How Australia’s Largest CFD Penalty Exposed a Broken Model

3 hrs ago

The largest stock market listing in history priced on 11 June 2026 at $135 per share, placing SpaceX at a valuation near $1.75 trillion and raising approximately $75 billion in a single transaction. This is not merely a technology IPO. SpaceX simultaneously occupies the roles of defence contractor, satellite infrastructure operator, and geopolitical actor, and the sheer scale of the capital raise carries measurable implications for institutional portfolios, index dynamics, and competing asset classes including gold and cryptocurrency. An Iranian threat against Elon Musk’s Middle East interests landed the day before pricing, embedding geopolitical risk into the equity story from the outset.

What follows covers the deal’s record-setting mechanics, how the $135 price was negotiated, what the $1.75 trillion valuation actually prices in, why geopolitical risk is now a permanent feature of this stock, how the listing moved markets across commodities and crypto on 12 June 2026, and what investors across different time horizons should consider now.

The numbers are difficult to contextualise without a benchmark. The previous record holder, Saudi Aramco’s 2019 listing on the Saudi Exchange, raised approximately $25.6-$29 billion at an initial valuation near $1.7 trillion. SpaceX surpassed it on both dimensions simultaneously: roughly $75 billion in proceeds and an implied market capitalisation of $1.75-$2.0 trillion at listing on Nasdaq, with trading scheduled to commence on 12 June 2026.

The record-breaking nature is not simply a function of company size. It reflects institutional demand deep enough to absorb tens of billions of dollars of new stock at a single price point without destabilising the opening session.

| Metric | SpaceX (2026) | Saudi Aramco (2019) |

|---|---|---|

| Capital raised | ~$75 billion | ~$25.6-$29 billion |

| Valuation at listing | ~$1.75-$2.0 trillion | ~$1.7 trillion |

| Exchange | Nasdaq | Saudi Exchange (Tadawul) |

| Year | 2026 | 2019 |

Aramco was a mature, high-cash-flow energy producer priced at the top of a commodity cycle. SpaceX is a technology-driven infrastructure platform priced on long-duration growth assumptions. The two deals share almost nothing in business model, yet SpaceX eclipsed Aramco’s capital raise by a factor of nearly three, a signal of how far institutional appetite for dual-use technology and space infrastructure has expanded in seven years.

An IPO price is not set by decree. It is a negotiated equilibrium between what the issuer wants to raise and what the market’s largest capital pools are willing to pay. For a deal of SpaceX’s magnitude, the process follows a mechanical sequence.

Price too high, and the stock trades below its offer on day one, a “broken IPO” that damages the issuer’s credibility. Price too low, and the issuer leaves billions on the table in an unnecessary first-day pop.

The final price of $135 signals that underwriters identified institutional appetite deep enough to support the largest single-day capital raise in market history. For retail investors unfamiliar with this process, the number is not arbitrary. It is the output of weeks of direct demand measurement from some of the world’s largest allocators.

SpaceX generates revenue from two primary streams. The first is launch services, covering commercial satellite deployment, NASA missions, and United States Department of Defence contracts. The second is Starlink, its satellite broadband network serving consumers, enterprises, and government users across dozens of countries.

Starlink subscriber and revenue estimates from industry research indicate the network surpassed 10 million subscribers by early 2026 and generated approximately $11.4 billion in revenue during 2025, representing around 61 percent of total SpaceX income, a revenue mix that underpins much of the growth trajectory investors are paying for at $135 per share.

A $1.75 trillion valuation implies very high multiples on current revenues and cash flow. Investors at this price are not paying for what SpaceX earns today. They are paying for a specific growth trajectory: deepening dominance in orbital launch, scaling Starlink into a large-margin cash generator, and potentially monetising new lines including in-space infrastructure and defence systems.

The comparable problem is real. SpaceX sits at the intersection of defence contractor, satellite operator, and platform technology company. No single peer group captures the business accurately, which makes investor discipline on valuation assumptions more important than usual.

The orbital compute thesis sits at the most speculative corner of the SpaceX investment case: regulatory filings have been submitted for up to one million satellites, but no orbital data-centre hardware has been launched, and the xAI acquisition’s ground-based cluster, roughly 320,000 Nvidia accelerators, is the only confirmed AI asset on the balance sheet today.

At a valuation of this size, even modest deviations from the bullish growth path carry large dollar consequences. Scenarios investors should stress-test include:

The question is not whether the story is compelling. It is whether 10-year growth and margin assumptions can realistically justify, and ultimately exceed, a $135 entry price.

Iran issued threats against Elon Musk’s Middle East business interests, including Starlink operations in the region, on 10 June 2026, the day before the IPO priced. The timing was striking. It was not coincidental in its effect.

The relationship between geopolitical risk and equity pricing is less intuitive than most headlines suggest: markets process escalation events as probability-adjusted inputs to future earnings rather than as proportional shocks, which is why the S&P 500 closed near record levels on 29 April 2026 despite a drone strike disrupting 1.7 million barrels per day of Kazakh crude output.

This episode is not an isolated headline. It is an illustration of a structural reality. SpaceX is a direct geopolitical actor. Starlink has been deployed in active conflict zones and is used by Western militaries and allied governments. That strategic importance enhances valuation in one direction and embeds risk in the other.

Geopolitical exposure is not a one-off headline risk for SpaceX. It is a permanent, structural component of the equity’s risk-return profile, analogous to how defence contractors are evaluated, but with broader geographic unpredictability.

Once publicly traded, every headline involving sanctions, cyberattacks, signal jamming, or government access-control mandates can drive sudden repricing. Governments may push for greater control over where and how Starlink is deployed. Export controls, licensing restrictions, and diplomatic pressure are recurring vectors, not theoretical ones.

Investors unfamiliar with dual-use technology stocks may underestimate how quickly a single geopolitical development can move a name of this strategic significance. The Iran episode is the first such test. It will not be the last.

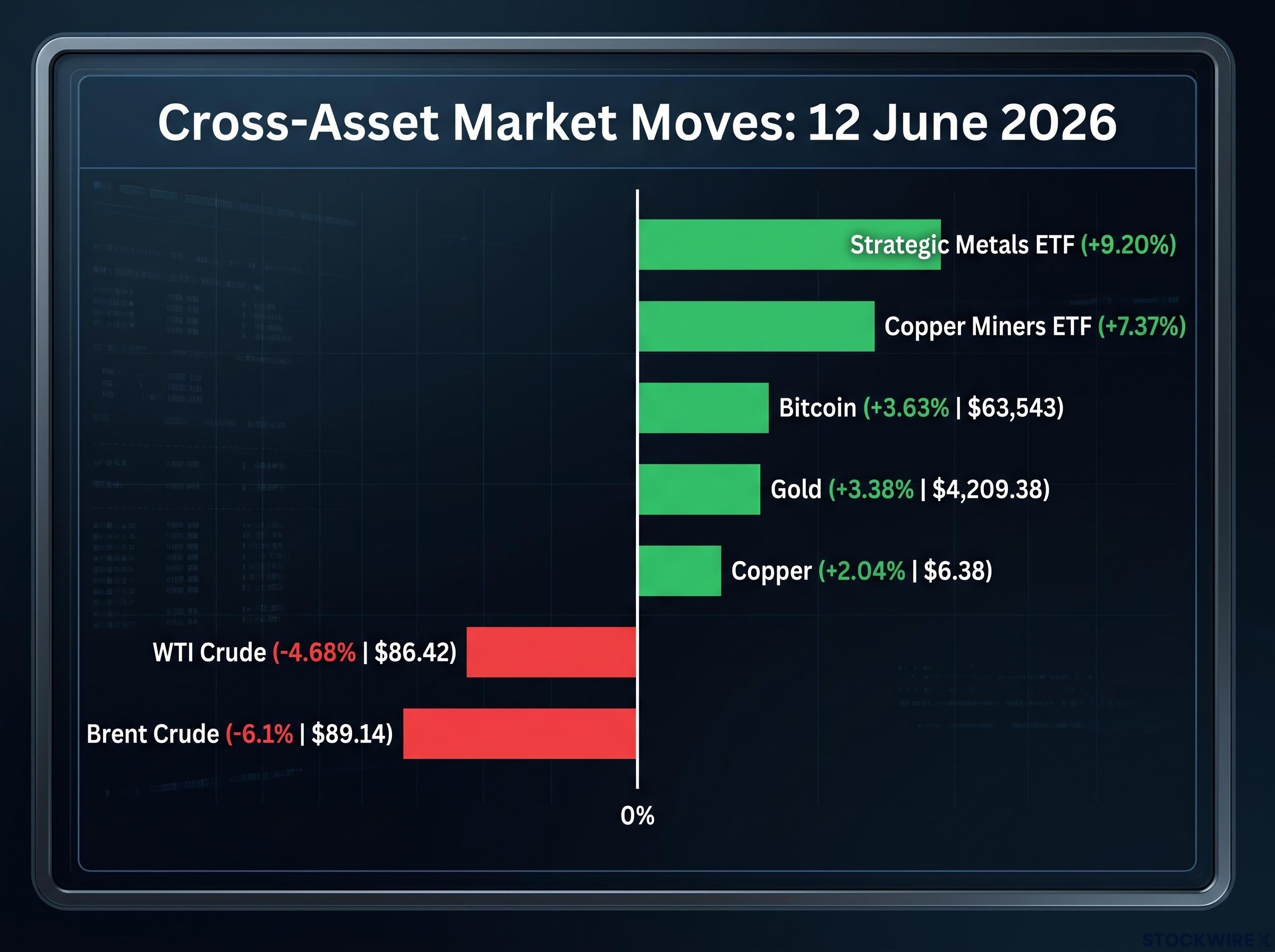

Markets moved sharply on 12 June 2026, SpaceX’s first trading day, though the primary catalyst was reduced geopolitical risk premium following the cancellation of an Iran strike rather than the listing itself. The cross-asset picture was complex.

| Asset class | Representative | Move | Price level | Primary driver |

|---|---|---|---|---|

| Precious metals | Gold | +3.38% | $4,209.38 | Risk-on, reduced geopolitical premium |

| Industrial metals | Copper | +2.04% | $6.38 | Improved industrial sentiment |

| Crypto | Bitcoin | +3.63% | $63,543 | Risk-on, high-beta rally |

| Crypto | Ethereum | +4.44% | A$2,380 | Risk-on, high-beta rally |

| Energy | WTI Crude | -4.68% | $86.42 | Escalation risk priced out |

Mining and strategic metals equities posted even larger gains: the Strategic Metals ETF rose 9.20%, the Copper Miners ETF gained 7.37%, and the Gold Miners ETF climbed 5.30%. Brent crude fell 6.1% to $89.14, its lowest level since 6 March.

Analysts flagged a mechanism that may play out over weeks rather than hours. Large institutional investors sometimes sell liquid alternatives, including gold, cryptocurrency, and sovereign bonds, to raise cash for participation in mega-deals. Despite the expected selling pressure, gold and crypto both rose on 12 June, suggesting the concurrent risk-on environment overwhelmed any liquidity drain.

The tension is real, however. Macro “risk-on” conditions support gold and crypto prices in the short term, while capital-raising “liquidity drag” from mega-IPOs could become a headwind over the medium term as institutional capital is reallocated. Investors with exposure to these assets should monitor whether periods of heavy primary-market activity correlate with directional shifts in flows and volatility.

Technology sector positioning among global fund managers reached its most extreme overweight level since before the 2021 peak in the weeks leading into the SpaceX listing, with sell-side consensus forecasts for tech growth now running above independent industry estimates, a reversal of the structural tailwind that drove repeated earnings beats across the prior cycle.

The brand, the vision, and the founder profile are powerful narrative forces. The discipline that matters here is simpler: whether the numbers can be made to work at $135 per share.

SpaceX’s listing is simultaneously a historic capital markets milestone and a portfolio-wide event with implications across technology, defence, commodities, and alternative assets. The $135 entry price demands a specific, modelable growth path across launch services and Starlink, and the Iran episode on 10 June is the first of many geopolitical reminders that this equity carries structural risk unlike any other listed name.

Investors who approach this deal with clear scenario thinking, rather than narrative enthusiasm, are better positioned for the volatility that a listing of this visibility will generate.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

SpaceX priced its IPO at $135 per share on 11 June 2026, implying a market capitalisation of approximately $1.75 to $2.0 trillion at listing on Nasdaq, making it the largest stock market listing in history by capital raised.

SpaceX raised approximately $75 billion in its IPO, nearly three times the capital raised by Saudi Aramco in its 2019 listing, which had previously held the record at around $25.6 to $29 billion.

The IPO price is determined through a bookbuilding process where underwriters conduct a roadshow, collect non-binding orders from institutional investors at various price levels, and set the final price at the level where demand is sufficient to absorb all shares without destabilising the opening session; SpaceX's $135 price reflected that demand was deep enough to absorb $75 billion in a single transaction.

SpaceX operates Starlink in active conflict zones and serves Western militaries, making it a direct geopolitical actor; threats from Iran against Elon Musk's Middle East interests arrived the day before the IPO priced, and ongoing risks include sanctions, export controls, signal jamming, and government access-control mandates that could drive sudden repricing.

On SpaceX's first trading day of 12 June 2026, gold rose 3.38% to $4,209.38 and Bitcoin gained 3.63% to $63,543, though analysts noted the primary driver was reduced geopolitical risk premium following the cancellation of an Iran strike rather than the listing itself, with the risk-on environment outweighing any liquidity drag from the capital raise.