Why AI Is Splitting Semiconductor Stocks From the Rest of Tech

49 mins ago

Bank of America has told clients the easy phase of the AI-driven rally is over. The warning, issued in a European equity strategy note in late June 2026, is not a vague caution about frothy sentiment. It is built on specific mechanics: pushback from corporate customers on what they will pay for AI tools, a competitive landscape that is eroding vendor pricing power, and risk premiums that have fallen to levels not seen for several decades.

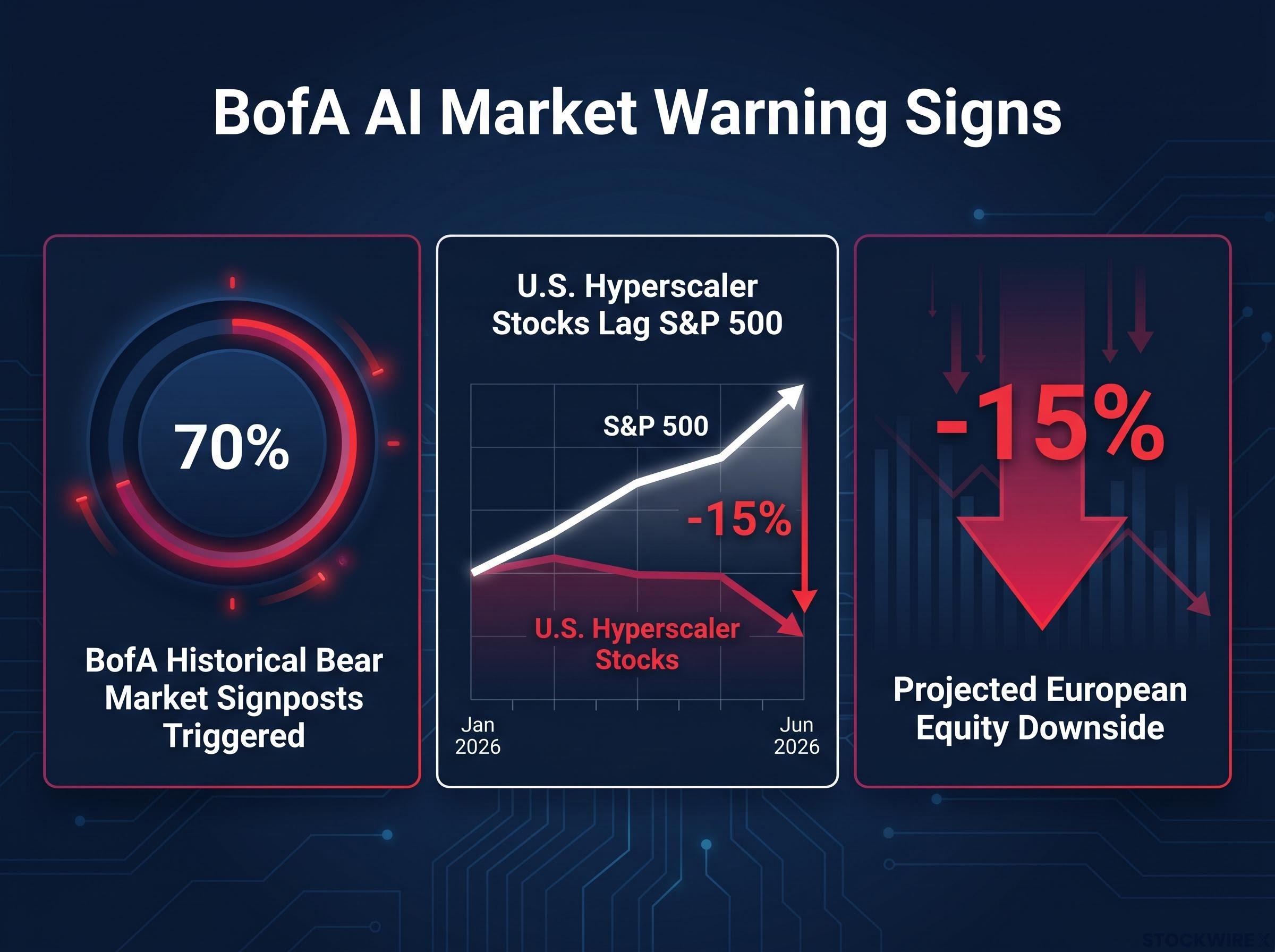

The timing matters. Since January 2026, U.S. hyperscaler stocks have trailed the S&P 500 by close to 15%. Approximately 70% of BofA’s historical bear market signpost indicators have now triggered. The repricing the bank warned about is not hypothetical; it is showing up in relative performance data that any investor can verify.

Here is a clear map of which parts of the AI trade carry the highest re-rating risk, which offer more defensible positioning, and what compressed risk premiums actually mean for portfolio downside from here. The distinction between AI sellers and AI users turns out to be the most consequential lens BofA offers, and it changes how you assess concentration risk in your own holdings.

BofA’s core argument is not that artificial intelligence fails as a technology. The argument is that equity markets priced AI-linked companies for a profit trajectory that real-world economics are now contradicting. Three conditions compounded to create the mismatch: AI infrastructure names priced for record profit margins, valuations stretched to peak multiples simultaneously, and risk premiums that have been pushed down to their lowest in several decades.

BofA’s European equity strategy note, late June 2026: Risk premiums across AI-linked equities have compressed to their lowest levels in multiple decades, leaving virtually no valuation cushion against earnings disappointment.

The equity risk premium is the mechanism through which compressed valuations translate into disproportionate downside: when the premium falls to historically low levels, even a modest earnings miss removes the buffer that would otherwise absorb the shock, producing share price declines larger than the fundamental miss alone would justify.

Roughly 70% of the bank’s historical bear market signposts have triggered. That indicator set includes elevated valuations, easy credit conditions, and extreme performance dispersion within the technology sector, conditions that historically precede market peaks rather than routine pullbacks. AI infrastructure providers, specifically chipmakers, data-centre operators, and capital goods suppliers, are described by BofA as trading at “all-time-high relative prices and peak earnings expectations.”

When stocks are priced for near-perfection, any deviation from the assumed path produces outsized losses. That means your AI-linked holdings carry more downside sensitivity right now than their recent price stability might suggest.

The pricing dilemma facing AI vendors operates as a structural trap, not a temporary headwind. BofA’s European equity strategy team notes that “doubts around the AI revolution are emerging,” driven primarily by end-user pricing resistance. Businesses are scaling back AI projects, trimming budgets, or capping consumption because the productivity improvements they can actually measure are not matching the ongoing costs vendors expect them to absorb.

This is not fringe behaviour. BofA’s analysts flagged the pattern as broad enough to warrant inclusion in a European equity strategy note, giving it systemic weight. Businesses are increasingly migrating toward open-source alternatives as a direct response to pricing pressure, reducing their dependency on proprietary platforms.

The two paths available to AI vendors are both margin-destructive:

BofA frames AI as a “double-edged sword” for corporate profits, capable of cannibalising existing revenue streams while simultaneously adding new cost lines. For investors holding AI software or platform names on the basis of pricing power, that active customer pushback is a direct challenge to the investment thesis, not background noise.

Commoditisation is the structural ceiling that makes recovery of pricing power unlikely, even if near-term pricing resistance eases. Lower-cost and open-source AI models are setting a worldwide baseline price for standard capabilities that proprietary vendors now have to compete against. Once that floor exists, proprietary vendors cannot charge software-like premiums for comparable functionality.

The dynamic parallels what happened in cloud computing. When a technology transitions from differentiated product to standardised infrastructure, margins compress toward commodity levels and do not recover. BofA explicitly warns that newer tools are weakening the hold vendors have over their customers and bringing greater transparency to what AI actually costs, handing corporate buyers durable bargaining leverage that will keep pricing under pressure for the foreseeable future.

Foundation model economics face a structural trap that the airline analogy captures precisely: massive capital intensity combined with interchangeable output means that even a technology succeeding at scale can deliver shareholder returns that are structurally capped, a conclusion BCA Research’s Peter Berezin formalised in a note published just days before BofA’s own European equity strategy warning.

| AI market phase | Pricing power | Vendor lock-in | Margin trajectory |

|---|---|---|---|

| Differentiated | Strong | High | Expanding |

| Transitional | Weakening | Eroding | Plateauing |

| Commoditised | Minimal | Low | Compressing |

If AI capabilities increasingly resemble generic infrastructure rather than differentiated software, the premium valuations attached to AI infrastructure providers are based on assumptions the competitive environment is actively dismantling. That is why BofA’s warning extends beyond any single earnings cycle.

The headline statistic is concrete and verifiable. According to BofA’s analysis published in late June 2026, U.S. hyperscaler stocks have fallen behind the S&P 500 by around 15% over the period from January 2026 to the time of writing.

BofA, January-June 2026: U.S. hyperscaler stocks have lagged the S&P 500 by approximately 15%, a gap the bank interprets as institutional investors beginning to reprice AI return expectations.

BofA does not read that underperformance as routine sector rotation. The bank frames it as the beginning of a valuation recalibration, with scepticism now visible in relative price action. Three technical signals reinforce that reading:

In Europe, BofA projects approximately 15% equity downside as AI-related repricing plays out. The hyperscaler lag is not just a U.S. phenomenon; it signals a global reassessment of what AI spending will actually return to shareholders. If BofA’s reading is correct, your exposure to AI-adjacent names carries more systematic risk than sector diversification alone addresses.

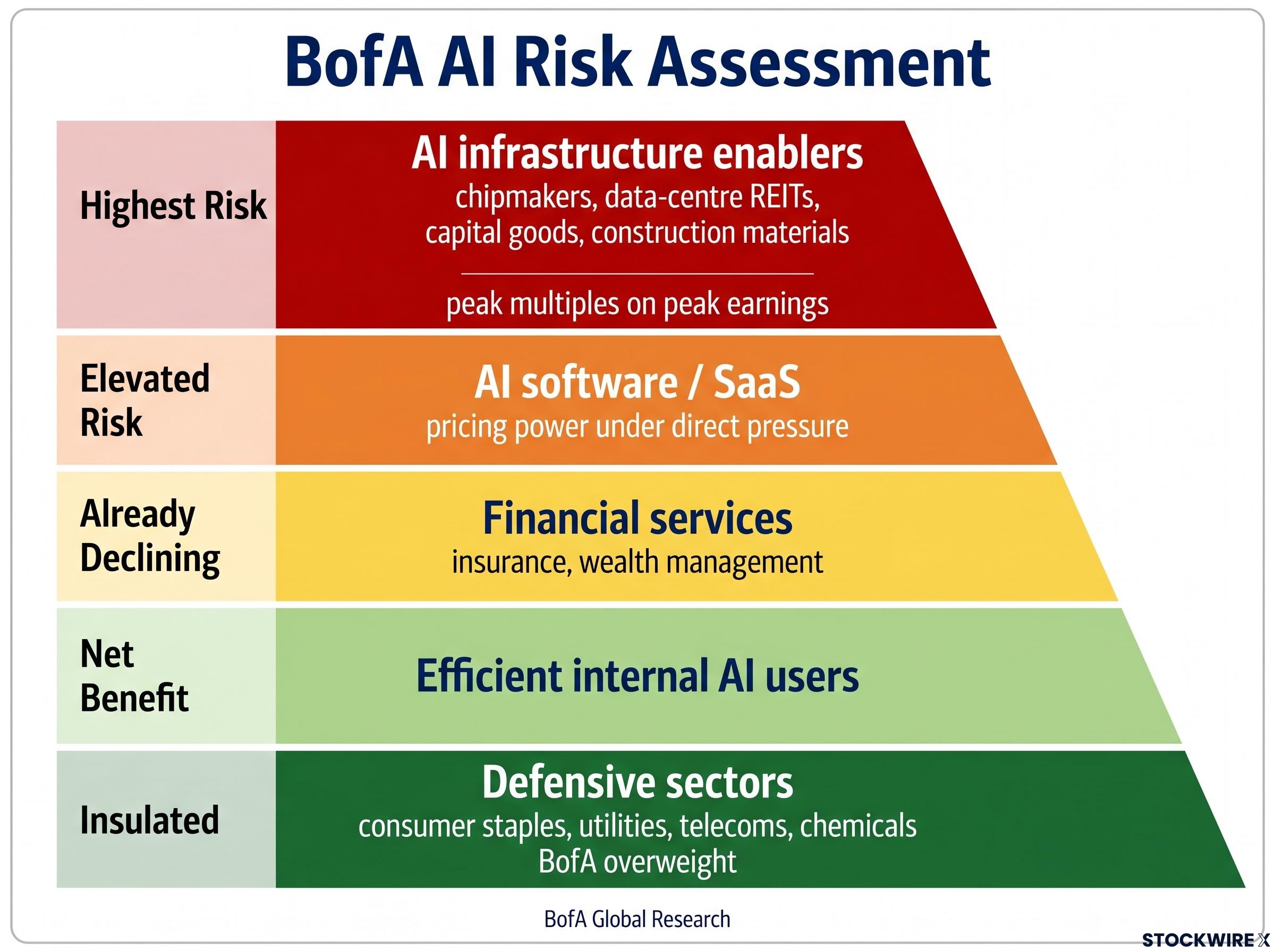

Not all AI exposure carries the same risk. BofA’s framework draws a clear distinction between categories, and the differences in re-rating vulnerability are substantial.

| Category | BofA risk assessment |

|---|---|

| AI infrastructure enablers | Highest risk: peak multiples on peak earnings |

| AI software / SaaS | Elevated risk: pricing power under direct pressure |

| Financial services facing cannibalisation | Already declining: insurance and wealth management hit |

| Efficient internal AI users | Net benefit without comparable valuation premium |

| Defensive sectors (BofA overweight) | Insulated: consumer staples, utilities, telecoms, chemicals |

The most exposed category is clear: chipmakers, data-centre REITs, capital goods, and construction materials suppliers that re-rated on peak capex narratives. These names sit at peak multiple and peak earnings expectations simultaneously, the most vulnerable position in a commoditisation scenario.

Peak-multiple valuations leave AI infrastructure stocks exposed to exactly the dynamic Arm Holdings demonstrated in May 2026: a clean earnings beat with raised guidance still produced an 8% share price fall when one disclosure, a supply gap covering only half of its $2 billion AGI CPU demand, introduced execution risk at a 121x forward price-to-earnings multiple.

Secondary exposure sits in software and financial services segments where AI may cannibalise existing fee-based and labour-based revenue models. BofA flags insurance and wealth management as areas already experiencing declines.

BofA’s “AI hiding places” include consumer staples, utilities, telecoms, and chemicals, sectors where the bank remains overweight. The bank also distinguishes between “AI sellers” (high valuation risk) and “efficient AI users” (companies deploying AI internally for productivity gains without depending on selling AI as their core product). That second category may benefit from AI without carrying comparable valuation exposure. For your portfolio, “AI exposure” is not a single risk category: infrastructure names face pressure from the top, application names face cannibalisation from below, and defensive names offer insulation that currently looks underpriced.

These four steps follow directly from the mechanisms BofA has identified. Each connects to a specific risk the bank has flagged.

BofA strategists, mid-2026: “The easy part of the rally is over.” The bank advises investors to take profits and play more defence.

The macro ripple-effect risk adds urgency. A cooling AI capex boom could weigh on data-centre and semiconductor demand chains, extending the repricing beyond equity indices into adjacent sectors.

BofA’s own framing is worth taking at face value: this is a recalibration story, not a collapse call. The bank is not arguing AI has no long-term value. It is arguing that near-term economics and valuations are misaligned, and that the gap between what markets priced and what companies can actually charge is now wide enough to produce meaningful downside.

Three interconnected mechanisms drive that gap. Corporate buyers are resisting AI price points, weighing on top-line growth for vendors. The spread of open-source alternatives is placing a structural ceiling on what proprietary providers can charge. Meanwhile, risk premiums have been compressed so tightly that even a modest earnings shortfall can trigger disproportionate share price falls. Together, these form a single coherent thesis: AI economics overshot what companies could realistically deliver, and markets are beginning to price in that reality.

Tail risk hedging becomes a more precise tool when risk premiums are compressed to the degree BofA describes: institutional demand for SPX collar structures and long-dated puts has risen alongside the multiple expansion that characterises the AI infrastructure trade, reflecting a gap between consensus forecasts and the fat-tailed outcomes embedded in derivative positioning.

The variables to watch from here are specific: whether AI monetisation evidence improves over the next two to three reporting cycles, whether open-source migration accelerates or plateaus, and whether risk premiums begin to normalise. The question is not whether to hold AI exposure but how to hold it, and BofA’s framework gives you a more precise vocabulary for making that assessment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The equity risk premium is the extra return investors demand for holding stocks over risk-free assets, and when it falls to historically low levels, even a small earnings miss can trigger share price drops far larger than the fundamental shortfall alone would justify. BofA warns that AI-linked equities have compressed risk premiums to their lowest in multiple decades, removing the valuation buffer that would normally absorb bad news.

BofA's June 2026 European equity strategy note flagged that roughly 70% of its historical bear market signpost indicators had triggered, U.S. hyperscaler stocks had lagged the S&P 500 by around 15% since January 2026, and corporate customers were actively resisting AI pricing, creating a gap between what markets priced and what vendors could realistically deliver.

BofA identifies AI infrastructure enablers, specifically chipmakers, data-centre operators, and capital goods suppliers, as the most exposed, because they sit at peak multiples and peak earnings expectations simultaneously. AI software and SaaS names face elevated risk from direct pricing pressure, while financial services firms in insurance and wealth management are already experiencing AI-driven revenue cannibalisation.

BofA remains overweight consumer staples, utilities, telecoms, and chemicals, framing these as insulated from the AI repricing dynamic while currently appearing underpriced relative to high-multiple AI infrastructure names.

AI sellers are companies whose core business depends on selling AI products or infrastructure, and they carry high valuation risk as pricing power erodes. Efficient AI users are companies deploying AI internally to cut costs and boost productivity without relying on AI as a revenue source, meaning they can capture AI benefits without the same re-rating downside.