Goldman Sachs Cuts 2026 Smartphone Shipment Forecast 10% on AI Crunch

22 hrs ago

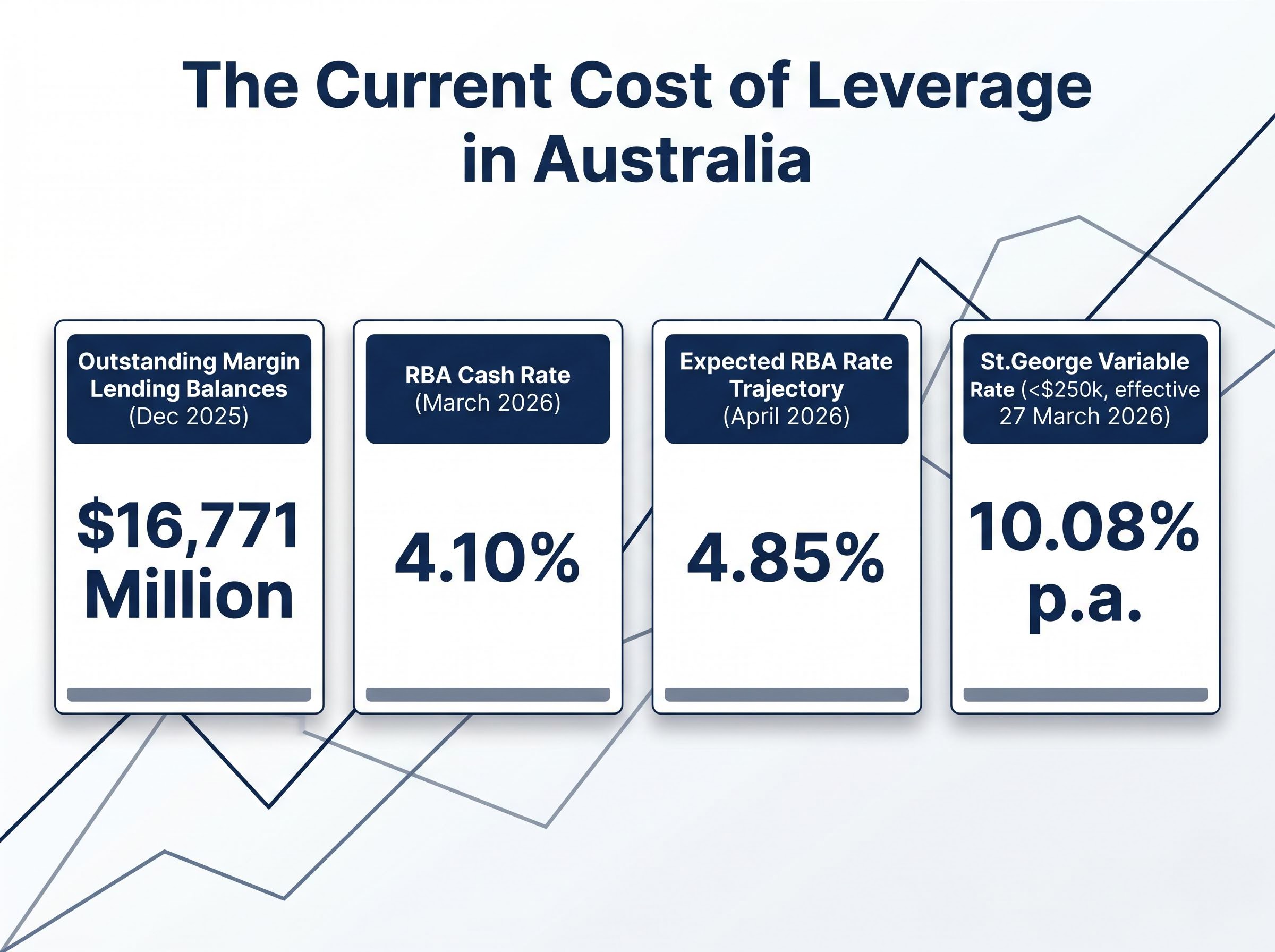

Australians currently hold $16,771 million in outstanding margin lending balances, according to the Reserve Bank of Australia’s D10 statistical tables as of December 2025. Yet many investors considering this strategy underestimate how quickly a market downturn can transform a calculated position into a forced sell-off.

With the RBA cash rate sitting at 4.10% as of March 2026 and variable margin loan rates at major providers reaching above 10% per annum, the arithmetic of borrowing to invest has shifted. The strategy’s appeal, amplified returns and faster portfolio growth, remains intact in theory. The conditions that make it viable or dangerous, however, are worth examining carefully.

What follows walks through exactly how margin lending works, what it genuinely offers Australian investors, what it can cost them, and how to honestly assess whether the risk-return trade-off suits a given situation.

Margin lending sits within the broader category of gearing: using borrowed money to increase the size of an investment position. In practice, a margin loan allows an investor to pledge existing assets as collateral in exchange for borrowed funds, which are then used to purchase additional securities.

The types of assets typically accepted as collateral include:

The loan is not open-ended. How much an investor can borrow, and the conditions under which the lender can demand repayment, both hinge on a single ratio.

The Loan to Value Ratio (LVR) is the mechanical centre of every margin loan. It measures the size of the loan relative to the total value of the assets securing it.

LVR = Loan Amount / Value of Collateral Assets

Each lender sets a maximum permissible LVR threshold for each approved security. If the ratio exceeds that threshold, the lender issues a margin call, demanding the borrower either deposit additional funds or sell holdings to bring the ratio back within acceptable limits.

Here is the insight that catches many borrowers off guard: the LVR moves when asset values change, not only when the borrower makes repayments or draws down additional funds. A 15% fall in the value of the collateral portfolio pushes the LVR upward even though the borrower has done nothing. That is precisely the mechanism through which a margin call is triggered, and understanding it is the foundation for everything that follows.

Margin lending carries genuine advantages for investors whose circumstances and risk appetite align with the product. Three benefits stand out:

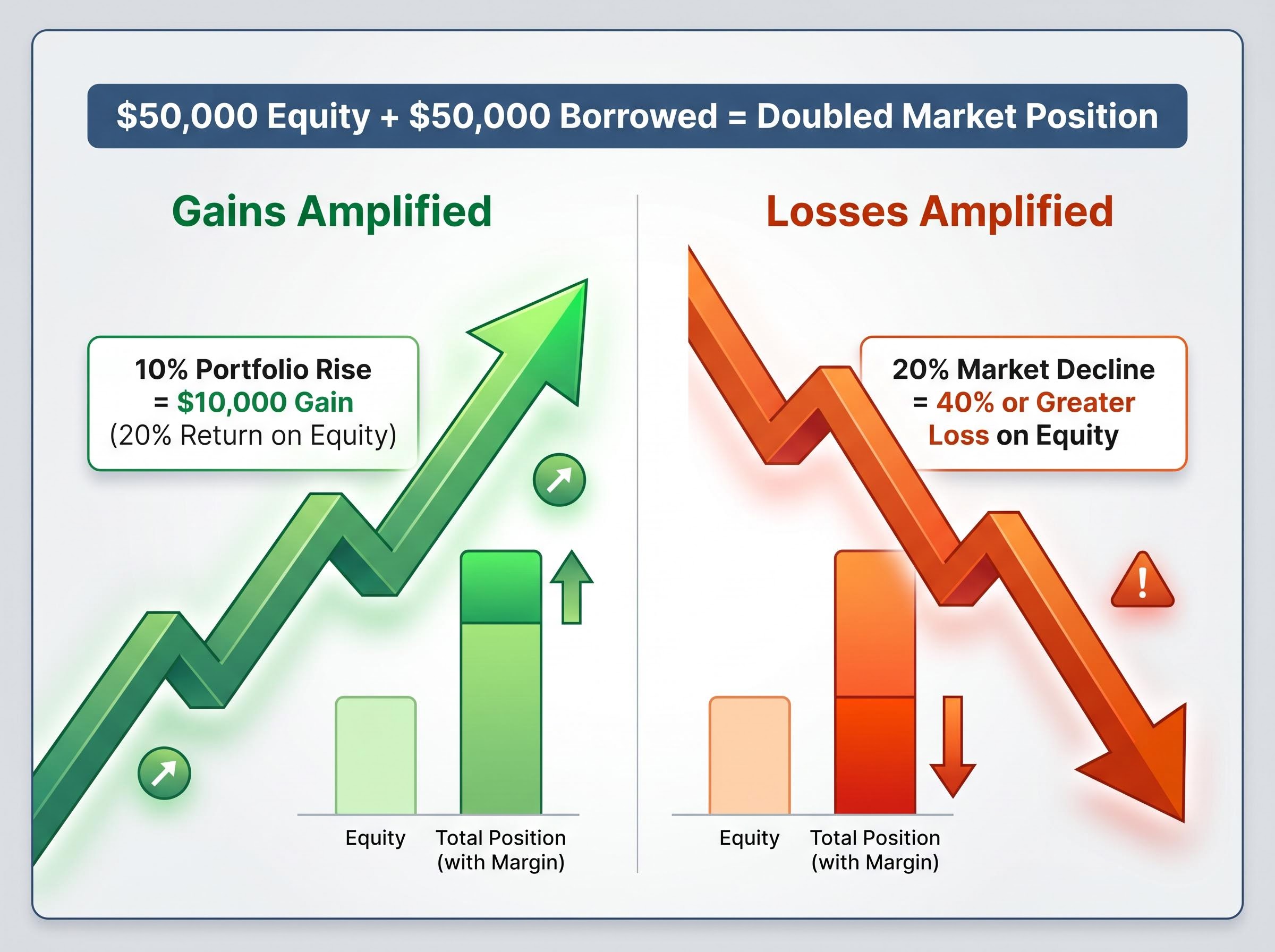

Amplified exposure is the primary draw. An investor with $50,000 in equity who borrows an additional $50,000 doubles their market position. If that portfolio rises 10%, the gain is $10,000 on a $50,000 equity base, a 20% return before interest costs. The leverage magnifies the outcome.

Diversification works alongside this. Rather than concentrating a smaller capital base in two or three positions, the additional borrowing capacity allows a broader spread across sectors or asset classes.

Portfolio diversification, one of the stated advantages of margin lending, has taken on new dimensions in 2026 as Australian retail investors shift capital toward international ETFs at a structural level, with international funds overtaking domestic products as the most purchased ETF category on major platforms for the first time on record.

Tax note: Interest on margin loans used to generate assessable income is generally deductible under Australian tax law. However, individual circumstances vary significantly, and professional tax advice should be sought before relying on this benefit.

Each of these advantages carries an implicit qualifier. Amplified returns are proportional to the level of gearing, which means they cut in both directions. The next section addresses what that looks like when markets move against a leveraged position.

The cost of leverage is not theoretical. At St.George’s current variable rate of 10.08% per annum for balances under $250,000 (effective 27 March 2026), investment returns must consistently clear that hurdle before a margin loan generates any net benefit.

Current cost benchmark: St.George’s variable margin lending rate sits at 10.08% per annum for balances under $250,000, effective 27 March 2026.

With the RBA cash rate at 4.10% (effective 18 March 2026) and market expectations as of April 2026 indicating possible further increases toward 4.85%, that hurdle rate could rise further still. The relationship between the cash rate and margin lending rates is direct: as one rises, the other follows.

Losses, meanwhile, are amplified symmetrically with gains. A fall in asset values reduces the portfolio while the loan balance stays fixed, eroding the investor’s equity far faster than an unleveraged position would experience. A 20% market decline does not produce a 20% loss for a geared investor; it can produce a 40% or greater loss on the equity component, depending on the gearing level.

| Risk Type | Description | Trigger Condition | Potential Severity |

|---|---|---|---|

| Interest cost pressure | Returns must exceed borrowing costs before any net gain is realised | Rising RBA cash rate, variable rate repricing | Moderate: erodes returns progressively |

| Amplified losses | Portfolio falls reduce equity faster than unleveraged positions | Market decline of any magnitude | High: losses magnified proportionally to gearing level |

| Margin calls | Forced deposit or sale when LVR exceeds lender threshold | LVR breach from falling asset values | High: forced selling at depressed prices locks in losses |

| Double gearing | Using home equity to fund a margin loan exposes both property and portfolio | Simultaneous property and equity market stress | Very high: both asset classes at risk concurrently |

The sequence is mechanical. When the LVR on a borrower’s account breaches the maximum threshold, the lender issues a margin call. The borrower must either deposit additional cash, transfer in additional approved securities, or sell existing holdings to reduce the ratio.

Failure to respond within the required timeframe results in the lender initiating a forced sale of assets. These forced sales overwhelmingly occur during falling markets, which means the investor sells at depressed prices, locking in losses that might otherwise have been temporary had the position been held through the downturn.

Double gearing compounds this further. Borrowers who use home equity (via a mortgage redraw or line of credit) as the funding source for a margin loan simultaneously expose both their property and their investment portfolio. ASIC’s responsible lending requirements include specific scrutiny of these arrangements, and for good reason: a downturn in either asset class can cascade into the other.

Regulatory and tax legislative changes can also shift the calculus after the fact. Tax deductibility assumptions that underpinned the original strategy can change with policy adjustments, retrospectively reducing the effectiveness of a margin lending position.

The level of regulatory attention directed at margin lending in Australia offers its own signal about the product’s risk profile. Lawmakers and regulators considered the risks serious enough to legislate specific protections.

Margin lending is regulated under the Corporations Act 2001 (Cth), with responsible lending obligations introduced in January 2011 specifically for margin lenders. The framework imposes several concrete requirements:

A 2016 ASIC review resulted in margin lenders improving their lending standards following regulatory scrutiny, indicating that oversight has had a direct effect on product quality and borrower protections.

ASIC’s consumer credit enforcement extends well beyond policy statements: a Federal Court order in April 2026 required Solvar subsidiary Money3 Loans to pay a $1.55 million penalty for National Consumer Credit Act contraventions, illustrating that lenders who fail responsible lending obligations face concrete legal consequences, not merely regulatory guidance.

ASIC’s margin lending regulatory framework introduced via the Corporations Legislation Amendment (Financial Services Modernisation) Act sets out the precise licensing obligations, responsible lending duties, and dispute resolution access requirements that margin lenders must satisfy before offering products to retail clients in Australia.

These protections are meaningful. An investor approaching a margin lender in Australia is dealing with a regulated entity that has legal obligations to assess suitability. But regulation does not eliminate risk. It reduces the likelihood of unsuitable lending; it does not prevent market losses. Understanding where the protections exist, and where their limits lie, helps investors engage with lenders from an informed position rather than a passive one.

Margin lending is explicitly not suitable for all investors. ASIC’s responsible lending framework requires lenders to make this assessment, but investors benefit from conducting their own evaluation before approaching a provider.

Four questions structure a honest self-assessment:

An investor who answers “no” to any of these is structurally unsuitable for margin lending, regardless of their long-term investment horizon or confidence in the market’s direction.

Conservative gearing benchmark: Financial adviser guidance recommends borrowing at 30-40% of maximum allowable LVR capacity, rather than at the limit. This provides a meaningful buffer against market falls and reduces the likelihood of margin calls while preserving the benefit of leverage.

The systemic dimension matters too. The RBA’s Financial Stability Review (March 2026) notes that leverage in non-bank financial institutions can exacerbate market volatility through deleveraging and fire sales during stress periods. Individual leverage decisions do not occur in isolation; they contribute to the broader dynamics that can intensify the very market falls that trigger margin calls.

The RBA Financial Stability Review published in March 2026 identifies leverage in non-bank financial institutions as a channel through which individual borrowing decisions can amplify broader market volatility, with deleveraging and fire sales during stress periods intensifying the price falls that initially triggered margin calls.

The numbers frame the present moment clearly. The RBA cash rate sits at 4.10%, with market expectations as of April 2026 pointing toward a possible trajectory to 4.85%. St.George’s variable margin lending rate is 10.08% per annum. Outstanding margin lending balances across Australia total $16,771 million.

Rate trajectory: With the RBA cash rate at 4.10% and possible further increases toward 4.85%, margin loan borrowing costs could rise further, compressing the return spread that leveraged investors depend on.

Those figures tell a layered story. The cost of leverage is materially higher than it was during the low-rate era that preceded 2022. The return threshold that a margin loan must clear before it generates any net benefit has risen accordingly. Yet $16,771 million in outstanding balances confirms that the market remains active; investors are still using margin loans, presumably because some of them have the risk tolerance, liquidity, and conservative gearing positions that make the trade-off work.

For investors with the right profile, margin lending remains a legitimate tool for portfolio growth and diversification within the Australian market. For investors without the financial resilience to absorb a margin call or the liquidity to respond to one, the current rate environment makes an already dangerous product more so.

Systematic investing strategies such as dollar-cost averaging into diversified index products have attracted renewed attention in 2026 precisely because the high-rate environment exposes the fragility of reactive, leverage-dependent approaches that depend on timing both market direction and interest rate movements correctly.

Three practical next steps apply:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

Margin lending is a form of gearing where an investor pledges existing assets as collateral to borrow funds for purchasing additional securities. The amount an investor can borrow is governed by the Loan to Value Ratio (LVR), and if asset values fall enough to breach the lender's maximum LVR threshold, a margin call is triggered requiring the investor to deposit more funds or sell holdings.

When a margin call is triggered, the borrower must either deposit additional cash, transfer in approved securities, or sell existing holdings to bring the LVR back within the lender's permitted limit. If the borrower does not respond in time, the lender can initiate a forced sale of assets, often at depressed market prices, locking in losses that might otherwise have been temporary.

As of late March 2026, St.George's variable margin lending rate sits at 10.08% per annum for balances under $250,000, meaning investment returns must consistently clear this hurdle before any net benefit is realised. With the RBA cash rate at 4.10% and possible further increases toward 4.85%, borrowing costs could rise further.

Interest on margin loans used to generate assessable income is generally tax deductible under Australian tax law, making it a potential advantage for eligible investors. However, individual circumstances vary significantly and professional tax advice should be sought before relying on this benefit, as policy changes can retrospectively alter the calculus.

Financial advisers recommend borrowing at only 30-40% of the maximum allowable LVR capacity rather than at the lender's limit, which provides a meaningful buffer against market falls. Investors should also maintain readily accessible cash reserves separate from their portfolio to meet a margin call at short notice if one is triggered.