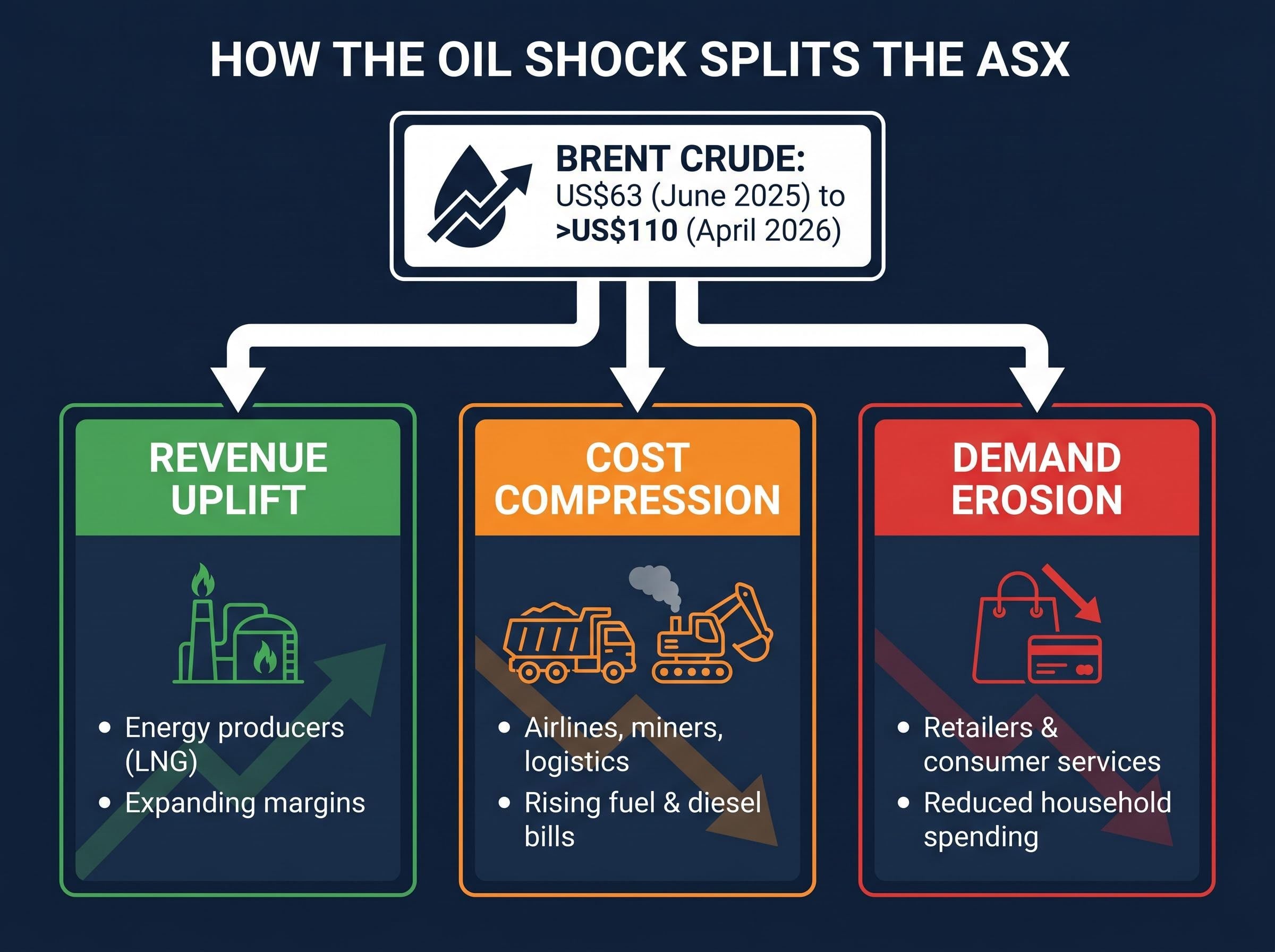

Brent crude surging past US$100 per barrel does not simply raise petrol prices. It reconfigures which ASX sectors investors should own and which they should avoid, sometimes within a single trading session. The 2026 oil shock, driven by escalating Iran conflict and OPEC supply discipline, pushed Brent toward US$110 per barrel and exposed deep fault lines across Australian equities. Woodside Energy climbed roughly 40% year-to-date while airlines absorbed fuel bills inflating by hundreds of millions of dollars. The same macro event produced opposite outcomes.

This analysis maps the transmission mechanism from crude oil prices to ASX sector performance, using real company data from the 2026 oil rally period. It concludes with a concrete rotation framework for Australian investors managing portfolio exposure during elevated oil price environments.

Why an oil price spike hits Australian equities unevenly

Crude oil is not a single-channel input. It functions as a revenue driver for producers, a cost input for airlines and miners, and a demand suppressant for consumer discretionary businesses through the household petrol bill. When Brent moved from US$63 in early June 2025 to above US$110 per barrel by late April 2026, these three channels activated simultaneously, splitting the ASX into winners and losers along structural lines.

The three distinct channels through which oil prices affect ASX sectors are:

- Revenue uplift: Energy producers receive higher prices for every barrel or LNG cargo sold, directly expanding margins.

- Cost compression: Airlines, miners, and logistics operators face rising fuel and diesel bills that squeeze operating margins from below.

- Demand erosion: Higher petrol prices reduce household discretionary spending capacity, pulling revenue from retailers and consumer services companies.

The ASX 200, trading in the range of approximately 8,600-8,800 points in late April 2026 with a market capitalisation of approximately A$3.15 trillion as of March 2026, demonstrated this bifurcation in real time. Documented single-session moves included a 1.1% decline on one occasion and gains of up to 2.67% on others amid Iran conflict volatility. The direction of the move depended almost entirely on which channel dominated sentiment that day.

Peer-reviewed research on oil price impacts on Australian equities, published in Studies in Economics and Finance, provides empirical confirmation that commodity-exporting economies like Australia experience asymmetric sector responses to crude price shocks, with resource company returns and broader equity market returns diverging in ways that align with the transmission channels outlined above.

The LNG pricing link

Australia’s large-scale LNG export contracts commonly use oil-indexed pricing formulas. This means producers such as Woodside and Santos capture revenue uplifts that exceed what a domestic fuel price movement alone would imply. When Brent rises, Australian LNG export revenues rise in parallel, amplifying producer gains relative to international peers without oil-linked contract structures.

When big ASX news breaks, our subscribers know first

Why miners occupy an ambiguous position during an oil shock

The instinct to group miners with energy producers as “commodity winners” during an oil spike misreads the operating model. Miners are commodity producers, but they are also heavy diesel consumers. An oil shock raises their operating costs without necessarily lifting the iron ore or copper prices that drive their revenues.

The structural contrast between energy producers and miners during a high-oil environment:

- Energy producers receive higher prices for their output (oil, LNG) while their input costs rise modestly. Net margin expands.

- Miners face higher diesel and freight costs while their output prices (iron ore, copper) are driven by separate demand dynamics. Net margin compresses or holds flat.

BHP gained approximately 49% over the 2025-2026 period into late April 2026. Rio Tinto delivered approximately 72.4% overall, but absorbed a sharp 15% correction in March 2026. Fortescue maintained record shipments through the period. These strong annual numbers reflect broader commodity cycle factors, including Chinese demand and supply dynamics, rather than oil price tailwinds.

Why iron ore prices don’t move with crude

Iron ore pricing is driven by Chinese steel demand and supply-side dynamics in major producing regions. There is no oil-indexed pricing mechanism for iron ore equivalent to what exists for LNG. When crude rises, iron ore does not follow. Miners therefore miss the revenue tailwind that energy producers capture, while absorbing the full cost impact of higher diesel and transport expenses.

During risk-off sessions driven by oil-related inflation fears, the materials sector experienced notable losses alongside the broader market. Energy producers held up. That divergence in session-level behaviour reveals the structural difference investors need to respect when allocating across commodity sectors.

How ASX energy producers capture outsized gains in an oil rally

The performance numbers tell the story before the explanation does. Woodside Energy (WDS) gained approximately 40% in 2026, with a 24% rise in the 30-day period around the oil spike. Karoon Energy (KAR) matched that trajectory, up approximately 40% year-to-date into late April 2026. Santos (STO) delivered positive performance driven by strong Q1 production results alongside the price escalation.

| Stock | Ticker | 2026 YTD Performance | Key Driver |

|---|---|---|---|

| Woodside Energy | WDS | ~40% gain | Oil-indexed LNG revenue, integrated operations |

| Karoon Energy | KAR | ~40% gain | Pure-play oil and gas exposure, operational leverage |

| Santos | STO | Positive | Strong Q1 production, oil price escalation |

These gains were not uniform in character. Integrated majors like Woodside and Santos offer diversified production profiles and balance sheet resilience. Smaller pure-play producers like Karoon carry higher operational leverage, meaning their earnings respond more aggressively to price movements in both directions.

Energy analyst Saul Kavonic, cited in the Australian Financial Review in June 2025, noted that smaller producers such as Beach Energy gain from operational leverage during oil price surges but carry higher volatility. The observation provides a risk-calibration framework: within the energy allocation itself, position sizing should reflect the difference between large-cap stability and small-cap leverage.

How oil shocks transmit into inflation and RBA policy risk

The damage from a sustained oil shock extends well beyond the companies that burn fuel. Crude prices flow into freight costs, manufacturing inputs, and agricultural production expenses. Those costs then pass through to consumer prices broadly, building inflationary pressure that forces a central bank response. For ASX investors, the sequence matters as much as any individual earnings report.

The transmission chain runs in a specific order:

- Crude oil prices rise, increasing the cost of fuel and petrochemical inputs.

- Freight and manufacturing input costs climb, raising the cost of goods across the economy.

- Consumer prices absorb the pass-through, pushing headline inflation higher.

- The RBA responds with tighter monetary policy or explicit tightening guidance.

- Higher rates compress equity valuations, particularly for growth and capital-heavy sectors.

The distinction between headline versus underlying inflation matters here: Australia’s trimmed mean sat at 3.3% even as headline CPI reached 4.6%, because underlying measures strip out volatile fuel components that are precisely what an oil shock amplifies most aggressively.

The RBA’s documented response to the 2026 oil shock traced this sequence closely. Trimmed mean inflation stood at 2.7% as of August 2025, within the 2-3% target band. By November, the RBA’s Statement on Monetary Policy projected headline inflation rising to approximately 3.7% by mid-2026. As the oil shock persisted, the RBA warned that sustained high prices could drive inflation above 5%, with rate commentary citing potential rises toward 4.85%.

Stagflation risk and what it means for equity multiples

By March 2026, RBA communications explicitly flagged stagflation risk: elevated inflation running concurrent with slowing economic growth. This combination is particularly corrosive for equity valuations. Rate hikes compress the multiples investors are willing to pay, while slowing growth reduces the earnings those multiples are applied to. For rate-sensitive sectors such as REITs and high-growth technology names, the double pressure can be severe.

The precise mechanics of stagflation risk for equity multiples involve the Taylor Rule, GDP contraction modelling, and the historical precedent of 1970s supply shock cycles, all of which suggest the RBA’s rate response may peak earlier than current market pricing reflects, with meaningful implications for rate-sensitive ASX sectors.

Airlines and consumer discretionary: where the losses accumulate

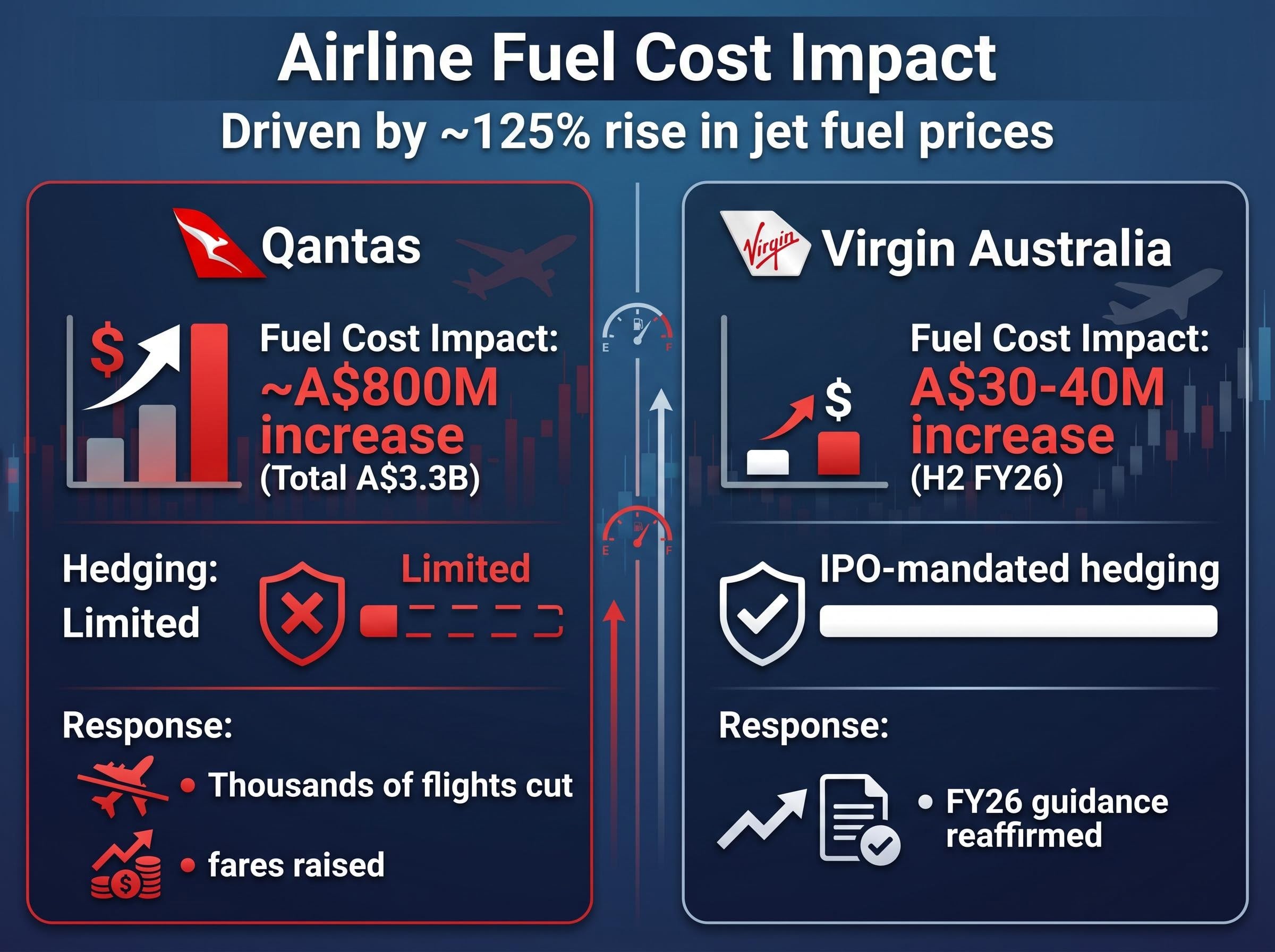

Qantas provides the clearest case study of how an oil shock translates into operating pain. The airline’s fuel bill rose by approximately A$800 million to reach A$3.3 billion in the second half of the financial year. Jet fuel accounts for roughly 20% of Qantas’s total operating expenses, and with jet fuel prices rising approximately 125% from the start of the Iran conflict, the cost pressure was immediate and material.

Jet fuel prices rose approximately 125% from the start of the Iran conflict, turning fuel from a manageable operating cost into the single largest earnings headwind for Australian carriers.

Qantas responded by cutting thousands of flights and implementing airfare increases. The response mitigated part of the margin damage but simultaneously reduced capacity, limiting revenue recovery.

Virgin Australia faced a smaller but still material fuel cost increase of A$30-40 million in H2 FY26. IPO-mandated hedging arrangements partially cushioned the impact, and Virgin reaffirmed its FY26 guidance despite the headwinds. The comparison illustrates how hedging and corporate structure create performance dispersion even within the same sector.

For investors wanting the full picture on how Qantas is managing this cost pressure operationally, our dedicated guide to Qantas’s fuel cost response covers the crack spread mechanics driving the fuel bill above $3.3 billion, the share buyback pause, the specific capacity reallocation between domestic and international routes, and the status of FY27 guidance.

| Airline | Fuel Cost Impact | Hedging Status | Management Response |

|---|---|---|---|

| Qantas | ~A$800M increase to A$3.3B | Limited hedging disclosed | Thousands of flights cut, fares raised |

| Virgin Australia | A$30-40M increase in H2 FY26 | IPO-mandated hedging in place | FY26 guidance reaffirmed, fares adjusted |

The earnings pressure extends beyond aviation. Higher petrol prices erode household purchasing power, reducing the spending pool available for non-essential retail and discretionary services. ASX-listed consumer stocks absorb this demand destruction indirectly, compounding the sector’s vulnerability during a sustained oil price environment.

The ABS fuel price history confirms that the March 2026 spike was directly attributable to the Middle East conflict, with automotive fuel carrying sufficient weight in the Consumer Price Index to translate pump price movements into measurable headline inflation shifts affecting household budgets across Australia.

Repositioning the ASX portfolio when oil prices surge: a practical rotation framework

The sector analysis above points to a specific rotation logic. Capital should move toward sectors with oil-linked revenue uplift and away from sectors facing cost compression or demand destruction. The following framework translates that analysis into a prioritised action list:

- Increase energy producer allocation. Woodside (WDS), Santos (STO), and Karoon (KAR) are the direct beneficiaries. Size large-cap positions for stability and small-cap positions (Karoon, Beach Energy) for leverage, recognising the higher volatility Kavonic flagged.

- Review and reduce airline and consumer discretionary exposure. Qantas’s A$800 million fuel cost increase illustrates the scale of earnings risk. Consumer discretionary names face indirect pressure through reduced household spending.

- Assess REIT exposure to rate risk. If the RBA follows through on tightening guidance, rate-sensitive sectors face valuation compression regardless of their direct fuel exposure.

- Consider hedging for positions held for fundamental reasons. Investors unable to reduce transport or consumer discretionary holdings outright can evaluate sector-level hedging strategies to manage near-term downside.

Post-spike analysis from Traders Circle recommended a defensive rotation toward energy producers, specifically naming Woodside, Santos, and Karoon, while hedging exposure to transport and consumer discretionary sectors vulnerable to fuel cost pass-through and softening demand.

The energy sector’s relatively higher dividend yield profile compared to the broader ASX 200 provides an additional income argument for the rotation, though this should be treated as a supporting factor rather than the primary thesis. This rotation is conditional on oil prices remaining elevated rather than representing a permanent strategic shift.

The oil shock playbook has a time limit

Oil shocks produce sector divergence, and understanding the direction of that divergence in advance is a material investment advantage for ASX investors. The 2026 oil rally separated energy producers from airlines, consumer discretionary names, and miners with a clarity that the data supports and the transmission mechanisms explain.

The rotation is conditional. If oil prices retreat sharply, as historical cycles suggest they eventually do (Brent moved from US$110 toward the US$70-80 range in prior episodes), energy sector outperformance unwinds and cost-pressured sectors recover. The variable to monitor beyond the oil price itself is the RBA’s inflation and rate trajectory. Monetary policy tightening can extend market pressure across growth equities and fixed-income holdings even after crude stabilises.

Structural deflationary forces operating beneath the headline CPI number, including AI-driven productivity gains, discounted Chinese goods diversion, and frozen global housing markets, create an unusual situation where aggressive defensive repositioning against inflation may itself become a portfolio risk if the shock resolves faster than rate-hike pricing implies.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.