What JEPI Actually Is and Whether It Fits Your Portfolio

4 hrs ago

Most retail investors hear “leveraged ETF” and picture the bold-fonted warnings on 2x or 3x product fact sheets: short-term trading instruments, daily reset mechanics, and the implicit message that these are not for buy-and-hold portfolios. But a quieter category of funds has been growing alongside those products, embedding just 25-50% additional exposure directly into the fund structure and asking nothing more of the investor than a single ETF purchase. The rise of these modestly leveraged products, from issuers such as Global X Canada and NEOS/Tap Alpha, represents a genuinely distinct design philosophy rather than a toned-down version of aggressive leveraged trading tools. Conflating the two categories leads investors to apply the wrong framework when assessing suitability, risk, and holding period. What follows unpacks how modest embedded leverage differs mechanically from daily-reset products, why the reset period is the structural fault line that matters most, and what the specific Canadian and US-listed products in this space actually look like in practice.

The warning label on a daily-reset leveraged ETF is not regulatory boilerplate for its own sake. It exists because the fund’s mathematics are anchored to a 24-hour window. Every trading day, the fund rebalances its derivative or swap exposure at market close to restore its stated leverage multiple. A 2x S&P 500 ETF that finishes Tuesday at 1.97x exposure will trade derivatives at the close to bring that ratio back to 2.0x before Wednesday’s open.

This daily recalibration creates path dependency. The sequence of daily returns, not merely the start and end price of the underlying index, determines what the investor actually earns over any multi-day period. Three consequences follow:

The mechanical explanation for the erosion sits in a well-established financial mathematics identity:

Geometric mean = Arithmetic mean minus (Standard Deviation squared divided by 2)

This formula captures why higher volatility, at any given average return level, reduces the compounded outcome. At 2x or 3x leverage, the standard deviation term scales aggressively, and the drag compounds with it.

The mechanics of volatility drag in leveraged ETF mathematics have been formalised in financial analysis that confirms the geometric mean penalty scales with the square of standard deviation, meaning higher-volatility underlyings impose a disproportionately larger compounding toll on daily-reset products than lower-volatility ones.

In sustained directional trends, daily compounding works in the investor’s favour and can produce returns exceeding the stated multiple over multi-day stretches. These are not broken instruments. They are instruments calibrated to a specific holding window.

Discussions of 2x MSTR ETFs in 2025 illustrated the drag mechanics sharply: volatility in the underlying asset produced leveraged fund losses that significantly lagged what a simple 2x calculation on the period return would have suggested. The underlying’s high annualised volatility meant the standard deviation penalty in the formula above extracted a large toll on compounded returns. Daily-reset leveraged ETFs remain widely characterised as instruments for traders rather than long-term holders, and the mechanical reason is this compounding structure.

Retail leverage losses across derivative instruments follow a well-documented pattern: a 5% adverse price move on a 5:1 leveraged position produces a 25% loss on deployed capital, a compounding arithmetic that daily-reset products at 2x or 3x magnify further through the standard deviation penalty described above.

The products covered in the remainder of this article sit in a structurally different category. Modest embedded leverage, working within a 25-50% range, is not a lesser version of a 3x daily-reset fund. It is a product built around a fundamentally different investor use case.

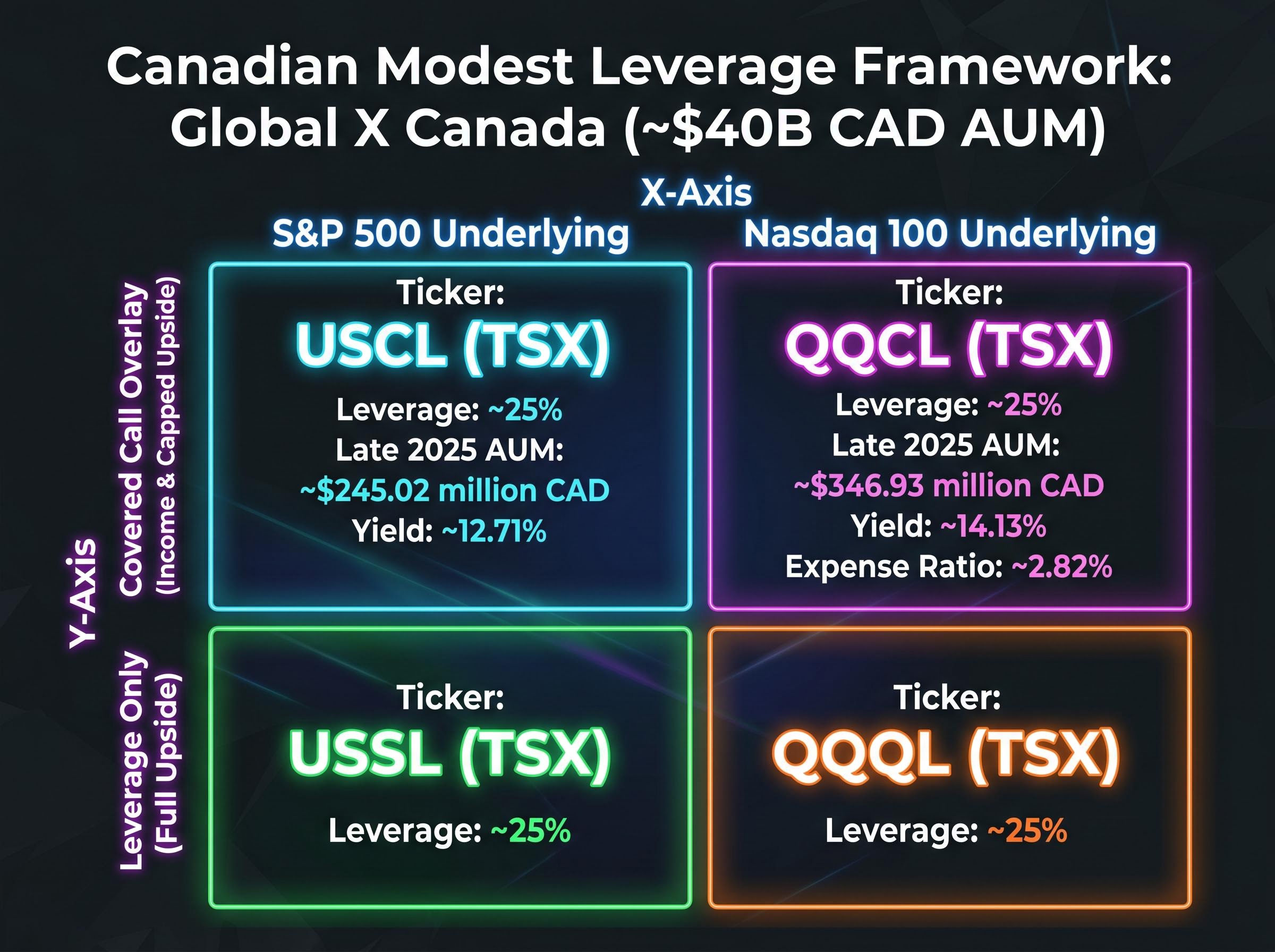

At the fund level, borrowing or derivative exposure is embedded by the asset manager. The investor holds a single ETF unit and never manages margin, faces no margin calls, and is not required to monitor leverage ratios. The delegation is complete. Institutional fund managers, by virtue of scale, typically access borrowing at more favourable terms than retail investors could obtain directly. Global X Canada, managing approximately $40 billion CAD in assets, negotiates borrowing rates that reflect that scale.

The structural investor-facing differences from self-directed margin borrowing are direct:

The contrast with margin lending mechanics matters here: self-directed borrowing exposes investors to margin calls triggered mechanically when falling asset values push the loan-to-value ratio above the lender’s threshold, a forced-sale risk that embedded leverage structures specifically eliminate by design.

The following table maps the four featured Canadian products against their structural characteristics:

| Ticker | Underlying index | Leverage level | Covered call overlay | Listed exchange |

|---|---|---|---|---|

| USCL | S&P 500 | ~25% | Yes | TSX |

| QQCL | Nasdaq 100 | ~25% | Yes | TSX |

| USSL | S&P 500 | ~25% | No | TSX |

| QQQL | Nasdaq 100 | ~25% | No | TSX |

On the US side, XSPI and XQQI (from NEOS/Tap Alpha) use approximately 50% leverage relative to their SPY and QQQ counterparts, with XQQI having launched as recently as February 2026. The Bank of Canada held its policy rate at 2.75% as of April 2025, providing the borrowing cost backdrop for the Canadian fund structures.

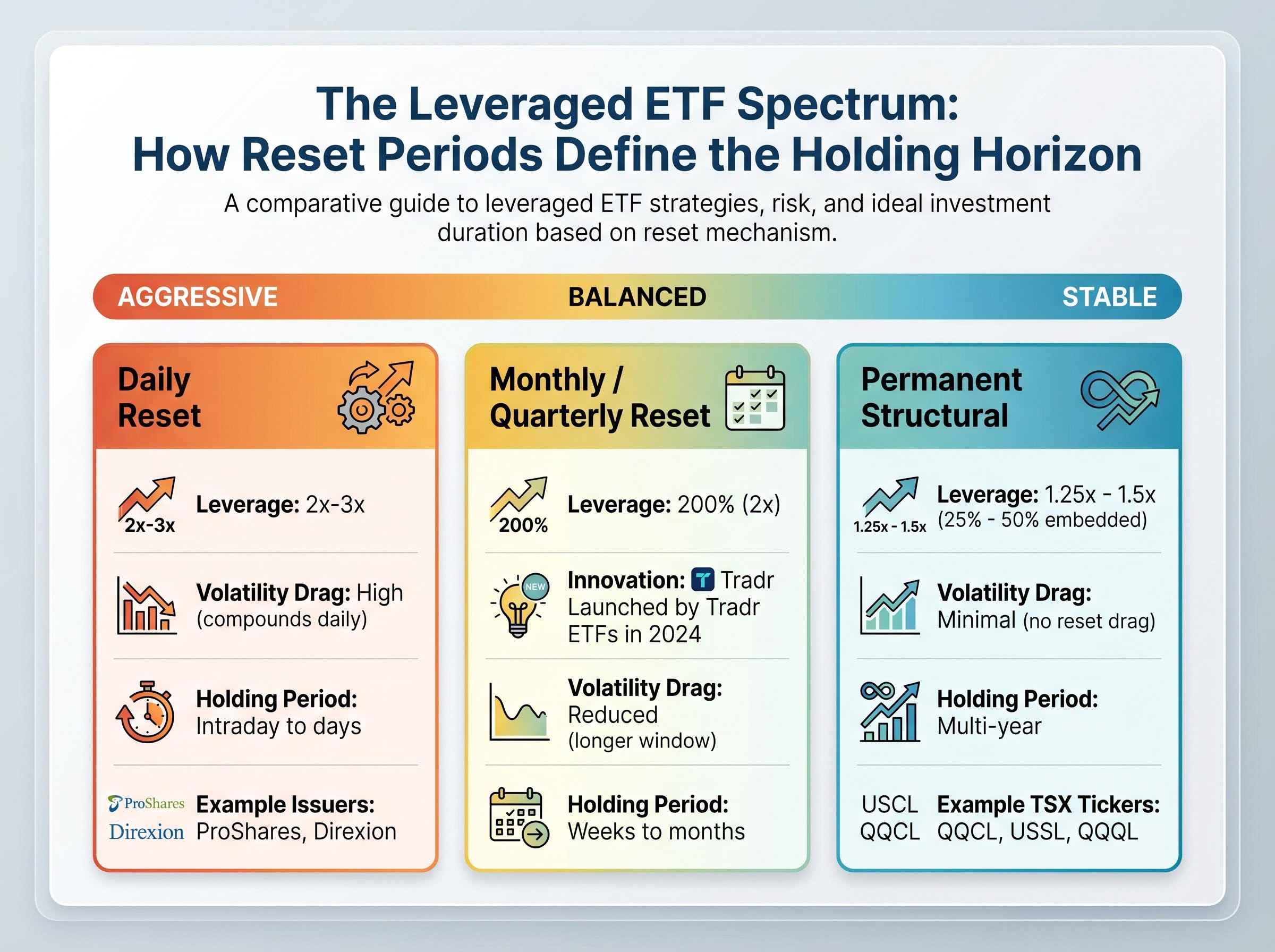

Reset period is not a technical footnote. It is the variable that determines the time window over which a fund’s leverage mathematics operate, and therefore the appropriate investor holding horizon.

Daily-reset products recalibrate every 24 hours, locking their compounding arithmetic into that window. Tradr ETFs introduced a structural innovation in 2024 by launching the world’s first monthly and quarterly reset leveraged ETFs, targeting 200% leverage using total return swaps but extending the compounding window to reduce the volatility drag that daily resets impose. These products still target 2x exposure, but the longer reset interval means the standard deviation penalty accumulates over a month or quarter rather than every single day.

Modest embedded leverage products (25-50%) sit further along this spectrum. They do not have a reset period in the daily-reset sense at all. The leverage is a standing structural feature, not a periodic recalibration toward a stated multiple.

The holding period principle: Matching a leveraged product’s reset period to the investor’s intended holding horizon is the single most consequential suitability decision in this category.

The table below maps reset type against its practical implications:

| Reset type | Typical leverage | Volatility drag exposure | Suitable holding period | Example products |

|---|---|---|---|---|

| Daily | 2x-3x | High (compounds daily) | Intraday to days | ProShares, Direxion 2x/3x |

| Monthly / Quarterly | 2x | Reduced (longer window) | Weeks to months | Tradr ETFs |

| Permanent structural | 1.25x-1.5x | Minimal (no reset drag) | Multi-year | USCL, QQCL, USSL, QQQL |

Regulatory attention is currently concentrated on the high-leverage end. In December 2025, the SEC halted reviews of highly leveraged ETF proposals on risk exposure grounds. Modest leverage structures have not attracted equivalent scrutiny.

Covered call strategies generate premium income by selling call options on the underlying holdings. The trade-off is straightforward: the fund collects options premium, which reduces portfolio volatility, in exchange for capping upside participation above the strike price.

In the modestly leveraged product lineup, this overlay is not incidental. It is the balancing mechanism. The volatility-dampening effect of covered calls is calibrated to approximately offset the volatility-amplifying effect of 25% leverage, targeting a net risk profile comparable to unlevered index ownership.

Covered call strategies structurally surrender upside participation in rising markets, the periods that tend to drive the largest proportion of long-term equity returns, which is why the net risk calibration argument for USCL and QQCL depends on the premium income offsetting that opportunity cost across a full market cycle rather than only in range-bound conditions.

Two distinct product pairs illustrate the design:

USCL held AUM of approximately $245.02 million CAD as of late 2025, while QQCL reached approximately $346.93 million CAD over the same period. The US Fed funds rate, held at 4.25-4.50% as of May 2025, provides relevant context for the cost of options-based leverage in US-listed products such as XSPI and XQQI.

QQCL carried a total expense ratio of approximately 2.82% and a distribution yield of approximately 14.13%. USCL delivered a distribution yield of approximately 12.71%. These figures reflect a combination of options premium income and leverage-enhanced return potential, not an unsustainably high income yield in the traditional fixed income sense.

Distribution frequency varies by product (weekly, biweekly, or monthly). Income-reinvesting investors are less exposed to short-term price volatility because they are not required to sell units to access returns. For income-focused investors evaluating yield against risk, understanding that the 12-14% distribution yields carry an options income component, rather than representing pure leverage risk compensation, reframes the apparent yield-to-risk relationship.

Over the approximately 20-month window from June 2024 through late February 2026, the early return data for these products tells a directionally encouraging but necessarily incomplete story.

USSL outperformed VFV (unlevered S&P 500) over the measured period. USCL outperformed USCC and matched or exceeded VFV. Both QQQL and QQCL delivered higher total returns than their non-leveraged equivalents. The following table summarises the directional comparisons:

| Product | Benchmark | Approx. leverage | Period return (directional) | Covered call overlay |

|---|---|---|---|---|

| USSL | VFV (S&P 500) | ~1.25x | Outperformed benchmark | No |

| USCL | USCC / VFV | ~1.25x | Outperformed USCC; matched/exceeded VFV | Yes |

| QQQL | Non-leveraged Nasdaq 100 | ~1.25x | Outperformed benchmark | No |

| QQCL | Non-leveraged Nasdaq 100 | ~1.25x | Outperformed benchmark | Yes |

Figures are directional based on presenter analysis over the June 2024 to February 2026 window. On the US-listed side, XQQI launched in February 2026 and has no performance record. Verifiable XSPI data for mid-2025 was not available.

The borrowing cost spread: With estimated fund borrowing costs of approximately 3.5-4% against the S&P 500’s historical average annual return of approximately 10-12%, the structural case for modest leverage rests on that spread remaining positive over a full market cycle.

Product proponents view QQQL as likely to rank highest among Nasdaq-tracking options over a complete cycle. Twenty months of data, however, is insufficient to test that thesis against a full range of conditions, including sustained downturns. In January 2026, FINRA fined a broker-dealer for inadequate supervision of leveraged ETF recommendations, reflecting increasing regulatory scrutiny of distribution practices across the broader category.

Long-term compounding at the S&P 500’s historical average of approximately 9-10% annually is the return base against which the borrowing cost spread for these products must be evaluated: a fund borrowing at 3.5-4% to amplify exposure to an index returning 10-12% historically is making a structural bet that the spread remains positive across a complete multi-year cycle, including sustained drawdown periods.

The distinction bears restating in its sharpest form. Daily-reset 2x and 3x products are tactical amplification tools with time-bound mathematics. Modestly leveraged products are structural enhancement features designed for investors who hold a long-term equity growth view and want a permanently embedded boost without managing leverage themselves.

The core distinction: Modest embedded leverage is a permanent structural feature of the fund. Daily-reset leverage is a tactical tool calibrated to a 24-hour compounding window. The two share a label but not a design philosophy.

The regulatory trajectory reinforces the separation. The SEC’s December 2025 halt on highly leveraged ETF reviews, FINRA’s January 2026 enforcement action for broker-dealer supervisory failures, and JPMorgan’s October 2025 commentary that leveraged ETFs exacerbated market sell-offs all target the high-leverage end of the spectrum. No equivalent regulatory events have focused specifically on modest leverage structures.

The SEC halt on high-leverage ETF reviews in December 2025 reflected specific concerns about systemic risk exposure at the high end of the leverage spectrum, a distinction that regulators have drawn carefully and that leaves modestly leveraged structures outside the immediate scope of that scrutiny.

For any modestly leveraged product, three questions form the suitability test:

These products suit long-horizon investors who are not dependent on near-term liquidation of positions and who understand that the leverage label requires reading the fine print on reset period, leverage magnitude, and any derivative overlays before assuming similarity to 2x or 3x products.

The phrase “leveraged ETF” now spans products designed for day traders and products designed for decade-long income investors. The differences between them are structural and mathematical, not merely a matter of degree. Reset period, leverage magnitude, and overlay strategy are the three variables that determine which framework applies.

As more modestly leveraged products launch in both Canada and the US, the vocabulary for distinguishing these categories from tactical leveraged tools will become increasingly important for retail investors and their advisors. Applying a single risk framework to everything carrying the leveraged ETF label is, at this point, a category error.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A modestly leveraged ETF embeds 25-50% additional exposure directly into the fund structure as a permanent feature, whereas 2x and 3x leveraged ETFs reset their leverage ratio daily, creating volatility drag and path dependency that makes them unsuitable for long-term holding.

Volatility drag is the compounding erosion of returns caused by amplified gains and losses in a daily-reset leveraged ETF; mathematically, the geometric mean of returns falls as standard deviation rises, meaning higher-volatility underlyings impose a disproportionately larger penalty on daily-reset products over time.

Covered call overlays generate options premium income that dampens portfolio volatility, and in products like USCL and QQCL this dampening effect is calibrated to approximately offset the volatility-amplifying effect of 25% leverage, targeting a net risk profile comparable to unlevered index ownership.

Yes, these products are designed for long-horizon investors who hold a multi-year equity growth view and want permanently embedded leverage without managing margin, margin calls, or leverage ratios themselves; the suitability case depends on the borrowing cost spread remaining positive across a full market cycle.

In December 2025, the SEC halted reviews of highly leveraged ETF proposals on risk exposure grounds, though this scrutiny was directed at the high-leverage end of the spectrum and has not extended specifically to modestly leveraged structures in the 25-50% range.