UBS Cuts Gold Forecasts by Up to $900 as Fed Delays to 2027

7 hrs ago

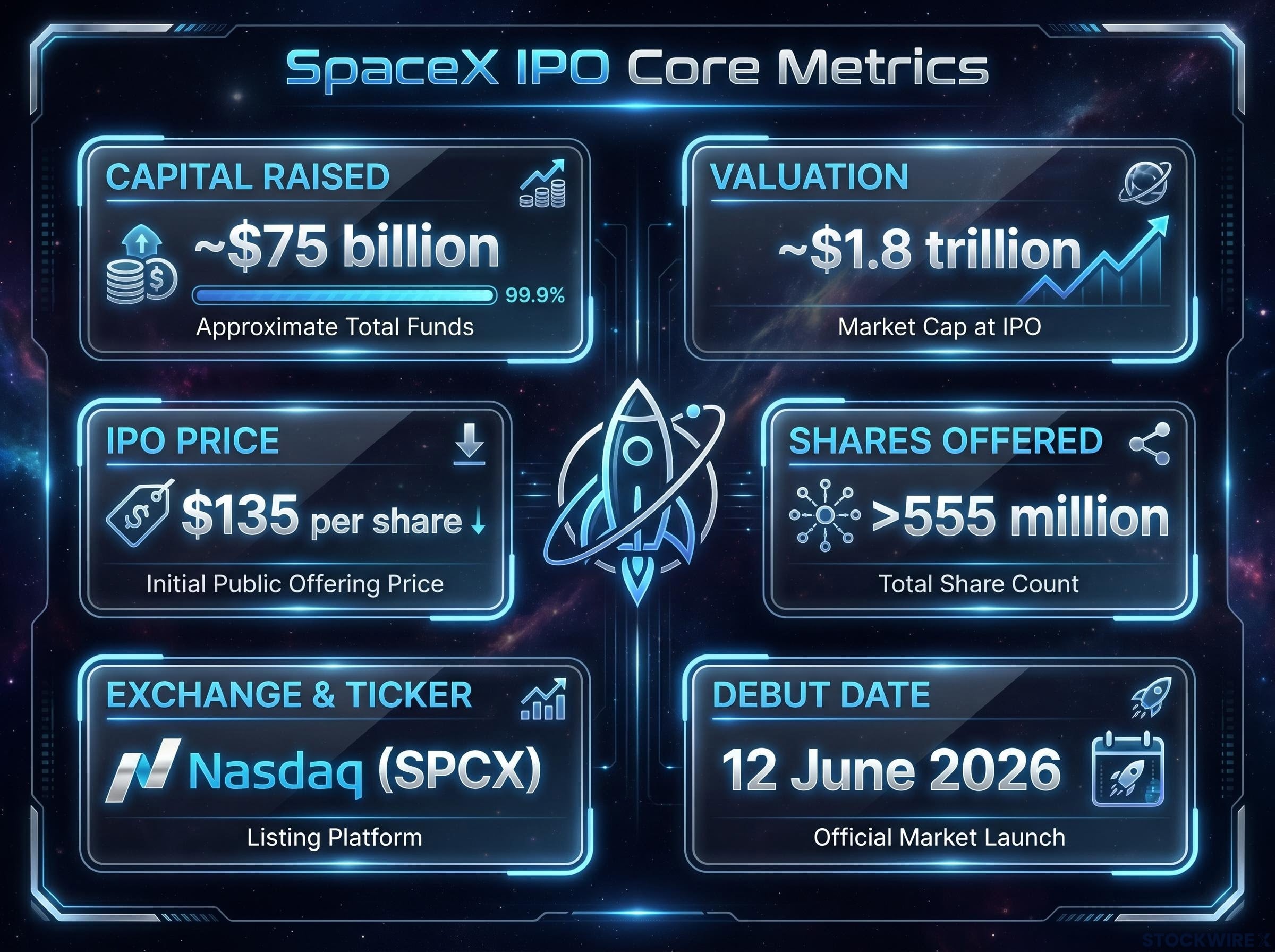

At $135 per share, SpaceX’s Nasdaq debut on 12 June 2026 raised approximately $75 billion in a single session, making every previous initial public offering (IPO) in recorded history look modest by comparison. The listing, trading under the ticker SPCX, arrives as the space industry transitions from a government-funded frontier to a mainstream investable asset class. More than 555 million shares priced at a valuation of roughly $1.8 trillion entered the public market with no precedent in scale or investor appetite.

What follows covers what happened today, why the numbers carry the weight they do, how institutional and retail demand shaped the debut, and what the event signals for the space sector and broader markets going forward.

The arithmetic speaks for itself. SpaceX priced more than 555 million shares at $135 each, raising approximately $75 billion and implying a company valuation at pricing of roughly $1.8 trillion (some reports specify $1.77 trillion). No IPO in any sector, in any geography, at any point in market history has matched that figure.

An inflation-adjusted IPO record comparison with Saudi Aramco’s 2019 listing complicates the headline narrative: Aramco’s $1.71 trillion implied valuation converts to roughly $2.21 trillion in 2026 dollars, meaning SpaceX’s nominal capital-raised record is genuine while its valuation record requires more careful qualification.

The core metrics of the offering:

One distinction matters for anyone interpreting the headline figure. The $75 billion raised reflects the capital generated from selling the IPO tranche, not the company’s total worth. The shares offered in the IPO represent only a fraction of total outstanding shares. The full share count, including pre-existing equity held by insiders and early investors, underpins the $1.8 trillion valuation at pricing. Conflating the two figures produces a misleading read of the stock’s opening position.

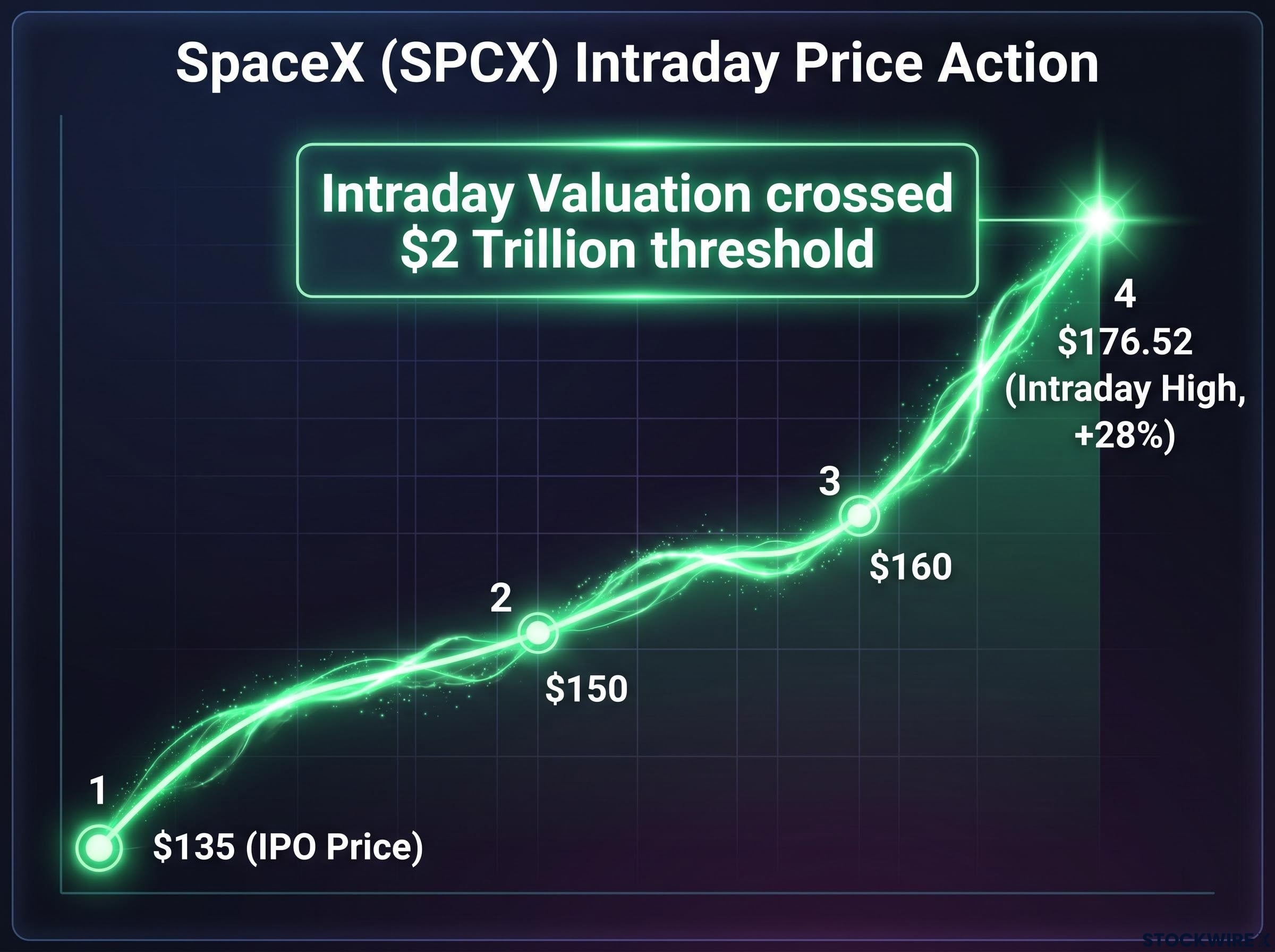

Trading opened and the price moved immediately. Within the first hours, SPCX climbed past $150, then pushed through $160, building momentum that carried the stock to an intraday high near $176.52, a gain of approximately 28% from the $135 IPO price.

That figure sits within the 25-30% intraday range documented by CNBC, Reuters, and Yahoo Finance throughout the session. As of reporting, final closing confirmation remained pending, meaning the 28% figure reflects the best available intraday data rather than a settled end-of-day print.

SpaceX’s intraday valuation crossed the $2 trillion threshold during its first trading session, a milestone no company has reached on debut day.

The $2 trillion crossing follows directly from the intraday arithmetic. A 28% gain applied to a $1.8 trillion starting valuation implies an intraday market capitalisation near $2.3 trillion. The $2 trillion marker was crossed during the session, supported by emerging Reuters data, though it had not been confirmed as a closing valuation at the time of reporting.

For investors tracking the stock, the distinction between intraday milestones and confirmed closing data is material. Debut-day volatility profiles can compress or expand rapidly in final-hour trading, and the difference between an intraday peak and a settlement price carries real portfolio implications.

Today’s trading bell was the visible end of a process that unfolded over months. For readers less familiar with the mechanics, an IPO (initial public offering) is the process by which a private company sells shares to the public for the first time, enabling anyone with a brokerage account to buy ownership in the business.

The pipeline for a listing of this magnitude follows a defined sequence:

The float, meaning the portion of total shares actually available for public trading, is smaller than the total share count. This is why 555 million shares at $135 raised $75 billion, while the company’s market capitalisation at pricing sat near $1.8 trillion. The remaining shares are held by insiders, early-stage investors, and employees whose stakes were not part of the public offering.

The pipeline for a listing of this magnitude follows a defined sequence, but IPO mechanics for retail investors diverge sharply from the institutional experience at almost every stage: most public buyers cannot access shares at the offering price and instead enter the secondary market after institutions have already been allocated, absorbing any first-day premium rather than benefiting from it.

Two forces shaped demand for this offering, and they are not the same force.

The first is operational. SpaceX operates the most active commercial launch vehicle programme in the world, holds government contracts across defence and civilian agencies, and runs Starlink, one of the fastest-scaling satellite communications networks ever built. Those fundamentals attracted institutional capital on their own merits.

The second is personal. Elon Musk’s ownership stake and leadership role featured prominently in coverage from Reuters, CNBC, Bloomberg, and the New York Times, with multiple outlets framing the IPO partly through the lens of its implications for Musk’s net worth. His track record across Tesla and other ventures has built a personal brand that functions, for better or worse, as a valuation input. Institutional investors pricing in a “Musk premium” are making a bet not just on the company’s cash flows but on the continued market-moving effect of its founder’s profile.

Tesla’s sell-off on IPO pricing day, with shares falling more than 5% as investors rotated into SPCX and reassessed Tesla’s standalone fundamentals, illustrates how directly the ‘Musk premium’ discussion affects adjacent positions, with some institutional allocators citing the merger thesis as a primary reason for holding TSLA even as Wolfe Research identifies mid-2027 as the earliest realistic deal timeline.

Coverage of the SpaceX IPO across major financial outlets devoted as much space to Musk’s ownership stake and wealth implications as to the company’s operational fundamentals, a dynamic that speaks to how heavily personal brand weighs on institutional sentiment at this scale.

That tension between company fundamentals and founder premium is unresolved, and it will remain so. Investors assessing whether the valuation at these levels reflects durable business value or sentiment-driven demand will need to sit with that ambiguity for some time.

The SpaceX debut sent energy in two directions at once.

The first was upward. The listing elevated the space industry’s profile as an investable asset class in a single session. Capital that had not previously considered space-sector exposure now has a liquid, large-cap entry point on a major exchange. That gravitational pull is expected to draw fresh institutional attention to the sector broadly.

The second was downward. Several smaller pure-play space companies experienced selling pressure concurrent with the IPO, a pattern consistent with how mega-IPOs have historically affected adjacent names.

The two-direction effect, in summary:

MSCI research on megacap IPO sector turnover identifies index inclusion mechanics and portfolio rebalancing as the primary transmission channels through which a large-scale debut generates selling pressure on existing sector peers, a pattern directly relevant to the smaller space-sector names that experienced concurrent declines during the SpaceX session.

This pattern is structurally plausible and consistent with mega-IPO history, though specific attribution to individual strategists in live coverage could not be independently verified across multiple sources.

For investors holding smaller space-sector positions, the near-term pressure may reflect temporary portfolio rebalancing rather than deteriorating fundamentals. That distinction matters for position management in the weeks ahead.

A $1.8 trillion valuation at pricing. An intraday crossing above $2 trillion. These are not just records; they are reference points that will shape every space-sector listing, valuation negotiation, and capital allocation decision that follows.

Future space companies approaching public markets will be priced and evaluated in reference to what SpaceX established today. The benchmark has shifted. The conversation about what public markets will pay for space-sector exposure has moved from speculative to empirical, anchored by a single session’s trading data.

What remains unresolved is whether the debut-day premium holds. Final closing figures for 12 June 2026 were pending at the time of reporting. Longer-term trading stability is unknown. The question of whether a 28% first-day surge represents price discovery or euphoria will take weeks, possibly months, to answer.

Those are different analytical problems. Today’s structural milestone, the largest IPO in history reaching a $2 trillion intraday valuation, is a settled fact. What the stock does next week is not.

For investors wanting to situate the SpaceX debut within the broader 2026 listing cycle, our full explainer on market absorption of mega-IPOs examines Standard Chartered’s warning that the near-simultaneous $3.5 trillion wave of SpaceX, Anthropic, and OpenAI listings is expected to create digestion difficulties over the summer months, with PwC Q1 2026 data and analyst commentary on how institutional demand behaves differently under compressed multi-offering windows.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and first-day trading data is subject to final settlement confirmation.

The SpaceX IPO was the company's initial public offering on the Nasdaq exchange under the ticker SPCX, which commenced trading on 12 June 2026 at a price of $135 per share, raising approximately $75 billion and implying a valuation of roughly $1.8 trillion at pricing.

SpaceX raised approximately $75 billion by selling more than 555 million shares at $135 each, surpassing every previous IPO in recorded history by capital raised; for context, Saudi Aramco's 2019 listing had the prior valuation record, which converts to roughly $2.21 trillion in 2026 dollars.

SPCX surged from its $135 IPO price to an intraday high near $176.52 on its debut day, a gain of approximately 28%, which pushed SpaceX's intraday market capitalisation above the $2 trillion threshold for the first time on a debut day.

The SpaceX listing created a two-direction effect: it elevated the space sector's profile as an investable asset class while simultaneously generating selling pressure on smaller pure-play space companies, consistent with the capital rotation pattern seen historically around large-scale IPOs.

The $75 billion reflects only the capital raised from selling the IPO tranche of more than 555 million shares, while the $1.8 trillion valuation is calculated from the full share count including pre-existing equity held by insiders, early investors, and employees whose stakes were not part of the public offering.