How Many Westpac Shares You Need for $10,000 in Income

3 hrs ago

A stock can fall after beating earnings estimates. It happened to Clorox, which dropped roughly 2.45% after its Q1 2025 beat. It happened to Wynn Resorts, which shed 5-7% despite clearing the headline bar. And it happened, in a different way, to Restaurant Brands International, whose near-miss was framed in some coverage as though the result were close enough. The pattern is not an anomaly; it is a signal that the headline number is the least important part of an earnings report. With approximately 71% of S&P 500 companies now publishing both GAAP and non-GAAP earnings figures, according to Calcbench data from June 2025, the number a retail investor sees on a brokerage feed is often an adjusted figure stripped of costs the company deemed inconvenient. In a market shaped by tariff uncertainty and softening consumer spending, the gap between reported beats and genuine business health has widened. This guide provides a repeatable framework for evaluating any earnings report across the four layers that matter most: the source of the beat, the accounting presentation, the forward outlook, and the multi-period margin trend.

Wall Street consensus estimates are not discovered; they are constructed. Management teams guide analysts toward beatable targets through investor relations conversations, pre-announcement signals, and carefully managed expectations. The result is a bar that companies can step over without necessarily demonstrating business strength.

The structural tendency for management to guide toward beatable targets was on full display in the most recent reporting season, where analyst estimate conservatism produced a blended S&P 500 surprise of 20.7%, nearly three times the five-year norm, because pre-season forecasts had been anchored well below actual results.

The distinction matters. A company that beats estimates because genuine demand exceeded forecasts is in a fundamentally different position from one that beat because the bar was set conservatively. Clorox shares fell approximately 2.45% after its Q1 2025 beat, with analysts flagging that the result relied more on cost discipline than organic revenue growth. Wynn Resorts fell 5-7% post-earnings despite a headline beat, as commentary pointed to consumer caution and high costs. Restaurant Brands International reported adjusted EPS of $0.75 versus the $0.78 consensus and revenue of $2.11 billion versus the $2.13 billion estimate, according to CNBC reporting on 8 May 2025. Even a technical miss can receive soft framing in headlines.

Comparing a company’s performance against its broader sector provides necessary context. A beat in a struggling industry may reflect genuine competitive advantage, or it may reflect that the company’s reporting presents a more favourable picture than the underlying business warrants.

Not all beats carry equal weight. A few conditions separate signal from noise:

When these conditions are absent, and instead the beat arrives with narrowed guidance, inventory buildup, or cost-cutting as the primary driver, scepticism is warranted.

GAAP, or generally accepted accounting principles, is the standardised accounting framework that U.S. public companies are required to use when filing financial statements. Non-GAAP figures exist as a supplementary presentation, intended to give investors a clearer view of recurring operating performance by stripping out items management considers non-representative.

The problem is what gets stripped out. With 71% of S&P 500 companies now publishing both GAAP and non-GAAP earnings figures, according to Calcbench data from June 2025, most earnings headlines a retail investor encounters are adjusted numbers. The most commonly excluded items include:

The SEC maintains active scrutiny of non-GAAP presentations that prioritise adjusted metrics over GAAP in ways that could mislead investors.

SEC scrutiny of non-GAAP presentations has intensified through Compliance and Disclosure Interpretations that specifically target adjustments giving undue prominence to adjusted metrics over GAAP results, making the reconciliation table not just a disclosure formality but a document regulators and informed investors examine closely.

The reconciliation table is typically located in the earnings press release, often in the supplementary financial tables section, and in the 10-Q quarterly filing. It shows each line item that management excluded to arrive at the adjusted figure.

Focus on two things. First, examine which items are being excluded and whether they recur quarter after quarter. Second, track the gap between GAAP and non-GAAP EPS over several periods. A large and growing gap suggests that management is increasingly relying on exclusions to present favourable results. That widening divergence is one of the most reliable signals that adjusted earnings are drifting further from economic reality.

Investors price anticipated future performance, not historical results. This is why a strong past quarter can still produce a negative price reaction if guidance disappoints; the market already absorbed the backward-looking data and is recalibrating around forward expectations.

The key guidance signals to monitor fall into a pattern. When management raises revenue and EPS guidance, narrows the range upward, and maintains or increases specificity, the forward outlook is amplifying the current quarter’s strength. When management cuts guidance, narrows the range to the downside, withdraws targets, or shifts from specific numeric projections to qualitative descriptions, the signal points in the opposite direction, regardless of the headline beat.

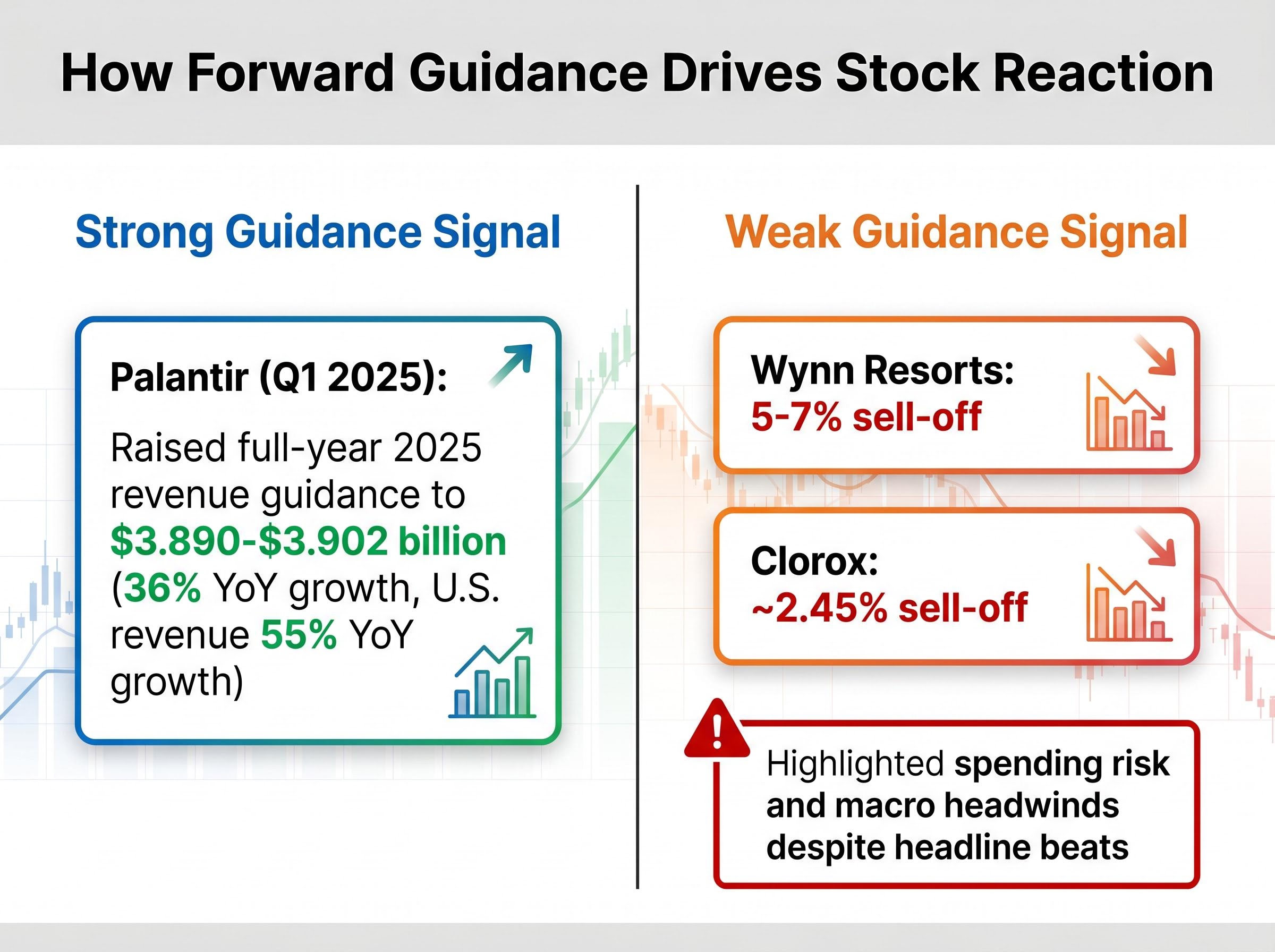

Palantir raised its full-year 2025 revenue guidance to $3.890-$3.902 billion following its Q1 2025 results, representing 36% year-over-year growth, with U.S. revenue growing 55% year-over-year, according to Palantir investor relations. The guidance raise gave the beat its durability signal.

Contrast that with the consumer sector. Both Wynn Resorts and Clorox highlighted spending risk and macro headwinds in their guidance commentary despite headline beats. The market’s response, sell-offs of 5-7% and approximately 2.45% respectively, reflected the guidance more than the reported quarter.

Several specific red flags in guidance language warrant attention:

Management language is where confidence (or its absence) becomes visible. The guidance section of an earnings press release often reveals more than the income statement.

A single quarter’s margin figure is a snapshot. The direction that margin has been travelling across six to eight quarters is the trend. Expanding margins over multiple periods indicate that a company is converting revenue growth into proportionally more earnings, the clearest signal of operational leverage and durable business strength.

Amazon and Uber both deliberately prioritised market share over near-term profitability during their growth phases, which meant evaluating their margin trajectories required understanding the business cycle context rather than applying a fixed profitability standard. Margin trajectory interpreted within business strategy context is more informative than margin level in isolation.

| Metric | Warning Signal | What It May Indicate |

|---|---|---|

| Receivables (days sales outstanding) | Rapidly rising relative to revenue growth | Aggressive revenue recognition; customers may not be paying on schedule |

| Inventory | Building faster than sales growth | Demand weakness or obsolescence risk; potential future write-downs |

| Payables | Stretching significantly beyond historical norms | Liquidity stress; the company may be delaying payments to preserve cash |

These three working capital metrics, drawn from the CFA Institute’s 2025 Quality of Earnings framework, are interconnected. Rising receivables paired with inventory buildup and stretching payables together paint a picture of a business under financial pressure, even if the income statement looks healthy.

Operating cash flow should broadly track net income over time. A persistent divergence where reported earnings grow but operating cash flow lags or declines is a red flag for accrual manipulation or premature revenue recognition.

Berkshire Hathaway’s Q1 2026 result illustrates what operating cash flow backing looks like in practice: $11.346 billion in operating profit driven by insurance underwriting and BNSF railroad, divisions that generate predictable cash rather than accrual-heavy accounting gains, alongside a $397 billion cash position that confirms earnings are not being consumed to fund the business.

The cash flow statement, found in every 10-Q and 10-K filing, shows operating cash flow as the first major section. Compare this figure to net income across four to six consecutive quarters. If free cash flow is declining while reported earnings grow over multiple periods, or if operating cash flow sits consistently below net income across several quarters, the reported earnings may lack genuine cash backing.

This is the CFA Institute’s “Proof of Cash” concept in practice. Cash is harder to manipulate than accrual-based earnings, making it the most reliable reality check available in public filings.

For investors who rely on the 10-Q cadence to run the cash flow checks described in this guide, our full explainer on SEC quarterly reporting changes covers the proposed shift to semiannual filings, what information would disappear between reporting periods, and the timeline before any rule takes effect.

Two mechanical paths lead to an earnings beat, and they carry very different implications for the quarters ahead.

A revenue-led beat means the company generated more income from customers than expected. Revenue growth outpaced operating expense growth, indicating that demand is doing the heavy lifting. This is generally repeatable because it reflects genuine market traction.

A cost-cut beat means the company held or shrank its expense base to deliver a better-than-expected bottom line, often while revenue growth was flat or modest. This lever gets harder to pull each subsequent quarter; a company can only reduce headcount, renegotiate supplier contracts, or defer discretionary spending so many times before the cuts begin to affect the business itself.

Clorox in Q1 2025 illustrates the distinction clearly. Earnings quality was flagged specifically for reliance on cost cutting rather than organic revenue growth. The headline beat masked the question of whether the company could sustain the result without further expense reduction.

Analyst commentary in early 2025, including coverage from Barron’s and the Wall Street Journal, identified a practitioner red flag threshold: when cost cuts account for more than 5% of the earnings beat rather than organic growth, the result warrants closer scrutiny.

The practical test is straightforward. If revenue grew faster than operating expenses, the beat has a structural foundation. If expenses shrank while revenue growth was limited, probe further.

| Attribute | Revenue-Led Beat | Cost-Cut Beat |

|---|---|---|

| What drives it | Genuine demand growth exceeding forecasts | Expense reduction, headcount cuts, deferred spending |

| Repeatability | Generally repeatable if demand persists | Diminishing returns each subsequent quarter |

| Margin implication | Expanding margins through operational leverage | Margins may appear stable but lack growth support |

| Investor signal | Business is gaining market traction | Business may be managing decline |

A company experiencing declining earnings may cut spending to limit the damage, making profitability appear healthier than the business actually is. Revenue should ideally increase at a faster pace than operating expenses over any sustainable growth period.

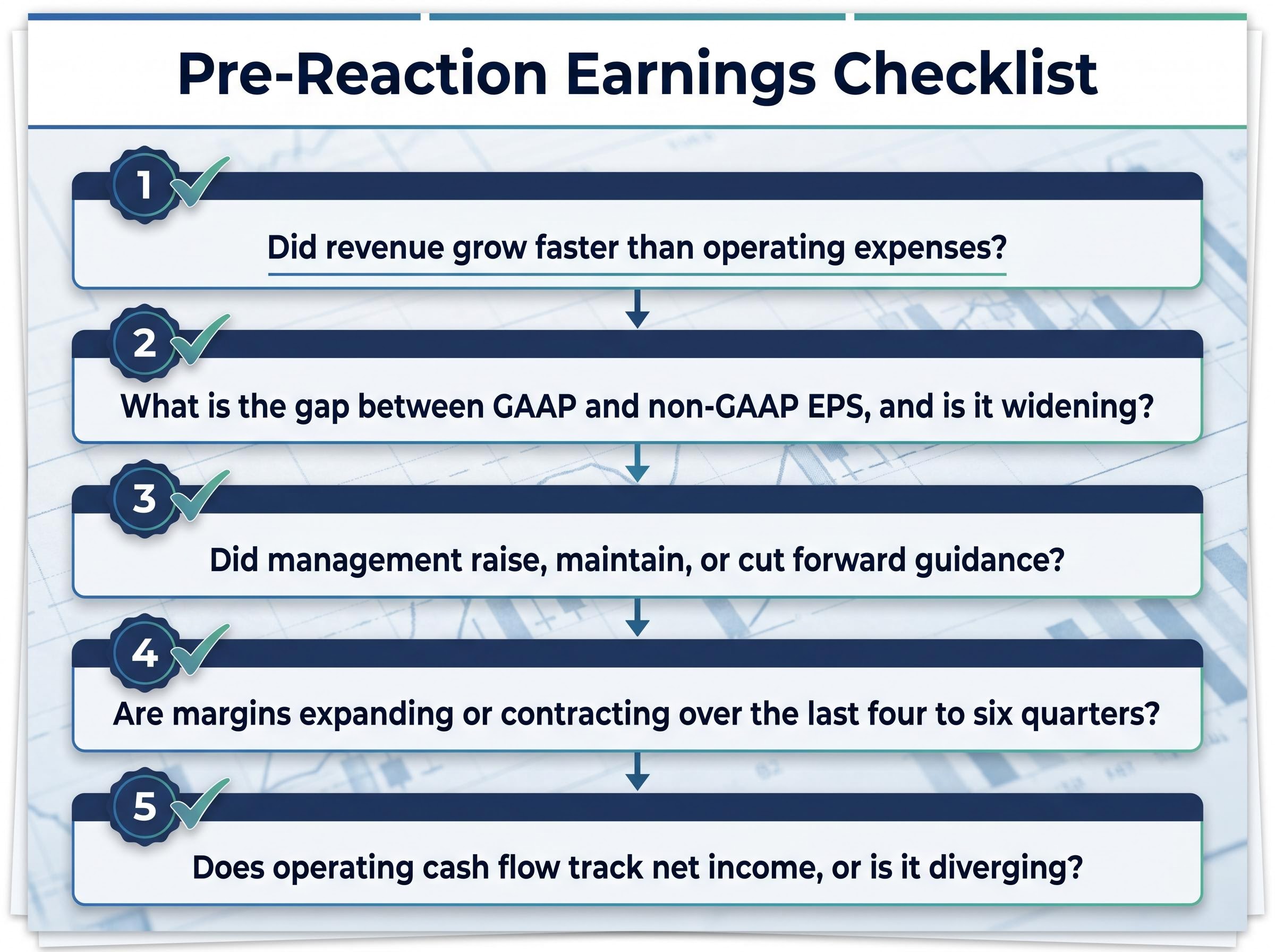

The four diagnostic layers covered in this guide, beat source, accounting presentation, guidance direction, and margin and cash trends, can be distilled into five questions to ask before reacting to any earnings headline:

Run this checklist against at least two to three prior quarters for context. Consistency across multiple reporting periods is a far stronger durability signal than any single quarter’s headline.

Earnings beat sustainability across an entire reporting season is subject to the same diagnostic questions this framework applies to individual companies: whether AI monetisation and consumer resilience can repeat the performance, or whether a blowout quarter has borrowed returns from future periods, is the central debate following the Q1 2026 results.

Consistency across multiple periods is a stronger durability signal than any single quarter’s headline beat. A company that passes all five checks once may be having a good quarter. A company that passes them repeatedly is demonstrating business quality.

Comparing results against sector peers adds a further layer. A company outperforming in a declining industry may reflect genuine competitive advantage, or it may indicate that reporting differences are flattering relative results. Growth driven by expansion of core products and services is more reliable than gains attributable to non-recurring items, and pricing power is a more durable revenue driver than volume gained through discounting.

The headline beat number is where analysis starts, not where it concludes. Whether the result warrants optimism or scepticism depends on the four layers beneath it: where the beat came from, how the accounting presents it, what management says about the future, and whether margin and cash flow trends confirm or contradict the reported strength.

Apply the five-question checklist to the next earnings report that crosses a brokerage feed, and revisit results across at least three consecutive quarters before drawing conclusions about business trajectory. The reconciliation table, the cash flow statement, and the guidance language section of a press release are the three most underread documents in a typical retail investor’s earnings review process. They are also where the most useful information lives.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

GAAP earnings follow standardised accounting rules required for SEC filings, while non-GAAP earnings are adjusted figures where management strips out costs like stock-based compensation or restructuring charges. The gap between the two matters because a large or growing difference can signal that a company is increasingly relying on accounting exclusions to present favourable results.

A stock can fall after an earnings beat when guidance disappoints, when the beat was driven by cost cuts rather than revenue growth, or when commentary signals macro headwinds ahead. Clorox dropped roughly 2.45% and Wynn Resorts fell 5-7% after headline beats because the market focused on forward outlook and earnings quality rather than the headline number alone.

Check whether revenue grew faster than operating expenses, examine the GAAP-to-non-GAAP reconciliation table for recurring exclusions, review whether management raised or cut forward guidance, and compare operating cash flow to net income across four to six consecutive quarters. A beat supported by all four of these checks is far more durable than one relying on cost cuts or accounting adjustments.

A revenue-led beat means customer demand exceeded forecasts, making the result generally repeatable if demand persists. A cost-cut beat means the company reduced its expense base to hit the bottom-line target, a lever with diminishing returns each subsequent quarter because there are limits to how many times headcount, supplier contracts, or discretionary spending can be cut.

Operating cash flow should broadly track net income over time; a persistent divergence where reported earnings grow but operating cash flow lags or declines is a red flag for accrual manipulation or premature revenue recognition. Because cash is harder to manipulate than accrual-based earnings, comparing the two across four to six quarters is one of the most reliable reality checks available in public filings.