The Reserve Bank of Australia has raised the cash rate to 4.35% for the third consecutive meeting, with eight of nine board members backing the 25 basis point increase as underlying inflation continues to run above the 2-3% target band. The decision, taken on 5 May 2026, arrives against a backdrop of domestic capacity pressures, fuel-driven cost shocks from the Middle East conflict, and rising short-term inflation expectations. The cumulative tightening now carries real consequences for variable-rate mortgage holders, savers, and equity investors alike.

What follows covers what the Board decided and why, what the inflation picture looks like heading into mid-2026, what the near-unanimous vote signals about future policy, and what the practical consequences are for Australian borrowers and investors right now.

RBA lifts cash rate to 4.35% in its third straight tightening move

The Monetary Policy Board raised the cash rate target by 25 basis points to 4.35% at its 5 May 2026 meeting, according to RBA Media Release No. 2026-12. The vote was decisive but not absolute.

RBA Media Release No. 2026-12 confirms the Board’s decision to raise the cash rate target by 25 basis points to 4.35%, including the vote breakdown of eight members in favour and one preferring to hold, along with the full text of the Board’s forward guidance language.

- Rate level: Cash rate target now 4.35%, up from 4.10%

- Vote breakdown: Eight members voted in favour of the hike; one preferred to hold at 4.10%

- Consecutive hikes: This marks the third straight tightening move

The single dissent matters. It signals that the threshold between hiking and holding is narrower than the headline margin suggests, and that the next decision is genuinely live.

The Board stated that monetary policy is now “well-positioned to respond to further developments,” language that conveys deliberate optionality rather than a commitment to pause or continue.

That phrasing is carefully chosen. It permits a fourth hike if inflation surprises higher. It equally permits a pause if the data cooperates. For borrowers and investors, the ambiguity is the message.

When big ASX news breaks, our subscribers know first

Why inflation forced the Board’s hand: domestic pressure meets global shock

Inflation did not arrive in a single wave. It built in two layers, and the Board’s reasoning reflects both.

The first layer is domestic. Inflation accelerated materially in the second half of 2025, and early 2026 data confirmed this reflected genuine capacity pressures, not transient supply effects. The Australian economy has been operating tighter than full employment, and that pressure has been pushing prices higher across services and domestically produced goods.

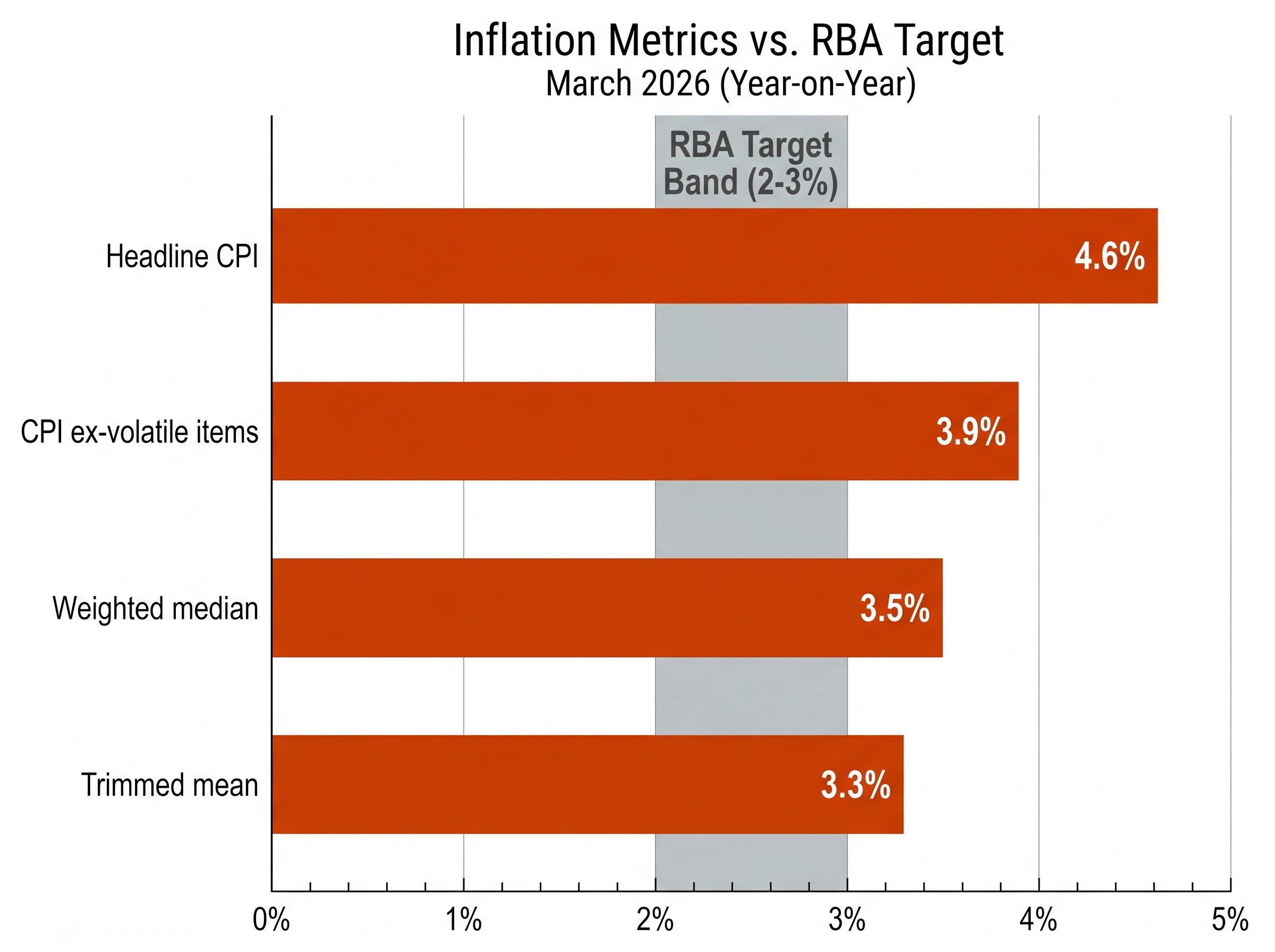

The numbers remain uncomfortable. All four headline and underlying measures sit above the RBA’s 2-3% target band, as the March 2026 Australian Bureau of Statistics (ABS) data confirmed.

| Measure | March 2026 reading | Prior period | RBA target |

|---|---|---|---|

| Headline CPI | 4.6% year-on-year | N/A | 2-3% |

| Trimmed mean | 3.3% year-on-year | 3.3% | 2-3% |

| Weighted median | 3.5% year-on-year | N/A | 2-3% |

| CPI ex-volatile items | 3.9% year-on-year | N/A | 2-3% |

The trimmed mean, the RBA’s preferred underlying gauge, has held steady at 3.3%, well above the top of the target range. That persistence is what matters most: inflation is not accelerating dramatically, but it is refusing to fall.

The divergence between headline and underlying inflation measures became central to the Board’s deliberations because it determined whether the rate decision was responding to a temporary energy shock or something more structurally embedded in the economy; with trimmed mean holding at 3.3% while headline ran at 4.6%, the Board was effectively deciding how much weight to place on a fuel-driven spike versus persistent domestic price pressure.

Fuel prices and second-round effects: what the Middle East conflict adds

The second layer is external. Elevated fuel prices linked to the Middle East conflict have added direct cost pressure and, more importantly, early evidence of second-round effects spreading into goods and services pricing. Many businesses were assessed as considering passing rising input costs through to consumers, creating upside risk to inflation independent of the oil price itself.

The RBA’s baseline forecast already assumed an eventual conflict resolution and a subsequent fuel price decline, yet underlying inflation was still projected to peak higher than the February 2026 forecast. An extended or intensified conflict remains a scenario that could entrench longer-term inflation expectations and suppress demand among Australia’s major trading partners, creating a separate drag on activity.

Short-term inflation expectations indicators had moved higher in the lead-up to the decision, reinforcing the Board’s concern that price pressures risked becoming self-sustaining.

What three consecutive hikes have done to financial conditions in Australia

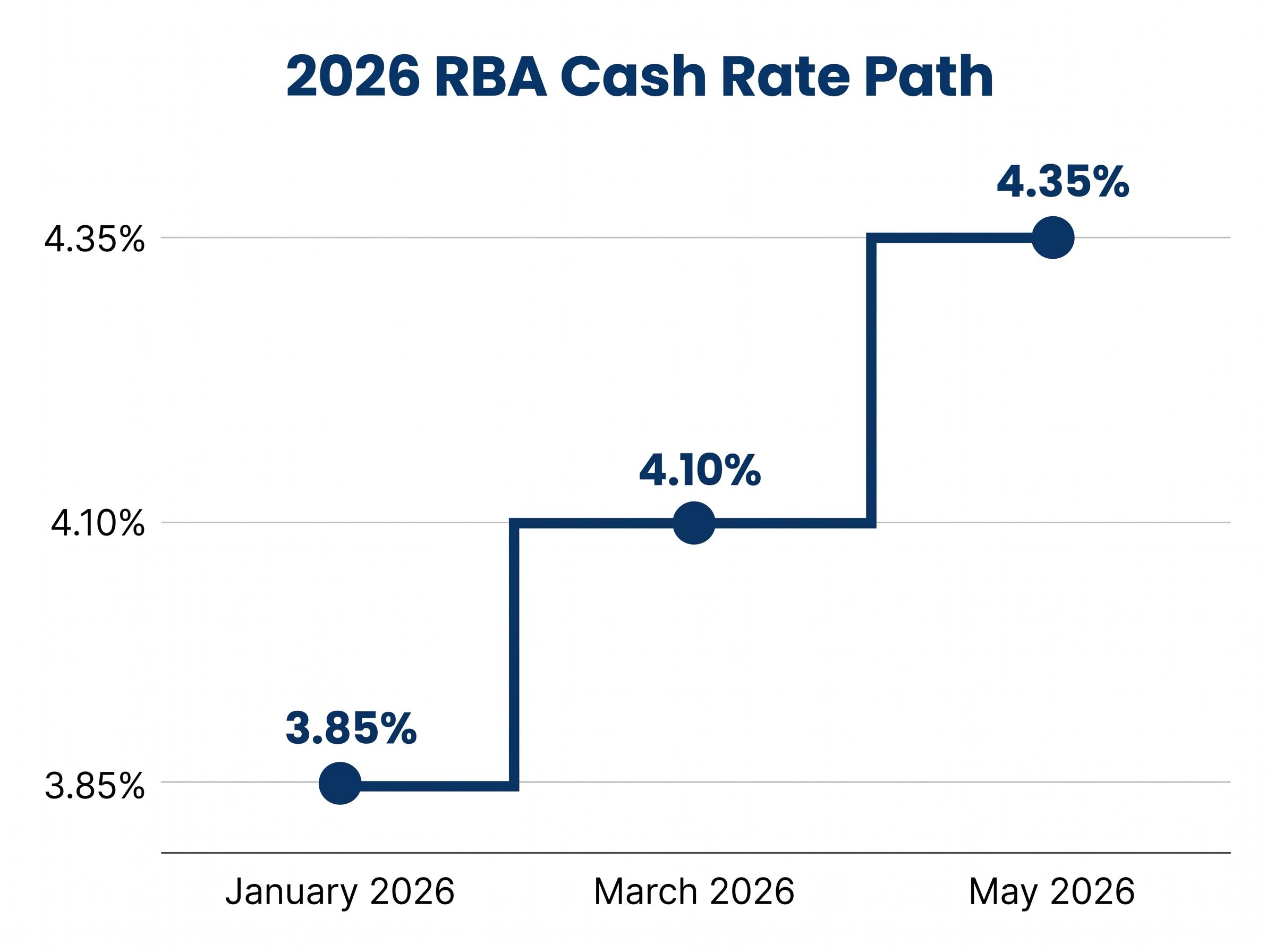

The cumulative path is now visible. Three consecutive moves have taken the cash rate from 3.85% to 4.35% across the first half of 2026.

- January 2026 meeting: Cash rate raised to 3.85%

- March 2026 meeting: Cash rate raised to 4.10%

- May 2026 meeting: Cash rate raised to 4.35%

Broader financial conditions have tightened across the board. Money market rates and government bond yields have risen, and the Australian dollar has appreciated. These are the standard transmission channels of monetary tightening, and all are now operational.

The RBA monetary policy transmission channels framework identifies rising market interest rates, currency appreciation, and tightening credit conditions as the primary mechanisms through which cash rate increases feed into household borrowing costs and, ultimately, into inflation outcomes.

The qualifier matters, though. Despite tighter conditions, the RBA assessed credit as remaining readily available for households and businesses. That distinction separates a repricing event from a financial stress event. Lending has not seized; it has become more expensive.

For variable-rate mortgage holders, the pattern of bank pass-through is now well-established. All four major banks passed the March 2026 hike to variable-rate customers within hours of the announcement. The same speed of transmission is expected following this decision.

What the decision means for mortgage holders and savers right now

Variable-rate borrowers should expect Commonwealth Bank of Australia (CBA), Westpac, NAB, and ANZ to announce increases to advertised home loan rates within hours, consistent with the March 2026 precedent. The 25 basis point increase will flow directly through to monthly repayments.

The impact is not uniform. Three distinct borrower types face different positions:

- Variable-rate existing borrowers: Immediate repayment increase once their lender adjusts rates, with the size depending on outstanding loan balance

- Fixed-rate borrowers approaching expiry: Insulated until their fixed term expires, but now facing a materially higher variable rate upon rollover

- Prospective buyers: Borrowing capacity calculations will tighten further, potentially affecting pre-approval amounts and affordability assessments

Savers benefit from the same repricing that burdens borrowers. High-interest savings accounts and term deposits should see upward rate adjustments, providing a counterbalancing positive in the tightening cycle.

For borrowers considering refinancing or locking in a fixed rate, RateCity and individual bank websites will publish updated advertised rates as banks respond throughout the day.

Forward guidance decoded: what the Board is and is not committing to

The phrase “well-positioned to respond to further developments” is not a pause signal. Nor is it a promise of more hikes. It is an explicit statement of optionality, designed to keep every future meeting live.

The Board outlined a range of plausible scenarios. In the baseline case, underlying inflation is expected to decline following its peak as demand moderates and capacity pressures ease. In the alternative case, an extended Middle East conflict drives further inflation while simultaneously suppressing trading partner growth. These two paths produce very different policy responses, and the Board is not choosing between them yet.

Three specific data streams will determine which path prevails:

The federal budget conflict with RBA tightening represents an underappreciated complication in the forward guidance picture: the 12 May 2026 budget includes personal income tax cuts, energy rebates, and potential fuel excise reductions that could simultaneously add fiscal stimulus and reduce headline CPI mechanically, creating a policy environment where the Board’s inflation-fighting signals and the government’s cost-of-living relief measures pull households in opposite directions.

- Global economic and financial market developments, including any shift in Middle East conflict dynamics

- Domestic demand trends, particularly consumer spending and business investment

- The outlook for inflation and the labour market, with the trimmed mean and employment data as the key metrics

The Board committed to “remain responsive to incoming data and the evolving risk assessment.” Pre-decision market pricing via the ASX RBA Rate Tracker implied a 76% hike probability as of 30 April 2026, suggesting markets had largely positioned for this outcome. The forward path is where uncertainty lives.

Three things to watch before the July 2026 RBA meeting

The next meeting provides the Board’s next formal opportunity to act. The data window between now and then will determine whether a fourth consecutive hike is warranted.

Three inputs will matter most: Q2 CPI data, which will show whether the trimmed mean has finally begun to retreat; monthly labour market reports, which will signal whether capacity pressures are easing; and any shift in Middle East conflict dynamics that changes the fuel price outlook.

The dissenting board member’s preference to hold is a reminder that the margin between hiking and pausing may be narrower than the 8-1 vote suggests. If even one or two of these data points soften, the Board’s calculus could shift.

Australian equity and currency markets face a recalibration moment

The ASX had already shown its hand before the announcement. The index closed at 8,697.10 on 4 May 2026, down 0.37%, marking the ninth decline in ten sessions.

Nine declines in ten sessions ahead of the decision captured the market’s pre-announcement caution.

With hike probability priced between 76-85% across major trackers (including the ASX RBA Rate Tracker, Octagon AI, and major bank forecasts), the rate decision itself was largely anticipated. The Finder RBA Survey found 75% of economists predicted a rise, a sharp improvement from the 38% who correctly called the March hike.

That pricing means the market reaction will focus more on the forward guidance language than the rate level itself. Rate-sensitive sectors face the most direct pressure:

- Headwinds: Real estate investment trusts (REITs), utilities, and consumer discretionary, where higher borrowing costs compress valuations and weigh on spending

- Relative resilience: Financials (where net interest margins may benefit from higher rates) and exporters (where a stronger Australian dollar creates a mixed but distinct set of dynamics)

For investors, the gap between what the market expects next and what the Board actually delivers in July is where portfolio risk concentrates. A largely priced-in decision today shifts the analytical weight to tomorrow’s data.

Three hikes in, with the path still uncertain

Three consecutive increases have taken the RBA cash rate to 4.35%. Inflation remains above target on all measures. The Board has preserved maximum flexibility on what comes next.

The single dissent is a reminder that the tightening cycle is not on autopilot. Incoming data between now and the July 2026 meeting will be scrutinised closely by both the Board and markets. The full statement text is available at rba.gov.au, and updated advertised mortgage rates will appear on RateCity and individual bank websites as CBA, Westpac, NAB, and ANZ respond throughout the day.

Peak rate forecasts from Australia’s major banks diverge significantly beyond the May move, with Westpac projecting a path to 4.85% through June and August 2026 while NAB places its terminal rate at 4.60%, a gap that represents thousands of dollars in annual repayment difference for households holding a median mortgage through the plateau period.

Borrowers approaching a fixed-rate rollover or considering refinancing may benefit from consulting a mortgage broker or financial adviser to assess their options in the current environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.