On 3 June 2026, SpaceX disclosed a fixed offering price of $135 per share through an amended regulatory filing, bypassing the institutional roadshow process that has defined large-scale U.S. public offerings for decades. With approximately 555.5 million shares set for sale, the filing implies a company valuation of roughly $1.75 trillion and total proceeds of approximately $75 billion, figures that would make this the largest initial public offering in history. The market debut is planned for approximately one week after the announcement. What follows covers how the pricing broke from convention, what business the valuation reflects, how to interpret that $1.75 trillion figure, and what retail investors should verify before shares begin trading.

A $135 fixed price and no roadshow: how SpaceX broke from IPO convention

The surprise was not the size. It was the method.

In a standard U.S. IPO, the issuing company and its underwriters spend weeks on an institutional roadshow, gauging demand from large investors and building an order book before settling on a final price range. SpaceX skipped the entire process. The $135 price appeared in an amended regulatory filing on 3 June 2026, fixed and final, with a public debut scheduled roughly one week later.

The key figures from the filing:

- Price per share: $135

- Shares offered: approximately 555.5 million

- Total expected proceeds: approximately $75 billion

- Implied valuation: approximately $1.75 trillion

- Planned debut: approximately one week after 3 June 2026

The compressed timeline and fixed price reflect a deliberate structural choice by Elon Musk rather than an oversight. For investors, the absence of a roadshow removes the institutional demand signal that typically helps gauge how the market is receiving an offering before it begins trading. That signal will not exist here. The first real price discovery will happen on the exchange.

The compressed timeline and fixed price reflect a deliberate structural choice by Elon Musk rather than an oversight, and the implications run deeper than they first appear: the standard IPO mechanics for retail investors mean most public buyers cannot access shares at the offering price, instead entering the secondary market after institutional allocations have already been filled.

When big ASX news breaks, our subscribers know first

What SpaceX actually does: the business behind the valuation

Before assessing whether $1.75 trillion is reasonable, it is worth examining what the number is being asked to value.

According to the offering documentation, SpaceX’s operations span three segments:

- Space exploration and launch services, including commercial satellite deployment and government contracts

- Satellite communications, primarily through the Starlink broadband network

- Artificial intelligence operations

SpaceX has been described in offering materials as operating across “space exploration, satellite communications, and artificial intelligence.”

The company functions as the central asset within Elon Musk’s broader business portfolio, positioned not as a single-product rocket manufacturer but as a vertically integrated technology and infrastructure business with multiple revenue streams.

The orbital compute thesis embedded in SpaceX’s AI segment valuation rests on regulatory filings for up to one million satellites and an xAI acquisition that brought approximately 320,000 Nvidia accelerators onto the balance sheet, but no orbital data-centre hardware has been launched or confirmed with specific deployment dates as of mid-2026.

One gap investors should note: detailed revenue, profitability, and segment performance figures from the May 2026 S-1 filing were not captured in available research for this article. Readers considering an investment should consult the S-1 directly for financial specifics before making any decision.

Understanding IPO valuations: what $1.75 trillion actually means

An IPO valuation represents what the market is being asked to collectively believe a company is worth on day one of trading. It is calculated by multiplying the price per share by total shares outstanding. At $135 per share, the implied valuation of approximately $1.75 trillion would place SpaceX among the ten most valuable publicly traded U.S. companies, according to its own amended regulatory filing.

That figure is not a measure of current revenue or profit. It is a forward-looking price that reflects what buyers are willing to pay based on expectations about future growth, competitive position, and earnings potential. A high valuation does not mean a stock is expensive in the way a consumer product is expensive; it means the market is pricing in substantial future performance that has not yet materialised.

From private funding rounds to public market pricing

Until this offering, SpaceX was accessible only to institutional and accredited investors through private funding rounds, where valuations are set in negotiated transactions between a small number of parties.

A public listing changes the mechanics entirely. Once shares trade on an exchange, the price is set by continuous buying and selling across millions of participants. That creates daily liquidity, but it also introduces volatility that private investors did not face. The shift from private to public ownership represents a material change in risk profile, not just a change in access.

The governance structure investors should examine before trading

The scale of the offering and the optimism surrounding it warrant a closer look at what public shareholders would actually control.

Dual-class share structures, a governance arrangement where different classes of stock carry different voting rights, were noted in initial reporting as a point of discussion in the context of this offering. Under such structures, founders or insiders can retain majority voting control regardless of how much economic ownership public shareholders hold. This means company decisions on strategy, executive compensation, and capital allocation may remain under the control of a small group even after billions in public capital flows in.

A super-voting share structure that allocates disproportionate voting power to founders or insiders is not a passive governance quirk; at SpaceX, it means public investors purchasing shares at $135 will have no ability to influence strategic decisions, capital allocation, or executive leadership regardless of how large their collective economic stake becomes.

No formal regulatory objections or named SEC-level scrutiny of the SpaceX governance structure were identified as of 4 June 2026. The amended S-1 filing remains the authoritative source for the specific terms.

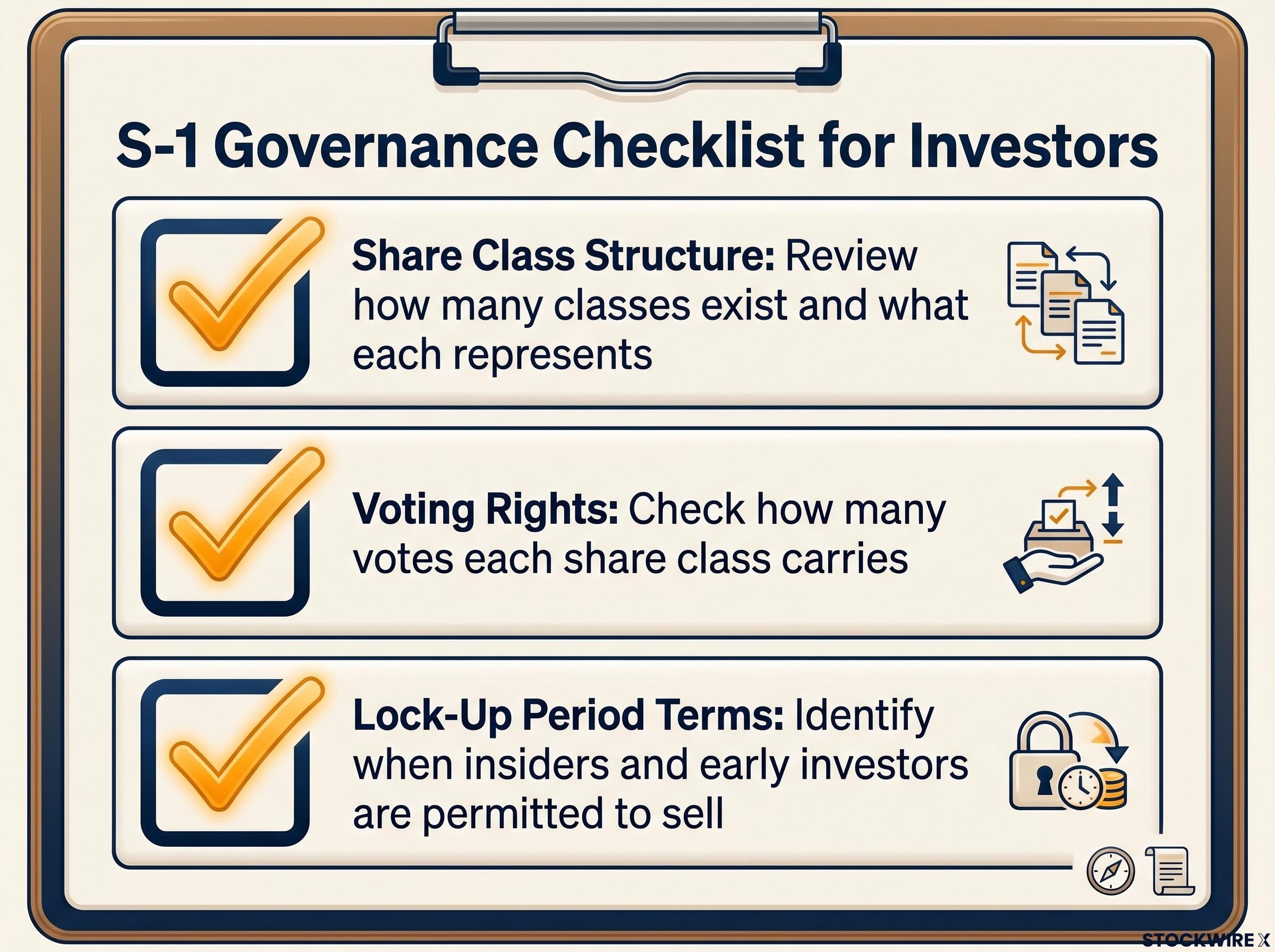

Before purchasing shares, retail investors should review three items in the S-1:

- Share class structure: how many classes exist and what each represents

- Voting rights per class: how many votes each share class carries

- Lock-up period terms: when insiders and early investors are permitted to sell

For a company led by a founder with a documented preference for operational autonomy, understanding voting rights is not a secondary concern. It determines how much influence public shareholders actually have.

What retail investors can and cannot know right now

Some facts are confirmed. Others are not yet available. Separating the two is the most useful thing a retail investor can do in the days before the debut.

| What Is Confirmed | What Remains Unknown |

|---|---|

| $135 per share fixed IPO price | Which brokerages will participate in the IPO allocation |

| Approximately $75 billion in total expected proceeds | Whether retail investors can buy at the $135 IPO price or only in secondary trading |

| Implied valuation of approximately $1.75 trillion | How IPO share allocations will be distributed |

| Debut planned approximately one week after 3 June 2026 | Post-announcement analyst commentary and institutional reaction |

| Approximately 555.5 million shares to be sold | What the secondary market opening price will be on debut day |

The absence of a roadshow means there is no institutional order book to signal demand levels ahead of trading. Secondary market pricing on debut day may differ significantly from the $135 fixed IPO price depending on how much demand materialises.

Retail investors should take three practical steps before the debut: check brokerage platforms for IPO access announcements, review the S-1 filing (particularly the financial statements and risk factors sections), and monitor financial news in the days leading up to trading.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The SpaceX debut is historic, but history does not guarantee returns

If completed on the disclosed terms, this would be the largest IPO in U.S. history. A $1.75 trillion valuation would place SpaceX among the most valuable publicly traded companies in the country from its first day of trading.

That scale is genuine. So is the uncertainty that accompanies it. Record-setting IPO size and investor enthusiasm have not historically guaranteed strong post-debut performance. A valuation at listing reflects expectations about future growth, not a guarantee of current earnings. The $135 price embeds assumptions about Starlink’s subscriber trajectory, launch services demand, AI revenue potential, and competitive positioning that have not yet been tested by public market scrutiny.

IPO cohort underperformance over multi-year holding periods is one of the most robust findings in market data, with newly listed companies trailing comparable established peers by an average of 3.3% per year across the first five years of trading, a drag that compounds into a material gap even when the underlying business performs reasonably well.

Two actions stand out before the debut: reading the risk factors section of the S-1 filing, which discloses what the company itself considers the material threats to its business, and monitoring brokerage IPO access announcements to understand whether participation at the offering price is even available.

The moment is historic. The investment decision should not be.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. These statements are speculative and subject to change based on market developments and company performance.