How Zero Commissions Changed the Maths on Thematic ETFs

2 hrs ago

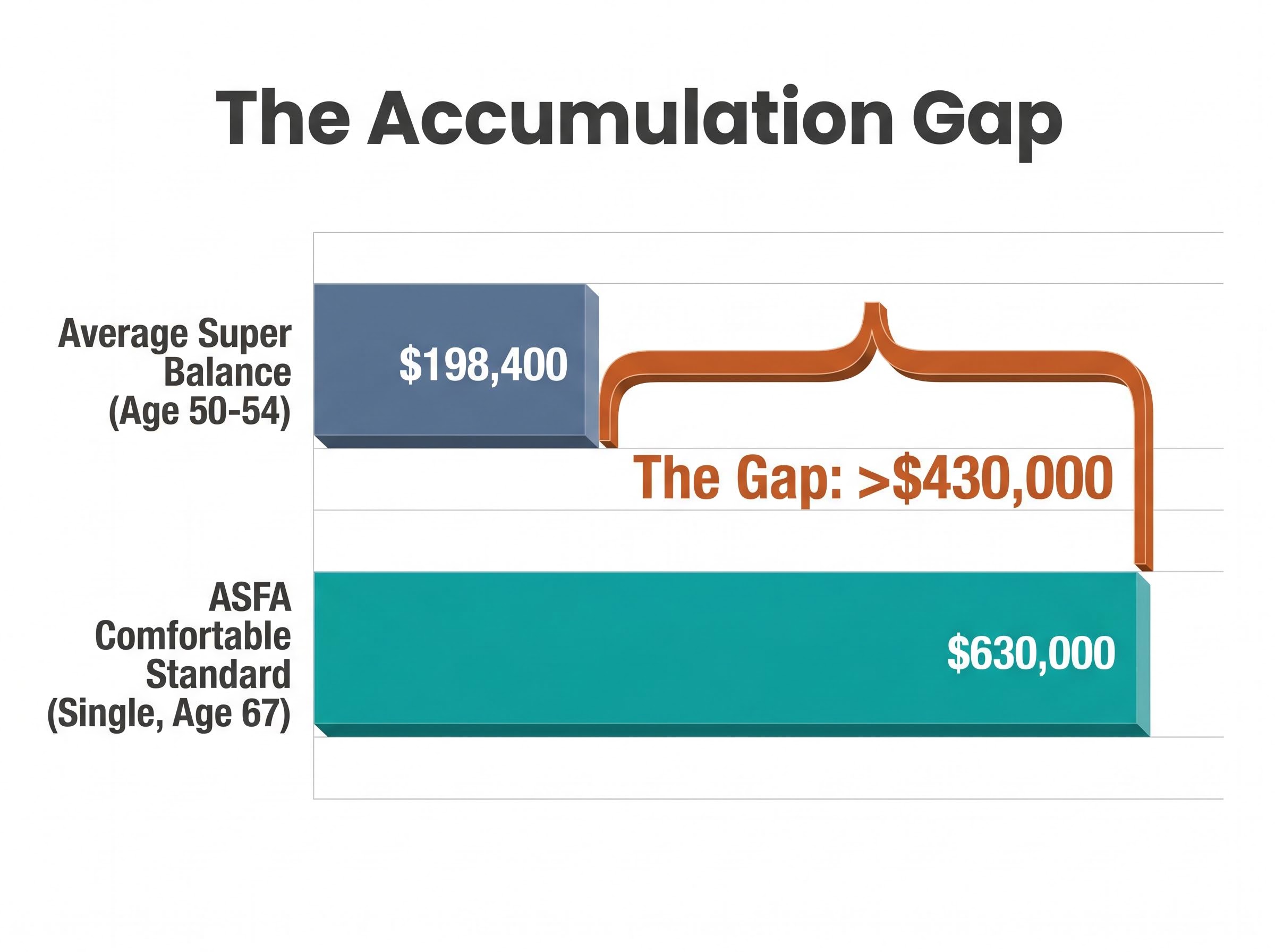

Most Australians assume superannuation is quietly sorting out their retirement. The numbers say otherwise. The typical person aged 50-54 holds around $198,400 in super. The Association of Superannuation Funds of Australia (ASFA) puts the comfortable retirement threshold for a single person at $630,000. That gap, more than $430,000, does not close by accident.

With the Super Guarantee (SG) now at 12% and concessional contribution caps lifted to $30,000 per year from July 2025, the policy architecture is improving. But policy changes do not automatically translate into individual adequacy. The distance between what most Australians accumulate and what they actually need is not primarily an income problem. It is a comprehension problem: most people have never seen what their balance needs to look like at 10, 20, and 30-year intervals to fund a retirement that does not run dry.

What follows shows the maths in plain terms. Readers will see what typical balances look like by age group, what compound growth actually produces over time, where most balances start falling short, and what specific moves remain available to change the trajectory.

The ASFA Retirement Standard, updated quarterly for inflation, puts a specific number on a comfortable retirement. As of the February 2026 update, the figures are:

The ASFA Retirement Standard is updated quarterly to account for inflation and sets specific lump sum and annual spending benchmarks for homeowner retirees, making it the reference framework most commonly used by Australian financial planners when assessing retirement adequacy.

| Household type | Lump sum required at 67 | Annual spending |

|---|---|---|

| Single | $630,000 | $54,840 |

| Couple | $730,000 | $77,375 |

Those figures carry built-in assumptions worth understanding:

Now set those thresholds against what Australians actually hold. ATO-derived data shows the average super balance for those aged 50-54 is approximately $198,400. For those aged 30-34, the figure is approximately $49,800.

These are averages, and averages are generous. They are skewed upward by high-balance holders. Median balances, the point at which half of all holders sit below, are materially lower. The gap between the ASFA standard and what most Australians have accumulated is not a rounding error. It is structural.

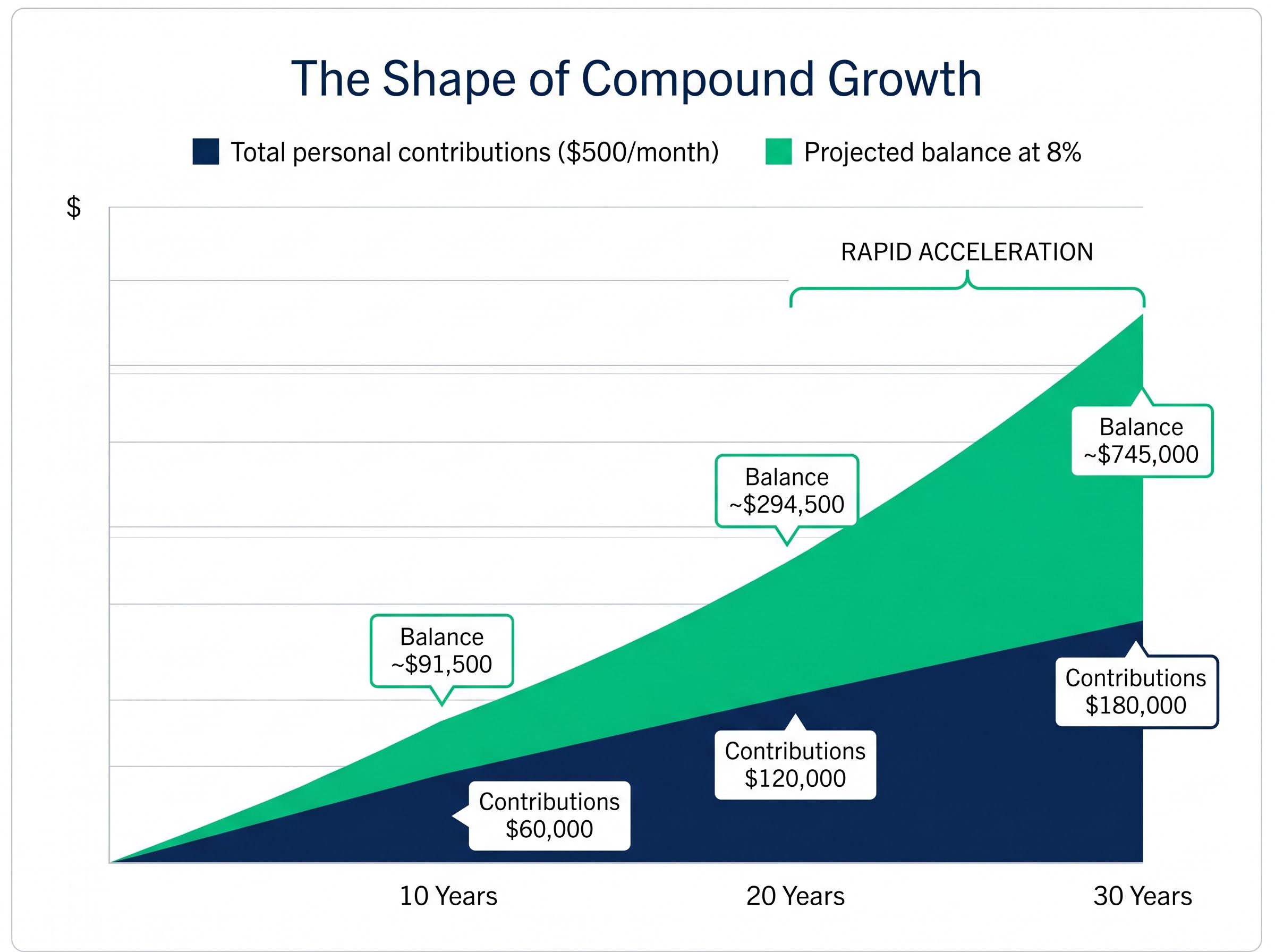

The shape of compound growth is the part most people misunderstand. It is not a straight line. It is a curve that stays frustratingly flat for years before accelerating sharply in the final stretch.

Compound growth mechanics follow a consistent pattern across asset classes and time periods: the second decade of an investment generates nearly double the dollar gains of the first decade on the same initial capital, which is the mathematical explanation for why the final decade in the 30-year projection above produces more than the first two decades combined.

Consider $500 per month invested consistently. At an 8% annual return, a figure consistent with the decade-long average for balanced superannuation funds, the trajectory looks like this:

| Years invested | Total personal contributions | Projected balance at 8% | Projected balance at 10% |

|---|---|---|---|

| 10 years | $60,000 | ~$91,500 | ~$102,000 |

| 20 years | $120,000 | ~$294,500 | ~$379,000 |

| 30 years | $180,000 | ~$745,000 | ~$1,130,000 |

$500 a month, left alone for 30 years at 8%, becomes approximately $745,000. The first 20 years of that only built $294,500.

The final decade produced more than the first two decades combined. That is not a quirk of this particular example. It is how compounding works: the return pool itself is growing, so each year’s gains are calculated on a larger base. Growth accelerates as the base expands.

This also means interruptions are disproportionately costly. Pausing contributions or withdrawing early does not just remove the capital taken out. It destroys all future growth that capital would have generated.

The 8% figure used above reflects a conservative blended benchmark. Balanced super funds have averaged approximately this rate over the preceding decade. ASX total returns, including dividends, have historically delivered approximately 9-10% per annum over 30-year periods.

The distinction matters for planning. Gross ASX returns of 9-10% do not translate directly into net portfolio growth. After fund management fees and inflation, net super fund returns typically land closer to 7-8%, which is why the more conservative figure is appropriate for projection purposes.

Growth asset allocation over a 30-year horizon absorbs drawdowns that would be damaging over a 3-year window; Australian shares delivered approximately 7.55% annualised over 20 years while cash produced a negative real return after inflation, which is why remaining in a default balanced option at age 35 represents a more consequential choice than most members recognise.

The same gap between current balance and retirement target means fundamentally different things depending on when a person encounters it. Two cohorts illustrate why.

The carry-forward concessional cap is the highest-leverage mechanism available to the 52-year-old cohort, but it has a hard deadline: unused cap amounts from the 2020-21 financial year expire on 30 June 2026, meaning any member who has not yet deployed that capacity will lose it permanently at the end of this financial year.

Around 55-60% of Australian retirees receive the Age Pension, in full or in part. Super alone, for the majority, is not enough.

That figure, drawn from Department of Social Services data, confirms what the projections suggest. For the 52-year-old cohort, the Age Pension is not a backup plan. It is already part of the baseline assumption.

Superannuation is the most tax-efficient accumulation vehicle available to most Australians, but it is not the only one. The three primary channels form a layered system, each with distinct tax treatment and accessibility constraints.

| Vehicle | Tax on contributions | Tax on earnings | Accessibility | Annual cap / limit |

|---|---|---|---|---|

| Salary sacrifice (concessional super) | 15% | 15% (up to 30% for some high earners) | Preserved until age 60 | $30,000/year |

| After-tax super (non-concessional) | Nil (already taxed) | 15% | Preserved until age 60 | $120,000/year (up to $360,000 via bring-forward) |

| ETFs / brokerage account | N/A | Marginal income tax rate on dividends; CGT on disposal | Accessible anytime | No cap |

Salary sacrifice is the sharpest tool for most workers. An $80,000 earner salary sacrificing $500 per month pays 15% contributions tax on that amount inside super, versus a 32.5% marginal income tax rate outside it. The tax saving alone accelerates accumulation meaningfully over a 15-30 year horizon.

For 52-year-olds with balances under $500,000, the carry-forward concessional cap provision is particularly relevant. Eligibility conditions include:

The ATO concessional contributions cap rules also govern carry-forward eligibility, requiring a super balance below $500,000 at the prior 30 June and allowing unused cap amounts from up to five prior financial years to be contributed above the standard $30,000 annual limit in a single year.

Broad index ETFs (ASX 300, global equities, with management fees typically below 0.2%) fill a different role. They are less tax-efficient than super but accessible before preservation age 60, making them appropriate for investors targeting financial independence earlier or building liquidity outside the super lock-up.

The maths above is not new. Most Australians have encountered compound growth projections in some form. The question is why so few act on them.

The answer has a name: present bias. It is the tendency to prioritise immediate consumption over long-term saving, and it is not a character flaw. It is a predictable cognitive pattern that affects the majority of people when faced with a trade-off between spending today and accumulating wealth decades from now. Low uptake of salary sacrifice, despite the 15% contributions tax rate advantage, is consistent with this pattern.

Consider the scale of what is being deferred. $500 per month is approximately $16.50 per day. The amount is not abstract. It is tangible, and that is precisely why it feels difficult to redirect.

Three specific failure modes recur:

The $209,000 difference between a 7.5% and a 6.5% net return over 30 years is not market risk. It is fee drag. It is avoidable.

That figure comes from a straightforward projection: $100,000 growing at 7.5% net over 30 years reaches approximately $870,000. The same balance at 6.5% net (reflecting 1% higher annual fee drag) reaches approximately $661,000. The gap is not a matter of investment selection. It is a matter of structural cost.

The $209,000 fee drag figure above assumes a clean 1% cost differential, but hidden super fees embedded in fund architecture, including pooled capital gains tax drag, swap-based index financing spreads, and franking credit dilution, sit entirely outside the headline rate and never appear as a line item on any member statement.

Automating contributions immediately after each pay cycle is not a “good habit” tip. It is the structural response to a structural problem. Strategies that require active monthly decisions fail because present bias ensures competing priorities win. Automation removes the decision point entirely.

Knowing the ASFA target is one thing. Knowing whether the current balance is tracking toward it is another. The following benchmarks represent approximate super balances, by age, consistent with reaching the $630,000 single comfortable standard at age 67, assuming 7.5% net returns and ongoing SG contributions.

| Age bracket | Approximate target (single) | Approximate target (couple) |

|---|---|---|

| Mid-30s | $80,000 – $120,000 | $95,000 – $140,000 |

| Mid-40s | $180,000 – $280,000 | $210,000 – $320,000 |

| Mid-50s | $350,000 – $450,000 | $400,000 – $520,000 |

These are diagnostic reference points, not pass/fail thresholds. They indicate whether a balance is broadly tracking, running ahead, or falling behind.

The levers available differ by cohort:

The policy environment is also moving toward better support at the decumulation stage. The Retirement Income Covenant, now enacted law with best practice principles released in February 2026, requires superannuation trustees to develop a retirement income strategy for members. This means funds are now formally accountable for helping members draw down their savings effectively, not just accumulate them.

The gap between typical Australian super balances and adequate retirement funding is not an income problem for most workers. It is a compounding problem. And compounding problems have a narrowing window of efficient solutions. The average balance at 30-34 is approximately $49,800. At 50-54, it is approximately $198,400. The ASFA comfortable threshold for a single person at 67 is $630,000. Every year of inaction widens the gap at an accelerating rate.

Rather than carrying these numbers as a mental calculation, the ASIC MoneySmart retirement planner (moneysmart.gov.au) provides a free, verified tool for modelling individual projections based on actual balance, contribution rate, and expected retirement age.

The Age Pension exists as a floor. Approximately 55-60% of Australian retirees rely on it, in full or in part. But reliance on it is a planning outcome, not a planning strategy. The difference between a funded retirement and a partially-funded one is determined by decisions made years before retirement arrives.

The most expensive retirement decision most Australians make is not a bad investment choice. It is waiting another year to start.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced above are subject to market conditions and various risk factors. Past performance does not guarantee future results.

The ASFA Retirement Standard sets the lump sum required for a comfortable retirement at $630,000 for a single person and $730,000 for a couple, assuming the retiree owns their home outright and can spend approximately $54,840 or $77,375 per year respectively.

According to the benchmarks in this article, a single person in their mid-50s should have approximately $350,000 to $450,000 in superannuation to be on track for a comfortable retirement at 67, yet the ATO-derived average for Australians aged 50-54 is only around $198,400.

From July 2025, the concessional contributions cap increased to $30,000 per year, and Australians with super balances below $500,000 may also be able to use carry-forward provisions to contribute unused cap amounts from up to five prior financial years above that standard limit.

Salary sacrifice contributions are taxed at 15% inside superannuation, compared to the standard marginal income tax rate of 32.5% for an $80,000 earner outside super, meaning the tax saving alone meaningfully accelerates wealth accumulation over a 15-30 year horizon.

Present bias is the tendency to prioritise immediate spending over long-term saving, and it is the primary behavioural reason most Australians fail to act on compound growth projections they already understand; automating contributions removes the recurring decision point that present bias exploits.