A single ETF share in a broad S&P 500 fund gives an investor simultaneous ownership stakes in 500 companies, yet it often costs the same or less than buying one share of any of those companies individually. That contrast captures why the question of stocks versus ETFs is one of the most important decisions beginners face when building a portfolio.

Global ETF assets reached $21.24 trillion by February 2026, up from $14.85 trillion at the end of 2024, according to ETFGI data. The growth reflects a structural shift in how retail investors access markets. Yet individual stocks remain heavily traded, and new investors are routinely uncertain about which instrument belongs in their portfolio, or whether both do.

This article explains what each instrument actually represents at the ownership level, how their risk profiles differ mechanically, and how costs, taxes, and control factors interact, so readers can make an informed choice grounded in their own goals and risk tolerance.

What you actually own when you buy a stock

Buying a stock means buying a fractional ownership stake in one specific company. It is not a contract that tracks the company’s price from a distance; it is a direct claim on the business itself.

That claim ties an investor’s outcome entirely to one company’s earnings trajectory, leadership decisions, regulatory environment, and competitive position. If the company thrives, the shareholder benefits. If the company falters, there is no buffer.

Stock ownership typically entitles the investor to:

- Price appreciation potential if the share price rises over time

- Dividends, which are distributions of a portion of the company’s profits to shareholders

- Voting rights on corporate matters such as board elections and major strategic decisions

- A proportional claim on assets in the event the company is wound up

Stock prices respond to supply and demand, company earnings, macroeconomic conditions, and market sentiment, all of which can work for or against a single-company holder. Understanding that a stock is an ownership claim, not just a price on a screen, is the foundation for grasping why concentration risk is a structural feature of stock investing rather than an accidental side effect.

When big ASX news breaks, our subscribers know first

What you actually own when you buy an ETF

If stock ownership is a single-company bet, an ETF is the architectural opposite. An exchange-traded fund (a pooled investment product that holds a collection of assets) trades on an exchange exactly like a stock share, but each share provides exposure to an entire basket of securities rather than one company.

The majority of ETFs are structured to replicate a market index rather than attempt to beat it, making them passively managed by design. Buying one share of an S&P 500 ETF, for example, provides proportional exposure to 500 of the largest U.S.-listed companies simultaneously. One transaction, hundreds of ownership positions.

Global ETF assets reached $21.24 trillion by February 2026, according to ETFGI and MarketsMedia, reflecting a 31% year-on-year increase from $19.44 trillion at the end of 2025.

The scale of that growth signals how central the instrument has become. According to Schwab’s 2025 ETFs and Beyond Study, 62% of ETF investors can envision moving to ETF-only portfolios, with roughly half saying this could happen within five years.

ETFGI global ETF industry data tracking monthly asset flows shows that the acceleration from $14.85 trillion at end-2024 to $21.24 trillion by February 2026 represents one of the fastest expansions in the instrument’s history, driven largely by retail inflows into passive index products.

ETF ownership provides:

- Diversification across holdings through a single purchase

- Intraday trading flexibility identical to individual stocks

- Dividends passed through from underlying holdings

- No direct voting rights in the underlying companies, a meaningful structural difference from stock ownership

That last point matters. ETF shareholders delegate governance to the fund provider, exchanging individual corporate influence for the breadth and simplicity of pooled exposure. For most beginners, the trade-off is one they willingly make.

Why concentration risk is the central difference between the two instruments

The ownership distinction between stocks and ETFs is not abstract. It produces measurably different outcomes when things go wrong.

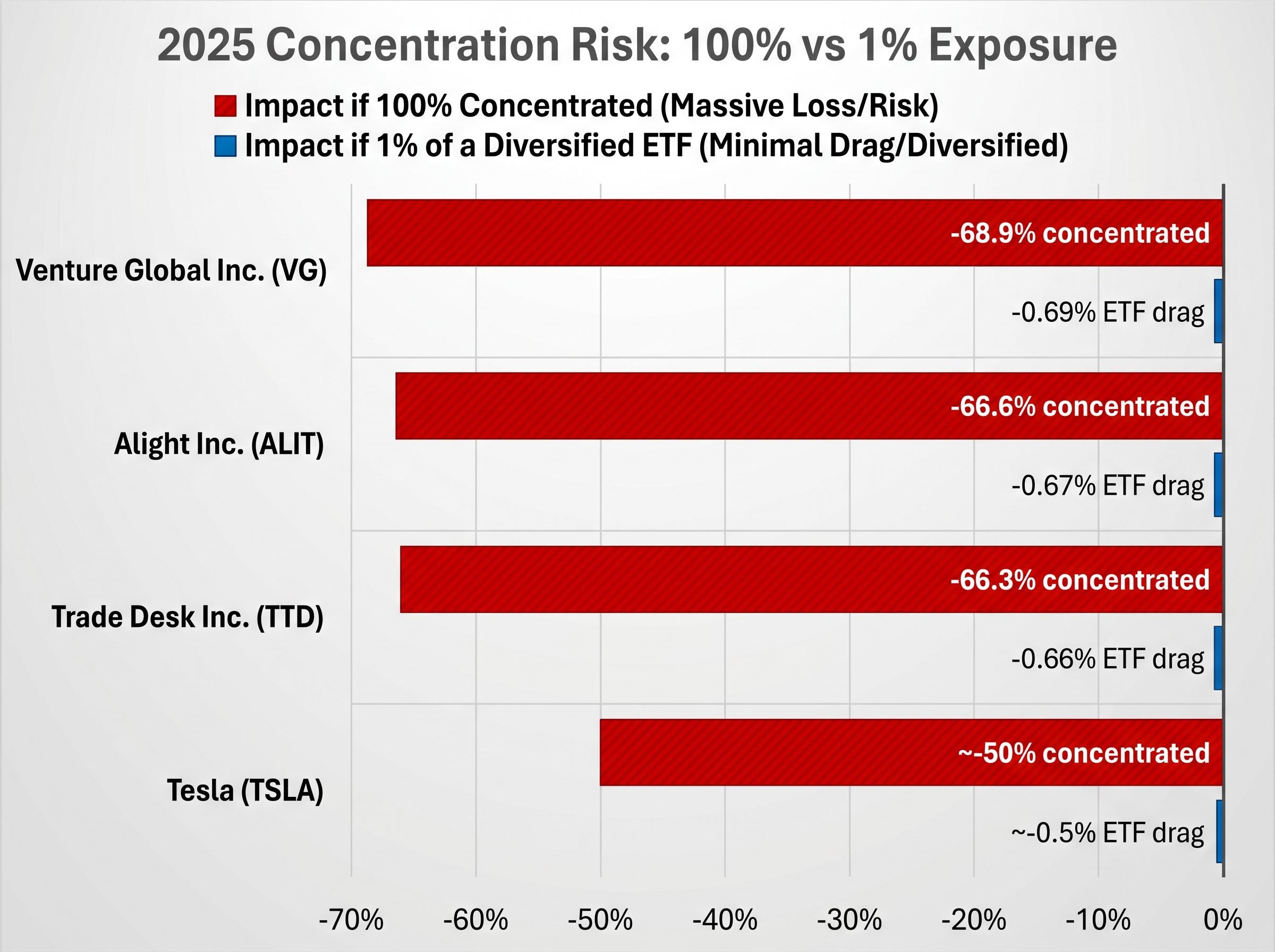

When 100% of capital sits in one stock, a 50% price decline means a 50% portfolio loss. When that same stock represents 1% of a diversified ETF, the identical 50% decline produces only a 0.5% drag on the portfolio. The maths is simple; the consequences are not.

2025 provided multiple real-world demonstrations of single-stock risk at full exposure.

| Company | 2025 Decline | Impact if 100% Concentrated | Impact if 1% of a Diversified ETF |

|---|---|---|---|

| Venture Global Inc. (VG) | -68.9% | -68.9% portfolio loss | -0.69% portfolio drag |

| Alight Inc. (ALIT) | -66.6% | -66.6% portfolio loss | -0.67% portfolio drag |

| Trade Desk Inc. (TTD) | -66.3% | -66.3% portfolio loss | -0.66% portfolio drag |

| Tesla (TSLA) | ~-50% | ~-50% portfolio loss | ~-0.5% portfolio drag |

These are not obscure microcaps. Tesla was among the most widely held retail stocks in the world when it fell approximately 50% in early 2025.

A 70% drop in one stock that represents 1% of an ETF translates to only a 0.7% drag on the overall fund.

ETFs do not eliminate risk. They redistribute it across a wider base. An investor in a broad index ETF participates fully in market-wide downturns, but is structurally insulated from the kind of company-specific catastrophe that destroyed two-thirds of a concentrated holder’s capital in a single year.

Index concentration risk complicates the diversification argument, because cap-weighted S&P 500 ETFs allocate roughly 23% of total weight to just five mega-cap stocks, meaning a broad market fund can behave more like a concentrated technology bet than a genuinely dispersed ownership pool.

How costs and tax treatment compare for everyday investors

The risk discussion is emotional. The cost discussion is arithmetic, and it compounds over decades.

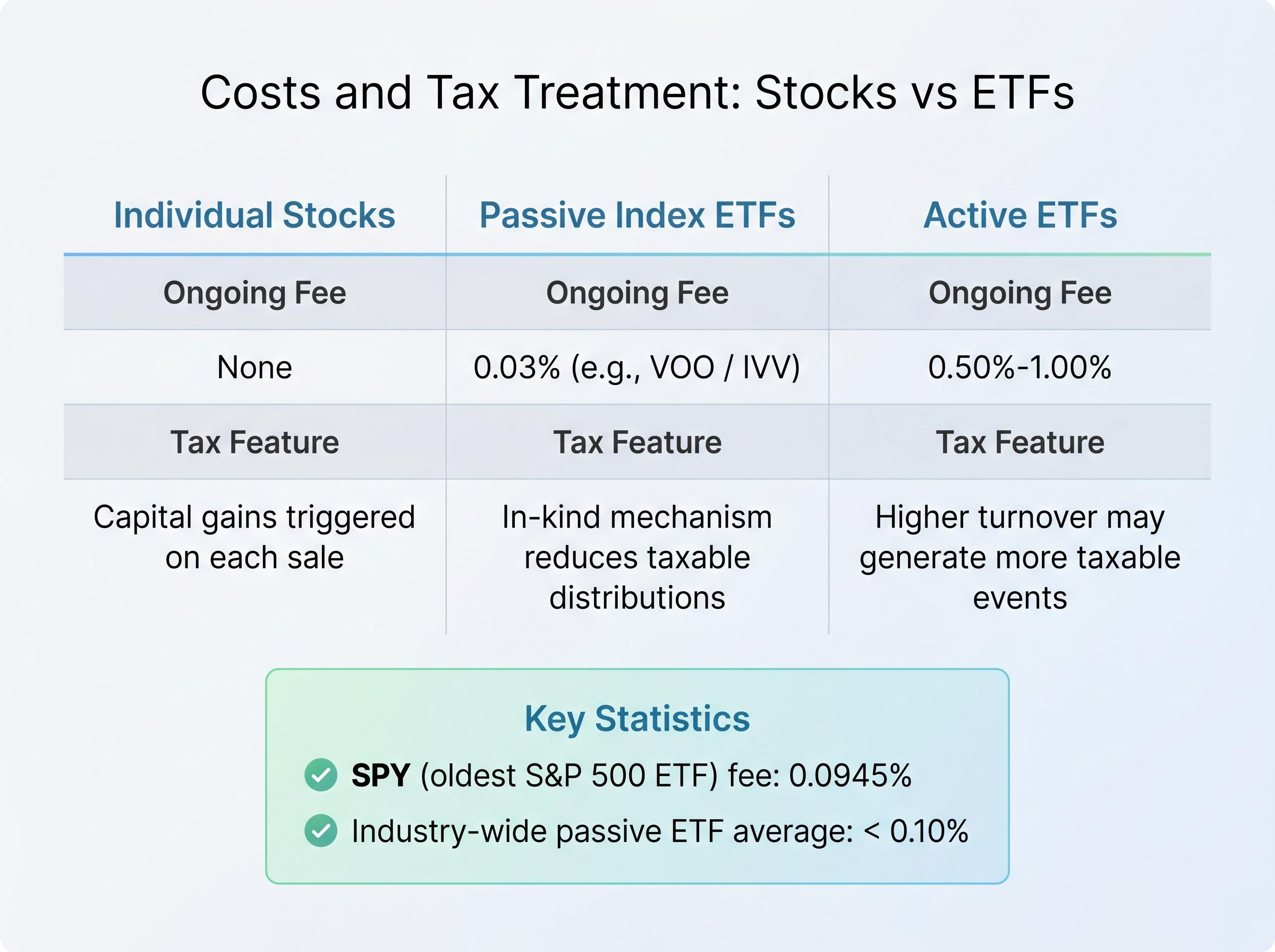

Individual stocks carry no ongoing management fee. Commission-free trading is now standard on major platforms, meaning an investor can buy and hold a single stock at zero recurring cost. The catch is that building a diversified portfolio of individual stocks requires multiple purchases, and each sale may trigger a capital gains event.

ETFs charge an expense ratio, an annually deducted percentage of the invested amount covering fund administration. For passive index ETFs, these fees have fallen to levels that are effectively negligible for most investors.

| Instrument | Ongoing Fee | Notable Tax Feature |

|---|---|---|

| Individual stocks | None | Capital gains triggered on each sale |

| Passive index ETF (e.g. VOO / IVV) | 0.03% | In-kind mechanism reduces taxable distributions |

| Active ETF | 0.50%-1.00% | Higher turnover may generate more taxable events |

According to ICI’s 2025 research, index equity ETF fees have declined approximately 33% over the past nine years, while bond ETF fees have declined approximately 50%. SPY, the oldest S&P 500 ETF, charges 0.0945%, still meaningfully higher than VOO and IVV at 0.03%. The industry-wide passive ETF average sits under 0.10%.

The tax efficiency edge ETFs carry over mutual funds

ETFs hold a structural tax advantage that is less obvious than their fee advantage but equally meaningful over time.

The mechanism is called in-kind creation and redemption. When large institutional investors exchange ETF shares for the underlying basket of stocks (or vice versa), the transaction occurs without triggering capital gains inside the fund. By contrast, when a mutual fund manager sells holdings to meet investor redemptions, the resulting capital gains are distributed to all remaining fund holders, often arriving as unexpected taxable events mid-year.

This does not eliminate capital gains tax for the ETF investor upon sale. It reduces the likelihood of receiving taxable distributions while still holding the position, giving the investor greater control over when tax events occur.

ETF tax efficiency operates through the in-kind creation and redemption mechanism at the institutional level, but the after-tax outcomes for individual investors also depend on holding period, account type, and whether the fund distributes franked dividends, all of which vary meaningfully by jurisdiction and investor structure.

Control, flexibility, and who each instrument suits best

The control trade-off between stocks and ETFs is not a deficiency of either instrument. It is a design choice, and the right answer depends on what an investor is optimising for.

Individual stocks allow high-conviction, targeted positions on specific companies, sectors, or leadership teams. This is precisely what experienced, research-capable investors want. They accept concentrated volatility in exchange for the possibility of outsized returns and direct corporate influence through voting rights.

ETFs structurally prevent concentrated positions in favour of averaged market-rate returns. The extreme upside is capped, but so is the catastrophic downside. Both instruments trade intraday on exchanges, giving investors equivalent liquidity and entry or exit flexibility.

According to Schwab’s 2025 study, ETF investors currently allocate an average of 27% of their portfolios to ETFs and expect to raise that figure to 34% within five years. The trajectory is clear, though it does not imply stocks are becoming obsolete.

Generational investing trends reveal that the ETF-heavy portfolio model is not evenly distributed across age cohorts: Millennials allocate approximately 70% of their investment capital to ETFs, while Gen Z and Gen X have converged around a 50/50 split between ETFs and individual stocks, suggesting the core-satellite balance shifts predictably with investment experience and age.

Financial educator and advisor consensus in 2024-2025 positions the instruments along a spectrum of investor experience:

- ETFs suit: Beginners, passive investors, those seeking broad exposure with minimal research time, and investors prioritising cost efficiency

- Individual stocks suit: Experienced investors with high conviction, dedicated research capacity, comfort with concentrated volatility, and a desire for direct corporate governance participation

The question is not which instrument is objectively superior. It is which instrument matches the investor’s available time, analytical confidence, and tolerance for concentration risk.

Using both in one portfolio: the core-satellite approach

Most investors do not need to choose one or the other. The core-satellite portfolio structure offers a practical way to use both.

ETFs form the diversified, low-cost core, providing broad market exposure that captures overall market returns. Individual stocks serve as satellite positions, expressing specific investment views or targeting growth opportunities the investor has researched independently.

This approach allows beginners to start with an ETF-only foundation and add individual stocks selectively as their research confidence and risk tolerance grow. Many advisors recommend a three-step progression:

- Establish an ETF core covering broad market exposure across sectors and geographies

- Build investment research habits before committing capital to individual company positions

- Add individual stock positions selectively as satellite holdings once the core is stable and the investor has developed analytical capacity

According to Schwab’s 2025 ETFs and Beyond Study, 62% of ETF investors can envision moving to ETF-only portfolios, with roughly half saying this could happen within five years.

That finding suggests the ETF-only model is a realistic long-term destination for many investors, not merely a starting point. ICI’s 2025 household research reinforces this, showing that cost effectiveness and diversification remain the primary motivators for ETF adoption among retail investors.

The appropriate balance between core and satellite positions depends on investment goals, time horizon, available research time, and risk appetite. Consulting a qualified financial professional is advisable for personalised guidance on portfolio construction.

The right instrument depends on the investor, not the market

Stocks offer ownership depth and upside concentration. ETFs offer breadth, cost efficiency, and structural risk reduction. Both serve legitimate purposes depending on investor profile.

Three questions clarify which instrument, or which combination, fits a given investor’s situation. How much time is available for company-level research? How much volatility is tolerable without selling at the wrong moment? Is the goal to build a core portfolio or supplement one that already exists?

For investors who find their risk tolerance in theory differs from their behaviour during market declines, our full explainer on staying invested through market volatility examines the behavioural research behind reactive trading, including the estimated 1.5% annual return drag that unnecessary selling imposes, alongside the systematic practices that help investors hold positions through drawdowns.

The global shift toward ETF adoption, reflected in $21.24 trillion in assets as of February 2026, does not represent a verdict against stocks. It reflects a recognition that diversification at low cost is a sound foundation for most investors, a foundation that individual stock positions can complement rather than replace.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.