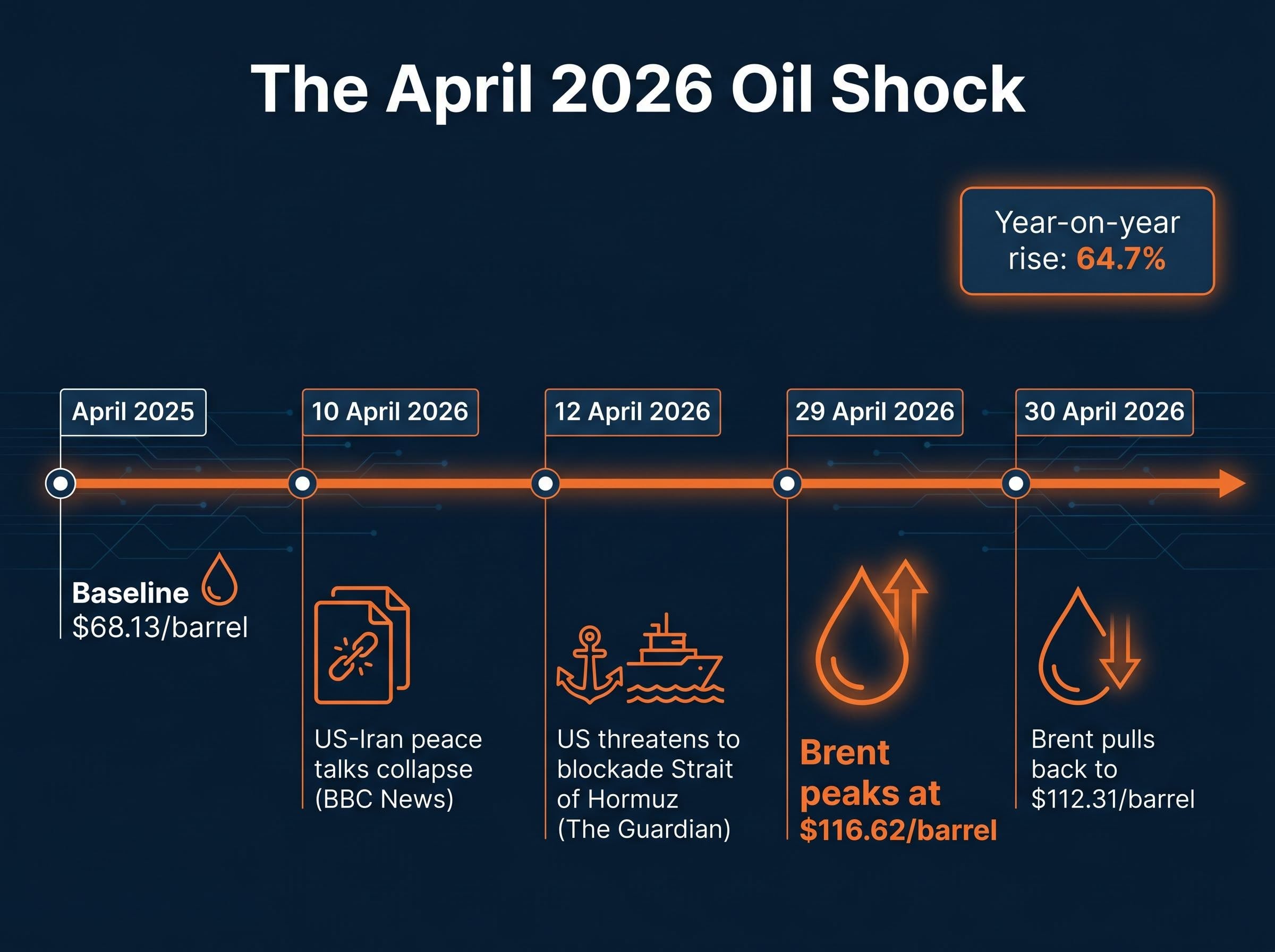

Brent crude hit $116.62 per barrel on 29 April 2026, its highest sustained level since Russia’s 2022 invasion of Ukraine. The ASX 200 fell from 8,786 points to 8,687 points across the session cluster that followed, with energy the only sector to finish higher. This is not a simple commodity story. Oil is the connective tissue of the modern economy, and when its price surges nearly 65% year on year, the consequences ripple through inflation data, central bank policy rooms, company earnings, and household budgets simultaneously. For Australian investors and consumers, the dynamics are particularly acute: Australia imports crude oil but exports LNG, creating a structural split between energy producers and the rest of the economy. What follows traces the full causal chain, from the geopolitical trigger in the Strait of Hormuz to the RBA’s rate calculus to the sector-level winners and losers on the ASX, so readers can understand not just what happened but why the initial shock compounds over time.

From the Strait of Hormuz to the trading floor: what set off this oil shock

The oil surge did not arrive as a single event. It built through a sequence of discrete escalations, each of which repriced supply risk higher.

- US-Iran peace talks collapsed in early April, removing any near-term expectation of Iranian supply returning to global markets (BBC News, 10 April 2026)

- On 12 April 2026, the US announced a threat to blockade the Strait of Hormuz, shifting supply disruption risk from theoretical to operational (The Guardian, 12 April 2026)

- OPEC+ had no meaningful spare capacity available to offset the disruption premium being priced in, leaving the market without a supply-side safety valve

Each step could have gone differently. A diplomatic resolution would have kept Brent near its March monthly average of $103.10. Instead, crude climbed to $116.62 on 29 April, a daily gain of approximately 4.82%, before pulling back to $112.31 on 30 April.

$116.62 per barrel on 29 April 2026: the first sustained period above $100 since Russia’s 2022 invasion of Ukraine.

One year earlier, in April 2025, Brent traded at approximately $68.13 per barrel. The year-on-year rise of 64.7% reflects not a gradual trend but a geopolitical repricing that happened in weeks.

When big ASX news breaks, our subscribers know first

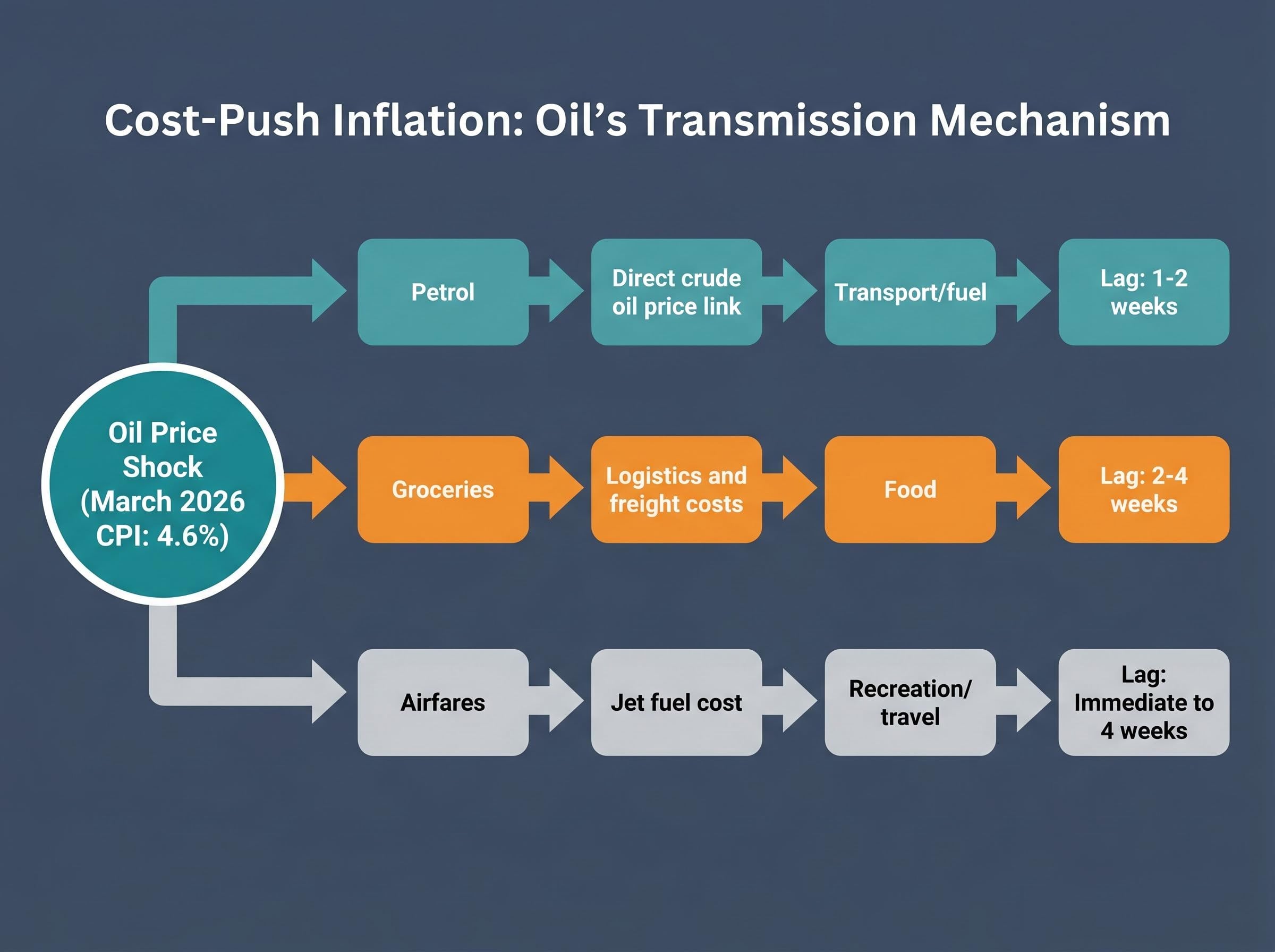

Why oil is not just an energy story: the cost-push inflation transmission mechanism

The petrol station is the most visible channel, but it is not the only one. Cost-push inflation, where rising input costs force businesses to raise prices rather than consumer demand pulling prices higher, operates across multiple pathways simultaneously. Higher crude makes diesel more expensive, which makes trucking more expensive, which makes groceries more expensive. It makes jet fuel more expensive, which makes airfares more expensive. It makes petrochemical feedstocks more expensive, which makes plastics and packaging more expensive.

Australian CPI rose 4.6% in the year to March 2026, up from 3.7% in February, with a quarterly increase of 1.4% for Q1. That figure already sits well above the RBA’s 2-3% target band. Housing costs, up 6.5% year on year, contribute separately, but the oil-linked components are accelerating fastest.

The table below maps how crude oil enters the consumer price basket through three distinct channels.

| Channel | How oil feeds in | CPI category affected | Lag time |

|---|---|---|---|

| Petrol | Direct crude oil price link | Transport/fuel | 1-2 weeks |

| Groceries | Logistics and freight costs | Food | 2-4 weeks |

| Airfares | Jet fuel cost | Recreation/travel | Immediate to 4 weeks |

RBC has warned that headline CPI could peak at 5-6% if oil remains elevated near current levels, a scenario that would place the RBA under considerable pressure.

Trimmed mean CPI, which strips out volatile items like fuel to reveal underlying price pressures, held at 3.3% even as the headline figure surged to 4.6%, a divergence that complicates the RBA’s task because it suggests the worst of the current spike is supply-driven rather than entrenched across the broader economy.

The currency multiplier: why AUD weakness makes oil shocks hit harder

Crude oil is priced in US dollars globally. A weaker Australian dollar increases the effective cost of imported oil for Australian refiners and distributors. This creates a compounding dynamic: geopolitical risk often weakens the AUD through risk-off sentiment at exactly the same moment crude prices spike. The Australian economy absorbs the dual impact of higher commodity prices and a less favourable exchange rate simultaneously, amplifying the inflationary pass-through beyond what the US dollar-denominated Brent price alone would suggest.

The RBA is not a bystander: how central bank policy amplifies the shock

The RBA raised its cash rate by 25 basis points to 4.10% in March 2026. That decision preceded the worst of the oil spike but anticipated it. The accompanying statement warned that sustained high oil prices could drive inflation higher and require holding elevated rates for longer.

The mechanism connecting oil to equity valuations runs through the RBA’s rate calculus in three steps:

- Oil rises sharply, pushing petrol, logistics, and energy input costs through the CPI basket

- CPI accelerates above the RBA’s 2-3% target band (already at 4.6% in March, with the 5-6% scenario flagged by RBC)

- The RBA holds or raises rates in response, compressing equity multiples across the ASX as higher discount rates reduce the present value of future corporate earnings

This third step is what transforms a commodity price event into a broad equity market event. Growth stocks, REITs, and high price-to-earnings companies fall even when they have no direct oil exposure, because the rate at which future earnings are discounted has risen.

The RBA’s assistant governor warned that central banks must prevent oil-driven price rises from becoming entrenched as broader inflationary expectations, according to a 25 March 2026 report in the Wall Street Journal.

Oxford Economics has predicted continued oil-driven price rises will damage non-energy corporate earnings. For investors holding diversified ASX portfolios, the RBA channel is the mechanism that connects a barrel of crude in the Persian Gulf to the valuation of a domestic REIT or a technology stock with no oil exposure at all.

Oil futures backwardation, where forward contracts price crude significantly below spot levels, signals that institutional capital views the Hormuz disruption as temporary rather than a permanent supply regime shift, which matters for how investors interpret the current CPI data and the likely duration of the RBA’s tightening stance.

Mapping ASX sectors: divergent impacts of an oil shock

The sector bifurcation is not a scoreboard; it is a structural logic. Each sector’s exposure to an oil shock operates through a different mechanism, and the mechanism determines both the severity and the likely duration of the impact.

Energy stocks are the direct beneficiaries. Woodside (WDS), Santos (STO), and Karoon (KAR) outperformed during the broad ASX decline as higher crude realisation prices flow directly to their revenue lines. Their outperformance is the predictable first-order effect.

The losses are distributed across multiple channels. Qantas (QAN) was among the hardest hit, given jet fuel’s direct linkage to crude. Woolworths (WOW) faced supply chain logistics cost pressure as diesel and freight charges climbed. BHP, Rio Tinto, and Fortescue operate diesel-intensive mining operations where input cost increases compress margins, even as their commodity outputs face separate demand-side uncertainty from weakening global growth expectations.

Commonwealth Bank (CBA) and the broader financials sector declined as part of the non-energy sell-off, driven less by direct oil exposure and more by the macro headwinds described in the RBA section above.

| Sector | Mechanism | ASX examples | Direction during shock |

|---|---|---|---|

| Energy | Direct revenue benefit | WDS, STO, KAR | Positive |

| Transport/Aviation | Jet fuel cost spike | QAN | Negative |

| Consumer Staples | Logistics pass-through | WOW | Negative |

| Mining/Materials | Diesel input cost squeeze | BHP, RIO, FMG | Negative |

| Financials | Macro headwinds/rate risk | CBA | Negative |

| REITs and Growth | Discount rate compression | Rate-sensitive names broadly | Negative |

The framework above applies beyond this specific shock. In any oil-driven disruption, the question for each sector is whether the exposure is direct cost, discount rate, or demand destruction. The answer shapes the appropriate investor response.

What investors can do with this information: thinking through portfolio positioning

The analysis above points in a clear direction, but the application requires nuance. Energy stocks have already repriced significantly; a 64.7% year-on-year rise in Brent is already reflected in the share prices of Woodside, Santos, and Karoon. The directional thesis may be correct, but the entry point question matters.

Three positioning considerations follow from the mechanisms described:

- Energy sector exposure: Direct beneficiaries of sustained high oil, but the repricing already embedded in share prices means the risk-reward is different from where it stood six months ago

- Reducing or hedging high-cost-sensitivity names: Transport, aviation, and discretionary retail face the most immediate margin pressure from cost pass-through, and the lag times in the CPI transmission table suggest the full impact has not yet been felt

- Reviewing rate-sensitive holdings: REITs, high price-to-earnings growth stocks, and long-duration positions face a headwind from a higher-for-longer RBA cash rate at 4.10%, with further tightening possible if CPI accelerates toward the 5-6% range flagged by RBC

Both Oxford Economics and RBC have flagged further downside risk to non-energy corporate earnings. The macro environment is not one where broad index exposure passively delivers.

Investors wanting to stress-test the higher-for-longer assumption against historical supply shock precedents will find our full explainer on the RBA rate cycle peak, which examines Taylor Rule analysis, the 6-12 month reversal pattern from past oil shock episodes, and Oxford Economics modelling of potential back-to-back GDP contractions in Australia during mid-2026.

The passive investor’s blind spot: oil shocks and index concentration risk

Standard ASX 200 index exposure carries a heavy weighting toward financials and materials. In a high-oil environment, both sectors face headwinds, financials through macro and rate channels, materials through diesel-intensive cost structures. Passive investors holding broad index positions may not realise their portfolio carries a concentration of oil-negative exposure, even without any active stock selection. The composition of the index itself becomes a risk factor during energy shocks.

The feedback loop does not stop at the petrol station

The mechanisms described above do not operate in isolation. They compound. Higher oil drives CPI higher, which forces the RBA to hold or raise rates, which depresses equity valuations and household borrowing capacity, which weakens consumer spending and corporate earnings, which feeds back into further ASX weakness.

“Oil spikes, CPI accelerates, RBA tightens, equity multiples compress, household spending falls, earnings disappoint, ASX falls further.”

The resolution timeline is tied to geopolitical developments largely outside the control of the RBA or any domestic institution. Two indicators will signal whether this shock is winding down or entrenching:

- Diplomatic developments affecting the Strait of Hormuz and Iranian supply: a resolution would remove the disruption premium that has driven Brent above $100

- The next quarterly CPI print: whether inflation shows acceleration toward the 5-6% peak scenario or deceleration back toward the RBA’s 2-3% target band

With CPI already at 4.6% and the cash rate at 4.10%, the margin for error is thin. Investors who understand the feedback loop can distinguish between a temporary spike and a structural repricing event, and that distinction determines whether the appropriate response is to hold through volatility or materially reassess risk exposure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.