How to Filter Australia’s 70 Fixed Interest ETFs to a Short List

3 hrs ago

One company has owned a supermarket chain, a hardware giant, a coal mine, a pharmacy network, and an explosives manufacturer. Each time, it has either transformed the asset or walked away at a profit. Wesfarmers (ASX: WES) has risen 5.81% year-to-date in 2026, sustaining its reputation as one of the ASX’s most reliable blue-chip names. Yet the question investors rarely ask is why a conglomerate spanning hardware, chemicals, pharmacies, and loyalty data consistently outperforms simpler businesses. The answer lies in the Wesfarmers business model itself, not in any single brand. What follows is an analysis of the structural logic behind how Wesfarmers acquires, builds, and exits businesses, what distinguishes this approach from ordinary conglomerate accumulation, and what the pattern reveals about long-term value creation on the ASX.

Wesfarmers generated A$45.7 billion in revenue during FY2025 and employed approximately 118,000 people across a portfolio that stretches from warehouse hardware to lithium extraction. The scale is remarkable. The logic behind it is more so.

Wesfarmers’ stated primary objective: Delivering satisfactory returns to shareholders through financial discipline and strong management of a diversified portfolio of businesses.

That objective is not a mission statement pinned to a lobby wall. It functions as a capital allocation philosophy that governs every division through three discrete stages:

Each division holds its own strategy and performance accountability under a decentralised management structure. The willingness to exit, rather than accumulate indefinitely, is the model’s most unusual feature and its most value-creating one.

Markets tend to punish conglomerates. The “conglomerate discount” describes the market’s tendency to value a collection of unrelated businesses below the sum of their individual parts, because investors perceive the capital allocation as opaque or self-serving. When a holding company owns unrelated assets and lets them drift without performance accountability, the discount widens.

Wesfarmers explicitly counters this by holding each business to measurable hurdles:

Return on capital is the primary performance hurdle Wesfarmers applies across its divisions, and each business must demonstrate acceptable returns relative to the capital deployed or risk becoming a restructuring candidate; this discipline sits at the heart of why the group’s diversification has historically added value rather than diluted it.

Capital is recycled from mature or underperforming assets into opportunities with stronger long-term prospects. The company operates across retail, health, chemicals, fertilisers, energy, industrial and safety, and data and loyalty, yet each segment must justify its place.

Active portfolio management is only as good as the quality of each decision, and not every Wesfarmers bet has succeeded on its original schedule. The UK Bunnings expansion stands as the highest-profile example: an attempt to export the warehouse hardware format outside its home market that ultimately required withdrawal when the model’s assumptions did not translate to a different competitive and consumer environment.

More recently, Catch.com.au ceased standalone trading on 30 April 2025, a wind-down that reflected the difficulty of scaling an online marketplace within a conglomerate retail framework. Coregas was disposed of in June 2025. Both represent portfolio corrections, evidence that the model demands ongoing adjustment rather than one-time discipline at the point of acquisition.

The Bunnings story is not a lucky retail bet. It is an accumulation of deliberate structural advantages built across nearly four decades.

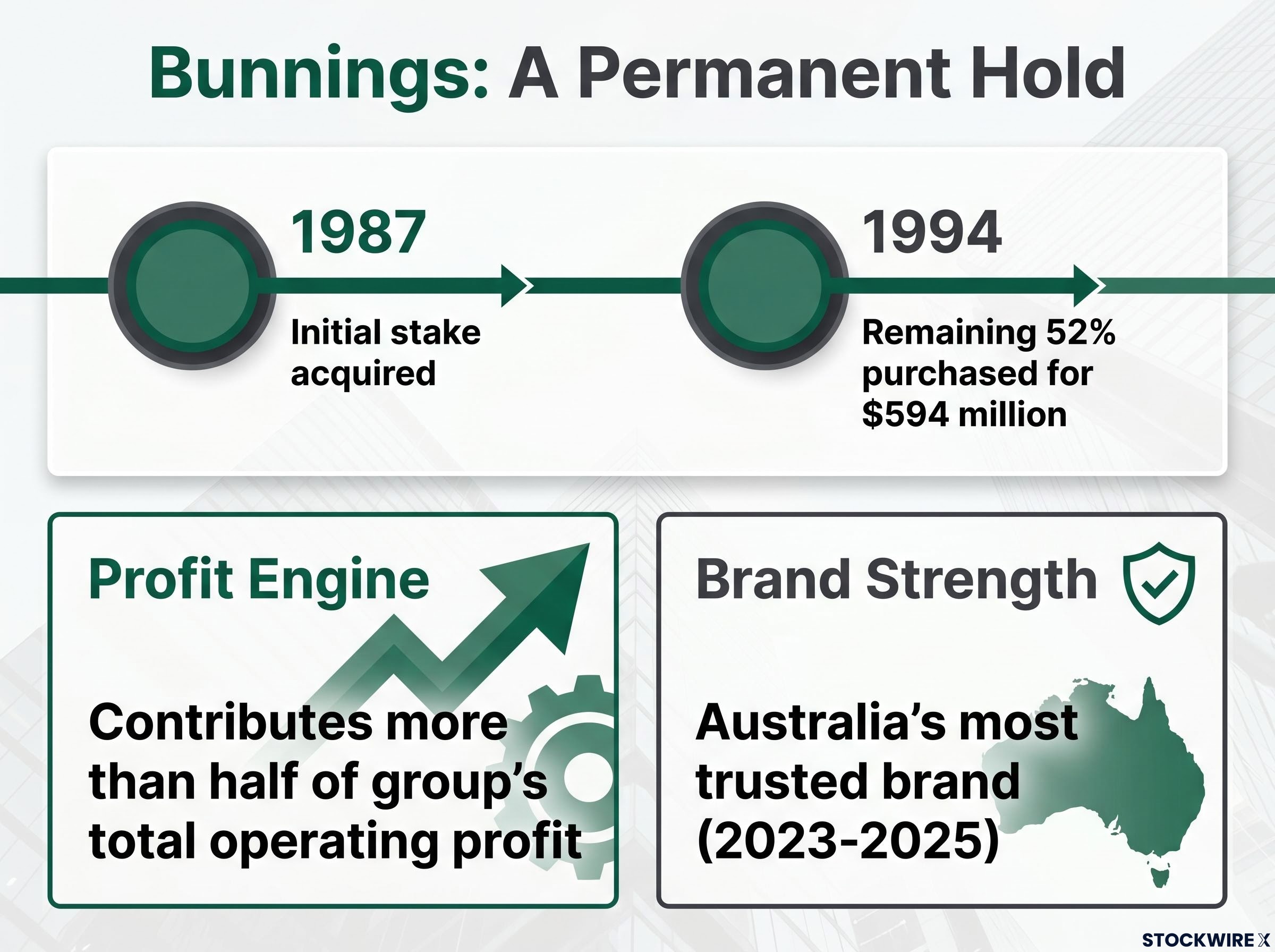

Wesfarmers first invested in Bunnings in 1987. Seven years later, in 1994, it purchased the remaining 52% stake for $594 million, committing to a multi-decade ownership horizon that few listed companies would tolerate. From that base, Wesfarmers developed Bunnings into a national warehouse-format home improvement chain, building scale and network effects through an extensive store footprint and product range.

| Milestone | Year and Detail |

|---|---|

| First investment | 1987: Initial stake acquired |

| Full acquisition | 1994: Remaining 52% purchased for $594 million |

| Most trusted brand | 2023-2025: Held Australia’s most trusted brand distinction across multiple quarterly rankings |

Today, Bunnings contributes more than half of the group’s total operating profit. It is the reason Wesfarmers has chosen not to exercise the divest stage of its own model for this asset: when a business reaches structural dominance, the rational capital allocation decision is to keep compounding, not exit.

Intrinsic value estimation for a conglomerate like Wesfarmers is complicated by the terminal value problem: when a business like Bunnings represents more than half of group profit and is explicitly classified as a permanent hold, the discount rate and perpetuity assumptions embedded in any DCF model carry outsized weight on the final output, and small changes in those inputs can shift the implied fair value by billions.

Australia’s most trusted brand during 2023 and 2024, sustained into 2025. That brand strength is not a marketing achievement alone; it functions as a proxy for the depth of competitive moat that underpins Bunnings’ durable cash generation.

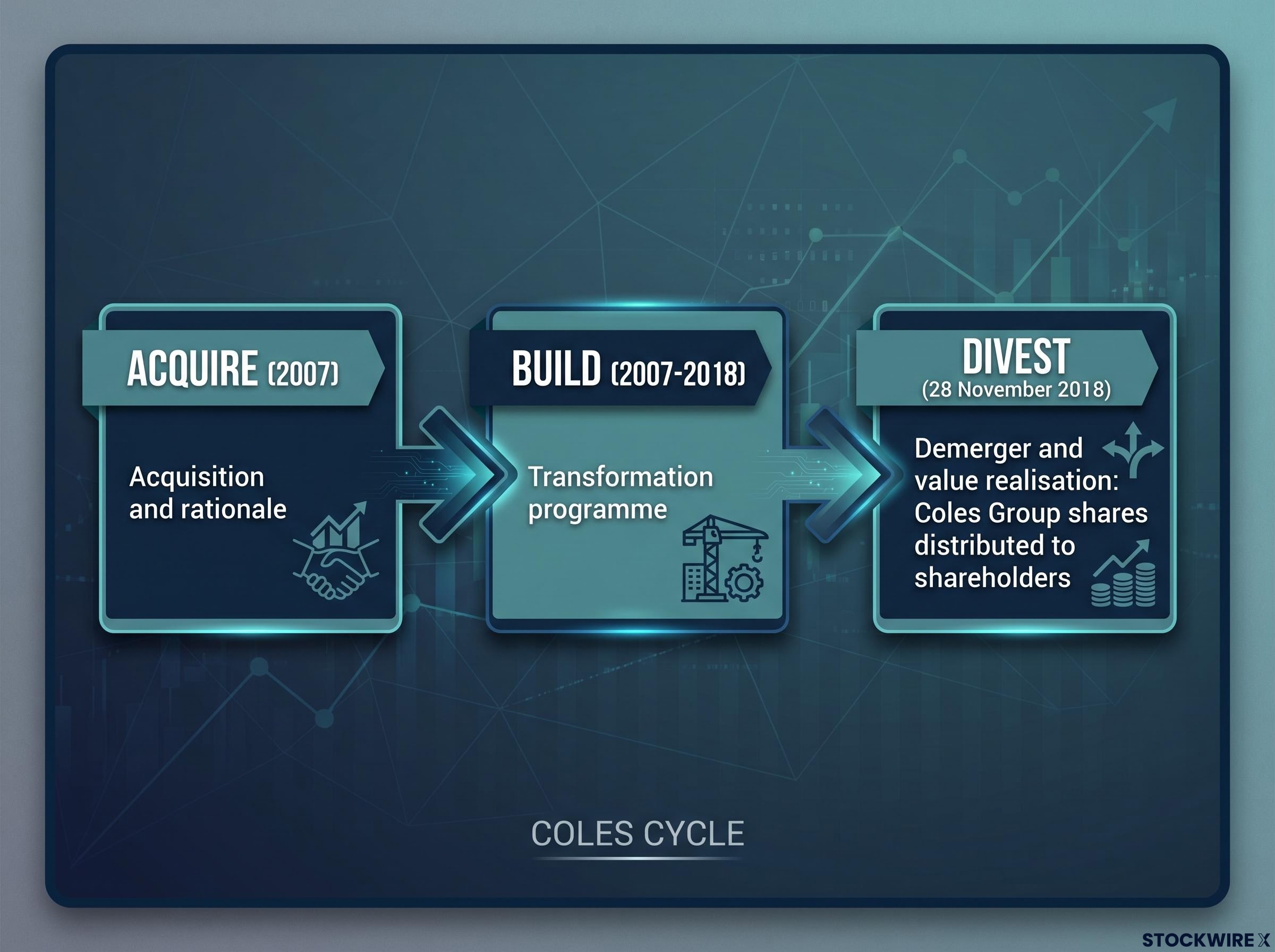

On 28 November 2018, Wesfarmers distributed Coles Group shares to its own shareholders, completing one of the largest corporate demergers in Australian history. The exit was not a retreat. It was the model’s most sophisticated expression.

The demerger structure Wesfarmers used to exit Coles sits within a defined regulatory framework: ASX Guidance Note 24 on acquisition and disposal of assets sets out the listing rule requirements that govern how ASX-listed companies must handle significant transactions, including demerger and spin-out events, ensuring shareholder approval and disclosure standards are met.

The arc began in 2007, when Wesfarmers acquired Coles Group in one of Australia’s largest corporate transactions. What followed was more than a decade of operational turnaround: store refurbishment, pricing reform, supply chain upgrades, and a sustained focus on customer experience.

The three phases of the Coles cycle illustrate the full acquire-build-divest logic in a single asset:

The exit criterion: Wesfarmers exits when the incremental value it can add by retaining an asset falls below the value shareholders could realise by owning it separately. In the Coles case, standalone listing was judged to create more value than continued conglomerate ownership.

The Coles cycle is the clearest proof that the divest stage is not a failure signal. It is a disciplined value realisation event, and it reframes how investors should interpret any future Wesfarmers exit.

The current Wesfarmers portfolio is not a static collection. It is a map of where each business sits within the acquire-build-hold cycle, and where the next decisions are most likely to emerge.

| Division | Key Brands | Current Model Stage | Strategic Note |

|---|---|---|---|

| Bunnings | Bunnings Warehouse | Hold | Core cash engine; more than half of group profit |

| Kmart Group | Kmart, Target | Build / Hold | Value retail positioned in mid-market segments |

| Officeworks | Officeworks | Hold | Stable position in office, education, and technology retail |

| Health | API, Priceline Pharmacy | Build | Strategic demographic bet with longer value realisation timeline |

| WesCEF | Chemicals, fertilisers, Covalent Lithium (50%) | Build | Industrial inputs plus long-cycle energy transition exposure |

| Industrial and Safety | Blackwoods, Workwear Group | Hold | Distribution network serving mining and industrial customers |

| Digital and Data | OnePass, flybuys (50% stake) | Build | Data and loyalty layer connecting retail ecosystem |

The WES share price gain of 5.81% year-to-date through 13 June 2026 suggests the market is currently pricing in continued execution rather than questioning the model. Wesfarmers operates over 1,900 retail stores across its brands, a scale footprint that reflects the cumulative output of decades of build-phase investment.

The Covalent Lithium joint venture (50% stake within WesCEF) represents a long-cycle bet on energy transition demand that is distinct in nature from Wesfarmers’ typical retail acquisition logic. The build phase for a lithium project is measured in years, not quarters, and the exit optionality is far less clear than it was for a mature supermarket chain.

The health segment (Australian Pharmaceutical Industries, Priceline Pharmacy and associated banners) and OneDigital (OnePass subscription and 50% stake in flybuys) represent structural diversification into demographic and digital tailwinds. These are early-stage builds with longer value realisation timelines, and the model’s discipline will be tested by the patience they require.

The Wesfarmers case study carries lessons that extend beyond a single ASX constituent. Four investment principles emerge from the pattern:

Capital allocation discipline, the ability to deploy retained earnings into opportunities earning above the cost of capital and to exit when returns deteriorate, is precisely what distinguishes genuine value creators from businesses that generate revenue growth while destroying shareholder wealth; the four screening metrics that identify this discipline, including free cash flow yield and debt-to-equity ratios, give investors a way to verify the claim rather than accept it on faith.

The distinction between Wesfarmers and a private equity fund is worth noting. Wesfarmers holds businesses operationally through their build phase rather than flipping on short cycles, which is what makes the returns sustainable rather than episodic. As a constituent of the S&P/ASX 200 with a long record of dividends supported by cash-generative retail businesses, Wesfarmers has earned its blue-chip status through execution, not inertia.

The model is only as durable as the discipline of the people running it. The framework itself is replicable; the management quality required to execute it consistently across decades is not.

Wesfarmers’ 5.81% year-to-date gain in 2026 is a market signal that the acquire-build-divest model continues to command investor confidence. That confidence is built on decades of consistent capital allocation discipline, not on any single transaction.

As Wesfarmers deepens its bets on lithium, health, and data, the question is whether the same portfolio discipline that worked in retail and industrials translates to sectors where the build phase is measured in decades and the exit optionality is far less clear.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Anyone considering WES shares should review Wesfarmers’ latest financial reports and consult a licensed financial adviser.

For readers who want to apply the principles in this article to their own portfolio decisions, our dedicated guide to evaluating ASX shares walks through a six-step checklist covering business quality, key financial metrics including EPS and P/E ratios, position sizing, and stop-loss discipline, providing a structured starting point before committing capital.

The Wesfarmers business model follows a three-stage acquire-build-divest cycle: the company buys businesses with strong underlying demand, improves their operations and earnings over time, and exits or demerges them when it can no longer add incremental value, recycling capital into higher-return opportunities.

Wesfarmers exits a business when the incremental value it can add by retaining the asset falls below the value shareholders could realise by owning it separately, as demonstrated by the 2018 Coles demerger where a standalone listing was judged to create more value than continued conglomerate ownership.

Bunnings contributes more than half of Wesfarmers' total group operating profit and holds Australia's most trusted brand distinction across multiple rankings, meaning the rational capital allocation decision is to keep compounding returns rather than exit an asset that has reached structural market dominance.

Wesfarmers is building positions in lithium through the Covalent Lithium joint venture (50% stake), in health through Australian Pharmaceutical Industries and Priceline Pharmacy, and in data and loyalty through the OnePass subscription platform and a 50% stake in flybuys, all of which represent longer build-phase timelines than its traditional retail businesses.

Wesfarmers counters the conglomerate discount by holding each division to measurable performance hurdles, including return on capital and cash generation targets, and by actively recycling capital away from underperforming or mature assets rather than allowing businesses to accumulate without accountability.