Why Imugene’s Fast Track Win in Marginal Zone Lymphoma Matters

46 mins ago

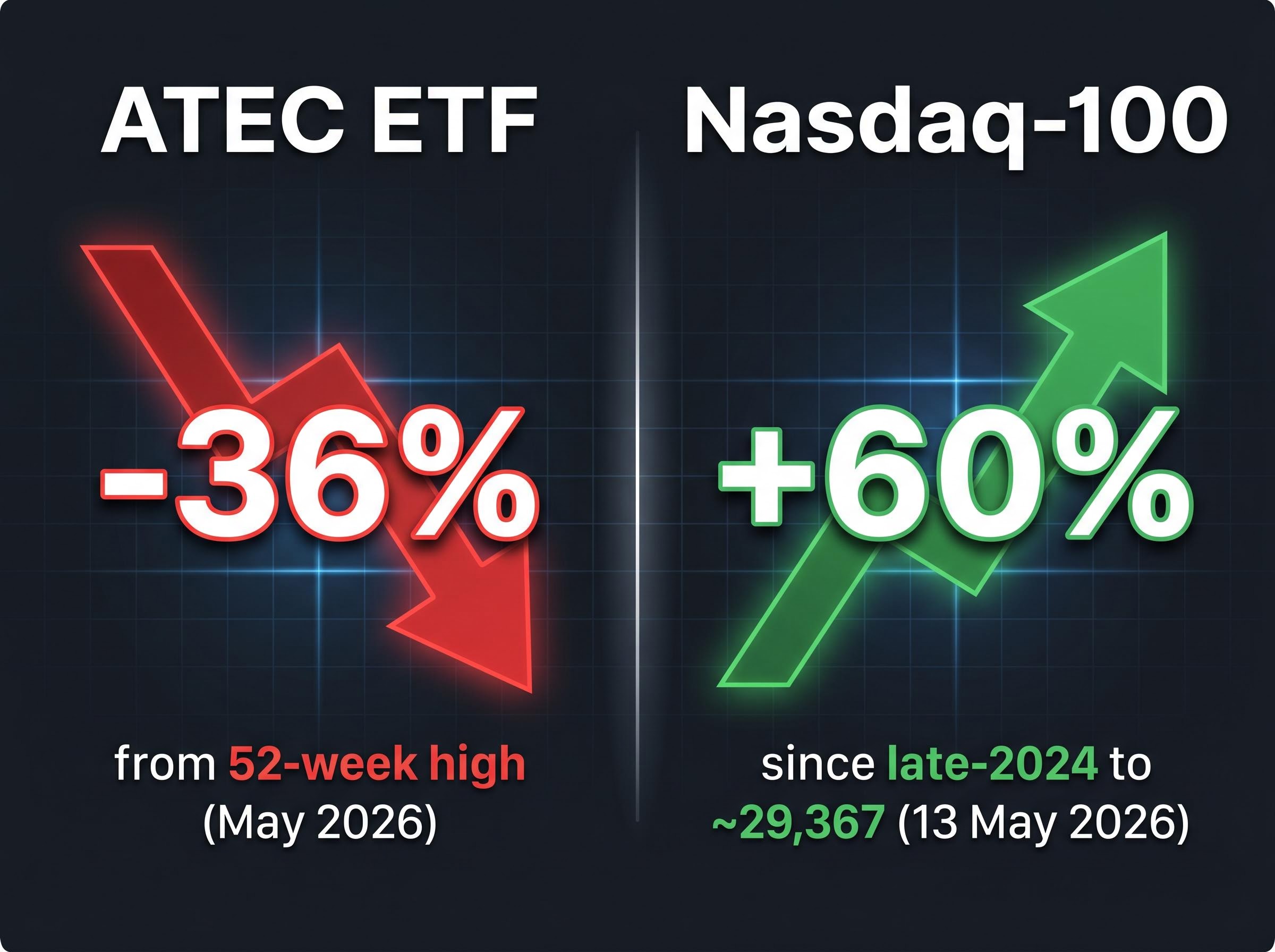

The BetaShares Australian Technology ETF (ASX: ATEC) is sitting approximately 36% below its 52-week high as of May 2026. Over the same stretch, the Nasdaq-100 has surged roughly 60% from its late-2024 levels, widening the gap between global mega-cap tech and Australia’s domestic technology sector to its most visible point in years. That divergence raises a direct question for investors evaluating the ATEC ETF: is the drawdown a signal that the Australian tech thesis has broken, or is it a cyclical repricing that has created a lower entry point into structurally growing businesses? What follows is a six-part analytical framework covering what the fund holds, why it fell, how its underlying businesses generate revenue, whether the structural case remains intact, how it compares to alternatives, and who the current price level is actually suited for.

ATEC is a concentrated domestic tech ETF with a management expense ratio of 0.48% p.a., tracking ASX-listed technology companies across several distinct sub-sectors. It is not a proxy for global tech. It carries no US mega-cap exposure, no Alphabet, no Nvidia, no Microsoft. Its character is entirely domestic, growth-oriented, high-beta, and rate-sensitive.

BetaShares positions the fund explicitly as a component within a diversified portfolio rather than a standalone holding. The volatility is a design feature, not a defect.

Despite the 36% drawdown, investor appetite has persisted. ATEC recorded approximately $193.7 million in year-to-date inflows during 2026, a signal that capital has been flowing into the fund even as its unit price has compressed.

The fund spans six identifiable sub-sectors, each carrying a different risk and return profile:

Xero, NextDC, and TechnologyOne are the primary weight anchors. Codan, SiteMinder, and Megaport add niche technology exposure at smaller allocations, broadening the fund’s reach across the domestic tech ecosystem.

The selloff did not arrive without a causal chain. Long-duration growth assets, which is precisely what ATEC’s constituents are, derive their valuations from earnings projected years into the future. When discount rates rise, the present value of those future cash flows compresses mechanically, even when the underlying businesses continue growing. This is the duration risk mechanism, and it has operated with textbook-free precision across ATEC’s holdings.

Three specific headwinds converged. Elevated RBA cash rates increased the discount rate applied to growth equities. Reduced investor risk appetite pulled capital away from high-multiple names toward defensive yield. And valuation-related concerns, which accumulated during the post-pandemic re-rating of ASX tech, left little margin for error when sentiment shifted.

Three consecutive RBA hikes to a cash rate of 4.35% compressed Australian growth equity valuations across all three meetings, with the tightening cycle starting from 3.85% in January 2026 and the Board explicitly preserving optionality for a fourth move in July, leaving long-duration names without the rate relief they need for re-rating.

ATEC fell approximately 36% from its 52-week high over the same period the Nasdaq-100 climbed roughly 60-63% from its late-2024 levels to approximately 29,367 as at 13 May 2026.

That divergence is not random. The Nasdaq-100 is dominated by profitable mega-cap technology companies with pricing power and global scale. ATEC is skewed toward mid-cap growth names with longer duration characteristics and narrower revenue bases. The AUD/USD exchange rate (approximately 0.7219 as at 14 May 2026, with a 2026 year-to-date average of approximately 0.6998) adds further translation complexity for holdings with offshore earnings.

If the selloff was macro-driven rather than fundamental, the logical next question is whether those macro conditions are changing.

A “long-duration asset” is a business whose most significant earnings are projected years into the future. Higher interest rates discount those distant earnings more heavily, reducing the price investors are willing to pay today. Lower rates do the reverse. This is why ATEC’s constituents move with outsized sensitivity to monetary policy expectations.

Not all of the fund’s holdings sit at the same point on this spectrum. The distinction matters.

Xero and TechnologyOne are profitable SaaS compounders. Xero reported approximately $2.1 billion in revenue for FY25 with roughly 23% revenue growth, demonstrating positive free cash flow and expanding margins. TechnologyOne’s SaaS transition is largely complete, generating high recurring revenue with consistent dividend growth. Its share price declined approximately 22% to around $20 during the April 2026 selloff, despite fundamental resilience in its public-sector and education verticals.

NextDC sits in a different category. It is a capital-intensive infrastructure business requiring large upfront investment against multi-year contracted returns, with an FY26 capital plan of approximately $2.2-$2.4 billion and equity and debt capital raises executed in April 2026 to fund expansion.

| Company | Business Model | Revenue Type | Rate Sensitivity |

|---|---|---|---|

| Xero | Profitable SaaS compounder | Recurring subscriptions, offshore revenue (UK, NZ) | High-multiple; benefits from rate cuts |

| TechnologyOne | Defensive SaaS compounder | Recurring subscriptions, public-sector anchor | Moderate; earnings visibility limits downside |

| NextDC | Capital-intensive data centre infrastructure | Contracted capacity, multi-year ramp | Very high; capex cycle and leverage amplify rate impact |

The market has shifted to rewarding “profitable growth” over pure revenue growth. Xero and TechnologyOne fit this new paradigm. Earlier-stage or loss-making ASX tech names have faced more sustained pressure, and that dispersion within the fund is worth understanding before treating ATEC as an undifferentiated block.

The relationship between earnings quality and recovery speed across the ASX tech sector is not uniform: Megaport, which reached profitability before the trough, surged 79% in recovery, while WiseTech posted zero recovery despite continued earnings growth, illustrating why the profitable-growth distinction within ATEC’s holdings matters more than the headline index return.

Three structural tailwinds that underpinned the original investment thesis remain intact through the drawdown:

The inflow data reinforces this reading. Approximately $193.7 million flowed into ATEC during 2026 year-to-date, even as the unit price fell.

Australian data centre capacity forecasts compiled by industry researchers point to sustained demand growth driven by AI workload expansion and cloud adoption, providing the contracted pipeline backdrop against which NextDC’s multi-billion dollar capital expenditure program is being evaluated by the market.

Approximately $193.7 million in year-to-date inflows during a 36% drawdown suggests that informed capital has been adding exposure during weakness, not exiting.

AUD dynamics provide a partial earnings buffer. The 2026 year-to-date average of approximately 0.6998 against the US dollar benefits Xero’s reported AUD earnings, given its substantial UK and international revenue base. TechnologyOne’s UK expansion offers an incremental long-term revenue driver beyond its domestic public-sector anchor.

The persistence of structural demand drivers alongside positive inflow behaviour suggests the drawdown reflects a repricing of risk rather than deterioration of the businesses themselves.

ATEC’s defining differentiator is its mandate: pure domestic ASX-listed technology exposure. Investors seeking Australian tech without global mega-cap dilution have limited alternatives. Those willing to accept global exposure face meaningfully different options.

| ETF | Focus | MER | 1-Year Return | 3-Year p.a. Return |

|---|---|---|---|---|

| ATEC | Australian technology (ASX-listed) | 0.48% | Live data required | Live data required |

| HACK | Global cybersecurity | 0.67% | -9.73% | 16.05% |

| RBTZ | Global robotics and AI | 0.57% | +19.60% | 12.56% |

| NDQ | Nasdaq-100 (global large-cap tech) | 0.48% | Live data required | Live data required |

HACK and RBTZ returns are to 30 April 2026. ATEC and NDQ returns require live data retrieval for current accuracy.

RBTZ’s +19.60% one-year return reflects its exposure to the global AI and robotics tailwind, a thematic that has rewarded international names more than domestic ones. NDQ offers the same 0.48% MER as ATEC but with Nasdaq-100 exposure, and the Nasdaq-100’s approximately 60% gain from late 2024 makes the domestic-versus-global question a live one.

Choosing ATEC is a deliberate bet on the Australian tech sector’s recovery. It is not simply a “buy tech” decision that could be satisfied by multiple alternatives with different geographic mandates and meaningfully different recent performance.

Investors comparing ASX thematic ETF alternatives should note that HACK’s 14.85% per annum return since inception and RBTZ’s one-year return of 19.60% both reflect geographic mandates and thematic concentrations that are fundamentally incompatible with ATEC’s domestic focus, making the choice between them a question of sector conviction rather than simple performance chasing.

The bull case is specific. ATEC at 36% below its high represents a lower entry point into structurally growing businesses, but the recovery requires three conditions to hold:

The bear case is equally specific:

Australian financial media commentary has characterised the sector as “full on valuation but constructive long-term,” and BetaShares’ own materials disclose that ATEC “should be considered as a component of a broader, diversified investment portfolio.”

The broader ASX growth ETF landscape reveals how wide return dispersion can be across funds sharing the same label, with one-year returns ranging from -22.6% to +101.2% as at March 2026; understanding where ATEC sits within that range, and what fee and allocation differences explain the spread, helps investors calibrate whether the current drawdown represents a genuine relative opportunity or simply the expected range of a high-beta thematic.

The appropriate investor profile is clear: a long-term horizon of five or more years, tolerance for ongoing volatility, and an existing diversified portfolio where ATEC functions as a growth satellite rather than a core holding.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

ATEC’s 36% decline from its high has improved the entry price. It has not eliminated the valuation risk on anchor holdings or resolved the macro uncertainty around the pace of RBA easing.

The ETF structure itself is appropriate for this kind of recovery positioning. Diversification across multiple ASX tech names removes single-stock execution risk while maintaining full exposure to the sector’s structural upside. The $193.7 million in 2026 inflows suggests that the broader investor community has collectively moved in this direction already, adding exposure during weakness rather than retreating.

For long-term investors with existing diversified portfolios, the current drawdown may represent a more rational entry point than the 52-week peak. The investment requires genuine patience, tolerance for further downside, and acceptance that the macro tailwinds may take time to materialise. The question has shifted from “is Australian tech expensive?” to “does the long-term structural case justify the current price for a patient investor?” That is a better question to be asking, even if the answer is not yet certain.

The BetaShares Australian Technology ETF (ASX: ATEC) is a concentrated domestic technology ETF with a 0.48% management expense ratio that tracks ASX-listed tech companies including Xero, NextDC, TechnologyOne, SiteMinder, Megaport, and Codan. It has no exposure to US mega-cap technology stocks like Nvidia or Microsoft.

ATEC declined approximately 36% from its 52-week high primarily due to elevated RBA cash rates reaching 4.35%, which mechanically compressed the present value of future earnings for long-duration growth assets. Reduced investor risk appetite and stretched post-pandemic valuations on ASX tech names added further downside pressure.

Both ATEC and NDQ share the same 0.48% management expense ratio, but they offer fundamentally different exposures: ATEC holds only ASX-listed domestic technology companies, while NDQ tracks the global Nasdaq-100 index dominated by profitable US mega-cap tech firms. The Nasdaq-100 gained roughly 60% from late 2024 while ATEC fell 36% over the same period, illustrating how different their return profiles have been.

A recovery in ATEC requires three conditions: an RBA easing cycle materialising to reduce the discount rate on long-duration earnings, AI and cloud demand sustaining NextDC's multi-billion dollar capital expenditure returns, and Xero and TechnologyOne maintaining earnings quality and margin expansion. None of these outcomes is guaranteed, and the timeline for RBA rate cuts remains uncertain.

ATEC is suited for long-term investors with a horizon of five or more years, a high tolerance for ongoing volatility, and an existing diversified portfolio where ATEC functions as a growth satellite rather than a core holding. BetaShares itself discloses that the fund should be considered a component of a broader diversified portfolio rather than a standalone position.