Tokenized Repo Could Pull $250B From the Fed’s Balance Sheet

3 hrs ago

The first face-to-face meeting between Donald Trump and Xi Jinping in over six months is underway in Beijing, and markets have already moved on anticipation alone. The Nasdaq climbed approximately 1.1%, the Shanghai Composite touched its strongest level since July 2015, and cyclicals pushed higher in pre-market trading. But summit optimism has a habit of outrunning summit outcomes.

With trade, artificial intelligence security, and the Iran conflict all on the agenda simultaneously, investors face the challenge of separating the durable from the performative before positions are set. The three agenda items carry very different probability distributions, and the market’s current bullish tilt is averaging across all of them as though each is directionally positive.

This analysis maps each of the three major areas against what analysts say is actually achievable, providing a calibrated investment framework rather than a reactive read of the market tape.

The opening session produced warm optics and a rally that began before the principals sat down. The market tone snapshot as of 13 May 2026:

Those numbers reflect a market pricing directional progress across all three agenda items. Preliminary readouts have referenced a “Phase One-lite” trade framework preview, but no tariff reductions have been confirmed. No official White House or Xinhua post-opening communiqués have been issued as of Day 1.

Fidelity International has flagged “low expectations for comprehensive agreement,” a framing that sits uncomfortably alongside the breadth of the equity rally.

The gap between market pricing and analyst expectation is the analytical tension that structures everything that follows. Markets are pricing in optimism. Analysts are pricing in process.

The broader context for how markets process geopolitical shocks helps explain the gap between the current rally and analyst caution: markets treat events as probability-adjusted inputs to future earnings rather than proportional headline shocks, which is why equity benchmarks can rise even as analysts flag low expectations for comprehensive agreement.

A joint statement previewed a “Phase One-lite” framework under which China would increase purchases of U.S. agricultural and energy products by $50 billion annually. This is the most tangible item to emerge from Day 1.

The framework is achievable precisely because it requires no legislative change on either side. Purchase commitments can be directed through state-owned enterprises in China and facilitated through existing export channels in the United States. If confirmed, U.S. agribusiness equities and liquefied natural gas exporters would be the most direct beneficiaries.

Ed Yardeni of Yardeni Research has flagged S&P 500 upside potential if agricultural and energy deals materialise, though he cautioned that midterm election politics could distort outcomes. His upside view should be treated as directional rather than a confirmed target.

Existing tariffs on Chinese goods remain intact. No tariff reduction language has appeared in any preliminary readout.

The two distinct types of potential trade outcomes should not be conflated:

The structural tariff reform constraints limiting this summit extend beyond the negotiating table: two federal courts struck down the broadest statutory pillars of US executive tariff authority in the three months prior, meaning that even if political will existed for phased reductions, the legal architecture for unilateral executive action has been significantly narrowed.

Heritage Foundation analysis highlights U.S. demands for curbs on Chinese investment in U.S. technology. Council on Foreign Relations (CFR) analysis suggests China holds the upper hand on technology and AI leverage in the broader negotiating context. Together, these framings indicate the structural trade relationship is not meaningfully changing at this summit.

The AI security dialogue is the agenda item most likely to generate headlines and least likely to generate substance. The competitive stakes that underpin the U.S.-China AI race make genuine concessions irrational for both sides.

Jonas Goltermann of Capital Economics summarised the analyst consensus: “Trade wins likely, but no AI thaw.”

An unconfirmed Financial Times report flagged a potential “memorandum on AI standards,” but analysts have treated it with scepticism rather than as a policy signal. CSIS confirmed no AI-specific concessions have emerged, and expectations remain low.

The specific policy non-events ground the scepticism in concrete absences rather than opinion:

Nvidia stock sat at approximately $220, up roughly 0.61% on 12 May. Julian Emanuel of BTIG sees the SMH ETF gaining 2-3% short-term on the Huang optics, but notes that export controls cap broader semiconductor upside. Bloomberg strategists have characterised Nvidia-linked gains as “overdone.”

Semiconductor investors need to distinguish between a short-term optics-driven move and a structural shift in export policy. The export control architecture remains the binding constraint regardless of summit atmosphere.

The Federal Register licensing rules for semiconductor exports to China, administered by the Bureau of Industry and Security, shifted H20 and equivalent chips from a presumption of denial to a case-by-case review framework, a regulatory architecture that summit communiqués cannot override without a separate rulemaking process.

The scepticism around AI cooperation is not a judgment on this particular summit. It reflects a structural dynamic that will recur at every future bilateral meeting, and investors who recognise the pattern can avoid over-rotating each time.

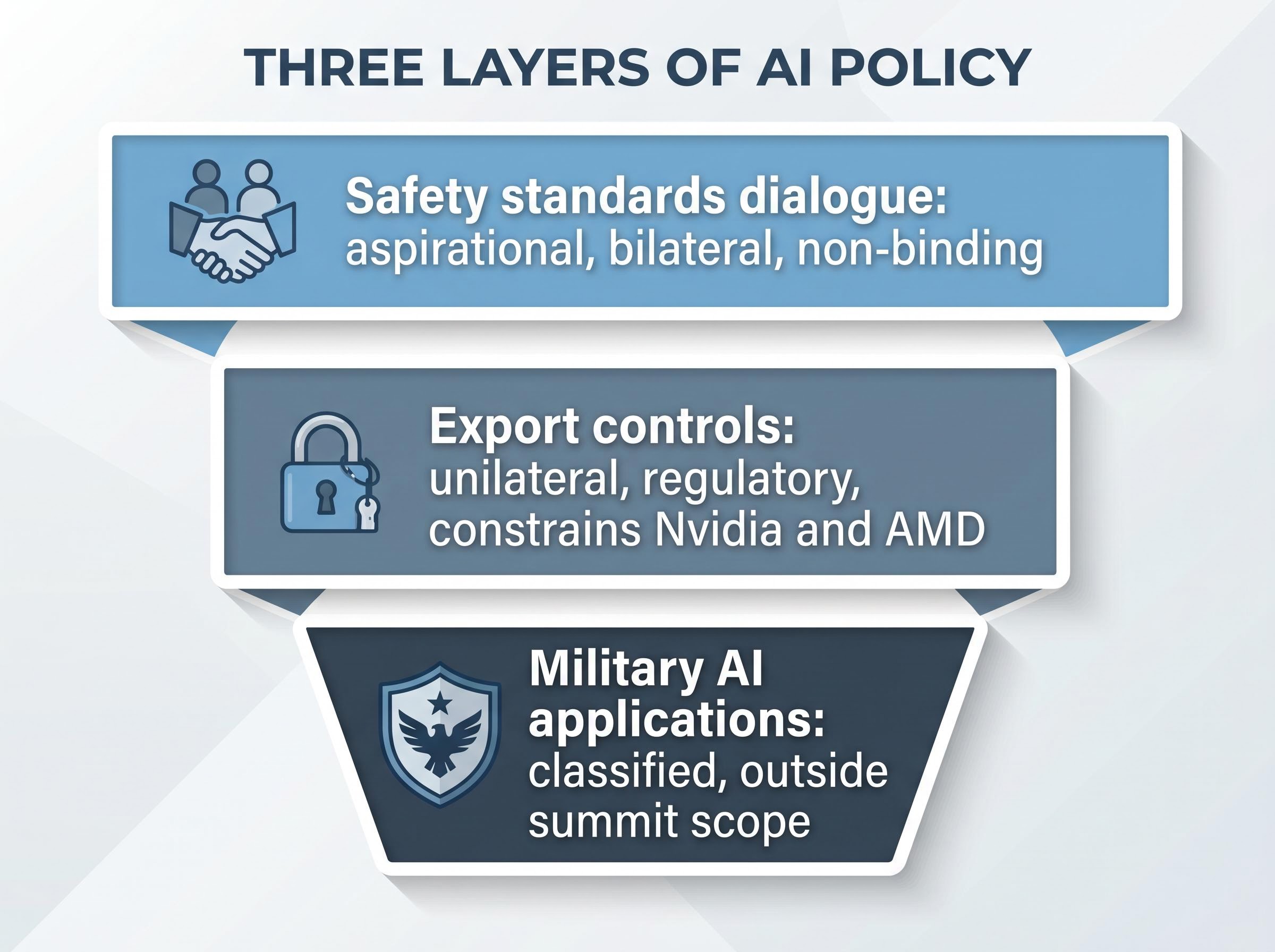

Three distinct layers of AI policy are frequently conflated in summit coverage, though they operate on entirely separate tracks:

Both nations are in an active AI race where revealing standards or constraints would disadvantage the disclosing party. CFR has noted that China holds leverage on technology in the broader negotiating context, which further reduces its incentive to concede ground.

Chip export rules, investment restrictions, and technology design controls are administered through agency rulemaking and executive orders, not through summit communiqués. Diplomatic warmth does not translate to policy change without separate regulatory action. A “memorandum on AI standards” (aspirational, non-binding) and an actual export control revision (requiring regulatory process) are not the same instrument, and confusing the two is what produces the over-reaction cycle that analysts are flagging.

This distinction gives investors a durable lens for reading future AI-related summit headlines.

Brent crude at approximately $106-107/bbl and WTI at approximately $100-101/bbl reflect ongoing Gulf disruptions, partially offset by summit de-escalation hopes. The U.S.-Iran conflict, initiated on 28 February 2026, continues with Strait of Hormuz targeting and proxy retaliation.

Iran stability is confirmed as a summit agenda item. Trump has previewed a “joint statement on Iran stability,” while China is pushing a neutral stance. CSIS confirms the topic is on the table, though no details have emerged. China’s ability or willingness to assist the U.S. on Iran remains genuinely uncertain.

Reuters has noted a potential U.S.-China buyer consortium for Iranian energy alternatives in the event of sustained disruptions, which would be a bullish signal for energy equities such as the XLE ETF if confirmed.

Fidelity’s Macro Team remains bearish on a sustained oil rally without a formal deal, suggesting current pricing already reflects the de-escalation premium.

Energy sector positioning around this summit requires a probability-weighted view across three distinct scenarios:

| Iran Outcome Scenario | Oil Price Direction | Energy Sector (XLE) Implication | Broader Market Effect |

|---|---|---|---|

| Diplomatic de-escalation | Bearish (prices ease) | XLE retraces; rotation into cyclicals | Risk-on rally; equities broaden |

| Status quo | Oil stays elevated | Energy sector holds current levels | Neutral to mildly negative |

| Escalation failure | Spike risk (above $110/bbl) | XLE rallies further | Defensive positioning; risk-off |

The summit’s Iran chapter is the least predictable of the three agenda items and carries the most asymmetric investment risk.

The downstream cost pass-through from sustained Hormuz disruption extends well beyond the energy sector directly: jet fuel tanker loadings collapsed 50% week on week in early May, and consumer-facing companies including Whirlpool and Shake Shack had already reported Q1 2026 earnings damage tied to petroleum-derived cost increases, meaning the Iran wildcard carries second-order equity exposure that the XLE and crude price alone do not capture.

The market’s current bullish tilt is treating all three agenda areas as directionally positive. That is an averaging of very different probability distributions.

| Agenda Item | Realistic Outcome Range | Asset Class Most Affected | Signal to Watch |

|---|---|---|---|

| Trade | Narrow but possible purchase wins; no structural tariff reform | U.S. cyclicals, agribusiness, LNG exporters | Confirmed $50B purchase framework language in communiqué |

| AI security | Optics-driven semiconductor rally; capped by export controls | SMH ETF, Nvidia | Any confirmed AI memorandum text; export control changes (unlikely) |

| Iran / energy | Widest uncertainty; most asymmetric risk | XLE, Brent, WTI | Joint statement specifics; oil price movement post-summit |

Jonas Goltermann of Capital Economics has warned that the CSI 300 rally is likely to fade without confirmed tariff cuts. Yardeni’s qualified S&P 500 upside remains conditional on agricultural and energy deal confirmation. Julian Emanuel of BTIG has reiterated that export controls cap the semiconductor rally regardless of summit optics. The USD/CNY at approximately 6.79 reflects modest risk-on conditions but no major repricing.

No final communiqués or binding outcomes have emerged from Day 1. Official White House and Xinhua post-summit press releases are the pending catalyst that will determine whether current positioning is validated or exposed.

Trade is the most achievable agenda item, with a narrow but real path to a confirmed purchase framework. AI security is structurally unlikely to produce substance, and the recurring pattern of diplomatic optics masking policy inaction should be expected at every future bilateral meeting. Iran is the highest-uncertainty wildcard with the most asymmetric market impact.

The specific pending catalysts are the official post-summit communiqués from the White House and Xinhua, any confirmed language in an AI standards memorandum, and oil price movement as the live Iran signal.

The current market enthusiasm is running ahead of binding outcomes. Calibrated positioning, with specific attention to the gap between Day 1 optimism and the structural barriers that remain across all three agenda areas, is better matched to the actual probability landscape than directional bets placed on summit atmosphere alone.

For investors wanting to translate the probability-weighted framework in this analysis into concrete portfolio action, our dedicated guide to geopolitical portfolio positioning covers gold allocation targets, sector exposure review, rebalancing cadence, and the specific conditions under which historical geopolitical drawdowns have reversed, with institutional frameworks from BlackRock and Vanguard built around the 2025-2026 crisis cycle.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and geopolitical conditions. Past performance does not guarantee future results.

A Phase One-lite framework refers to a narrower trade agreement where China commits to increasing purchases of U.S. agricultural and energy products, in this case by a reported $50 billion annually, without requiring legislative changes or structural tariff reform on either side.

Chip export controls are administered through agency rulemaking and executive orders, not summit communiques, meaning diplomatic warmth cannot override the existing regulatory architecture that restricts sales of advanced chips like the H20 to China without a separate rulemaking process.

Brent crude is trading near $106-107 per barrel due to ongoing Strait of Hormuz disruptions, and the summit's Iran agenda item carries the widest uncertainty of the three topics, with escalation failure posing a spike risk above $110 per barrel while diplomatic de-escalation would pressure energy sector holdings like the XLE ETF.

U.S. agribusiness equities and LNG exporters are the most direct beneficiaries of a confirmed trade purchase framework, the SMH ETF and Nvidia are exposed to short-term semiconductor optics plays, and the XLE ETF along with Brent and WTI crude prices are the key instruments for tracking the Iran wildcard.

The key pending catalysts are the official post-summit communiques from the White House and Xinhua, any confirmed language in an AI standards memorandum, and oil price movement as a live signal on the Iran outcome, since no binding agreements emerged from Day 1.