Why AI Is Splitting Semiconductor Stocks From the Rest of Tech

5 hrs ago

Two index providers quietly changed their rules in May 2026. Six weeks later, SpaceX priced the largest IPO in history. The collision of those two events is about to place one of the most structurally unusual stocks ever listed inside millions of 401(k) accounts, whether the account holders want it or not. SpaceX priced at $135 per share on 12 June 2026, closed its first trading day near $160.95, and instantly ranked as the sixth-largest publicly traded company in the United States. What makes the index inclusion story distinctive is not the size of the IPO itself but the combination of a multi-trillion-dollar market capitalisation sitting on top of a tradeable float of roughly 5% of total shares, meeting index rules that have never moved this fast before. What follows is an examination of the specific mechanics behind the Nasdaq and Russell fast-entry rule changes, what they mean for the scale of forced buying, and what passive investors holding QQQ, Russell ETFs, or target-date funds should understand about the SpaceX position heading toward them.

The IPO is not the trigger for the SpaceX index inclusion story. The regulatory architecture that preceded it is. Two of the three largest index families revised their entry rules in spring 2026, and both changes took effect before SpaceX listed a single share.

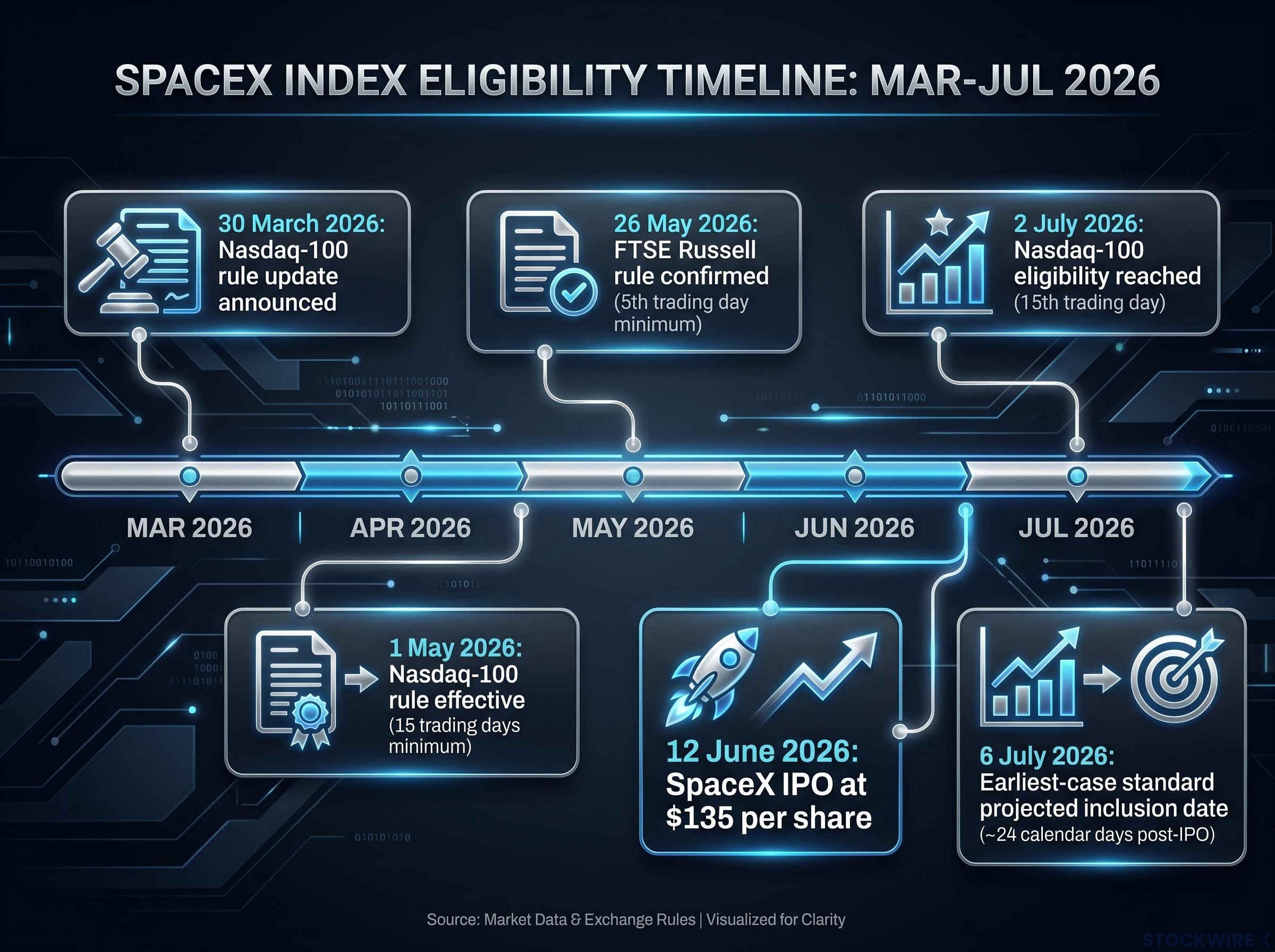

Nasdaq announced a methodology update on 30 March 2026, effective 1 May 2026, that created a fast-entry pathway for very large IPOs. Under the prior framework, newly listed companies faced a minimum waiting period of three months before becoming eligible for Nasdaq-100 consideration. The revised methodology collapsed that period to as few as 15 trading days for companies ranking among the top 40 by market capitalisation.

The Nasdaq-100 fast-entry methodology published on 1 May 2026 confirms that qualifying candidates ranked in the top 40 by market capitalisation may be added to the index after 15 trading days, collapsing what had previously been a three-month minimum waiting period.

The original analysis of the rule change characterised the minimum free-float requirement as fully eliminated for fast-entry candidates. Nasdaq’s own public methodology documents are less explicit on this point, emphasising float-adjusted market capitalisation and liquidity screens rather than an outright exemption. The practical effect, however, is not in dispute: SpaceX can enter at full weighting despite a very small float.

FTSE Russell confirmed its own fast-entry rule on 26 May 2026, allowing qualifying companies to be added to its Russell 1000 and Russell 3000 indexes as soon as the fifth trading day after listing. FTSE Russell retains a float-adjusted index framework; the new rule modifies timing thresholds rather than discarding float considerations entirely.

Both index providers framed these changes as efforts to keep indexes representative of the investable market when large, long-private companies go public. Commentators and index practitioners have noted SpaceX as a likely beneficiary of the timing.

| Index Provider | Old Waiting Period | New Waiting Period | Effective Date |

|---|---|---|---|

| Nasdaq-100 | Three months minimum | 15 trading days (top-40 market cap) | 1 May 2026 |

| FTSE Russell (Russell 1000/3000) | Standard reconstitution cycle | Fifth trading day after listing | 26 May 2026 |

The rules changed before the IPO, not because of it. That sequence matters for understanding whether the forced buying that follows is accidental or structural, and for assessing whether similar dynamics could repeat in future large-cap listings.

Start with the size. At its first-day close of approximately $160.95, SpaceX’s total market capitalisation fell in the range of $1.77 trillion to $2.1 trillion, depending on whether the calculation uses the IPO price or the closing price as its basis. Either figure places SpaceX among the largest companies on Earth on day one.

Now the float. Of the approximately 12.9 billion shares outstanding, only 555-556 million were sold in the IPO. That produces a publicly tradeable float of roughly 4.9-5% of total shares, valued at approximately $89 billion at the first-day close.

Approximately 95% of SpaceX shares remain locked up at IPO, held by founders, employees, and venture capital firms, against a multi-trillion-dollar market capitalisation.

The mismatch is the story. The index weight assigned to SpaceX will be derived from its overall market cap size, but all the buying pressure generated by that weight must be absorbed by the small fraction of shares actually in circulation. Three conditions combine to create this pressure:

That structural gap between index-weight-driven demand and available supply is the single mechanism most likely to produce short-term price distortion.

The SpaceX IPO deal structure itself introduced several features that compound the index inclusion dynamics: a bypassed institutional roadshow removed the normal demand-signalling mechanism, a dual-class share arrangement concentrates voting control with insiders, and no S-1 financials were available to anchor early price discovery on fundamental grounds.

Understanding why the buying is “forced” requires tracing the chain of obligation from an index committee decision to a fund manager’s trade ticket. Index funds and exchange-traded funds (ETFs) tracking the Nasdaq-100 or Russell 1000/3000 are required by mandate to hold index constituents in proportion to their assigned weights. Once the index committee announces SpaceX’s inclusion, the buying is non-discretionary. Fund managers do not choose whether to participate; the mandate compels it.

The obligation extends beyond strict passive trackers. Active fund managers benchmarked against these indexes face tracking error penalties, a measure of how far a portfolio’s returns deviate from its benchmark, if they do not hold SpaceX after inclusion. This effectively compels participation from a broader universe of capital than passive vehicles alone.

The scale is substantial. QQQ manages approximately $493 billion in assets as of mid-June 2026, with total Nasdaq-100-tracking ETFs (including QQQM and others) reaching approximately $527 billion. Total Nasdaq-100 benchmarked capital, including institutional portfolios and derivative-linked products, sits in the trillion-plus range. Russell 1000 and Russell 3000 tracking funds collectively represent an even larger pool of assets.

According to Bloomberg Intelligence analysis, passive funds tracking the Russell 1000 and Nasdaq-100 would need to absorb approximately 24% of SpaceX’s public float. When active managers benchmarked to those indexes are included, total absorption is projected to exceed 50% of publicly available shares.

At an expected index weight of approximately 0.5% to 0.75%, mandatory purchasing from Nasdaq-100 trackers alone is estimated at roughly $2.5 billion to $4 billion. Combined estimates across Nasdaq-100 and Russell 1000 trackers range between $7 billion and $27 billion.

The dollar range is wide, but context sharpens it. Even the low end of the scenario represents a material demand shock into a float of roughly $89 billion. What is verified versus what is estimated:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The abstraction collapses when a 401(k) holder opens their brokerage account and sees SpaceX in their holdings without having placed an order. The following fund categories will carry automatic SpaceX exposure upon inclusion:

| Fund | Ticker | Index Tracked | Inclusion Trigger |

|---|---|---|---|

| Invesco QQQ Trust | QQQ | Nasdaq-100 | Nasdaq-100 addition |

| Invesco Nasdaq-100 ETF | QQQM | Nasdaq-100 | Nasdaq-100 addition |

| iShares Russell 1000 ETF | IWB | Russell 1000 | Russell 1000 addition |

| iShares Russell 3000 ETF | IWV | Russell 3000 | Russell 3000 addition |

| iShares Russell 1000 Growth ETF | IWF | Russell 1000 Growth | Russell 1000 addition |

SpaceX valuation at the IPO price rests on a specific set of long-duration assumptions: at a 250x EBITDA multiple, the market is pricing in decades of Starlink subscriber growth and launch services dominance, a trajectory that passive investors will now hold regardless of whether their own assessment of that growth path aligns with the implied price.

ICI retirement account fund ownership data shows that roughly half of all IRA and defined-contribution plan assets were invested in mutual funds at year-end 2023, with index-tracking strategies representing the dominant and growing share of that pool, which is why mandatory index additions carry direct consequences for tens of millions of retirement savers.

Under the updated Nasdaq rules, SpaceX became eligible for Nasdaq-100 consideration on approximately 2 July 2026, the 15th trading day after the 12 June IPO. Standard index committee procedure would set the effective inclusion date as the following Monday, 6 July 2026, placing total elapsed time from IPO to inclusion at approximately 24 calendar days.

Passive investors cannot avoid this exposure in most retirement account structures. Understanding which funds carry it and approximately when it arrives allows informed decisions about any additional discretionary exposure.

Academic and practitioner research around major index additions documents a consistent pattern. Prices tend to rise ahead of the effective inclusion date as event-driven and arbitrage capital positions in anticipation of the forced buying. Once the mechanical demand subsides and those positions unwind, prices frequently underperform.

The documented pattern: prices move up into the inclusion date, then frequently underperform afterward as event-driven positions unwind and mechanical demand subsides.

Tesla’s S&P 500 inclusion in December 2020 remains the primary precedent. The majority of price appreciation occurred before the inclusion date. Investors who attempted to front-run the event frequently held positions through the subsequent reversion. The pattern is directional, not deterministic; the exact magnitude of any inclusion premium is unknowable in advance.

SpaceX presents a more acute version of this dynamic for three reasons. First, the timeline is compressed: as few as 15 trading days from listing to eligibility, compared with the prior three-month minimum at Nasdaq. Second, the float is restricted to roughly 5% of outstanding shares, meaning all the mechanical buying pressure concentrates into a fraction of the market cap. Third, two major index families are involved simultaneously, layering Russell-driven demand on top of Nasdaq-driven demand in the same window.

The combination of compressed timing, tight float, and dual-index inclusion creates conditions for a sharper and potentially more volatile inclusion premium than a standard large-cap addition. Historical data informs the directional risk; it does not determine the outcome.

The geopolitical risks embedded in the SpaceX equity story add a structural complication that standard index inclusion analysis omits: Starlink’s dependence on government contracts and its exposure to adversarial state threats means passive holders absorb not just a concentrated, illiquid position but one whose fundamentals are partly determined by factors outside conventional financial modelling.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The rule changes, the float constraint, and the mandatory buying mechanism are not separate concerns. They are one connected system. Passive investors are participants in that system whether or not they actively chose to be.

The practical orientation for investors holding index-tracking funds comes down to three steps:

SpaceX exposure is expected to appear in Nasdaq-100 and Russell tracking funds within approximately four weeks of the 12 June 2026 IPO. The forced buying absorption window runs from late June or early July through the effective inclusion date and several days following. The question for passive investors is not whether they will own SpaceX. That decision has already been made by the index rules. The question is whether they add to it deliberately, and October gives them a more appropriate window to answer it.

For investors who want a framework for thinking about the position sizing implications of an involuntary holding like SpaceX, our dedicated guide to managing ETF concentration risk examines the core-and-satellite approach in detail, covering how broad index ETFs interact with concentrated single-stock exposures and the volatility trade-offs involved when one constituent grows to dominate an index’s effective weight.

These statements reflect projected timelines and scenario-based estimates. Actual inclusion dates, index weights, and price behaviour are subject to index committee discretion and market conditions.

SpaceX index inclusion refers to the process by which SpaceX shares are added to major indexes like the Nasdaq-100 and Russell 1000, triggering mandatory purchases by ETFs and index funds that track those benchmarks, meaning millions of 401(k) holders will automatically own SpaceX shares without placing an order.

ETFs expected to carry SpaceX exposure include QQQ and QQQM (Nasdaq-100 trackers), IWB (iShares Russell 1000 ETF), IWV (iShares Russell 3000 ETF), and IWF (iShares Russell 1000 Growth ETF), along with many target-date and 401(k) default funds that hold combinations of these.

Nasdaq updated its methodology effective 1 May 2026 to allow top-40 market cap companies to enter the Nasdaq-100 after just 15 trading days, down from a three-month minimum, while FTSE Russell confirmed a parallel change on 26 May 2026 permitting inclusion as early as the fifth trading day after listing.

With roughly 95% of shares locked up and only about 555-556 million shares in the public float, all the mechanical buying generated by SpaceX's multi-trillion-dollar index weight must be absorbed by a very small pool of available shares, which can concentrate demand and distort price during the inclusion window.

Tesla's December 2020 S&P 500 inclusion showed that most price appreciation tends to occur before the effective inclusion date as arbitrage capital positions ahead of forced buying, with prices frequently underperforming afterward as those event-driven positions unwind and mechanical demand subsides.