Morgan Stanley Rules Out Fed Hikes, Names Two Numbers to Watch

1 hr ago

Barclays published a client note today warning investors to expect sustained equity market turbulence through summer 2026. This is not a routine caution about short-term choppiness. It is the first major institutional signal that the Federal Reserve’s policy shift under Chair Kevin Warsh is now actively repricing risk across markets, and that the adjustment is far from over.

The warning lands while equity investors are still processing Warsh’s hawkish debut at the June 16-17 Federal Open Market Committee (FOMC) meeting. Treasury yields in real terms have climbed past the upper boundary of their trading range this year. The dollar has strengthened sharply. And September rate hike speculation, once a fringe view, is now showing up in institutional positioning. This is a regime shift story, not a passing wobble.

Here is what today’s Barclays note tells you about the months ahead: which forces are compounding the pressure on stocks, why September’s Fed meeting is already moving markets today, and how to think about positioning when the central bank backstop you have long relied on may no longer function the way it once did.

When a major Wall Street bank tells clients the rules have changed, the language matters. Barclays analyst Emmanuel Cau used a specific phrase in his June 26, 2026 client note: a “new Fed reality.”

Emmanuel Cau, Barclays: The current market environment reflects a “new Fed reality” under Chair Warsh, where the old assumptions about central bank responsiveness no longer hold.

That phrase is doing more work than it looks. Cau is not describing a single hawkish meeting. He is describing a structural change in how the Fed is perceived to operate. Warsh’s first FOMC meeting on June 16-17 was read by markets through three specific lenses:

Warsh’s adoption of strategic ambiguity, stripping all forward guidance from a statement that ran less than half the word count of its predecessors, means every incoming data point now carries direct rate-path implications that the Fed previously absorbed and interpreted on investors’ behalf.

The fundamental change here is in the perceived reaction function, the market’s understanding of how the Fed responds to economic data and market stress. That uncertainty, on its own, is a source of ongoing stock market volatility. Both the sharp move higher in the dollar and the breach of the year’s prior real rate ceiling trace back directly to this post-meeting repricing.

For your portfolio, the implication is concrete: the so-called “Fed put” (the long-held belief that the central bank would move quickly to stabilise markets during stress) has eroded. If your positioning has implicitly counted on that backstop, the risk calculus just changed.

Barclays identifies three structural drivers behind the current equity pressure. They are worth understanding as a system rather than separate items, because each one reinforces the others.

Real interest rates (interest rates adjusted for inflation) pushed through the ceiling of their year-to-date trading range in the wake of the June FOMC meeting. The mechanics matter:

The breach of the real yield ceiling that had capped the 10-year TIPS benchmark through most of 2026 is not simply a bond market event; at 2.22%, the yield establishes a materially higher hurdle rate that every equity valuation model running pre-Warsh assumptions is now systematically understating.

The post-Warsh dollar surge is not purely a domestic issue. It transmits stress globally and that stress re-enters U.S. equities:

Because these three forces, real rates, dollar strength, and policy uncertainty, are mutually reinforcing, a partial easing in one (say, a softer inflation print) may not be enough to break the volatility cycle if the other two remain elevated. That is what makes this environment structurally different from a single-catalyst pullback.

Barclays’ economics team does not treat a September rate hike as its base case. But the note explicitly identifies the September 15-16 FOMC meeting as a live and increasingly priced-in risk.

Barclays economics team: A September rate hike is not the central forecast, but it is a live risk that markets are increasingly pricing in.

That distinction matters less than you might think. The mere pricing-in of a possible hike is already altering equity behaviour today. For the first time in years, markets are assigning genuine probability to the next U.S. rate move being a hike rather than a cut. That repricing is happening now, not in September.

The dot plot revision from 3.4% to 3.8% as the median year-end rate projection placed at least one 25 basis point hike into the Fed’s own baseline, a shift that moved September from a theoretical risk into a scenario the committee itself is openly planning for.

| Market Expectation | Before Warsh’s First Meeting | After Warsh’s First Meeting |

|---|---|---|

| Rate direction expectation | Next move likely a cut | Next move could be a hike |

| Fed put assumption | Backstop broadly intact | Backstop credibility diminished |

| Volatility regime expectation | Contained, short-lived spikes | Sustained, structurally elevated |

The broader context compounds the pressure. The global monetary easing cycle that defined the past two years is fading. Central banks are no longer uniformly cutting rates. September is a symptom of that macro shift, not an isolated calendar event, and it means the volatility is unlikely to calm materially before the meeting arrives.

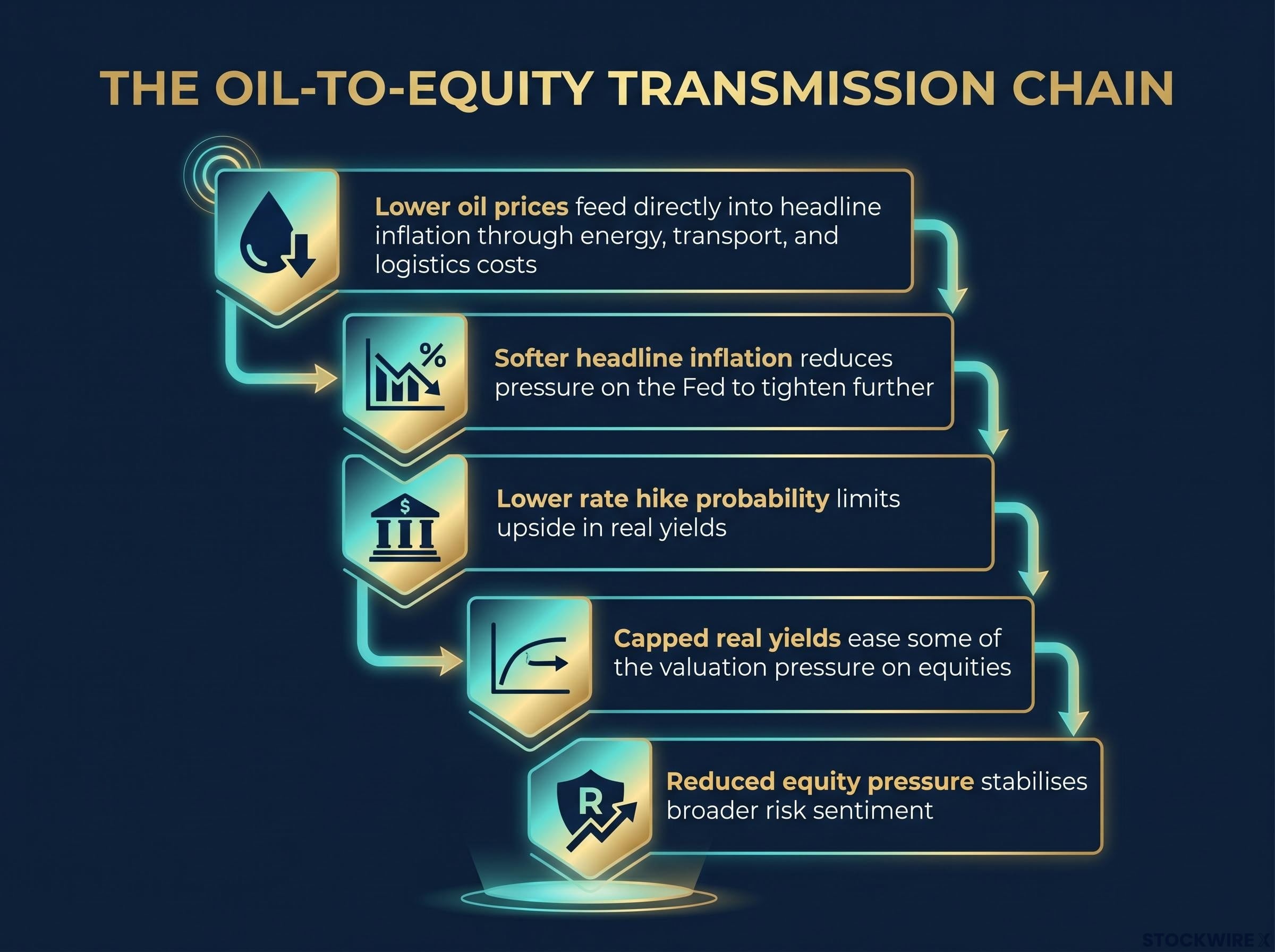

This is the variable most equity-focused investors are underweighting. Barclays points to lower oil prices as among the most significant factors that could curb further hawkish repricing, and the transmission chain explains why.

That chain makes oil a macro signal, not just a commodity price. But Barclays is explicit about the caveat: falling oil does not eliminate tighter policy risk. It is a moderating factor, potentially significant, but not a guarantee against a September hike.

For investors watching crude this summer, the relevant question is not just what oil prices mean for energy sector earnings. It is what they signal about whether the Fed has room to hold rates steady in September. That dual significance makes oil one of the most information-dense prices to track in the months ahead.

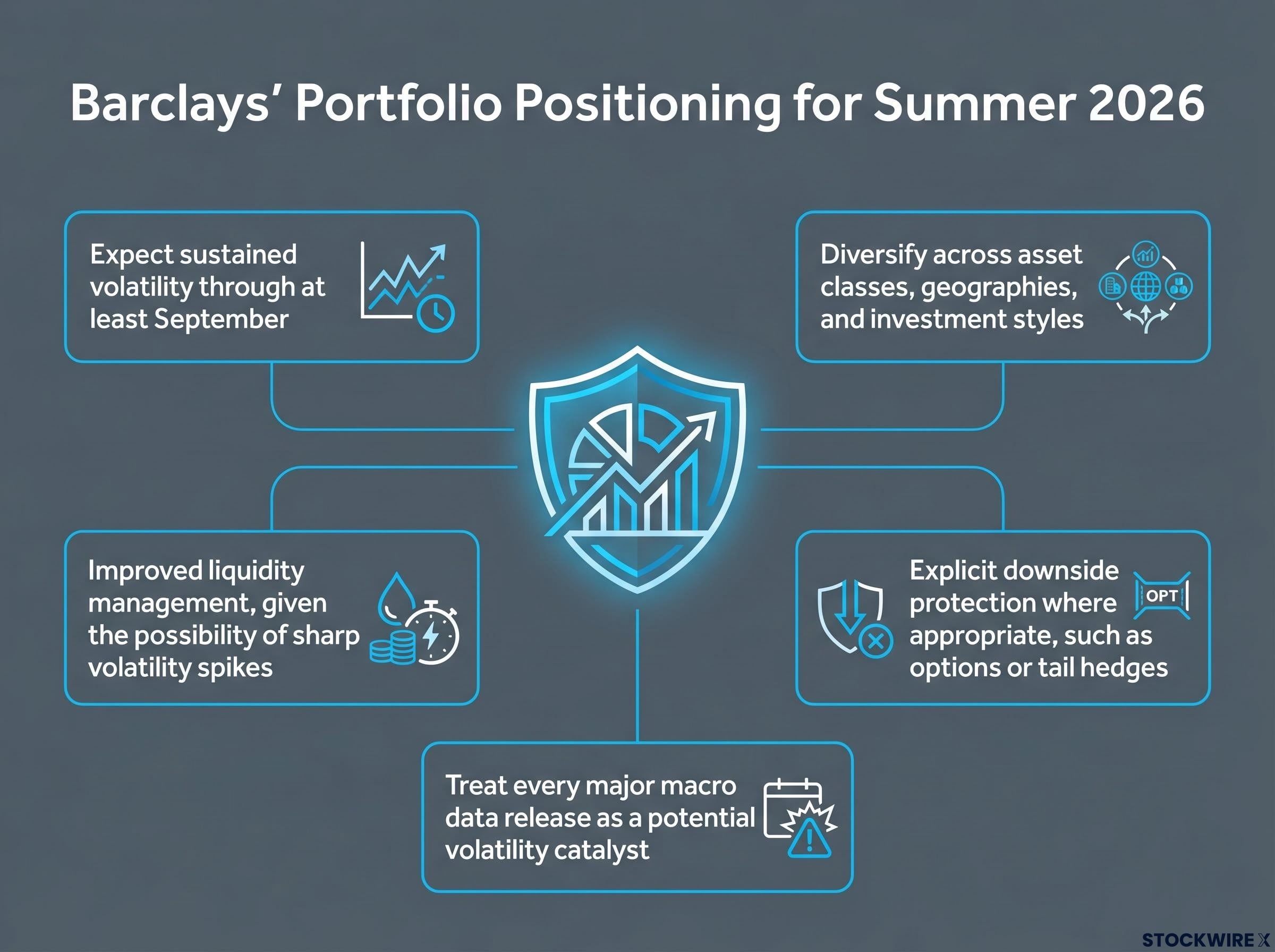

Barclays’ note carries four practical implications for portfolio positioning:

The specific positioning orientations Barclays flags include:

With September as a live hike risk, each incoming data point (Consumer Price Index prints, payrolls reports, GDP revisions) is now capable of moving rate expectations and therefore equity markets materially. This hypersensitivity to data is a feature of the current environment, not temporary noise.

Portfolios built for a world where the Fed reliably intervened during market stress are now carrying more unpriced risk than their owners may realise. This is not a call to exit equities. It is a call to stress-test the assumptions that were reasonable in a different rate environment and adjust where those assumptions no longer hold.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Three variables will determine how the rest of summer 2026 unfolds. They are worth tracking explicitly:

If September delivers an actual hike, it would represent the first tightening move under a more hawkish Fed chair, a potential reset of equity risk premia, and a confirmation that the old Fed put assumptions are definitively outdated. That is a meaningful regime change, not a routine policy adjustment.

But whether or not the hike materialises, the volatility regime Barclays describes is already operating. Barclays’ note is not a call to abandon equities. It is a call to enter the second half of 2026 with clear-eyed assumptions about a structurally different macro environment, one where the adjustment to a new Fed reality is not a future event but a present one.

For investors reassessing their strategic allocation in light of the structural macro shift Barclays identifies, our full explainer on portfolio resilience examines why the stock-bond negative correlation that underpinned conventional diversification has broken down during inflation shocks and what frameworks now offer genuine protection.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Fed put is the market assumption that the Federal Reserve would move quickly to stabilise equities during periods of stress, effectively providing a floor under prices. Barclays warns that this backstop has eroded under Chair Kevin Warsh, meaning portfolios that implicitly relied on rapid Fed intervention now carry more unpriced risk than their owners may realise.

Barclays analyst Emmanuel Cau identifies three mutually reinforcing structural forces: real interest rates breaching their year-to-date ceiling, a sharp post-Warsh dollar surge weighing on multinational earnings, and genuine uncertainty about the Fed's new reaction function under Chair Warsh following his hawkish June 16-17 FOMC debut.

A September hike would represent the first tightening move under a more hawkish Fed chair, potentially resetting equity risk premia and confirming that the old Fed put assumptions are definitively outdated, according to Barclays. Markets are already repricing this possibility today, not waiting for September to arrive.

Higher real rates increase the discount rate applied to future corporate earnings, which directly compresses equity valuations, especially for growth stocks where cash flows sit years in the future. With the 10-year TIPS yield at 2.22%, every equity valuation model built on pre-Warsh assumptions is now systematically understating the hurdle rate, per Barclays.

Barclays recommends diversifying across asset classes, geographies, and investment styles, adding explicit downside protection such as options or tail hedges, and improving liquidity management to handle sharp volatility spikes. The firm also advises treating every major macro data release, including CPI prints and payrolls reports, as a potential volatility catalyst until the September Fed meeting clarifies the rate path.