How to Build a Global Portfolio With Two ASX ETFs

1 hr ago

A $50,000 salary supports roughly $200,000 in borrowing. A $100,000 salary supports $400,000. That single ratio, the four-times-income rule most Australian lenders apply, illustrates why the order of financial decisions matters more than any individual move a young person can make. Most wealth-building content for young Australians focuses on what to do: save more, invest early, buy property. It rarely addresses the sequence in which those moves should be made. With the combined capitals median dwelling now at $1,014,401 and average new owner-occupier loans at $736,257 (ABS, December 2025), the cost of getting the sequence wrong has never been higher.

This guide lays out a practical sequencing framework covering income growth, borrowing capacity, the property-versus-shares trade-off, first home buyer scheme eligibility, and superannuation engagement. The goal is not another to-do list. It is a priority order, built around the financial mechanics that determine how quickly each step unlocks the next.

The instinct makes sense. Diversify effort. Spread resources across every goal at once. The problem is that when income is modest, splitting funds across competing priorities means none of them reaches a useful threshold at speed. The three goals most young Australians try to pursue simultaneously are:

On a median full-time income of approximately $74,672 annually (ABS, May 2025), directing a third of surplus income to each of these goals produces painfully slow progress on all three. The deposit takes longer to reach. The portfolio stays too small to compound meaningfully. The debt lingers.

“A $50,000 salary supports roughly $200,000 in borrowing. Double your income, and your borrowing power doubles too.”

Sequencing works differently. It concentrates all available surplus on completing one goal, then pivots the freed-up resources into the next. The effect is compounding momentum: finishing step one faster means step two starts with more fuel behind it. The distinction is between financial multitasking, which spreads money thin, and financial sequencing, which concentrates effort and then redirects it.

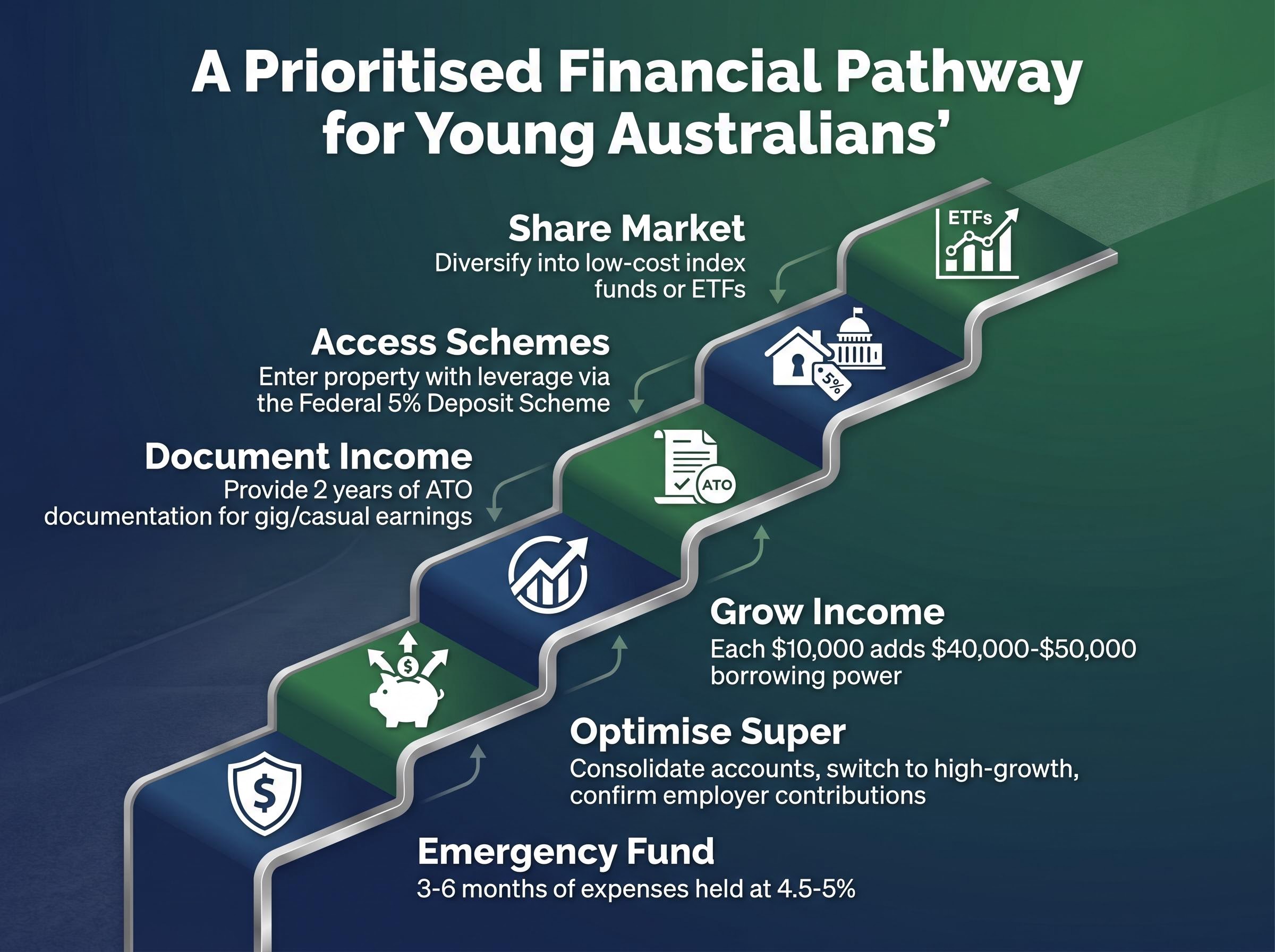

Before any sequencing begins, the non-negotiable first step is a 3-6 month emergency fund held in cash. Without it, any disruption forces a sale, a withdrawal, or new debt, resetting the entire sequence.

Superannuation is already running for every employed young Australian. The employer contribution rate sits at 11.5%, rising to 12% by July 2026 (ATO). The average superannuation balance for a 20-24 year-old is approximately $10,000. With a 40-plus year horizon before preservation age, even that modest balance compounds substantially, provided the fund settings are working in the right direction.

The issue is that most young Australians leave their super on default settings. That often means a balanced or conservative investment option and duplicate accounts from multiple employers, each charging separate administration fees. Reviewing these settings costs nothing.

Superannuation balance benchmarks by age show the average 20-24 year-old sitting at approximately $10,000, a figure that looks modest until a high-growth investment option and a 40-year compounding runway are applied, at which point the gap between default balanced settings and optimised settings becomes substantial.

Three no-cost superannuation actions available this week:

“The average 20-24 year-old has around $10,000 in super. In a high-growth option over 40 years, that $10,000 alone compounds into a meaningfully different retirement position before a single extra dollar is contributed.”

For those with surplus income, voluntary concessional contributions offer a tax-efficiency lever. The cap is $30,000 per year, and contributions are taxed at 15% within the fund rather than at the contributor’s marginal income tax rate. For a young worker on a higher marginal rate, each dollar directed to super retains more value than the same dollar saved in a high-interest account averaging 4.5-5% per annum before tax.

The ATO key super rates and thresholds page confirms the concessional contributions cap sits at $30,000 for the 2024-2026 period before rising to $32,500 from 1 July 2026, a change that opens an additional voluntary contribution window for young workers who act before the cap increases.

Readers employed in state government roles should note that constitutionally protected funds (such as West State Super or Gold State Triple S) allow contributions of up to the full salary with taxation deferred to withdrawal, and carry different balance thresholds of approximately $1.865 million rather than the standard concessional cap structure.

Expenses can be cut to zero. Income has no ceiling. That asymmetry makes income growth the single variable with the most upside for a young Australian on a modest base. ABS earnings data illustrates the trajectory: median weekly earnings for 15-19 year-olds in full-time work sit at approximately $43,680 annually, rising to roughly $62,500 for 20-24 year-olds and $78,200 for 25-29 year-olds. The progression is steep, and it is not accidental. It reflects experience, credential accumulation, and deliberate career moves.

Each additional $10,000 of verified annual income adds approximately $40,000-$50,000 in borrowing power under the four-times rule. That means the gap between a $60,000 salary and an $80,000 salary is not just $20,000 in annual take-home pay. It is roughly $80,000-$100,000 in additional borrowing capacity, a number that directly determines which properties are within reach.

Three practical income-growth pathways are available without requiring a full-time university degree:

Lenders accept gig and casual income, but they require two years of consistent, documented earnings verified via ATO tax assessments. Major lenders such as Westpac and NAB apply a haircut of approximately 70-80% to gig income. Westpac, for example, counts Uber income at roughly 75% of the reported figure.

Verified gig income can add approximately $50,000-$100,000 to borrowing capacity. However, roughly 40% of gig income applications faced rejection in 2024, according to Canstar survey data. The two-year documentation runway is not optional; it is the difference between income that counts and income that does not exist in a lender’s assessment.

A bank does not see a young borrower the way the borrower sees themselves. The lender sees income documentation, liability schedules, and a serviceability model that stress-tests repayment capacity well above the actual loan rate.

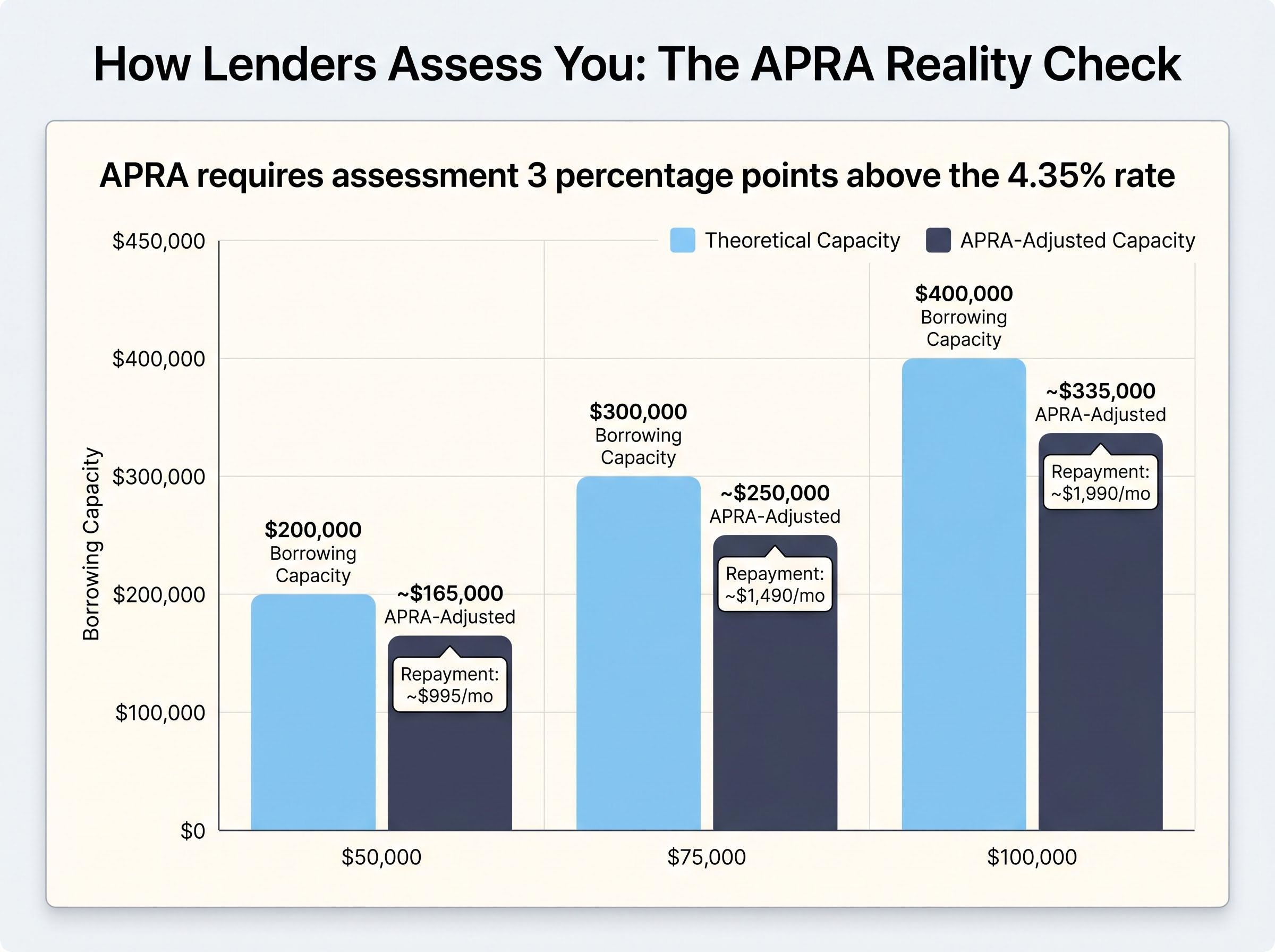

The APRA serviceability buffer requires lenders to assess repayment capacity at 3 percentage points above the assessed rate. With the RBA cash rate at 4.35% as of May 2026, that means a borrower is stress-tested at approximately 7.35% or higher, depending on the product rate. This buffer alone reduces borrowing capacity by approximately 15-20% compared to an assessment at the actual rate. APRA confirmed the buffer remains unchanged as of July 2025, with new rules effective 1 February 2026.

The RBA cash rate reached 4.35% in May 2026 following the third consecutive hike from a starting point of 3.85% in January, a tightening cycle that directly raises the APRA stress-test rate for new borrowers and compresses borrowing capacity for anyone mid-way through building their deposit.

APRA’s macroprudential settings update, published in July 2025, confirmed that the 3 percentage point serviceability buffer remains in place, meaning any borrower assessed today is stress-tested well above their actual loan rate regardless of where the RBA cash rate sits.

“Lenders assess your repayment capacity at 3 percentage points above your actual rate. On a $600,000 loan, that changes everything.”

Most lenders apply an income multiplier in the range of 3.5-5x gross annual income, down from pre-2022 peaks of 6-7x. CBA policy caps serviceability at a 30% debt-to-income ratio for under-30s. The two-year income documentation rule applies across employment types, whether PAYG, casual, self-employed, or gig worker.

The following table illustrates how income level, the four-times borrowing rule, and the APRA buffer interact:

| Annual Income | Borrowing Capacity (approx. 4x) | Monthly Repayment at 4.35% | APRA-Adjusted Capacity |

|---|---|---|---|

| $50,000 | $200,000 | ~$995 | ~$165,000 |

| $75,000 | $300,000 | ~$1,490 | ~$250,000 |

| $100,000 | $400,000 | ~$1,990 | ~$335,000 |

Understanding these mechanics before walking into a broker’s office turns borrowing capacity from a mystery into a variable that can be managed: grow the income, document it for two years, reduce liabilities, and time the application accordingly.

The property-versus-shares argument generates more heat than light because it is usually framed as a preference. In a sequencing framework, it is a timing question: which asset class serves the reader best at the current stage of their wealth-building sequence?

The long-run returns are closer than most partisans admit. Property Update data (referencing Michael Yardney’s analysis) shows Australian property returning approximately 8.2% per annum since 2000, while the ASX returned approximately 7.9% over the same period. Vanguard data complicates the picture, suggesting shares edge ahead on a volatility-adjusted basis at approximately 9.1% versus property at 7.8% post-fees. The ASX 200 returned 9.97% in FY2024/25 and sat at 8,878.10 as of 8 May 2026. National dwelling values grew approximately 9.6% annually to March 2026, according to CoreLogic.

| Asset Class | Long-Run Annual Return | Leverage Available | Liquidity | Government Scheme Access |

|---|---|---|---|---|

| Property | ~8.2% pa | Up to 95% LVR via govt schemes | Low (months to sell) | Yes (5% Deposit Scheme, state grants) |

| Shares (ASX 200) | ~7.9-9.1% pa (varies by measure) | Limited (margin lending) | High (T+2 settlement) | No |

The distinction that matters for sequencing is leverage and scheme access. A first home buyer who enters property with a 5% deposit via the federal scheme is deploying $50,000 to control an asset worth $1,000,000. No equivalent leverage multiplier exists for shares at this stage. One personal example, referenced in property commentary, illustrates the stakes: choosing shares over property for roughly eight years produced an estimated $1.2 million difference in outcomes, based on a property purchased for $270,000 that subsequently reached approximately $1.2 million.

Margin lending mechanics in Australia carry variable rates now exceeding 10% per annum, which means the leverage multiplier that makes property so powerful for first home buyers, where government schemes allow a 5% deposit to control a $1,000,000 asset, has no practical equivalent in the share market at current borrowing costs.

That does not mean property is always the correct first move. It means that for readers who can access scheme-assisted leverage, the sequencing argument favours property early. Once equity is building, layering in share market exposure adds diversification and liquidity to the portfolio.

The federal landscape shifted significantly from 1 October 2025. The key current conditions:

Not all lenders participate in every government scheme. Eligibility is determined by the state where the property is located, not the buyer’s current residence. Readers in NSW and Victoria should not pursue discontinued programmes.

The sections above covered individual components. What follows is the consolidated priority order, not a checklist to complete simultaneously but a sequence where finishing each step faster enables the next one.

The sequence is not rigid. Departing from it has opportunity costs, not penalties. But the borrowing capacity maths illustrate why income growth must precede a property application rather than run alongside it: a $74,672 median income supports roughly $300,000 in borrowing, while reaching $100,000 pushes that to approximately $400,000-plus. Verified gig income documented over two years can add another $50,000-$100,000 on top.

At a combined capitals median of $1,014,401, property entry is genuinely out of reach for many young Australians without parental support or access to government schemes. That reality does not invalidate the sequencing logic; it redirects it.

The alternative sequence runs: emergency fund, super optimisation, income growth, then a disciplined low-cost ETF contribution strategy using the same sequential concentration logic. Low-cost index funds on the ASX offer broad market exposure with no minimum entry beyond the cost of one unit, making them accessible at any income level. The principle remains: concentrate effort on one step, complete it, then pivot the freed-up resources to the next.

The $1.2 million property example bears repeating, not for the specific number but for what it reveals about sequencing.

“Choosing shares over property for eight years produced an estimated $1.2 million gap in outcomes. The issue was not the asset class chosen. It was the order.”

A property purchased for $270,000 that subsequently reached approximately $1.2 million illustrates the leverage multiplier at work. National dwelling values grew approximately 9.6% annually to March 2026 (CoreLogic). That growth rate applied to a leveraged asset produces a fundamentally different outcome than the same growth rate applied to an unleveraged share portfolio.

Now layer on the income maths. A borrower at $50,000 income had access to approximately $200,000 in borrowing. The same person at $100,000 income accessed approximately $400,000-plus. If property prices are rising at 9.6% per year while the borrower spends eight years growing income, the target moves further away with every year the income growth is delayed.

The three compounding costs of wrong-order sequencing:

The framework is most powerful when started early. But each step remains available to readers at any point in their 20s. The argument is for urgency in starting the sequence, not panic about where someone currently sits within it.

Inflation-era portfolio construction becomes particularly relevant once the share market layering phase begins: with Australia’s headline CPI at 4.6% and savings account returns in the 4.5-5% range, the real return on cash held beyond the emergency fund buffer is effectively zero, reinforcing the sequencing logic that surplus capital should move into growth assets once the deposit and scheme eligibility steps are complete.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

For young Australians on modest incomes, the order of financial decisions matters more than the individual moves themselves. The sequencing framework in this guide, from emergency fund through super optimisation, income growth, income documentation, scheme-assisted property entry, and eventual share market diversification, provides a starting point for that ordering.

The most useful next step is the smallest one. Log into the ATO’s myGov portal this week to confirm the current super balance, verify employer contributions are being paid, and review the investment option allocation. It is the lowest-cost, highest-leverage action in the entire sequence, and it takes less than fifteen minutes.

From there, identify which step in the framework applies to the current financial position and direct all available surplus toward completing that single step before moving to the next. The sequence works because each completed step unlocks greater capacity for the one that follows.

—

The four-times income rule is a common benchmark most Australian lenders apply, meaning a borrower on a $50,000 salary can access roughly $200,000 in borrowing capacity, while a $100,000 salary supports approximately $400,000 in borrowing.

APRA requires lenders to stress-test repayment capacity at 3 percentage points above the assessed loan rate, which reduces borrowing capacity by approximately 15-20% compared to an assessment at the actual interest rate.

From 1 October 2025, the federal 5% Deposit Scheme has no income caps, no place limits, and higher property price caps by region (for example, $1,000,000 in Brisbane), and no Lenders Mortgage Insurance is required.

Lenders accept gig and casual income but require two years of consistent, documented earnings verified via ATO tax assessments, with major lenders such as Westpac and NAB applying a haircut of approximately 70-80% to gig income figures.

Young Australians can consolidate multiple super accounts to eliminate duplicate fees, switch to a high-growth investment option if their time horizon exceeds 20 years, and verify that employer contributions are being paid correctly through the myGov portal linked to the ATO.