Why AI Is Splitting Semiconductor Stocks From the Rest of Tech

42 mins ago

Bank of America’s latest European equity strategy note, published on 26 June 2026, reads less like a buy list and more like a warning label. The sectors it flags, the risks it quantifies, and the defensive positioning it recommends all point in one direction: the most popular trades in European equities have accumulated enough valuation and momentum risk that the priority is knowing where not to be.

That framing matters. Partial macro relief has arrived. A U.S.-Iran peace agreement has eased geopolitical risk premiums. U.S. employment growth has recovered. Neither was enough to shift BofA’s overall cautious posture. Cyclicals remained underweight relative to defensives in the bank’s positioning, with AI-enabling sectors and banks carrying significant momentum-driven price risk flagged as the areas most vulnerable to a sharp repricing.

Here is what the note actually gives you: a sector-by-sector diagnostic for identifying which parts of your European equity exposure carry asymmetric downside risk, why banks face a compounding problem that goes beyond the usual cyclical story, and how to build a defensive counterweight without stepping out of equities entirely.

Most strategy notes lead with a conviction buy. BofA’s does something different. Its June 2026 European equity note is structured around what to underweight, making the avoid list the primary strategic output rather than a single sector recommendation.

That distinction is worth pausing on. Even with two meaningful macro tailwinds in play (the U.S.-Iran peace agreement and recovering U.S. employment), BofA held its cautious positioning. The implication is that the risk being flagged is not cyclical. It is structural to valuations and momentum flows, which means it will not resolve on its own as macro conditions improve.

That cautious posture sits within a broader pattern: a BofA sell signal triggered in May 2026 when the bank’s Bull and Bear Indicator reached 8.0, a level reached only 18 times since 2002, driven by record fund manager equity overweights and technology inflows of approximately $9 billion in a single week.

The four sectors BofA identified as overextended:

The actionable move here is not to panic-sell cyclicals. It is to audit your current overweights before building any new positions.

European banks have had a strong run, and the earnings story behind it is real. Rate-driven improvements in net interest margins have lifted profitability across the sector. That is the fundamental case, and it has not disappeared.

The problem is what has been layered on top. According to BofA, banks occupy the leading position by weight within European equities’ high-momentum basket. Systematic and momentum-driven strategies have amplified the price run well beyond what the earnings improvement alone would justify. Banks now sit at the intersection of two separate risk factors: cyclical earnings sensitivity and momentum flow dependency.

That combination creates a compounding vulnerability. If momentum selling begins, banks face drawdowns driven not by deteriorating fundamentals but by systematic flow reversals. BofA’s note raises a scenario worth stress-testing directly.

The scale of that vulnerability became visible in early June 2026, when a momentum factor unwind erased approximately 9.5-10% from high-beta equities in a single session, the worst one-day loss for this factor since the COVID-19 era, while the S&P 500 simultaneously held firmly positive for the year.

If European bank prices fell 20-30% purely on systematic momentum selling, with fundamentals unchanged, would your current position sizing still be comfortable?

Three diagnostic questions to apply to your own bank holdings:

The standard earnings-improvement thesis is not a sufficient justification for current sizing if the momentum overlay has made the position larger, in risk terms, than the fundamental case alone would warrant.

Two paths are reasonable. The first is trimming: if bank positions have drifted above their intended portfolio weight purely through outperformance, reduce them back to target. Position drift is not a thesis; it is an unmanaged risk.

The second is maintaining with tighter limits. If you choose to hold, prefer names with higher capital ratios, cleaner balance sheets, less exposure to structurally weak loan books, and geographic diversification across your bank holdings. Apply tighter stop-loss thresholds and treat the position as high-beta cyclical exposure, not a stable earnings compounder.

BofA is not calling AI a false thesis. The distinction matters. The concern is that semiconductors, capital goods, and mining may already be priced for near-perfect execution of the AI capex ramp, leaving no room for a slower, later, or more cyclical trajectory than consensus expects.

The relevant question for your holdings is not whether AI spending will materialise. It is whether your current position prices in anything less than perfect execution. If it does not, the risk-reward is asymmetric to the downside at current entry points, regardless of how bullish you are on AI infrastructure demand.

AI stock valuation risk is compounded by a structural feature of broad indices: low headline volatility can mask violent distributional divergence between individual winners and losers, leaving investors exposed to single-stock concentration they believe they have diversified away through passive index exposure.

Apply this scenario-test framework to each AI-linked position:

| Sector | AI Narrative Driver | Key Valuation Risk | Scenario-Test Variable | Rotation Alternative |

|---|---|---|---|---|

| Semiconductors | Data centre and AI chip demand | Multiples assume sustained order growth at peak rates | Capex ramp timing and magnitude | Industrials with diversified revenue streams |

| Capital goods | AI infrastructure and electrification buildout | Order books priced for multi-year acceleration | Speed and cyclicality of capex deployment | Utilities with grid exposure |

| Mining | Electrification-driven commodity demand | Demand assumptions may be fully embedded in spot prices | Commodity demand growth versus consensus | Defensives with commodity-cost hedging |

The rotation guidance is scale back, not exit. Reduce overweight positions, rotate toward names with broader demand drivers beyond AI and data centres, and favour stronger balance sheets and diversified end markets. Replacing part of your pure AI-enabler exposure with a combination of diversified industrials and grid-exposed utilities builds a more balanced risk profile without abandoning the theme entirely.

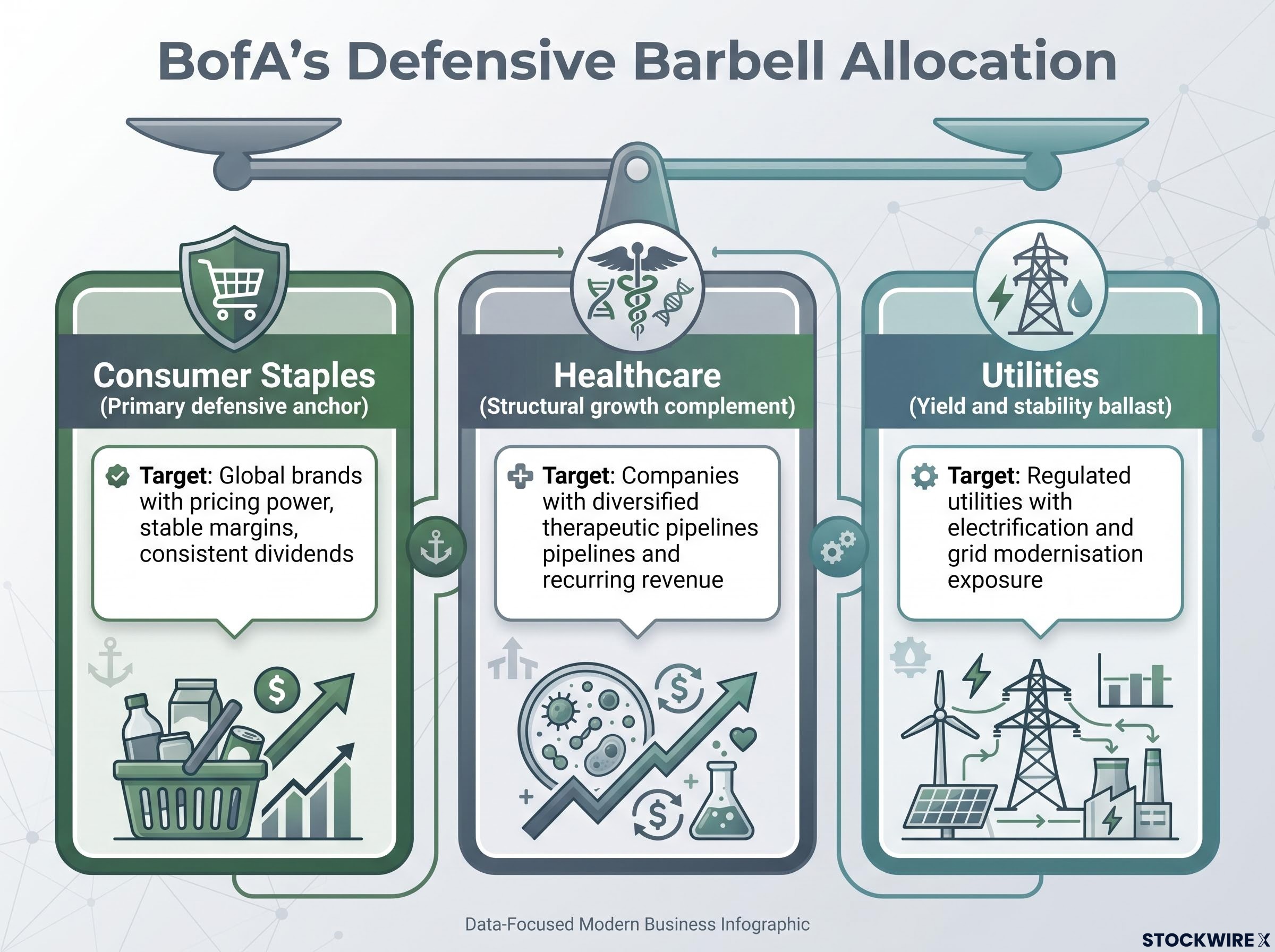

BofA’s preference for consumer staples is not a defensive parking move. The sector serves a dual purpose: it offers fundamental earnings resilience (stable margins, pricing power, consistent dividends) and stands as a likely destination for flows if momentum in cyclicals unwinds. Sizing it correctly relative to your benchmark matters as much as the selection itself.

The implementation focus is specific. Target global brands in food, beverages, and personal care with demonstrated pricing power, strong cash flows, and consistent dividend histories. Avoid staples names with extreme leverage or heavy emerging-market foreign exchange risk, both of which would undermine the defensive thesis at precisely the moment you need it to hold.

BofA frames this as part of a broader defensive barbell, pairing staples with healthcare and utilities to build a diversified defensive allocation.

| Sector | Core Rationale | What to Target | What to Avoid | Role in Barbell |

|---|---|---|---|---|

| Consumer staples | Earnings resilience plus flow destination in a momentum unwind | Global brands with pricing power, stable margins, consistent dividends | Names with extreme leverage or heavy EM FX risk | Primary defensive anchor |

| Healthcare | Structural demand driver, defensively characterised earnings | Companies with diversified therapeutic pipelines and recurring revenue | Single-product or binary-outcome names | Structural growth complement |

| Utilities | Regulated returns with grid exposure upside | Regulated utilities with electrification and grid modernisation exposure | Names with heavy rate sensitivity or concentrated policy risk | Yield and stability ballast |

Sizing considerations for the defensive allocation:

BofA’s positioning is a tilt, not a prophecy. Three substantive counterpoints deserve weight before you commit to the full rotation.

| Risk Scenario | What It Implies | How to Mitigate Without Abandoning the Tilt |

|---|---|---|

| AI capex accelerates beyond consensus | Underweighting AI-linked cyclicals too aggressively means missing a continued multi-year capex wave | Retain some cyclical exposure; scale back rather than exit entirely |

| Defensives underperform in a sustained high-rate environment | Staples and utilities may remain unloved if investors prefer fixed-income yields over defensive equity dividends | Diversify the defensive leg across staples, healthcare, and utilities rather than concentrating in one |

| Global cycle surprises to the upside | Stronger growth or further rate cuts could reignite cyclical outperformance regardless of elevated starting valuations | Keep cyclical allocation at or near benchmark (not zero) to preserve upside optionality |

The common thread across all three mitigations is the same: avoid extreme positioning. No all-in defensives, no zero cyclicals.

Adjust over weeks or months rather than in a single trade. Pair sector calls with formal risk management tools: position limits, volatility targets, and periodic stress tests. The rebalancing process itself should be staggered to avoid locking in a single view at a single moment.

These counterpoints mean the strategy’s value is not in being definitively right about the AI trajectory. It is in building a portfolio that does not rely on near-perfect execution of one scenario to avoid serious drawdown. Knowing the limits of the framework helps you calibrate how aggressively to tilt, which is as important as the direction of the tilt itself.

The framework is clear. The question is what to do first.

This is a tilt, not an exit. Some cyclical exposure is retained deliberately, preserving upside if growth and AI spending surprise positively. The goal is asymmetric repositioning: reducing concentration in the segments most vulnerable to a momentum reversal while building a genuine defensive counterweight that captures both earnings stability and flow rotation.

For investors who want to quantify exactly how much of their portfolio’s risk is concentrated in high-momentum positions before beginning the rebalancing sequence, our dedicated guide to beta-weighted position sizing explains how to convert each holding into market-risk equivalent dollars and apply volatility targeting to set deliberate exposure limits.

The sequence matters because implementation paralysis is the most common response to sector rotation guidance. Knowing what to do first, second, and third turns a directional view into a concrete process.

BofA’s core argument is one of asymmetry. Certain parts of the European equity market, specifically semiconductors, capital goods, mining, and banks, have accumulated downside risk from the combination of valuation stretch and momentum dependence that is not symmetrical with their remaining upside.

The decision-point is straightforward. The cost of repositioning now is some missed upside if AI momentum continues to extend. The cost of not repositioning is exposure to a momentum unwind across the most crowded parts of the market simultaneously.

The cost of inaction is not philosophical. It is structural, and it concentrates in the sectors that have already outperformed the most. A momentum reversal does not announce itself, and the positions with the largest systematic flow component are the ones that reprice fastest when the selling starts.

BofA’s resolution is not to leave equities. It is to stay invested, reduce the most overextended positions, and build a genuine defensive counterweight through a benchmark-relative tilt. The question is not whether you believe in AI. It is whether your current European equity positioning is built to absorb a momentum shock in the most crowded sectors without requiring a macro call to go right.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A defensive barbell pairs sectors with stable, recurring earnings such as consumer staples and healthcare with yield-generating utilities, creating a portfolio counterweight that captures both earnings resilience and flow rotation if cyclical momentum unwinds.

European banks face a compounding risk: rate-driven earnings improvements are real, but systematic momentum strategies have amplified prices well beyond what fundamentals alone justify, meaning a momentum unwind could trigger sharp drawdowns even without any deterioration in bank earnings.

BofA identifies semiconductors, capital goods, mining, and banks as the four overextended sectors, all flagged for combining valuation stretch with dependence on momentum flows that could reverse rapidly.

The key test is to assess what earnings and capex trajectory is already priced into current multiples, then estimate fair value if AI capex growth runs 20-30% slower or starts six to twelve months later than consensus, identifying how sensitive the position is to anything less than perfect execution.

The sequence starts with mapping your current sector weights against a European equity benchmark, then reducing overweights in semiconductors, capital goods, mining, and banks to at or below benchmark, and finally increasing allocations to consumer staples, healthcare, and utilities so total defensive exposure sits clearly above benchmark.