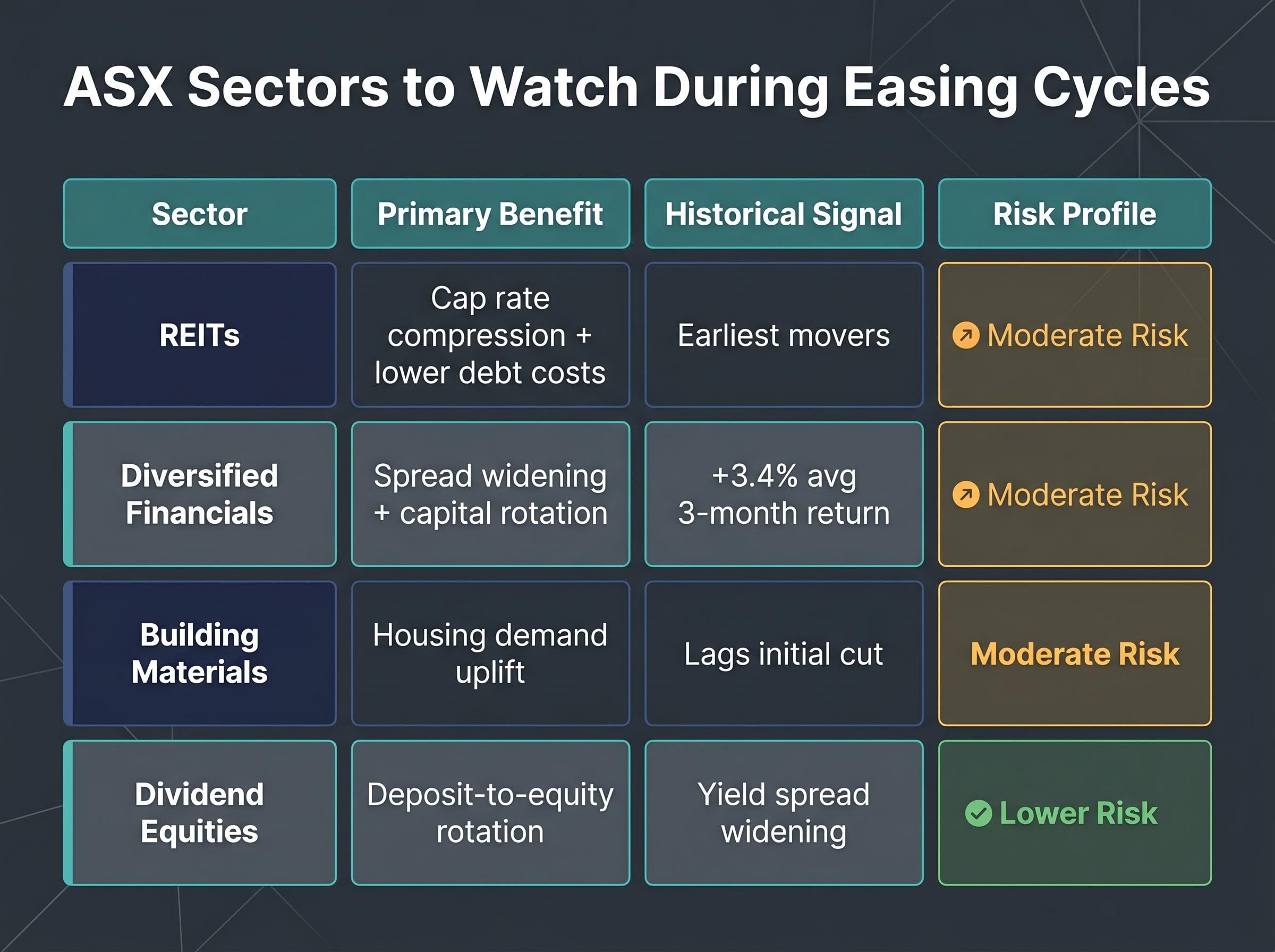

| Sector | Primary rate-cut benefit | Historical performance signal | Risk profile |

|---|---|---|---|

| REITs | Cap rate compression + lower debt costs | Among earliest movers in easing cycles | Moderate; rate reversal risk |

| Diversified Financials | Spread widening + capital rotation | +3.4% average 3-month return in declining rate environments | Moderate |

| Building Materials | Housing construction demand uplift | Lags initial cut; accelerates as approvals rise | Moderate; tied to housing cycle |

| Dividend Equities | Deposit-to-equity rotation demand | Yield spread widening attracts income capital | Lower; income stability |

Dividend stocks and building materials offer a less volatile entry point into the rate-cut thesis than growth stocks, making them particularly relevant for income-focused investors and those with lower risk tolerance.

The one sector to approach with caution: how banks actually respond to cuts

Banks are financials, so they should benefit from rate cuts. The logic seems straightforward, but the mechanics tell a different story. Banks are not straightforward beneficiaries of monetary easing, and understanding why prevents a common portfolio construction error.

Net interest margin compression explained

When the RBA cuts by 25bp, a bank’s lending rates (on mortgages, business loans, and credit facilities) typically fall faster and further than the deposit rates they pay to savers. The spread between what a bank earns on loans and what it pays on deposits, the net interest margin (NIM), compresses.

Two competing forces shape the outcome:

NIM expansion and funding headwinds at regional and mid-tier Australian banks demonstrate the asymmetry in practice: Bendigo Bank’s Q3 FY26 results showed a 6 basis point NIM gain to 1.98% driven by business lending mix shift, yet management simultaneously flagged wholesale funding cost repricing as a constraint on further margin gains — a dynamic that captures exactly why cutting rates does not straightforwardly lift bank profitability.

- NIM compression: The lending spread narrows, reducing per-loan profitability. This is the immediate and mechanically predictable effect of a rate cut on bank earnings.

- Volume growth offset: Lower rates can stimulate new loan demand (more mortgages, more business borrowing), partially compensating for the thinner margin on each loan over time.

The net result is genuinely mixed rather than clearly negative. But in the short term, margin compression tends to dominate, creating a headwind that other rate-sensitive sectors do not face.

What this means for ASX bank stock positioning

For investors holding Commonwealth Bank (CBA.AX) or Westpac (WBC.AX), the two major banks most commonly held directly by ASX retail investors, cuts may create short-term relative underperformance compared to REITs and growth names. Broker consensus in early 2026 favoured bank stocks for rate-resilience in a tightening environment, which suggests the sector loses that relative advantage when cuts begin.

The RBA’s March 2026 monetary policy decision confirmed the cash rate increase to 4.10% on a narrow 5-4 board split, with the majority citing a pick-up in inflation as the basis for tightening — a decision that directly shapes the easing-cycle positioning framework relevant to the May 2026 meeting.

The practical distinction matters: diversified financials historically averaged +3.4% three-month returns in declining rate environments, while banks face the NIM headwind that diversified financials do not share. Treating all financials as equivalent beneficiaries of rate cuts is the error this distinction is designed to prevent.

Volume-driven recovery can follow if the cut cycle stimulates broader credit demand, but patient positioning and realistic return expectations are warranted.

Positioning ahead of the cut: a practical framework for ASX investors

The sector analysis across this guide points to a positioning hierarchy. Long-duration assets (REITs, infrastructure) sit at the top as the most direct and historically consistent easing-cycle beneficiaries. Growth and technology stocks follow for higher-risk-tolerance investors. Dividend equities serve income-oriented portfolios. Banks require nuanced handling.

The timing principle: Rate-sensitive sectors begin repricing when cuts are anticipated, not when they are confirmed. Historical easing cycles show that investors waiting for the RBA announcement may be late to the initial move.

A sequenced framework for the self-directed investor:

- Assess current rate-sensitive exposure. Review existing portfolio weightings across REITs, infrastructure, growth, and bank holdings to identify gaps or overconcentrations before acting.

- Prioritise REITs and infrastructure for initial positioning. These sectors have the most direct mechanical link to rate cuts and the strongest historical track record during easing cycles.

- Evaluate growth and technology allocation relative to risk tolerance. Higher-duration equities carry larger upside from cuts but greater downside if cuts are delayed or reversed.

- Review bank and dividend stock positioning for rotation implications. Consider whether bank holdings are serving a rate-resilience thesis that may weaken in an easing environment, and whether dividend equities offer a better risk-adjusted income alternative.

The 2025 easing cycle, which brought the cash rate to 3.60%, serves as the most recent precedent. But the subsequent shift to tightening in 2026 (with the March hike decided on a narrow 5-4 board split) demonstrates that easing cycles can be shorter than anticipated. Portfolio construction should account for the possibility that cuts may be paused or reversed, rather than assuming a linear easing path.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The window for cut-cycle positioning is shorter than most investors expect

The sectors best positioned to benefit from RBA rate cuts are identifiable in advance. Historical evidence from the 2019-2020 and 2025 easing cycles points consistently to REITs, infrastructure, diversified financials, and growth stocks as the primary beneficiaries. The mechanics driving each are distinct, but the common thread is duration sensitivity: the longer the cash flow profile, the larger the valuation response to a falling discount rate.

The 2025-to-2026 policy reversal, cuts followed by hikes, is a reminder that easing cycles can be shorter than investors anticipate. Disciplined positioning and exit awareness are as important as entry timing.

For investors wanting to understand how the current inflationary backdrop interacts with sector-level positioning more broadly, our full explainer on ASX sector rotation during oil shocks examines the specific performance dynamics across energy, transport, mining, financials, and rate-sensitive sectors — including the conditional nature of energy sector outperformance and the RBA inflation trajectory that determines when and whether a rate-cut cycle can resume.

Individual stock selection within each sector category requires assessing balance sheet quality, earnings trajectory, and valuation rather than relying solely on sector-level tailwinds. Investors may benefit from reviewing their current ASX portfolio allocation against the framework outlined in this guide before the May 2026 RBA decision is announced.