Barclays Warns of Prolonged Market Volatility Under New Fed Reality

Jun 27, 2026

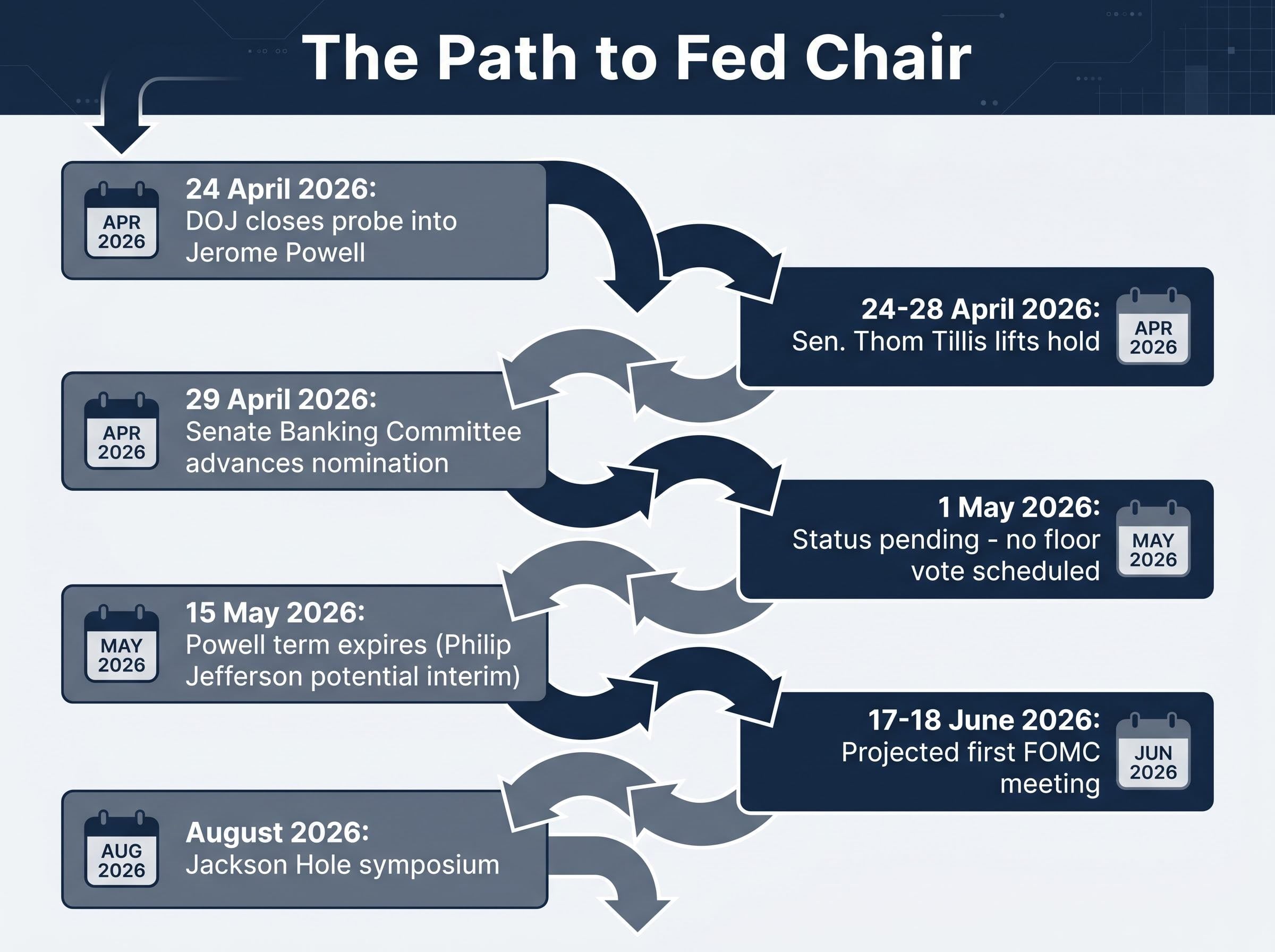

The Senate Banking Committee advanced Kevin Warsh’s nomination to chair the Federal Reserve on 29 April 2026, voting along strict party lines to send the appointment to the full Senate floor. The vote arrived five days after the Department of Justice closed its criminal probe into Jerome Powell on 24 April, removing the last procedural obstacle that had stalled the confirmation process for weeks. With Powell’s chair term set to expire on 15 May 2026, the window for a clean transition is narrow. If the full Senate does not act before that date, Vice Chair Philip Jefferson would assume the role on an interim basis, introducing a layer of institutional uncertainty during an already sensitive policy period. What follows covers the procedural chain that brought the nomination to this point, what actual market data reveals about investor sentiment, who Warsh is and what he has proposed, and why a new Fed chair does not automatically translate into lower interest rates.

The confirmation process moved in a tight sequence, with each step unlocking the next. Understanding the chain matters because a single delay at any point could have pushed the timeline past Powell’s 15 May departure.

No floor vote date has been publicly announced. If the Senate does not confirm Warsh before 15 May, Vice Chair Philip Jefferson would step in as acting chair. A Jefferson interim period, even a brief one, would add an open variable to an already complex policy environment, though it would not alter the Federal Open Market Committee’s (FOMC) rate-setting authority or near-term meeting calendar.

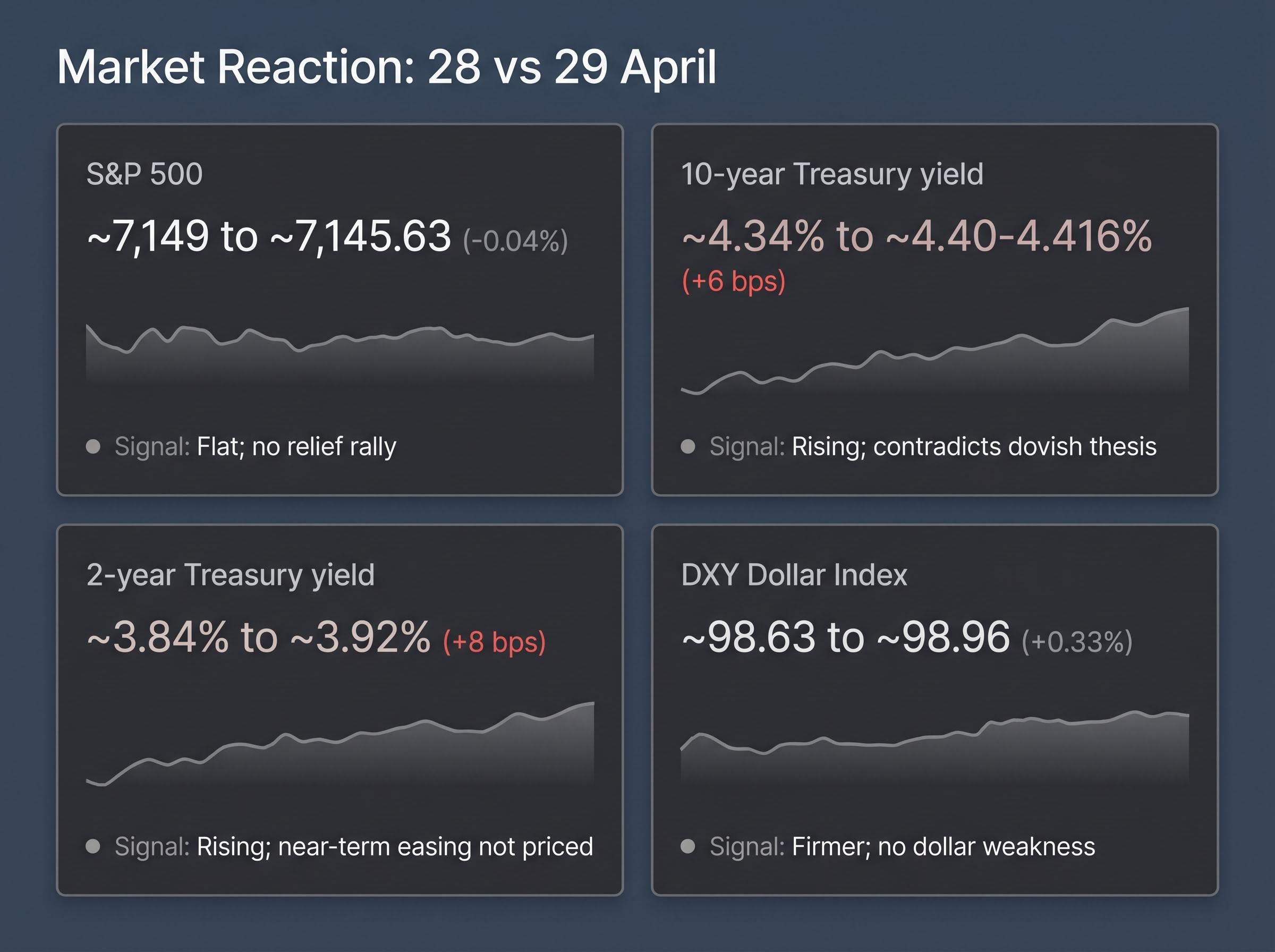

The committee vote landed on 29 April. If markets had interpreted the confirmation’s advance as a signal of imminent rate cuts, the data would show equity gains, falling yields, and a weaker dollar. It showed none of those things.

| Asset | 28 April level | 29 April level | Change | Signal |

|---|---|---|---|---|

| S&P 500 | ~7,149 | ~7,145.63 | -0.04% | Flat; no relief rally |

| 10-year Treasury yield | ~4.34% | ~4.40-4.416% | +6 bps | Rising; contradicts dovish thesis |

| 2-year Treasury yield | ~3.84% | ~3.92% | +8 bps | Rising; near-term easing not priced |

| DXY Dollar Index | ~98.63 | ~98.96 | +0.33% | Firmer; no dollar weakness |

The S&P 500 closed roughly flat. Treasury yields rose across the curve. The dollar strengthened modestly. Taken together, the market’s response to the committee vote was neutral to slightly hawkish, not the dovish-relief trade some commentators had anticipated.

The same session that recorded these moves also saw investors navigate the convergence of a Fed hold and big tech earnings, with mega-cap technology companies reporting capital expenditure commitments that introduced their own set of rate-sensitivity questions into a single trading day.

CME FedWatch data as of late April assigned approximately 99% probability of no rate change at the 17-18 June FOMC meeting, with only roughly 1% probability of a cut. For full-year 2026, approximately 56.5% probability was assigned to zero cuts.

For investors positioning around a Warsh-driven easing rally, this data provides a corrective. Markets are not treating the confirmation as a catalyst for near-term rate cuts, and trades built on that assumption carry meaningful risk.

Warsh served on the Federal Reserve Board from 2006 to 2011, a tenure that placed him at the centre of the global financial crisis. During that period, he built a reputation as a relatively hawkish voice on the board, frequently expressing scepticism about the scale and duration of emergency monetary interventions.

His 2026 confirmation hearings told a somewhat different story. Warsh signalled a more accommodative posture on interest rates than his earlier record suggested, though he declined to pre-commit to specific policy moves or a timeline for cuts. He affirmed the Fed’s independence from political interference and disclosed ethics divestitures of approximately $100 million in assets.

The structural reforms he proposed attracted as much attention as his rate posture:

The dot plot currently functions as the Fed’s most direct form of forward guidance on rates. Bond traders and equity strategists use it to calibrate expectations for the path of monetary policy over the following 12-18 months. Removing it would force markets to rely more heavily on post-meeting statements and economic data alone, increasing uncertainty around rate expectations. For rate-sensitive positioning in bonds, equities, and currency markets, less forward guidance means wider ranges of possible outcomes, and potentially higher volatility around FOMC meetings.

FRBSF research on dot plot disagreement, published in August 2023, found that the chart’s informational value for market participants derives precisely from the dispersion of individual member projections, meaning its elimination would remove a signal that bond and equity markets have come to treat as a primary anchor for rate path expectations.

The Jackson Hole symposium in August 2026 would represent Warsh’s first major public platform as chair, offering the earliest opportunity to signal whether these reforms are aspirational or imminent.

A common assumption runs that a more accommodative chair equals lower rates. The FOMC’s structure complicates that assumption considerably.

The committee has 12 voting members at any given time. Warsh would hold one vote, the same as any other member. His appointment effectively replaces Stephen Miran, who is departing in May 2026, substituting one Trump-aligned voice for another rather than shifting the committee’s ideological centre of gravity.

The FOMC structure and voting membership, as defined by the Federal Reserve Board, confirms that the committee consists of twelve voting members at any given time, with the chair holding a single vote equal in weight to every other member on the committee.

Several constraints limit the scope for near-term easing:

The data dependency constraint carries extra weight given the current macro environment; geopolitical pressure on Fed rates from Middle East energy disruptions has added roughly one percentage point to inflation readings, narrowing the conditions under which any chair, regardless of personal policy preference, could justify an easing move.

Analysts at Edward Jones have indicated they anticipate one or two cuts later in 2026, representing one of the more optimistic sell-side positions.

Even that relatively constructive view places cuts in the second half of the year at earliest. Warsh’s projected first FOMC meeting as chair would be 17-18 June 2026, and the probability data leaves almost no room for a cut at that gathering.

The rate story has absorbed most of the attention around Warsh’s nomination. The balance sheet story may matter more.

Warsh has argued consistently that the Fed’s ownership of Treasury securities blurs the boundary between monetary and fiscal policy. During his prior tenure from 2006 to 2011, the balance sheet was considerably smaller. His philosophical position holds that a leaner balance sheet creates room for rate cuts without the risk of over-stimulating the economy, a framework that treats balance sheet reduction and rate easing as complementary rather than contradictory.

Warsh’s balance sheet philosophy assumes a relatively stable inflation environment in which reducing asset holdings can coexist with rate easing; the supply-side inflation mechanics driving crude above $100 per barrel complicate that framework directly, since a leaner balance sheet paired with stubborn energy-driven CPI produces a narrower policy corridor than his prior tenure offered.

If Warsh moves to accelerate balance sheet reduction, the most acute near-term consequence would be a rapid steepening of the yield curve, pushing long-term borrowing costs higher independent of any FOMC rate decision.

That steepening would carry direct implications for bond investors and anyone with exposure to rate-sensitive sectors including housing and technology, where valuations are tightly linked to long-term discount rates. Reserve adequacy concerns could also emerge if the pace of reduction outstrips the banking system’s comfort level.

Institutional constraints would likely slow any aggressive move. The Fed’s internal consensus-building process, including working groups and formal studies, acts as a brake on rapid policy shifts. The December reintroduction of a short-term Treasury purchase mechanism underscored the complexity of managing the balance sheet even under stable leadership.

One additional variable remains unresolved. Powell’s board term runs through January 2028, meaning he could retain his seat as a voting FOMC member even after vacating the chair. No public statements from Powell have clarified his intentions. Markets are expected to treat resolution of this question as a marginal positive: one fewer open variable in an already crowded uncertainty landscape. His vote, however, would remain one of 12, limiting its individual influence on outcomes.

Three threads run through the Warsh confirmation story. Procedurally, the nomination is near-complete, with only a full Senate floor vote remaining before the 15 May deadline. The market data shows investor restraint rather than optimism; yields rose, equities were flat, and rate cut probabilities remain negligible for June. The real policy uncertainty lies not in the fed funds rate headline but in balance sheet decisions and structural communication reforms that could reshape how the Fed signals its intentions.

The Jackson Hole symposium in August 2026 will offer the first substantive window into what a Warsh-led Fed looks and sounds like. Until then, the variables remain open: the floor vote timing, the balance sheet trajectory, the fate of the dot plot, and Powell’s board seat decision. Investors positioning for a new chapter in monetary policy would be well served by monitoring each of these individually rather than treating the confirmation as a single, resolved event.

For investors building scenarios around the second half of 2026, our deep-dive into how the oil surge has rewired rate expectations examines Morningstar’s three fixed income scenarios, the simultaneous repricing across the Fed, ECB, and Bank of England, and what the duration of the Strait of Hormuz disruption means for bond portfolio positioning.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Kevin Warsh is President Trump's nominee to replace Jerome Powell as Federal Reserve chair. He previously served on the Federal Reserve Board from 2006 to 2011, where he was known as a relatively hawkish voice during the global financial crisis.

Not necessarily. Warsh holds only one of 12 votes on the FOMC, and CME FedWatch data as of late April assigned roughly 56.5% probability to zero cuts for the full year 2026, with a 99% probability of no change at the June meeting.

If the full Senate does not vote before Powell's chair term expires on 15 May 2026, Vice Chair Philip Jefferson would assume the role on an interim basis, adding a layer of institutional uncertainty to the policy environment.

Warsh has proposed eliminating the dot plot, reducing the frequency of post-meeting press conferences, lowering the Fed's public profile, and refocusing policy attention on the balance sheet alongside the fed funds rate.

Markets responded with restraint: the S&P 500 closed nearly flat, the 10-year Treasury yield rose approximately 6 basis points, the 2-year yield rose around 8 basis points, and the dollar strengthened modestly, a neutral to slightly hawkish reaction rather than a dovish relief rally.