Brent at $126: What History Says About Stocks After an Oil Shock

just now

SpaceX is reportedly targeting a $75 billion raise at a valuation exceeding $2 trillion, a figure that would make it the largest initial public offering by dollar value in recorded market history, surpassing Saudi Aramco’s 2019 listing. A confidential SEC filing was completed around 1 April 2026, with a June roadshow and a dedicated retail investor event planned for 11 June to accommodate approximately 1,500 participants. For U.S. retail investors, this is not a passive news story but an active commercial decision with a short runway. This analysis breaks down the IPO’s structure and valuation, how retail investors can access shares, and what historical data reveals about long-term IPO performance, so readers can make an informed decision before the roadshow begins.

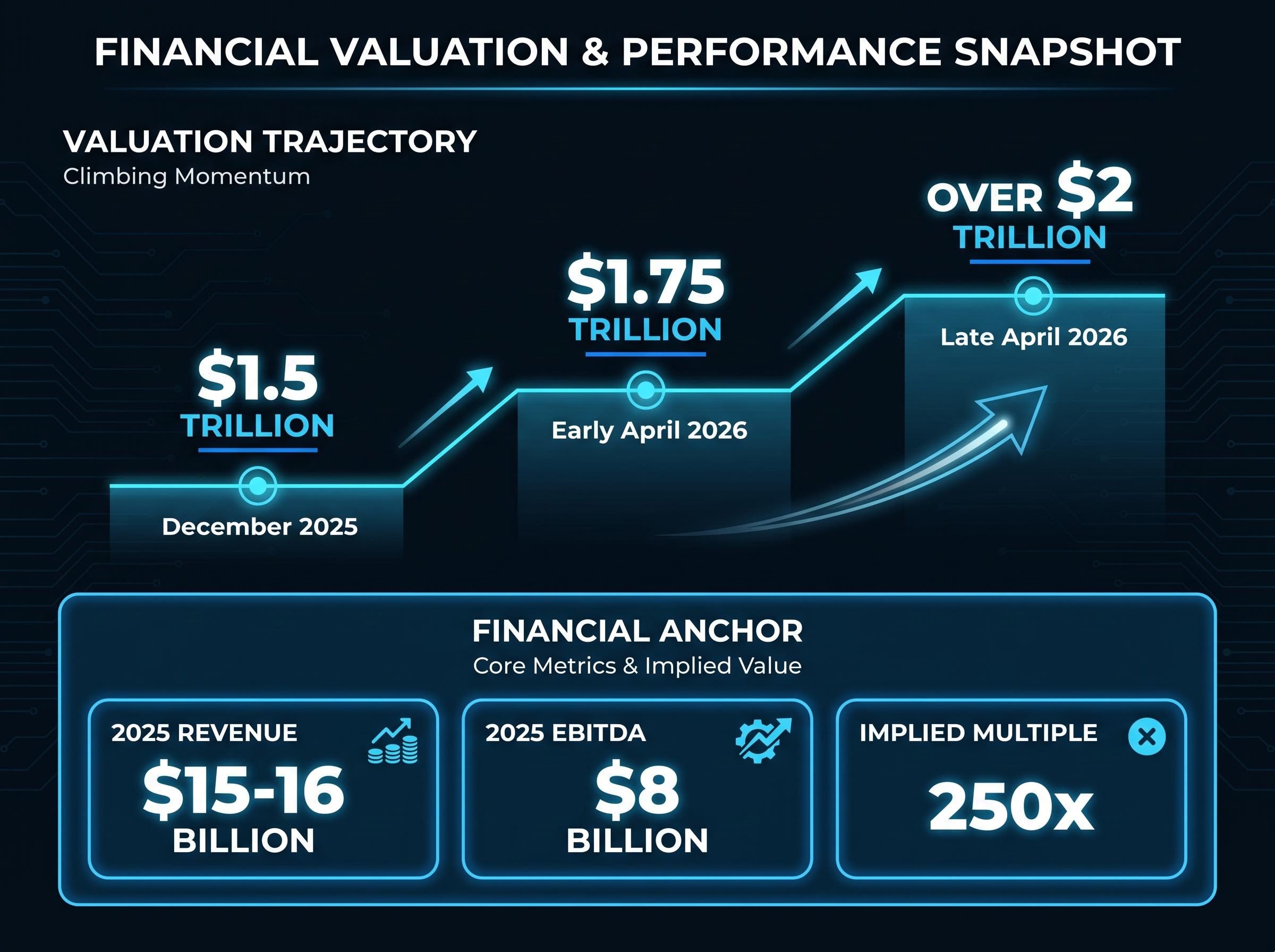

The headline numbers are large enough to obscure what they actually imply. SpaceX is targeting approximately $75 billion in fundraising proceeds at a valuation that has moved consistently upward: from $1.5 trillion in December 2025, to $1.75 trillion by early April 2026, to over $2 trillion in later April reporting from Reuters. If achieved, the offering would exceed Saudi Aramco’s record as the largest public listing in history.

| Reporting Period | Reported Valuation | Source |

|---|---|---|

| December 2025 | $1.5 trillion | TechCrunch (citing Bloomberg) |

| Early April 2026 | $1.75 trillion | Confidential filing reports |

| Late April 2026 | Over $2 trillion | Reuters |

The financial anchor behind that valuation trajectory tells a different story about the pricing logic. SpaceX reported approximately $15-16 billion in revenue for 2025.

Financial anchor: SpaceX reported approximately $8 billion in EBITDA for 2025. A $2 trillion valuation applied to $8 billion in EBITDA implies a multiple of roughly 250x, a figure that prices in decades of growth before a single public share changes hands.

Each upward valuation revision widens the gap between reported earnings power and the price investors are being asked to pay. That gap is where the analytical tension in this deal lives.

The most direct analyst signal available comes from FutureSearch.ai, which published an assessment on 1 April 2026 framing the IPO valuation as representing approximately 30% overpayment for SpaceX. The assessment stands out not because it is uniquely bearish but because no reviewed source characterised the valuation as fair or undervalued. The absence of a counterpoint is itself a meaningful data point about the direction of expert opinion.

Space sector IPO failures provide the clearest available data on what narrative-driven valuations produce when execution disappoints: Virgin Galactic fell from above US$1,100 per share in 2021 to under US$3 by 2026, a 99.7% destruction of shareholder value in a company that reached public markets through a SPAC rather than a conventional listing with revenue thresholds.

The predicted share price range at debut sits between approximately $400 and $1,200 per share, a wide band that reflects the medium confidence attached to any pre-S-1 estimate. Without a public filing, independent analysts are working from secondary market activity and private equity valuation structures rather than verified financials.

Leeds School of Business professor Shaun Davies has cautioned that the risks of participation are meaningful even for investors who ultimately choose not to buy in, citing overvaluation and volatility concerns.

No ticker symbol, listing exchange, final share count, or S-1 has been publicly released. The 11 June retail event details and syndicate composition beyond Morgan Stanley and **E*TRADE** remain unconfirmed from official sources. Retail investors entering this deal before the S-1 filing are committing capital based on incomplete information, a condition that favours the issuer rather than the buyer.

A standard initial public offering (where a private company lists its shares on a public stock exchange for the first time) follows a well-established sequence:

That sequence concentrates early access with institutional buyers. By the time retail investors can purchase shares, the price has usually moved. SpaceX’s reported structure departs from this model in several ways:

The structural intent is clear: broader retail access at the offering price. Whether that intent translates into guaranteed access for any individual investor remains a separate question, subject to brokerage relationships and allocation mechanics that have not been publicly detailed.

**E*TRADE is the primary confirmed retail access point, given Morgan Stanley’s** role as lead underwriter and ETRADE’s confirmed distribution position. Fidelity appears as a potential secondary participant, though its role is less central than ETRADE’s in available reporting.

Elon Musk denied through an X post that Robinhood and SoFi had been excluded from the IPO. Neither platform has confirmed participation as of the research period.

Platforms including Charles Schwab, Moomoo, Webull, Zacks Trade, and TradeStation were not referenced in Reuters reporting as having a confirmed role.

| Brokerage | Confirmed Role | Platform Strength | Key Limitation |

|---|---|---|---|

| E*TRADE | Lead retail distributor | Broad investment selection, educational resources | Weaker cash interest rates, navigation |

| Fidelity | Potential secondary participant | Multi-year NerdWallet awards, strong research tools | No futures trading, options fees apply |

| Robinhood | Unconfirmed (Musk denial of exclusion) | Commission-free trading, mobile-first design | Participation not verified |

| SoFi | Unconfirmed (Musk denial of exclusion) | Integrated banking and investing | Participation not verified |

For investors who want IPO-price access, the practical implication is direct: opening an **E*TRADE or Fidelity** account before the June roadshow may be necessary. That window is narrowing.

The SEC guidance on IPO share eligibility at Investor.gov specifies that brokerage firms assess factors including net worth, income, investment objectives, and trading history when determining which retail customers receive an allocation at the offering price, conditions that may exclude many standard account holders regardless of demand.

Before applying any conclusion to SpaceX, the base rate for IPO performance deserves examination on its own terms.

A Nasdaq analysis published 15 April 2021 found that approximately two-thirds of IPOs from 2010 to 2020 were underperforming broader market benchmarks by their third year of public trading.

The pattern is consistent with a well-documented dynamic: media attention and retail enthusiasm generate post-listing price spikes, but those initial surges tend not to sustain over a multi-year horizon. Investors who buy at debut expecting long-term outperformance are, statistically, more often disappointed than rewarded.

SpaceX accounted for approximately half of all orbital launches globally in 2025, a level of operational dominance that distinguishes it from the pre-revenue or early-revenue companies that populate most IPO cohorts. The business generates real cash flow, operates in a sector with significant barriers to entry, and holds government contracts that provide revenue visibility.

Whether that dominance is sufficient to override the structural forces that have historically compressed post-IPO returns remains an open analytical question. No S-1 has been filed, no institutional analyst consensus exists, and the valuation premium already priced into the offering leaves limited margin for error. The market position is real. Whether the price adequately reflects it, or overshoots it, cannot yet be determined with the available information.

The SpaceX IPO is not the only path to space sector exposure. Several publicly traded companies with market capitalisations above $1 billion have delivered substantial returns over the past year, accessible through any standard brokerage account without IPO allocation requirements.

The SpaceX IPO has already begun reshaping how space-focused funds are structured and marketed globally, with BetaShares timing the launch of Australia’s first ASX space ETF (RCKT) directly to the June 2026 listing window, a move that illustrates how fund managers are positioning retail distribution around the IPO’s gravitational pull.

| Company | Ticker | One-Year Return |

|---|---|---|

| Planet Labs PBC | PL | ~1,062% |

| Viasat Inc | VSAT | ~652% |

| EchoStar Corp | SATS | ~520% |

| BlackSky Technology Inc | BKSY | ~427% |

| Rocket Lab Corp | RKLB | ~351% |

| Globalstar Inc | GSAT | ~308% |

| Intuitive Machines Inc | LUNR | ~271% |

Past performance does not guarantee future results. Data sourced from Finviz as of market close 20 April 2026. All companies listed have been publicly traded for at least one year with market capitalisations above $1 billion. Individual stock selection carries its own risk profile.

Investors who cannot or choose not to participate in the SpaceX IPO are not shut out of space sector growth. The returns above were available through standard brokerage accounts with no special allocation required.

The preceding sections build a picture with clear tensions: a historically significant deal, meaningful overvaluation concerns, restricted access channels, and a base rate showing two-thirds of IPOs underperform by year three. The question is what to do with that picture.

The absence of a public S-1 means any position taken before the filing is based on incomplete information. The most informed decision available right now is deciding what information would change the decision, and waiting for it.

For investors wanting to understand how pre-IPO valuation structures work in practice before the S-1 is filed, our deep-dive into the Findi pre-IPO investment process examines how cornerstone investor pricing, implied share price uplift, and structured timelines to a liquidity event operate across a real deal, providing a concrete reference point for the mechanics that will eventually govern SpaceX’s own offering.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

SpaceX’s operational dominance is real. Half the world’s orbital launches, $8 billion in EBITDA, and a competitive position that no rival can replicate in the near term. These are not the characteristics of a speculative pre-revenue listing.

They are also not a resolution to the pricing question. A 250x EBITDA multiple prices in a future that has not yet arrived, and the historical record shows that two-thirds of IPO investors would have been better served buying an index fund. Scale and quality are not synonyms. The readers who understand that distinction are better positioned than those who do not.

The S-1, once public, will be the document that changes everything retail investors currently cannot verify. Until then, the most rational posture is preparation without commitment.

The SpaceX IPO is the planned public listing of SpaceX shares on a stock exchange, targeting approximately $75 billion in fundraising at a valuation exceeding $2 trillion. A June 2026 roadshow is reported, with a dedicated retail investor event scheduled for 11 June 2026.

E*TRADE is the primary confirmed retail distribution channel for the SpaceX IPO, with Fidelity as a potential secondary participant. Investors wanting IPO-price access are advised to open an account with one of these brokerages before the June roadshow, as allocation is subject to eligibility criteria set by the brokerage.

Multiple analyst assessments, including a FutureSearch.ai report published 1 April 2026, characterised the IPO valuation as representing approximately 30% overpayment. A $2 trillion valuation applied to SpaceX's reported $8 billion in 2025 EBITDA implies a multiple of roughly 250x, which prices in decades of growth before public trading begins.

A Nasdaq analysis found that approximately two-thirds of IPOs from 2010 to 2020 were underperforming broader market benchmarks by their third year of public trading, suggesting that buying at debut does not statistically favour long-term outperformance.

Investors should monitor for the S-1 registration statement, which will disclose verified financials, share count, risk factors, and use of proceeds. Until that document is public, any investment decision is based on incomplete information, and the article recommends preparation without commitment.