JDO Shares Collapse 46% After Judo Capital Breaks April Guidance

1 hr ago

Berkshire Hathaway posted its strongest quarterly operating profit in more than a year this morning, clearing $11.346 billion in Q1 2026 and beating analyst expectations by a comfortable margin. Yet the stock remains down roughly 6% year-to-date. That gap between what the business is earning and what the market is paying tells the story investors are trying to read right now: a company firing on most operational cylinders while sitting on a record $397 billion cash pile that its new CEO has not yet put to work.

The results landed on Saturday 2 May 2026, the same morning Greg Abel presided over his first annual shareholder meeting as chief executive in Omaha. Warren Buffett, now 95, attended as a spectator. The quarterly numbers, the leadership transition, and the unanswered question of capital deployment all arrived on the same stage. What follows is a breakdown of the headline figures, the segment-level detail, the cash position debate, and what the Abel era means for shareholders evaluating the company from here.

Berkshire Hathaway reported $11.346 billion in operating earnings for Q1 2026, up approximately 18% from $9.641 billion in the year-ago quarter.

$11.346 billion in Q1 2026 operating profit, up 18% year-over-year.

On a per-share basis, operating EPS came in at approximately $5.26 for BRK.B, comfortably ahead of pre-release analyst consensus estimates near $4.82. Net EPS, a figure that includes unrealised investment gains and losses, was approximately $4.68, a divergence worth understanding (more below).

Berkshire does not hold earnings conference calls. The results were published via press release and Form 10-Q filing at approximately 7:00 a.m. Central Time, ahead of the annual shareholder meeting. That gathering, rather than any analyst dial-in, serves as the primary venue for executive commentary on the numbers. The 18% operating profit increase gives Abel a strong opening data point, though the earnings beat alone has not been enough to reverse the stock’s year-to-date slide.

Berkshire has guided investors to focus on operating earnings since at least 2018, a preference that Abel inherits and maintains. The distinction matters because it determines whether a given quarter looks strong or weak in the headlines.

Berkshire’s 2018 shareholder letter formally established operating earnings as the company’s preferred performance metric, with Buffett arguing that GAAP net income had become an unreliable indicator of business value for any company holding a large equity portfolio subject to mark-to-market accounting rules.

Operating profit measures what the company’s businesses actually earned from their day-to-day operations. It strips out the noise that market movements create in the investment portfolio. What it includes and excludes:

Q1 2026 illustrates the point directly. Operating EPS came in at approximately $5.26, reflecting genuine business performance. Net EPS landed at approximately $4.68, dragged lower by mark-to-market adjustments in the investment portfolio. A reader scanning only the net figure would conclude the quarter was softer than it actually was.

For a company with one of the largest equity portfolios in the world, net income is a volatile figure that can mask or inflate the underlying business trajectory. Operating earnings offer a cleaner read, and that is why Berkshire treats them as the preferred metric.

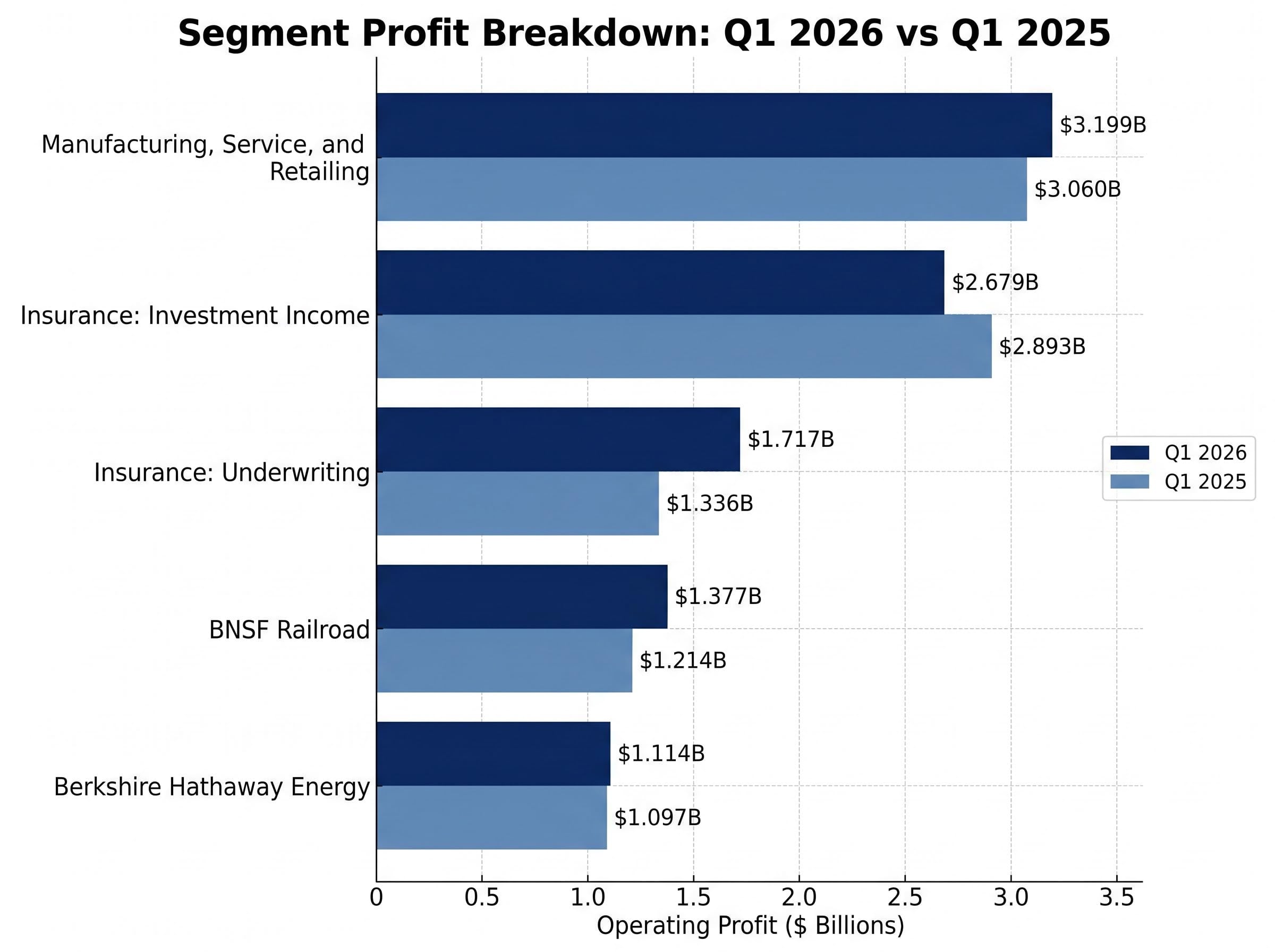

The headline profit figure gains more meaning at the segment level. Five reporting lines contributed to the $11.346 billion total, and the improvement was not evenly distributed.

| Segment | Q1 2026 | Q1 2025 | Direction |

|---|---|---|---|

| Insurance: Underwriting | $1.717B | $1.336B | ▲ |

| Insurance: Investment Income | $2.679B | $2.893B | ▼ |

| BNSF Railroad | $1.377B | $1.214B | ▲ |

| Berkshire Hathaway Energy | $1.114B | $1.097B | ▲ |

| Manufacturing, Service, and Retailing | $3.199B | $3.060B | ▲ |

Insurance underwriting delivered the largest absolute improvement, adding $381 million year-over-year. BNSF contributed a $163 million increase, its strongest quarterly showing in recent periods. Manufacturing, Service, and Retailing remained the single largest segment at $3.199 billion, growing modestly.

The one line moving the wrong way was insurance investment income, which fell from $2.893 billion to $2.679 billion. The decline likely reflects the composition and yield environment of the fixed-income portfolio, though Berkshire’s limited disclosure makes it difficult to attribute the drop to a single factor.

Berkshire Hathaway Energy was essentially flat. The operational story of Q1 2026 is one of insurance and rail strength offsetting modest softness elsewhere.

The figure that draws the most attention in this release is not on the income statement.

Berkshire’s cash and short-term Treasury holdings reached approximately $397 billion at the end of Q1 2026, a record high.

The position is concentrated heavily in short-term U.S. Treasuries, a deliberate choice that generates yield while maintaining near-instant liquidity for a large acquisition. A minor measurement note: the Wall Street Journal cited approximately $381 billion, reflecting a narrower definition of cash; Bloomberg and Reuters both reported the broader figure inclusive of Treasury holdings at approximately $397 billion.

At what point does a cash reserve this large shift from a signal of Buffett-era discipline into a drag on shareholder returns? That question has followed Berkshire for several quarters, and Q1 2026 brings no resolution. As of today’s earnings release, no specific acquisition targets, buyback commitments, or deployment timelines have been publicly announced.

Berkshire’s cash deployment framework under Abel centres on opportunity quality rather than any fixed timetable, with the $373 billion position built across 19 months of deliberate abstention from meaningful stock purchases while the Buffett Indicator signalled historically poor forward return conditions.

BRK.B closed at $473.60 on 1 May and traded modestly higher on 2 May following the release, reaching an intraday high of $479.10. The stock remains down approximately 6% year-to-date, a gap between operational performance and market price that the cash pile partially explains. Investors are pricing in the opportunity cost of nearly $400 billion sitting in Treasuries rather than compounding in acquired businesses.

The annual meeting Q&A, running approximately 2.5 hours this afternoon, is the most likely near-term venue for Abel to address capital deployment directly.

Greg Abel assumed the CEO role at the start of 2026, five years after being publicly designated as Buffett’s successor in 2021. Today’s annual meeting is his first in the chair, and the format reflects his approach: approximately one hour of operational overview followed by approximately 2.5 hours of shareholder questions, beginning at 9:15 a.m. ET.

Buffett attended the meeting as an audience member, not a leadership figure. The symbolic weight of that shift is difficult to overstate for a company that has been synonymous with a single individual for six decades.

Investors watching Abel are evaluating three things:

One quarter does not define a CEO tenure. But today’s earnings give Abel a platform of operational strength from which to begin making his own decisions visible.

Q1 2026 confirms that Berkshire Hathaway’s operating engine is performing well. $11.346 billion in operating profit, an 18% year-over-year increase, and a beat against consensus expectations all point to a business with strong underlying momentum across insurance, rail, and its diversified manufacturing and services portfolio.

The unresolved question remains the same one investors have asked for several quarters: when and how will approximately $397 billion in cash and Treasuries be deployed, and will the return on that deployment justify the patience? That is the defining unknown of the Abel era, and today’s meeting Q&A may offer the first substantive clues.

For investors who want to contextualise Berkshire’s patience within a broader framework, our full explainer on US equity market valuation signals examines three converging indicators — the Buffett Indicator at 223.6%, the compressed equity risk premium, and the shrinking margin-of-safety opportunity set — that collectively explain why holding cash at near-$400 billion may be rational discipline rather than missed opportunity.

For investors tracking the story from here, the most immediate next steps are the annual meeting Q&A transcript, post-meeting analyst coverage, and the Form 10-Q filed today at Berkshire’s website. The earnings and press release were published on 2 May 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Berkshire Hathaway reported $11.346 billion in operating profit for Q1 2026, up 18% from $9.641 billion in Q1 2025, beating analyst consensus estimates of approximately $4.82 per share on a BRK.B basis.

Berkshire focuses on operating earnings because net income includes unrealised gains and losses on its massive equity portfolio, which can swing by billions in a single quarter and distort the true performance of its underlying businesses.

Berkshire Hathaway held approximately $397 billion in cash and short-term U.S. Treasury holdings at the end of Q1 2026, a record high, with the position concentrated in short-term Treasuries to maintain liquidity for potential acquisitions.

Greg Abel became CEO of Berkshire Hathaway at the start of 2026, five years after being designated as Buffett's successor in 2021; Buffett, now 95, attended the May 2026 annual shareholder meeting as a spectator rather than a leadership figure.

Despite strong Q1 2026 operating results, BRK.B shares remain down approximately 6% year-to-date, as investors are pricing in the opportunity cost of nearly $400 billion sitting in Treasuries rather than being deployed into acquired businesses.