US Inflation Hits 4.2% but Core Data Tell a Calmer Story

11 hrs ago

On 14 May 2026, two developments landed simultaneously that investors in AI infrastructure had been waiting months to see. Cisco announced a $1 billion restructuring explicitly tied to AI networking, and the U.S. government cleared roughly 10 Chinese firms to purchase Nvidia’s H200 chip. Cisco surged more than 20% in a single session. Nvidia climbed more than 5%. Together, these moves signal that the AI infrastructure buildout is entering an accelerated phase, one where both the hardware layer and the networking layer are seeing corporate strategy and institutional capital converge around the same thesis on the same day. What follows covers what each development means, how analysts are framing the stock moves, which geopolitical risks the market is discounting, and which other AI infrastructure names are rising in sympathy.

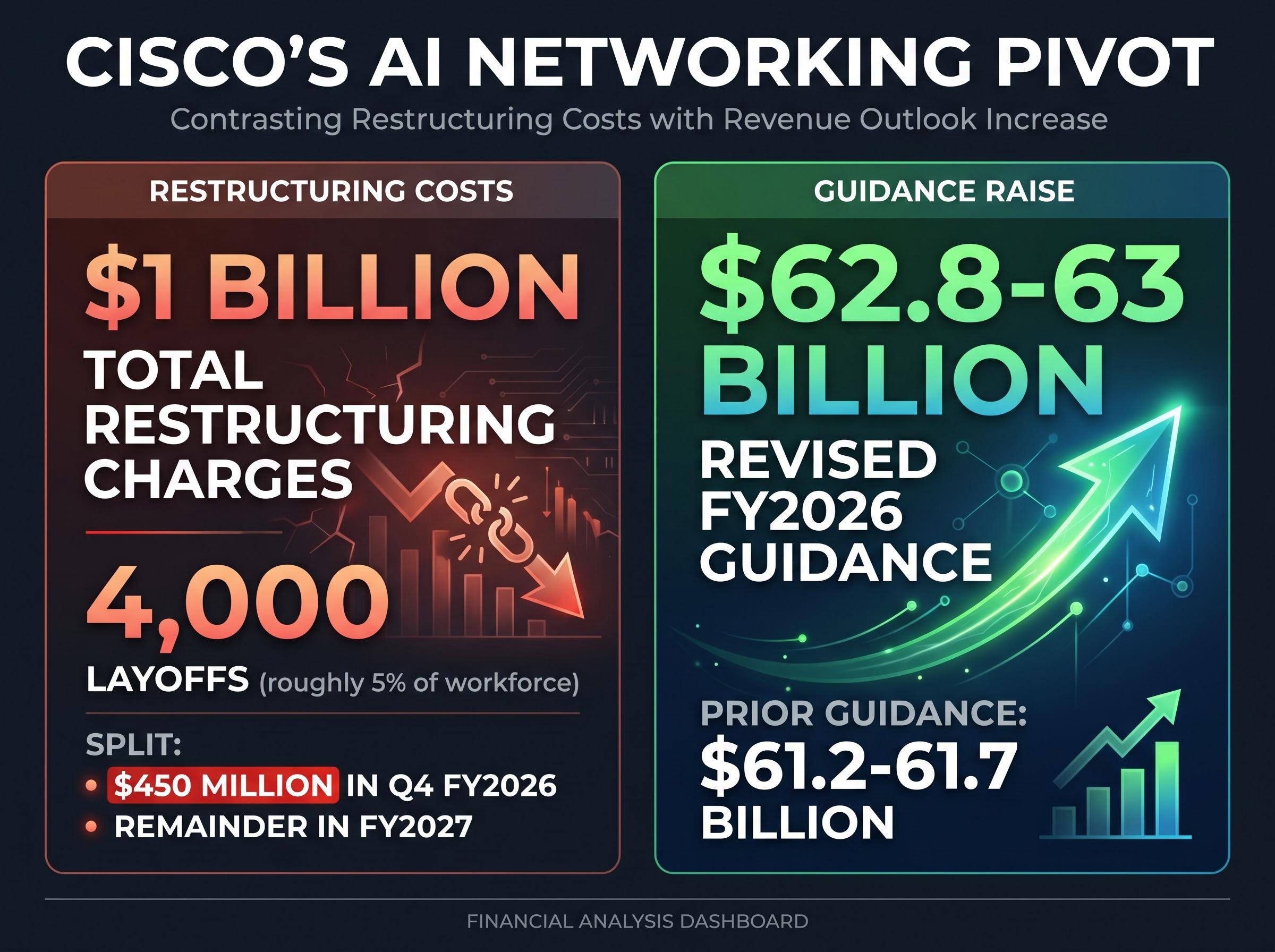

The numbers arrived first. Cisco disclosed $1 billion in total restructuring charges, approximately 4,000 layoffs representing roughly 5% of its workforce, with charges split between $450 million in Q4 FY2026 and the remainder in FY2027. CEO Chuck Robbins framed the move as strategic reallocation toward AI networking rather than conventional cost-cutting. Revised FY2026 revenue guidance rose to $62.8-63 billion, up from a prior range of $61.2-61.7 billion.

The stock responded before the framing did. Cisco opened at $54.20, up 18.5% from its 13 May close of $45.75, on volume of 45 million shares. By 10:00 AM UTC, shares reached $55.40, with a pre-market peak of $56.10.

Analyst upgrades arrived in quick succession:

Morgan Stanley characterised the restructuring as an “AI pivot accelerator,” projecting 20%-plus networking growth funded by the $1 billion in charges.

The guidance raise, not the restructuring itself, is the cleaner signal. The order book and revenue outlook are what the market is rewarding. Whether the restructuring represents genuine strategic transformation or a rebranded layoff cycle remains contested.

Deutsche Bank’s Sherri Scribner held her price target at $58, questioning whether the move constitutes “AI transformation vs. cost-cutting” and noting the 4,000 layoffs mirror 2024 cuts. Evercore ISI’s Amit Daryanani set his target at $57, flagging the 50% cash component of restructuring charges as execution risk. Stifel described the move as “repackaging a 5% headcount trim as strategy.”

JPMorgan dismissed these sceptical takes as “short-term noise,” emphasising Cisco’s AI order surge as the thesis that matters.

Approximately 10 Chinese firms received clearance to purchase Nvidia’s H200 chip, including Alibaba, Baidu, Tencent, ByteDance, and Huawei (under a restricted volume designation). As of 14 May, no deliveries had been completed. First shipments are anticipated for June 2026.

Nvidia opened at $142.50, up 3.2% from the prior close. By 10:00 AM UTC, shares traded at $145.20, a 5.1% intraday gain, after an 8% after-hours surge on 13 May. The intraday high reached $146.80.

The deal emerged in part from Jensen Huang’s presence on the Trump administration’s diplomatic trip to China. The revenue math, however, is what separates sentiment from substance.

Jensen Huang’s role in the Trump delegation was interpreted by markets the day before as a direct signal that U.S. chip export restrictions were under active bilateral discussion, with the Shanghai Composite closing at its highest level since July 2015 on that anticipation alone.

| Analyst Firm | Price Target | FY2026 Revenue Impact | FY2027 Revenue Impact |

|---|---|---|---|

| JPMorgan | $165 | Less than 1% of $120B+ guidance | $2-3B contribution |

| Goldman Sachs | Not revised | Negligible ($500M max) | Bolsters growth to 40%+ |

| Piper Sandler | Not revised | Minimal | $1.5B annualised by mid-2027 |

JPMorgan’s Harlan Sur characterised the clearance as signalling “U.S.-China AI detente,” while estimating near-term FY2026 revenue impact at less than 1% of guidance.

The stock’s 5% intraday gain prices in the long-term thesis, not the near-term revenue. Investors should understand that gap before sizing a position based on this news alone.

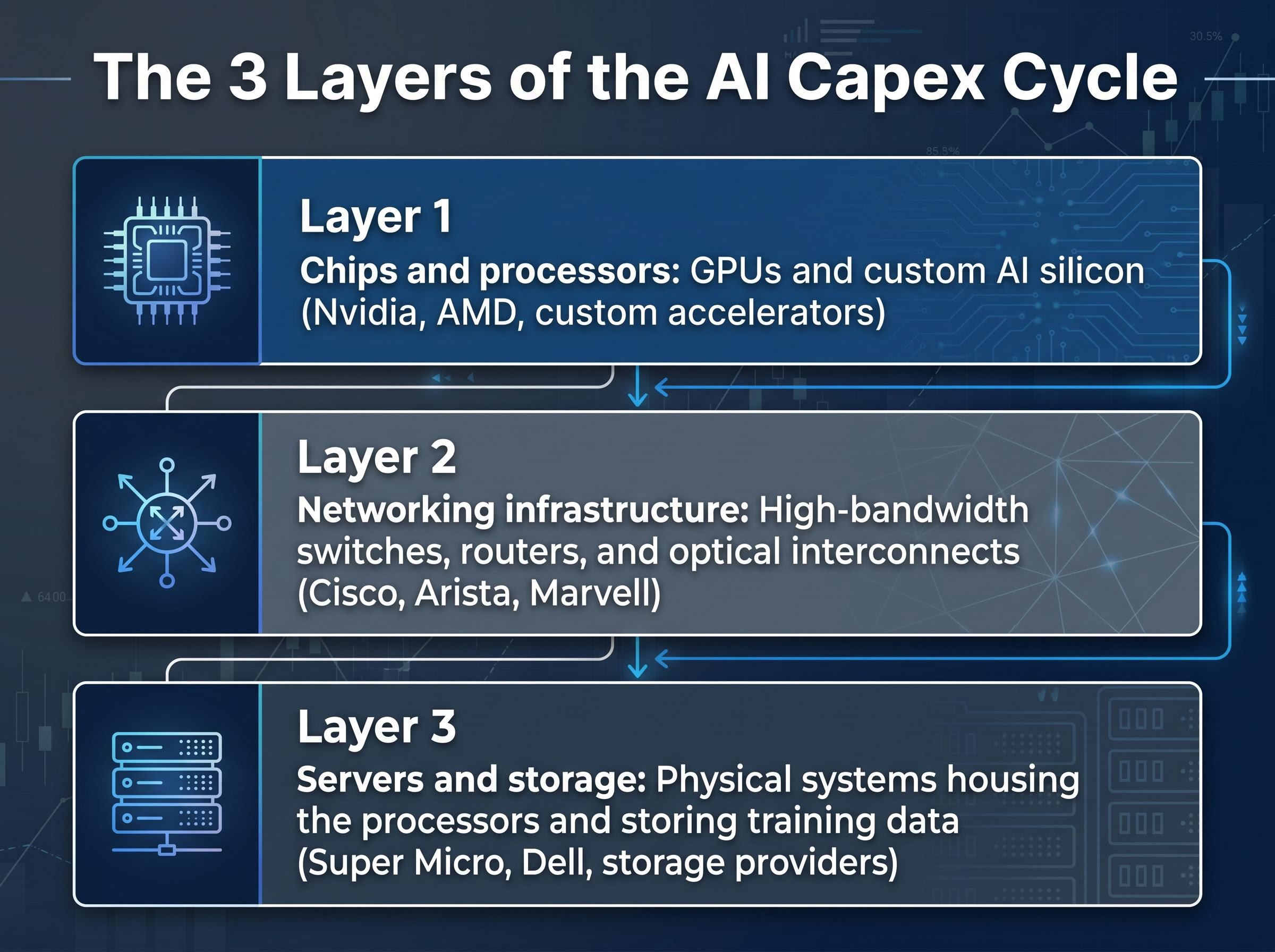

AI model training and inference require more than processors. Thousands of GPUs must communicate with each other at high bandwidth and low latency, and that communication layer, the networking fabric, is where Cisco operates. When a hyperscaler orders GPUs, it must also build or upgrade the networking infrastructure connecting them, creating a cascading demand cycle.

The AI capex cycle, a term investors will encounter frequently in analyst notes, flows through three layers:

Cisco’s FY2026 guidance raise to $62.8-63 billion is a real-world confirmation that networking orders are arriving alongside chip demand. That is why the restructuring is being treated as a sector signal rather than an isolated corporate event.

Hyperscaler capex commitments reached approximately $130 billion in Q1 2026 alone, with full-year guidance across Amazon, Microsoft, Alphabet, and Meta converging around $725 billion, a spending rate that creates the sustained order flow into networking and chip supply chains that both Cisco’s guidance raise and Nvidia’s China expansion are positioned to capture.

The gains on 14 May were concentrated in infrastructure names, not spread across technology broadly. Bloomberg characterised the collective move as an “AI infrastructure re-rating,” and the pattern had a clear logic: the market was rewarding the entire hardware stack, from chips to networking to servers.

| Ticker | Company | May 14 Move | New Price Target | Analyst Firm |

|---|---|---|---|---|

| ANET | Arista Networks | +6.2% to $385.40 | $420 | Wedbush |

| MRVL | Marvell Technology | +5.8% to $82.10 | $95 | Piper Sandler |

| AVGO | Broadcom | +4.1% to $1,850 | $2,000 | Goldman Sachs |

| SMCI | Super Micro Computer | +7.5% to $1,120 | $1,300 | Rosenblatt |

Bloomberg described the session as an “AI infrastructure re-rating,” with gains expanding from pure-play AI names into semiconductors and networking.

Vital Knowledge noted that software and services companies did not participate in the rally. The equal-weighted S&P 500 underperformed the cap-weighted version, confirming that gains were concentrated, not broad-based. For investors deciding where to add exposure, that distinction matters: this was a hardware-layer story, not a generalised AI rally.

The market priced in delivery. Whether delivery actually occurs on schedule is a different question.

Congressional pushback emerged within hours of the announcement from three distinct sources:

Senator Rubio characterised the H200 clearance as an “export loophole,” the sharpest expression of Congressional opposition as of 14 May.

Deal details themselves remain unsettled. Reuters cited approximately 10 firms including Huawei under a restricted volume designation. Investing.com listed only 8 firms, omitting Huawei entirely. No deliveries have been completed. First shipments are anticipated for June 2026, meaning the regulatory environment has time to shift before the deal becomes commercially irreversible.

The Trump administration framed the clearance as a “diplomatic win.” Whether Congressional pressure triggers a CFIUS review or delays shipments past June 2026 remains an open question, one that directly affects the FY2027 revenue estimates underpinning Nvidia’s current stock move.

Summit-level AI security talks are structurally unlikely to produce binding policy changes on chip export controls because those controls are governed by agency rulemaking and executive orders rather than diplomatic communiques, a distinction that matters when Congressional actors retain the authority to trigger CFIUS reviews independently of any White House framing.

Two storylines converged on 14 May: Cisco’s restructuring validated that the networking layer of the AI capex cycle is generating real revenue, and the Nvidia H200 clearance opened a potential demand expansion into China. Both are priced on expectations, not delivered results.

For the current price moves to hold, two conditions need to remain true:

Gains were concentrated in AI infrastructure names, not broad technology. That concentration signals a thesis-specific move, not market euphoria. Investors who understand what the thesis requires will be better positioned to evaluate whether it holds as Q4 FY2026 results and June shipment data arrive.

AI investment cycle concentration risks are now a live consideration for portfolio managers: Magnificent Seven names represent approximately 33.7% of S&P 500 market cap, and the gains on sessions like May 14 further compress the already-narrow base of stocks driving index performance, raising the question of whether the infrastructure thesis is a stock-picker’s opportunity or a systemic exposure that broad index holders are accumulating without choosing to.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including analyst price targets and revenue projections, are subject to change based on market developments and company performance.

AI infrastructure stocks are companies that supply the hardware layer powering artificial intelligence, including chips and processors (Nvidia), networking equipment (Cisco, Arista), and servers (Super Micro). They matter because every major AI model training or inference workload requires this physical stack, making these companies direct beneficiaries of hyperscaler capital spending.

Cisco disclosed $1 billion in restructuring charges tied to a strategic reallocation toward AI networking, alongside a guidance raise to $62.8-63 billion for FY2026. Analysts at Morgan Stanley and Barclays raised price targets, with the guidance increase, rather than the layoffs, treated as the primary bullish signal by the market.

Approximately 10 Chinese firms received clearance, including Alibaba, Baidu, Tencent, ByteDance, and Huawei (under a restricted volume designation), though no deliveries had been completed as of 14 May 2026 and first shipments were anticipated for June 2026.

Congressional pushback emerged quickly, with Senator Rubio calling the deal an export loophole and demanding a CFIUS review, while the House China Committee vowed oversight hearings. Because no deliveries had occurred as of 14 May, the regulatory environment retains time to shift before the deal becomes commercially irreversible.

The market re-rated the entire AI hardware stack, not just individual companies, because Cisco's guidance raise confirmed that networking orders are arriving alongside chip demand, creating a cascading signal across interconnected supply chain names including Arista Networks (up 6.2%), Super Micro Computer (up 7.5%), Marvell Technology (up 5.8%), and Broadcom (up 4.1%).