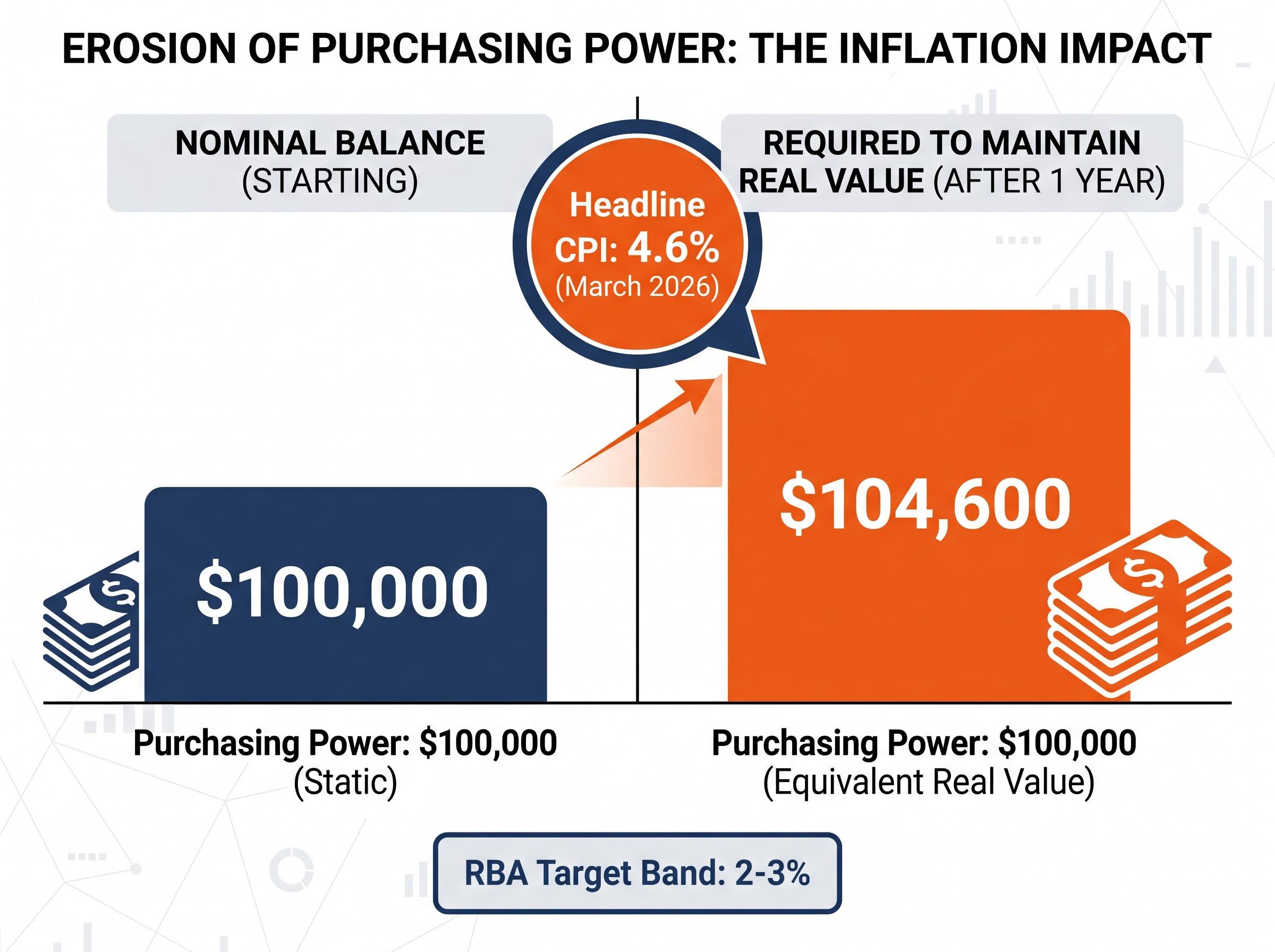

Australia’s headline Consumer Price Index (CPI) reached 4.6% for the 12 months to March 2026, released by the Australian Bureau of Statistics on 29 April 2026. The RBA’s cash rate climbed to 4.10% effective 18 March 2026. For Australian retail investors, the arithmetic is uncomfortable: holding cash in an ordinary savings account while inflation sits well above the RBA’s 2-3% target band quietly erodes purchasing power, even as the nominal balance stays flat.

The combination of persistent domestic inflation, geopolitical disruption from the Iran conflict pushing Brent crude toward $80-82 per barrel, and ongoing US tariff uncertainty has created conditions where standard portfolio assumptions no longer apply cleanly. This guide explains which asset classes hold up during inflationary periods and which do not, walks through six ASX-listed ETFs suited to different inflation-era objectives, and covers how disciplined investment approaches such as dollar cost averaging can turn market volatility from a threat into a structural advantage.

Why inflation erodes portfolios quietly and what to do about it

A 4.6% annual inflation rate means that $100,000 in purchasing power today requires $104,600 to maintain the same real value after one year. That erosion happens silently. The account balance does not change; the world around it simply gets more expensive.

The mechanism by which inflation erodes purchasing power operates across every asset class, not just cash: equities face margin compression, fixed-rate bonds lose real yield, and even property can underperform when rising rates push up borrowing costs faster than rents adjust.

“Australia’s headline inflation reached 4.6% for the 12 months to March 2026, more than double the top of the RBA’s 2-3% target band.”

Moderate inflation is normal. Central banks target 2-3% because mild price growth encourages spending and investment. The problem arises when inflation sits materially above that band for sustained periods. According to IMF research, each additional percentage point of inflation beyond 3% reduces real GDP growth by approximately 0.1-0.2 percentage points, compounding the drag on both the economy and portfolio returns.

Three drivers are currently at work in Australia:

- Demand-pull inflation: Strong household spending and tight labour markets have kept domestic demand elevated, pushing prices higher across services and discretionary goods.

- Cost-push inflation: Brent crude at $80-82 per barrel in March 2026, driven by the Iran conflict, has fed directly into higher petrol, transport, and manufacturing costs.

- Currency depreciation: A weaker Australian dollar against the US dollar has increased the cost of imported goods, from electronics to industrial inputs.

With trimmed mean CPI at 3.3%, the underlying inflationary pulse remains above target even when volatile items are stripped out. Waiting for inflation to resolve on its own carries a measurable cost. Understanding that cost is the precondition for taking an active portfolio response seriously.

The ABS CPI release for March 2026 confirmed both the 4.6% headline figure and a trimmed mean of 3.3%, meaning the underlying inflationary pulse remains above the RBA’s target band even after stripping out the most volatile price movements.

When big ASX news breaks, our subscribers know first

How the RBA’s higher-for-longer stance reshapes the investment landscape

The RBA raised the cash rate from 3.85% (effective 4 February 2026) to 4.10% (effective 18 March 2026). Two consecutive increases are not an isolated adjustment; they signal a sustained tightening posture in response to inflation that has refused to ease as quickly as forecast.

The RBA monetary policy decision statement from 18 March 2026 set out the Board’s inflation outlook and the reasoning behind the move to 4.10%, signalling that further tightening remains possible if domestic price pressures do not ease in line with forecasts.

The Taylor Rule, a widely referenced framework for assessing central bank policy, suggests that rates need to rise by approximately 1.5 percentage points for every 1 percentage point inflation sits above target to genuinely tighten financial conditions. Anything below that threshold may leave policy settings more accommodative than they appear. By that measure, the RBA’s current rate, while the highest in over a decade, may still be insufficient to bring inflation back within band quickly.

Morgan Stanley’s base case foresees potential rate cuts by mid-to-late 2026, but only if unemployment rises and inflation eases meaningfully. The Iran oil shock complicates that scenario directly: higher energy costs feed into headline CPI and make the disinflation path slower and less certain.

Oil futures markets remain in backwardation, a structure where near-term contracts price higher than longer-dated ones, signalling that the market expects the current supply disruption to be temporary. Historical patterns suggest rate normalisation following supply shocks typically occurs within six to twelve months. That said, history also shows that the cost of getting inflation under control can be steep: when the US Federal Reserve raised rates aggressively between 1980 and 1982, inflation fell from 14% to 3%, but unemployment climbed above 10%.

What a soft landing would mean for your portfolio

Soft landings, where inflation returns to target without triggering a recession, are historically rare. The 1990s US experience remains the most cited exception. Several disinflationary forces are still at work globally:

- AI-driven productivity gains are reducing costs in services and logistics sectors.

- Falling US rents are easing a persistent contributor to American inflation, reducing pressure on global rate expectations.

- Softening wage growth in several developed economies is narrowing the services inflation gap.

- Chinese export redirection due to US tariffs is increasing supply of manufactured goods into non-US markets, including Australia, potentially lowering imported goods prices.

If inflation eases faster than expected and the RBA begins cutting, rate-sensitive assets such as bonds could see capital gains on top of their income yields. ETFs like VBND and CRED would benefit in that scenario, adding upside to the income case. The current higher-for-longer environment, however, means investors should weight duration risk carefully until that path becomes clearer.

Which asset classes hold their value when inflation runs hot

Not all asset classes respond to inflation the same way. Commodities, real assets, and equities with pricing power have historically outperformed during inflationary periods, while long-duration fixed-rate bonds tend to underperform as real yields erode. Building an inflation investment strategy requires understanding these dynamics before selecting specific products.

“Gold hit approximately $4,702 per ounce on April 27, 2026, near all-time highs, reflecting its traditional role as a store of value during inflationary and geopolitical uncertainty.”

Ray Dalio’s all-weather portfolio framework allocates approximately 7.5% to commodities and 7.5% to gold, with the rationale that both stocks and bonds can underperform simultaneously in high-inflation environments. That framework has gained renewed attention among Australian commentators in 2026, with gold trading at approximately $4,587.60 per ounce as of 30 April 2026 and silver at approximately $71.90 per ounce as of 29 April 2026, surpassing the historical $50 per ounce ceiling from prior cycles.

The nuance for equities is pricing power. Companies that can pass rising input costs through to consumers preserve their margins; those that cannot see margin compression accelerate. Quality-factor equity selection specifically targets this characteristic.

Identifying pricing power on the ASX involves screening for companies with return on equity above 15%, low debt-to-equity ratios, and demonstrated ability to expand margins during prior inflationary periods, criteria that apply equally when selecting individual stocks to complement an ETF core.

Global ETF inflows of $722.6 billion in Q1 2026, with March alone contributing $174.42 billion, reflect a broad investor shift toward diversified, liquid vehicles during volatile conditions.

| Asset Class | Inflation Behaviour | Key Risk | Australian Example |

|---|---|---|---|

| Commodities / Gold | Tends to rise with inflation; physical stores of value | Volatile; no income yield | Gold near $4,588/oz; ASX resource sector ETFs |

| Quality International Equities | Companies with pricing power preserve margins | Currency risk; valuation compression in downturns | QUAL (VanEck MSCI International Quality ETF) |

| Short-Duration Bonds | Lower sensitivity to rate rises; capital preservation | Modest yield compared to longer-duration alternatives | ISEC (iShares Enhanced Cash ETF) |

| Long-Duration Fixed Bonds | Underperforms as rates rise; real yields erode | Capital losses if rates stay elevated | VBND in current environment carries duration risk |

| Cash / Money Market | Preserves nominal value; real return negative when rates sit below CPI | Purchasing power erosion over time | AAA (BetaShares High Interest Cash ETF) |

Dollar cost averaging as a practical inflation-era investment method

Knowing which ETFs to hold is one decision. Knowing how to build those positions during volatile markets is another.

Dollar cost averaging (DCA) involves investing a fixed dollar amount at regular intervals regardless of market price. When prices fall, the fixed amount purchases more units; when prices rise, it purchases fewer. Over time, this produces an average entry cost that smooths out the impact of short-term volatility.

Enhanced DCA takes this further: increasing the investment amount during significant price dislocations or pullbacks to capture more upside. ASX volatility throughout early 2026, driven by US tariff threats and the Iran oil shock, created multiple such dislocations, conditions where enhanced DCA would have been directly applicable.

“Consistent investing through market dislocations, and increasing investment amounts during significant price declines, is recommended to capture more of the potential upside.” (Selfwealth by Syfe)

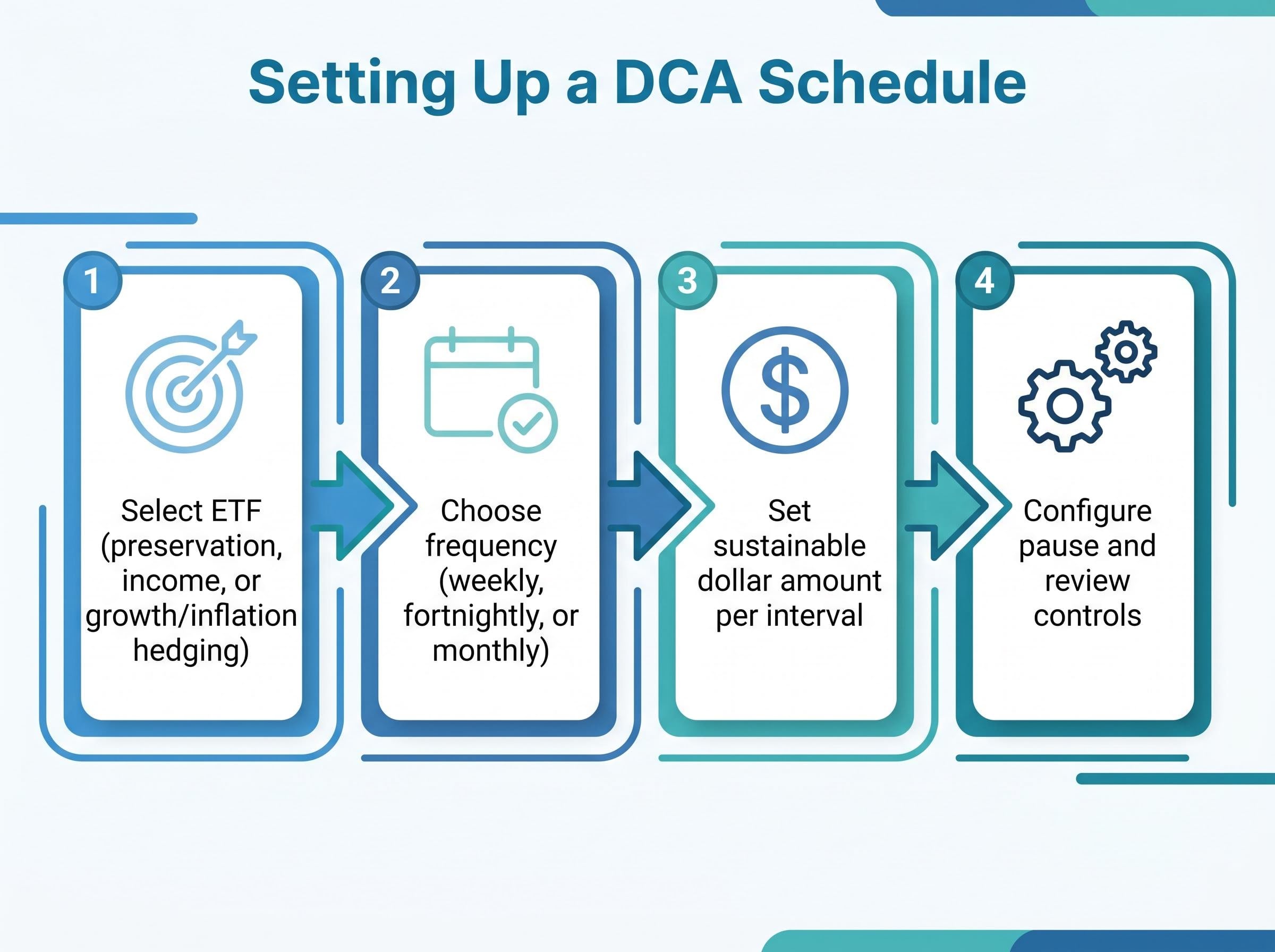

Setting up a DCA schedule involves four steps:

- Select the ETF or ETFs that align with the chosen portfolio objective (preservation, income, or growth and inflation hedging).

- Choose the investment frequency: weekly, fortnightly, or monthly, ideally aligned with pay cycles.

- Set the dollar amount per interval, ensuring it is sustainable across multiple months without requiring withdrawal.

- Configure pause and review controls so the schedule can be adjusted if circumstances change, without abandoning the strategy entirely.

The Selfwealth Auto-Invest feature supports weekly, fortnightly, or monthly recurring investments in selected ASX stocks or ETFs, executed as market orders. Users can pause, review, or modify schedules through the Portfolio or Orders sections of the app. Community popularity data and insights surfaced within the platform can assist with selection decisions.

Automating this process removes the psychological burden of market timing, which is particularly valuable during volatile inflationary periods when short-term anxiety is most likely to override a sound long-term strategy.

For investors wanting a step-by-step implementation framework, our dedicated guide to dollar-cost averaging mechanics covers how automated periodic investments reduce average entry costs over time, with worked examples across different investment frequencies and platforms available to Australian investors.

Six ASX-listed ETFs suited to the current inflationary environment

Each of the following six ETFs serves a specific function in an inflation-aware portfolio. All are listed on the ASX and accessible to Australian retail investors through standard brokerage accounts.

Income and capital preservation: AAA, ISEC, and CRED

In a 4.10% cash rate environment, income-generating instruments that prioritise capital security are more compelling than in prior years when rates sat near zero.

AAA (BetaShares Australian High Interest Cash ETF) holds Australian dollar interest-bearing bank deposits. Its inflation-era role is straightforward: provide a base of high capital security while generating income linked to prevailing deposit rates. The trade-off is that returns will trail inflation if rates remain below headline CPI.

ISEC (iShares Enhanced Cash ETF) invests in short-term money market instruments and short-duration corporate bonds. It targets a modestly higher yield than deposit-based ETFs by accepting slightly more credit and duration exposure, while remaining positioned at the conservative end of the fixed income spectrum.

CRED (BetaShares Australian Investment Grade Corporate Bond ETF) holds senior fixed-rate bonds from high-quality Australian corporations. It offers equity-comparable income with a positioning advantage when rates peak: as the RBA eventually moves to cut, existing fixed-rate bonds gain in capital value. The risk is that CRED carries more duration exposure than AAA or ISEC, making it less appropriate for investors prioritising capital preservation over income maximisation in the near term.

Global diversification and quality: VGS and QUAL

The ASX is heavily concentrated in banks and resources. International exposure reduces that concentration risk and provides access to sectors and companies underrepresented domestically.

VGS (Vanguard MSCI Index International Shares ETF) tracks over 1,000 large companies across developed markets excluding Australia, with an approximate yield of 1.69%. It serves as a core diversification holding, spreading risk across geographies, currencies, and sectors that behave differently from the Australian market during inflationary periods.

QUAL (VanEck MSCI International Quality ETF) selects highly profitable global companies with strong balance sheets, low debt, and demonstrated pricing power. VanEck has recommended QUAL and its AUD-hedged counterpart, QHAL, as core holdings for flight-to-quality portfolios in 2026. When margin compression is a risk across the broader market, quality-factor selection specifically targets the companies best positioned to maintain earnings.

| ETF (ASX Code) | Issuer | Inflation-Era Role | Key Feature | Risk Consideration |

|---|---|---|---|---|

| AAA | BetaShares | Capital security base | AUD bank deposits; high capital preservation | Returns may trail inflation |

| ISEC | iShares | Enhanced cash yield | Short-duration money market and corporate bonds | Modest credit risk above pure cash |

| CRED | BetaShares | Income with rate-peak upside | Senior investment-grade Australian corporate bonds | Duration risk if rates stay elevated longer |

| VBND | Vanguard | Global bond diversification | Investment-grade global debt, AUD hedged | Duration risk; underperforms if rates rise further |

| VGS | Vanguard | Core international equity diversification | 1,000+ developed market companies ex-Australia | Currency and global equity market risk |

| QUAL | VanEck | Quality-factor inflation resilience | High-profitability, low-debt global companies | Quality premium may compress in risk-on rallies |

Commodities and gold exposure can complement these six holdings. Resource-sector ETFs on the ASX offer direct commodity exposure, and the Dalio all-weather framework’s 7.5% allocation to each of commodities and gold provides a reference point for sizing that position.

Building an inflation-aware portfolio that can adapt as conditions change

Portfolio construction during an inflationary period is a function of individual objectives, not a single formula. Three broad tilts illustrate how the same set of ETFs can be weighted differently depending on what the investor is trying to achieve:

- Preservation focus: Lean toward AAA and ISEC for capital security, with a smaller allocation to CRED for income. Minimise duration risk. Suitable for investors who need to protect a defined sum over the next 12-18 months.

- Income focus: Weight toward CRED and VBND for bond income, complemented by VGS for dividend yield. Accept moderate duration risk with the understanding that rate cuts, if they materialise, would add capital gains. Suitable for investors seeking regular cash flow.

- Growth and inflation-hedge focus: Anchor in QUAL and VGS for equity exposure to companies with pricing power, add commodity and gold exposure through resource-sector ETFs, and maintain a smaller cash buffer via AAA. Suitable for investors with a longer time horizon who can absorb short-term volatility.

The higher-for-longer rate environment changes the trade-off between duration risk and income. Shorter-duration instruments are more appropriate now, with the option to extend duration if and when rate cuts materialise. Maintaining liquidity and flexibility is particularly valuable given the conditional nature of the 2026 rate outlook.

Vanguard Australia’s 2026 guidance favours globally diversified portfolios combining bond and international equity exposure (a VBND plus VGS framework) as a buffer against domestic inflation and rate risk. VanEck’s 2026 recommendation centres QUAL and QHAL as core quality holdings in uncertain rate environments. The Dalio all-weather model provides a reference for commodities and gold sizing.

When to consider rebalancing your inflation-era allocation

Rather than reviewing on a fixed calendar, watch for specific signals that the environment has shifted:

- RBA rate cut announcement: A move to lower the cash rate below 4.10% would signal the tightening cycle has ended. Consider extending bond duration and increasing fixed-rate exposure through CRED or VBND.

- CPI returning to within the 2-3% target band: If headline inflation drops below 3%, the urgency of inflation hedging reduces. Rebalance away from commodities and toward growth-oriented equity positions.

- A sustained shift in the oil price trajectory: If Brent crude falls materially below $70 per barrel and stays there, one of the primary cost-push inflation drivers weakens. Reassess the weighting given to commodity and resource exposure.

These are not predictions. They are decision points. Identify which signals matter most for the chosen portfolio tilt, and act when they arrive rather than waiting for certainty across all three.

The case for acting now rather than waiting for the all-clear

With CPI at 4.6% and the cash rate at 4.10%, real returns on passive cash holdings are negative in purchasing power terms. Every month of inaction carries a measurable cost that compounds.

Global ETF inflows of $722.6 billion in Q1 2026, with $174.42 billion in March alone, suggest that sophisticated investors are already repositioning rather than waiting for the all-clear. That signal is worth noting: when capital moves at that scale and pace toward diversified, liquid vehicles, it reflects a collective judgment that the time to act is before conditions fully resolve, not after.

Australia’s 50% CGT discount for patient investors who hold assets beyond 12 months functions as a structural incentive built into the tax code: the government effectively co-funds the cost of staying invested through volatility by halving the tax rate on long-term gains compared to assets sold within the year.

The practical next step is straightforward. Identify one objective from the three outlined above: preservation, income, or growth and inflation hedging. Select the corresponding ETF or ETFs. Set up a DCA schedule through a platform such as Selfwealth Auto-Invest. Begin building exposure at regular intervals, and increase the amount during dislocations if circumstances allow.

Waiting for inflation to return to target, for the RBA to cut, or for geopolitical uncertainty to clear is itself a portfolio decision. It is a decision to accept negative real returns in exchange for the comfort of certainty that may not arrive for months.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—