When EOS (ASX: EOS) announced it was lifting the ceiling on its MARSS earnout from €100 million to €140 million, most headlines focused on the contract win that triggered the change. The more instructive story sits in the amendment itself, and what it reveals about how acquisition deals actually work once signed. On 15 May 2026, EOS disclosed revised terms for its MARSS acquisition via an ASX announcement titled “MARSS Business and Transaction Update.” The upfront consideration of US$36 million remained unchanged. What changed was the maximum contingent payment the seller could receive over the earnout period, lifted by €40 million to reflect a stronger-than-expected contract pipeline, including a single order worth approximately €102 million from a Middle Eastern national defence force. This article uses the EOS-MARSS transaction as a practical case study to explain what earnout structures are, why they get renegotiated, and what the revised terms tell retail investors about how deal economics function in practice.

What an earnout structure actually is (and why buyers and sellers both want one)

Buyers and sellers often disagree on what a business is worth. This is especially true in sectors like defence and technology services, where revenue arrives in lumpy, large contracts rather than steady monthly streams. Near-term financials may not reflect the underlying value of the pipeline a business has built.

The earnout solves this problem by deferring part of the purchase price. The buyer pays a base amount upfront, then pays more later if the acquired business hits agreed performance targets over a defined period. Both sides share the risk: the buyer avoids overpaying for unproven performance, and the seller captures upside if the business delivers.

Earnouts are particularly common where sales cycles run long and contract pipelines are difficult to value at the time of signing. Defence, technology services, and project-based businesses all fit this profile. Typical measurement periods run 2-3 years, with longer windows used in industries where contract cycles extend beyond that horizon.

The key components of a typical earnout

Four structural elements define how an earnout works in practice. The choice of metric matters most: order intake-based earnouts (like the MARSS structure) behave differently to revenue or EBITDA-based structures, because they measure business won rather than business delivered.

| Element | Typical form | Common use case |

|---|---|---|

| Metric | Revenue, EBITDA, or qualified order intake | Defence businesses often use order intake or contracted backlog |

| Measurement period | 2-3 years (longer in project-based sectors) | Extended windows allow contract cycles to complete |

| Cap | Explicit maximum total payment | Gives the buyer cost certainty on total consideration |

| Payment form | Cash, shares, or a combination | Share-settled earnouts preserve cash but carry dilution risk |

When big ASX news breaks, our subscribers know first

The original EOS-MARSS deal and what the upfront terms established

EOS first announced the MARSS acquisition on 12 January 2026, setting out a deal with two distinct components: a fixed upfront payment and a contingent earnout.

The original terms established a clean baseline:

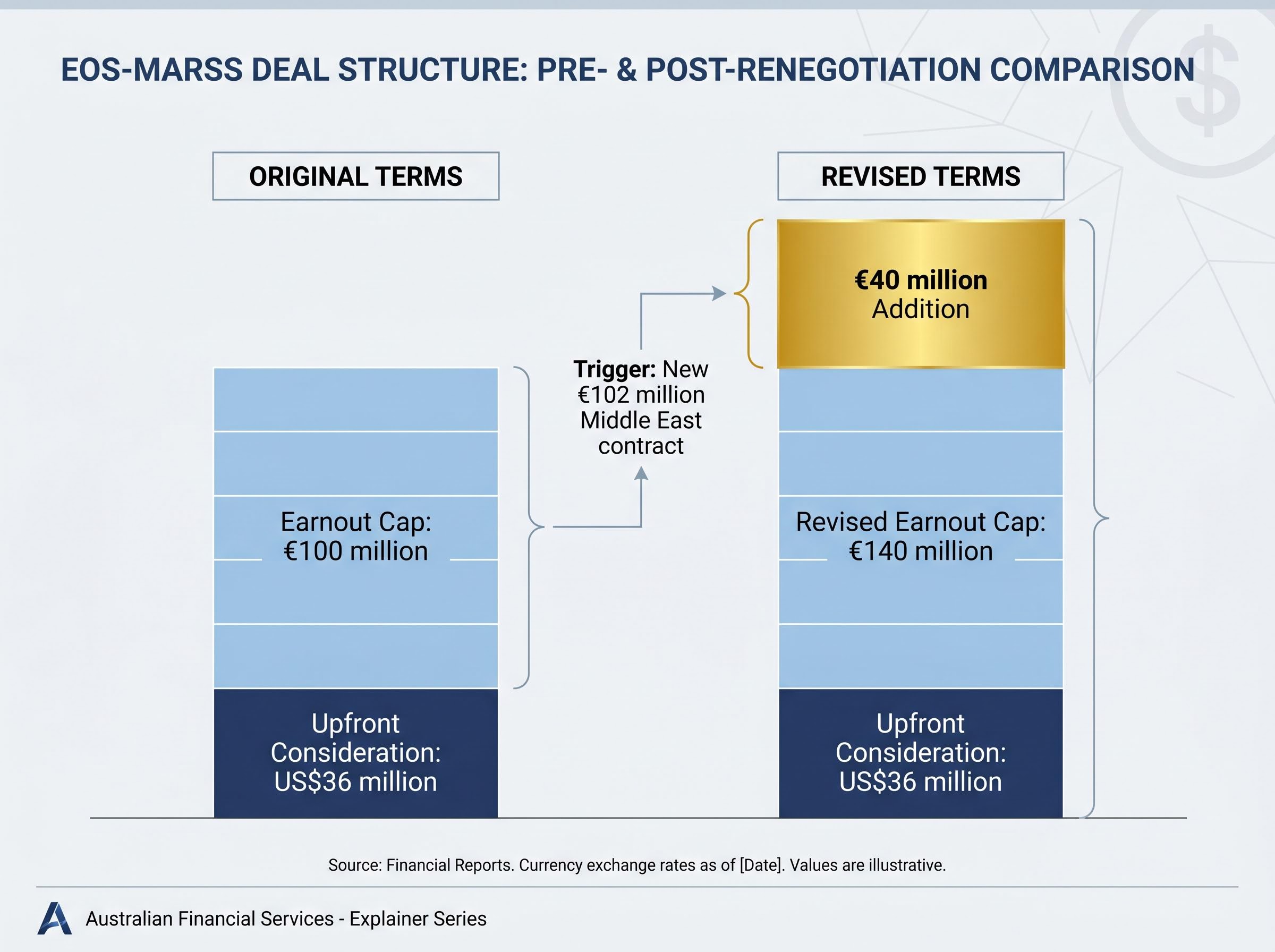

- Upfront consideration: US$36 million (cash)

- Earnout cap: €100 million, calculated as a percentage of Qualifying MARSS Orders over a defined measurement period

- Settlement form: a combination of cash and shares

- Measurement basis: Qualifying MARSS Orders (order intake, not revenue)

The share-settled component of the earnout introduced a specific risk for existing EOS shareholders. If shares were issued in settlement at a time when the share price was depressed, the dilution impact would be amplified.

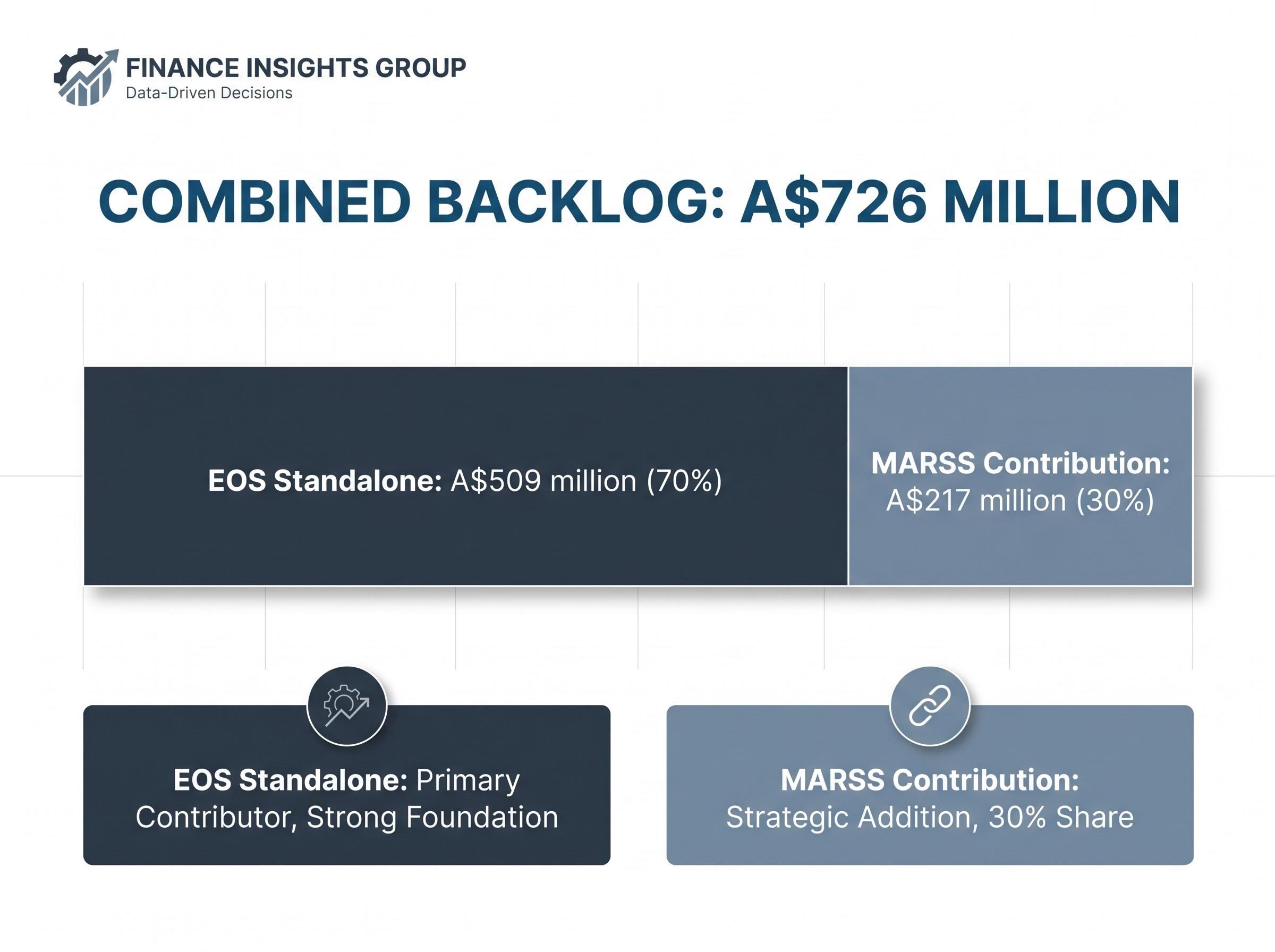

Combined order book at announcement: EOS’s standalone order book sat at A$509 million; MARSS contributed A$217 million, giving a combined backlog of approximately A$726 million subject to completion.

That combined figure framed the strategic scale of the transaction. MARSS was not a bolt-on acquisition; its backlog represented roughly 30% of the combined total.

Why EOS raised the earnout ceiling (and what triggered the renegotiation)

Between January and May 2026, something shifted the economics of the deal. MARSS secured a new order from a Middle Eastern national defence force worth approximately €102 million (around A$165 million), designed to expand MARSS installations for nationwide drone detection and neutralisation using its NiDAR C2 platform.

A single contract of that size, arriving early in the earnout measurement period, changed the probability distribution of future earnout payments. The original €100 million cap suddenly looked constraining. If MARSS continued winning at this rate, the earnout ceiling would cap out before the measurement period ended, removing the performance incentive for MARSS management and key technical staff at precisely the moment the pipeline was accelerating.

EOS noted that MARSS had several additional prospective contracts, each exceeding A$100 million in value. The NiDAR C2 platform has an established operational track record in the Middle East, including documented neutralisation of Shahed drone and missile attacks.

The renegotiation followed a logical three-step sequence:

- MARSS won a €102 million contract that materially raised its strategic value during the earnout period

- The original €100 million cap became structurally constraining to seller incentives

- EOS lifted the cap to €140 million to re-align the economics and retain management engagement

Incentive alignment, not deal repair

EOS characterised the amendment as having no change to the expected broadly neutral impact on 2026 earnings and operating cash flow. This framing is important.

Lifting the cap only costs EOS more if MARSS materially outperforms the original expectations. In the base case, the amendment is value-neutral. The rationale was explicitly about aligning incentives and securing long-term strategic co-operation, not correcting a mispriced transaction. This pattern is consistent with documented Australian M&A practice, where earnout caps are increasingly re-opened by mutual agreement when performance data shifts materially.

How earnout renegotiations typically work in Australian M&A

Retail investors often read an earnout amendment as a warning sign, something changed, so something must be wrong. Australian M&A practice tells a different story.

Legal commentary from Clayton Utz and broader industry guidance confirms that earnouts are increasingly re-opened after completion as business conditions change. Targets may prove too aggressive or too conservative once real performance data emerges. Common renegotiation drivers include regulatory delays, integration timing shifts, and (as in the MARSS case) unexpectedly strong contract pipelines that make original targets look conservative.

Well-drafted earnout agreements typically include protections for both sides:

The Magellan-Barrenjoey transaction illustrates how ASX merger deal structure shapes post-completion dynamics: a 5.5-year weighted average escrow period on vendor consideration aligns seller incentives over a multi-year horizon, serving a function structurally similar to an earnout cap in keeping key parties engaged through integration.

| Buyer protections | Seller protections |

|---|---|

| Non-compete clauses preventing sellers from starting competing activities | Anti-sandbagging clauses preventing the buyer from suppressing performance |

| Operational covenants restricting actions that artificially inflate earnout metrics | Audit rights over the buyer’s calculation of earnout metrics |

| Clawback provisions if manipulation or misrepresentation is later revealed | Operational independence covenants protecting the business from harmful integration changes |

Disputes arising from earnout calculations in Australian M&A are typically resolved via expert determination, a faster and lower-cost process than litigation, under Australian contract law. Arbitration and Federal Court proceedings remain available but are less common for purely financial calculation disputes.

CGT treatment for sellers: Under Australian tax law, earnout payments are treated as capital proceeds for CGT purposes. Where the earnout amount is uncertain at the time of the transaction, look-through earnout treatment may apply, with each payment treated as a separate CGT event when received. Sellers may need to amend prior-year tax returns upon receipt of earnout payments.

The ATO look-through earnout rules treat each contingent payment as a separate CGT event upon receipt, meaning sellers who receive earnout instalments across multiple income years may need to amend prior-year tax returns as each tranche crystallises.

How EOS is funding the deal and what the debt structure means for investors

The upfront acquisition cost is real and already financed. EOS drew A$70 million from a secured term loan facility, with A$50 million of that drawdown earmarked specifically to fund the upfront cash component of the MARSS acquisition.

The lender is Washington H. Soul Pattinson (WHSP), a single domestic lender rather than an international bank syndicate. That distinction carries implications. A relationship-dependent facility with one lender has different refinancing dynamics compared to a diversified syndicate; EOS’s ability to renegotiate terms or extend the facility depends on a single counterparty relationship.

The facility is described as commercially competitive and floating-rate, with remaining headroom beyond the A$70 million drawn. The tenor is medium-term, aligned with the expected integration and earnout periods for MARSS. If the facility is floating-rate, higher interest rates could pressure future earnings regardless of MARSS’s commercial performance.

Floating-rate debt facilities carry refinancing and interest rate sensitivity that fixed-rate instruments do not, and the current leveraged finance environment, shaped by a large near-term corporate refinancing cycle, means the cost of rolling single-lender facilities could move materially against borrowers if conditions tighten before an earnout period concludes.

What investors should watch in future EOS reporting

The MARSS earnout and debt structure will flow through EOS’s periodic reports in several specific ways. Key line items and disclosures to monitor include:

- Contingent consideration liability movements in EOS’s balance sheet, reflecting re-measurement of expected earnout payments

- Share issuances in settlement of earnout tranches, with dilution impact dependent on the prevailing share price

- Leverage ratio disclosures and any covenant waiver announcements in half-year and full-year reports

- WHSP relationship developments, including any refinancing, facility amendments, or governance considerations tied to the sole-lender structure

- CUAS pipeline progress, particularly further Middle Eastern and global order wins that validate the strategic thesis

What the EOS-MARSS amendment tells investors about reading deal announcements

The EOS-MARSS case offers a reusable framework for any retail investor encountering an acquisition earnout disclosure on the ASX. Three questions cut through the complexity:

- What is the upfront cost versus the contingent ceiling? The upfront amount is the committed capital at risk. The contingent ceiling is the maximum additional payment, triggered only by performance. In EOS’s case, US$36 million was committed; up to €140 million is contingent.

- What metric drives the earnout and how verifiable is it? Order intake-based earnouts, like MARSS’s Qualifying MARSS Orders metric, are tied to contract wins rather than revenue recognition. The verifiability of this metric depends on how clearly “qualifying” is defined in the agreement.

- What does any amendment to terms tell you about the relative negotiating position of buyer and seller? The MARSS vendors had leverage. The €102 million Middle Eastern contract materially raised MARSS’s strategic value during the process, prompting EOS to sweeten the contingent terms to retain management alignment.

Analyst characterisation: The amendment has been broadly characterised as value-neutral in the base case and potentially value-accretive under upside scenarios, with execution risk (integrating a European C2 software business into an Australian hardware-oriented group) as the key watchpoint.

The EOS share price rose by over 4% following the 15 May 2026 announcement, and no major broker rating downgrades were linked to the amended earnout terms at the time of publication. Fund manager commentary flagged share-settled earnout dilution risk if the share price is depressed, execution risk integrating NiDAR into EOS’s hardware stack, and the question of why EOS needed to renegotiate early in the earnout period, suggesting MARSS vendors held meaningful negotiating leverage.

The EOS-MARSS deal as a live lesson in acquisition mechanics

The earnout ceiling increase is not evidence of a deal gone wrong. It is evidence of a deal structure doing what earnouts are designed to do: adjusting contingent consideration when performance shifts the probability distribution of future outcomes. MARSS won a large contract earlier and bigger than the original deal anticipated, and EOS recalibrated the incentive structure to keep management aligned.

For retail investors, the framework applies beyond defence. Any growth sector with long sales cycles, whether technology services, resources, or industrials, produces acquisition structures where earnouts bridge the valuation gap between buyer and seller. The questions remain the same: what is fixed, what is contingent, what metric drives it, and what does any amendment signal about who holds the leverage.

EOS’s periodic reporting and ASX announcements remain the primary source for tracking earnout accruals, share issuances, and debt covenant headroom as the MARSS integration progresses.

For retail investors building the habit of reading ASX announcements as a primary research source, our dedicated guide to investing in Australia covers the practical foundations: how to interpret company disclosures, what periodic reports contain, and how to develop the analytical habits that compound over time.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.