Early 2026 began with Wall Street pricing in a steady glide path for Fed interest rates to fall, but that optimism has collided with a central bank now frozen by international conflict. Analysts previously mapped a straightforward trajectory for monetary easing based on cooling domestic metrics. By late April 2026, escalating geopolitical tensions in the Middle East have severely disrupted those economic projections.

This analysis traces how overseas instability directly dictates the trajectory of central bank policy. Financial markets are recalibrating their expectations as policymakers react to forces entirely outside their domestic jurisdiction.

Understanding this transmission mechanism is critical for market participants. The ongoing foreign policy developments translate global supply shocks into sustained borrowing costs, a dynamic that is fundamentally altering the landscape for US consumer spending.

The Federal Reserve’s Immediate Policy Constraint

The US central bank opted to maintain its benchmark borrowing range during its Wednesday afternoon announcement. This was not a routine policy hold for policymakers heading into their mid-year gatherings. It represents a forced delay driven entirely by unpredictable international inflation variables.

Policymakers must now adjust their public communication regarding consumer prices. The local economic strength that typically dictates policy has been sidelined by global events.

Policy Communication Pivot “The calculus for near-term monetary easing has been suspended, with international conflict establishing a new baseline for energy-driven price pressures that supersede domestic economic data.”

Financial authorities recognise that lowering borrowing costs while energy markets spike risks reigniting the exact inflation cycle they spent two years suppressing. This reality leaves the central bank effectively trapped by external forces. Their personal borrowing costs are currently dictated more by global events than local economic strength.

The Federal Reserve’s interest rate trajectory remains anchored in a restrictive monetary pattern as policymakers attempt to balance slowing domestic demand against these external energy shocks.

When big ASX news breaks, our subscribers know first

The Transmission Mechanism of Global Conflict to Domestic Inflation

Targeted financial restrictions against major energy producers restrict global supply, which immediately elevates crude oil baseline prices. Sustained elevated energy costs subsequently bleed into the core inflation metrics that financial authorities monitor to set policy.

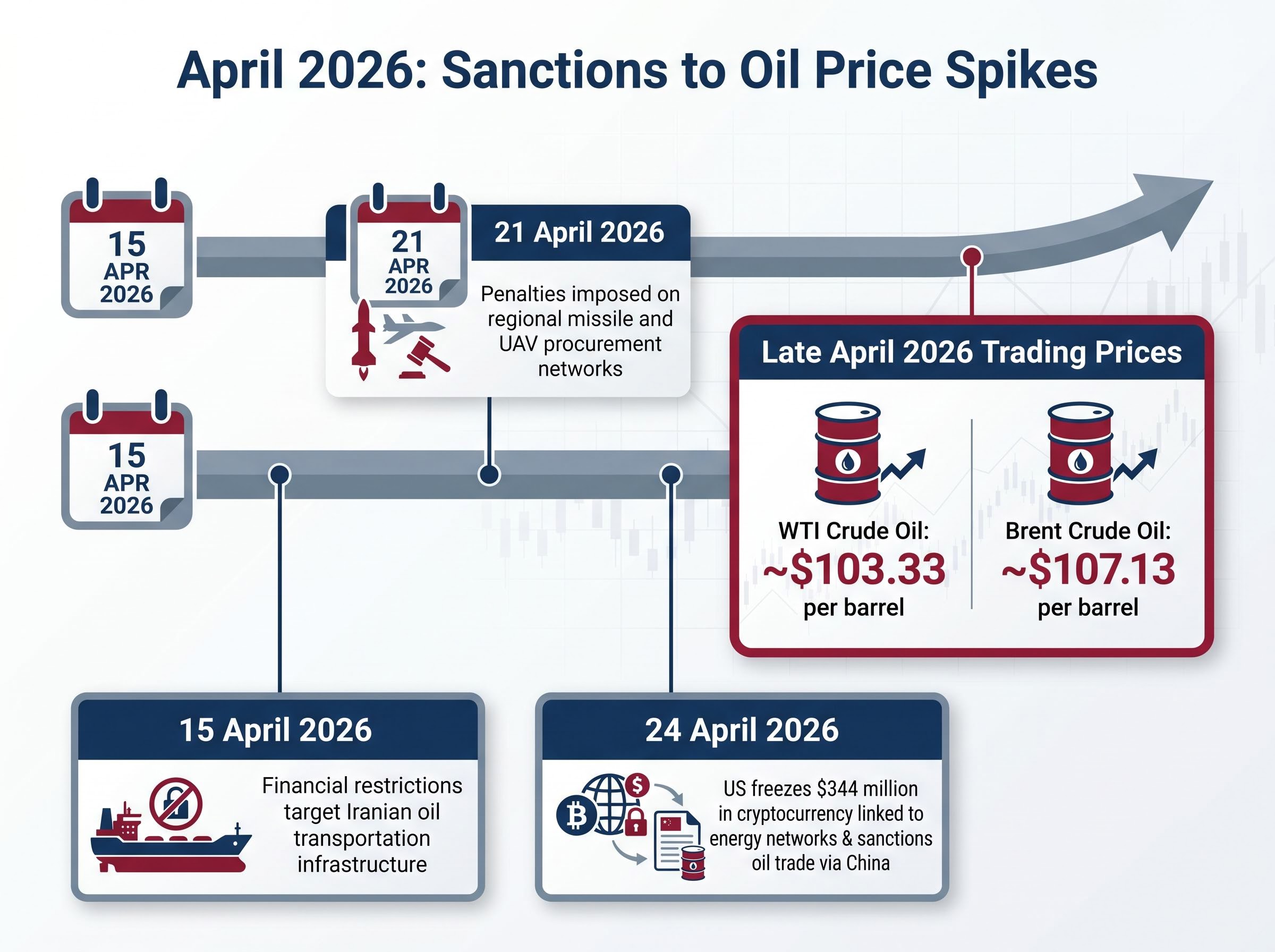

The aggressive US sanctions timeline deployed throughout April 2026 connects directly to the current pricing pressures observed in global energy markets.

- 15 April 2026: Financial restrictions target Iranian oil transportation infrastructure, disrupting shadow fleet operations.

- 21 April 2026: Authorities impose new penalties on regional missile and UAV procurement networks.

- 24 April 2026: The US freezes $344 million in cryptocurrency linked to energy networks and sanctions oil trade operating via China.

These Treasury Department enforcement actions actively target the financial infrastructure supporting illicit petroleum networks, attempting to choke off capital flows before they further destabilise broader energy markets.

These geopolitical interventions immediately registered in commodity trading pits.

| Crude Oil Benchmark | Late April 2026 Trading Price |

|---|---|

| WTI Crude Oil | ~$103.33 per barrel |

| Brent Crude Oil | ~$107.13 per barrel |

The Ripple Effect on Core Consumer Prices

A distinct lag time exists between crude oil spikes and broader retail price increases. Manufacturers and logistics providers initially absorb the shock of higher fuel costs before passing them onto consumers at local storefronts.

Central banks are particularly sensitive to these energy-driven inflation cycles. Transportation costs inevitably become embedded in the price of everyday goods, converting a temporary foreign policy shock into structural domestic inflation.

Immediate Casualties in Corporate Travel and Aviation

The combination of regional instability and surging fuel costs is aggressively compressing margins across the global travel sector. Aviation companies are feeling the most acute, immediate pain from crude oil trading above $100 per barrel.

According to industry reports, JetBlue recently withdrew its annual financial guidance, explicitly citing fluctuating aviation fuel expenses as a source of deep market uncertainty. The withdrawal of annual guidance by major carriers operates as a signal of fundamental operational instability. Airlines cannot confidently hedge their fuel exposure when the geopolitical landscape shifts weekly.

This JetBlue financial guidance suspension highlights how quickly operational visibility deteriorates when carriers face structural energy shocks that exceed their near-term hedging capacities.

The Accommodation Sector Headwinds

Diminished flight availability and rising ticket prices compound the headwinds facing online reservation platforms. Corporate executives have warned that prolonged regional instability is beginning to depress global travel enthusiasm.

This has manifested in tangible financial metrics. According to market estimates, Booking Holdings reported an approximate 2 percentage point decline in first-quarter accommodation occupancy expansion. Investors tracking these metrics can identify which industries are most vulnerable to the current geopolitical climate before allocating capital.

The Consumer Spending Shift to Value Retail

The US consumer environment is currently defined by a sharp dichotomy between top-line spending resilience and an underlying flight to affordability. Overall transaction volumes remain exceptionally high, but the destination of those retail dollars is shifting rapidly.

Continuous digital payment transition currently masks the underlying household budget strain caused by elevated borrowing costs. Processing networks confirm this sustained spending activity across their platforms.

| Digital Payment Network | Q2 2026 Transaction Volume Growth |

|---|---|

| American Express | increase |

| Visa | increase |

Despite these strong transaction volumes, value-oriented retailers possess a distinct operational advantage. Restricted consumer purchasing capacity forces shoppers to prioritise discounted goods at the expense of premium brands. Broad macroeconomic pressure pushes capital towards established discount entities like Costco and TJX Companies, creating potential safe havens in retail equities.

Investors exploring how this retail trend impacts corporate earnings will find our comprehensive walkthrough of the consumer recovery dichotomy, which outlines how affluent spenders are temporarily masking the significant financial strain faced by lower-income households.

Recalibrating Timeline Expectations for Borrowing Costs

Financial market forecasting instruments have adapted rapidly to the reality of sustained geopolitical tension. Early expectations for policy easing have evaporated, forcing analysts to realign timelines for future central bank relief.

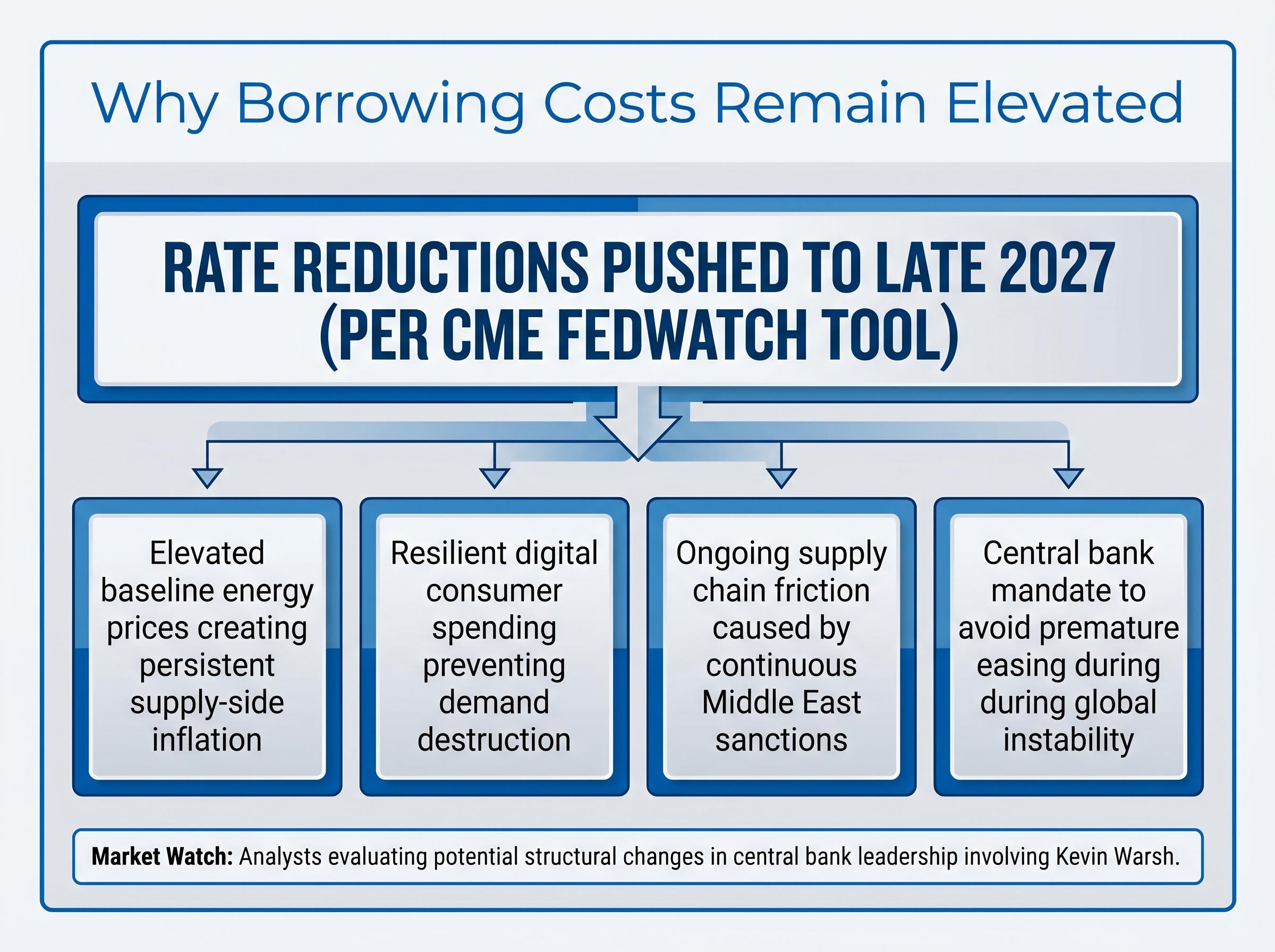

According to market estimates, the CME FedWatch Tool indications now push anticipated borrowing cost reductions deep into the final months of 2027. This extended timeline forces a fundamental recalculation for both corporate debt issuance and household mortgage planning.

This fundamental recalculation exposes algorithmic trading models that struggle to incorporate qualitative geopolitical risks, leaving equity markets vulnerable to sharp repricing if energy shocks become entrenched.

Market analysts are also evaluating potential structural changes within the central bank leadership, including a potential transition involving Kevin Warsh. These administrative adjustments will not have an immediate impact on the current high-rate trajectory.

Several primary factors are keeping rates elevated through 2027: Elevated baseline energy prices creating persistent supply-side inflation. Resilient digital consumer spending that prevents demand destruction. Ongoing supply chain friction caused by continuous Middle East sanctions. A central bank mandate to avoid premature easing during global instability.

The Market Reality of Sustained Tension

A direct line connects overseas conflict to domestic corporate struggles and shifting US consumer habits. The central bank’s policy constraints remain firmly tied to energy sector outcomes, leaving policymakers with little room to manoeuvre until global supply risks abate.

Navigating this prolonged high-rate environment will require continuous resilience from US consumers and businesses alike. Financial projections regarding future rate cuts are entirely subject to market conditions and unpredictable geopolitical risk factors.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and forward-looking statements are speculative and subject to change based on market developments.