Barclays Warns of Prolonged Market Volatility Under New Fed Reality

19 hrs ago

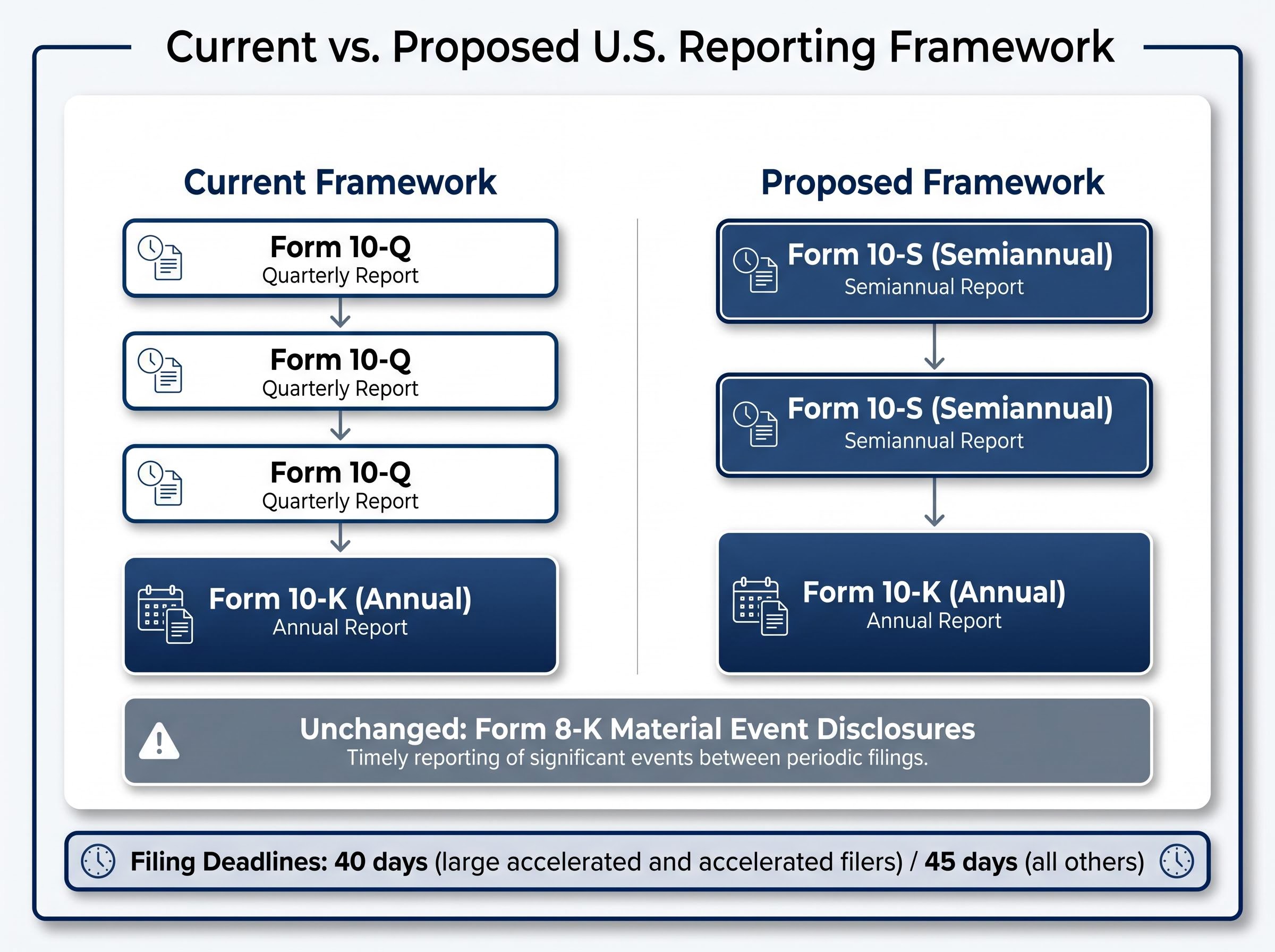

The Securities and Exchange Commission (SEC) proposed the most significant change to U.S. public company reporting cadence in decades on 5 May 2026, offering companies the option to file financial results twice a year instead of four times. The mechanism: a new Form 10-S that would replace the quarterly Form 10-Q for companies that opt in, while leaving annual Form 10-K and material event Form 8-K requirements untouched.

Published under release number 33-11414, the proposal arrives as part of a broader regulatory push under Chair Paul S. Atkins to reduce compliance burdens and give public companies more control over their disclosure rhythm. The change is optional, but its eligibility is sweeping and its implications for investor transparency are real.

What follows is a breakdown of who qualifies, how the new filing mechanism works, what investors stand to gain or lose, and how the proposal fits into global reporting norms, all before the public comment window closes.

Under the current framework, domestic public companies file three quarterly reports (Form 10-Q) and one annual report (Form 10-K) each year. The proposal published yesterday would let eligible companies replace their two mid-year 10-Q filings with a single new form, the Form 10-S, covering six-month semiannual periods.

The contrast is straightforward:

The annual 10-K stays. The 8-K stays. What disappears, for companies that elect the option, is the structured quarterly cadence that has defined U.S. public company reporting for decades.

The proposal also includes modifications to Regulation S-X to simplify financial disclosure requirements within the new semiannual framework.

Chair Atkins’ framing: Companies have an obligation to disclose material information, but the current system constrains their ability to determine the most appropriate reporting cadence.

This is not a minor procedural adjustment. It is a structural reclassification of how often investors receive comprehensive financial snapshots of the companies they own.

The most striking feature of the proposal’s eligibility criteria is what is absent: there is no size threshold, no revenue floor, and no listing-status requirement.

Any domestic public company subject to Exchange Act reporting under Sections 13(a) or 15(d) that currently files Form 10-Q is eligible. That includes:

The SEC drew deliberate lines around four categories:

The exclusion of foreign private issuers is logical rather than punitive; they already report semiannually. No adoption rate projections exist yet. That data is expected to emerge from analyst commentary during the comment period.

The election mechanism is a checkbox on Form 10-K or certain registration statements (S-1, S-3). Reverting to quarterly reporting requires simply leaving the box unmarked on the next Form 10-K. No 30-day notice is required.

Mid-year switches are not permitted. Any change takes effect at the start of the following fiscal year.

The cadence of financial disclosure is a structural element of how markets price risk and how investors detect deterioration early.

A standard Form 10-Q provides investors with a comprehensive interim update. Its core components include:

Financial professionals rely on Q1 and Q3 data specifically to track interim liquidity, operational trends, and forward-looking guidance between annual reports. Under current rules, large accelerated and accelerated filers must submit the 10-Q within 40 days of the quarter’s end; all others have 45 days.

The quarterly earnings cadence shapes how analysts build forward estimates, with each 10-Q filing providing the interim liquidity and margin data that feeds consensus models; the Q1 2026 season illustrated this dynamic sharply, producing a blended S&P 500 growth rate of 27.1% against a pre-season forecast of 13.1%, a gap that would have been significantly harder to detect under a semiannual reporting schedule.

The proposed Form 10-S would use those same deadlines but for semiannual periods only, reducing the filing count from four per year to two.

The distinction between periodic reports (10-Q, 10-K) and event-driven disclosures (8-K) is where the proposal’s design becomes consequential. Form 8-K triggers remain unchanged; material events must still be disclosed promptly.

An 8-K is triggered by specific material events: earnings releases, leadership changes, material agreements, and similar developments. It is not a substitute for the comprehensive periodic financial disclosure that a 10-Q provides.

The concept at stake is information asymmetry. Corporate insiders always have access to real-time operational data. Periodic filings narrow that gap for outside investors. Reducing the frequency of those filings widens it, regardless of whether 8-K obligations remain intact. Critics of the proposal have argued for expanding 8-K triggers as a compensating mechanism if quarterly reporting is reduced.

Material event disclosures through Form 8-K remain the primary real-time channel investors use to receive corporate news between periodic filings, but as high-profile cases such as unsolicited takeover bids illustrate, the timing and completeness of those disclosures depend entirely on whether a specific triggering event has occurred, not on whether the underlying financial picture has quietly deteriorated.

The policy tension is genuine, and both sides reflect structural concerns rather than rhetorical positioning.

The corporate and pro-reform case centres on a long-standing argument: quarterly reporting creates short-termism pressure, drives earnings guidance management, and imposes compliance costs that reduce management’s time for long-term strategic planning. Chair Atkins has framed the proposal as a flexibility measure, not a deregulation mandate, and it includes Regulation S-X simplification alongside the cadence change.

The investor protection counterarguments are equally specific. Longer reporting gaps increase information asymmetry, raise insider trading risk during extended windows, and weaken Regulation Fair Disclosure (Regulation FD) enforcement between filings. Retail investors, who lack the resources to conduct independent due diligence, lose a structured monitoring tool.

For investors wanting to understand how shareholder information rights operate in practice during periods of corporate deterioration, our deep-dive into the Lululemon proxy fight examines how a $17 billion equity value decline unfolded over five years of staggered board governance, including the specific disclosure gaps and failed accountability mechanisms that activist shareholders cited when seeking a leadership overhaul.

| Arguments for semiannual reporting | Arguments against |

|---|---|

| Reduces short-termism pressure on management | Widens information asymmetry between insiders and outside investors |

| Lowers compliance costs, especially for smaller filers | Creates longer windows for unreported deteriorating financials |

| Aligns with international reporting norms | Elevates insider trading risk during extended reporting gaps |

| 8-K material event filings still capture significant developments | Reduces retail investors’ ability to monitor company health |

The core investor concern is straightforward: 8-K filings cover specific triggering events, but they do not replace the comprehensive financial portrait that periodic reporting provides. The removal of structured periodic windows is the real policy question.

The SEC’s proposal does not emerge in a vacuum. Several major markets already operate on semiannual or hybrid models, and foreign private issuers listed on NYSE and Nasdaq already file semiannually, establishing an existing precedent within U.S. markets.

| Jurisdiction | Mandatory frequency | Key body | Notable feature |

|---|---|---|---|

| United Kingdom | Half-year plus annual | Financial Reporting Council (FRC) | No quarterly mandate on LSE |

| European Union | Half-year plus annual | Transparency Directive | Moved away from mandatory quarterly reporting in 2007 |

| Australia | Half-year plus annual | ASX | Quarterly cash flow updates mandatory for mining and resources companies |

| United States (current) | Quarterly plus annual | SEC | Most frequent mandatory reporting among major markets |

Proponents of the SEC proposal cite the EU’s 2007 shift as evidence that semiannual reporting need not increase market volatility. Australia’s hybrid model, combining mandatory semiannual financials with sector-specific quarterly cash flow disclosures, has been referenced as a potential template for an expanded U.S. 8-K framework.

The EU Transparency Directive 2013/50/EU formally removed mandatory quarterly reporting for listed companies across EU member states, establishing the legislative precedent that semiannual disclosure is compatible with liquid, well-functioning capital markets at scale.

The counterargument is structural. The U.S. retail investor base is larger and more directly engaged with individual company earnings than in most international comparators. The comparison is useful context, but it is not a clean policy translation.

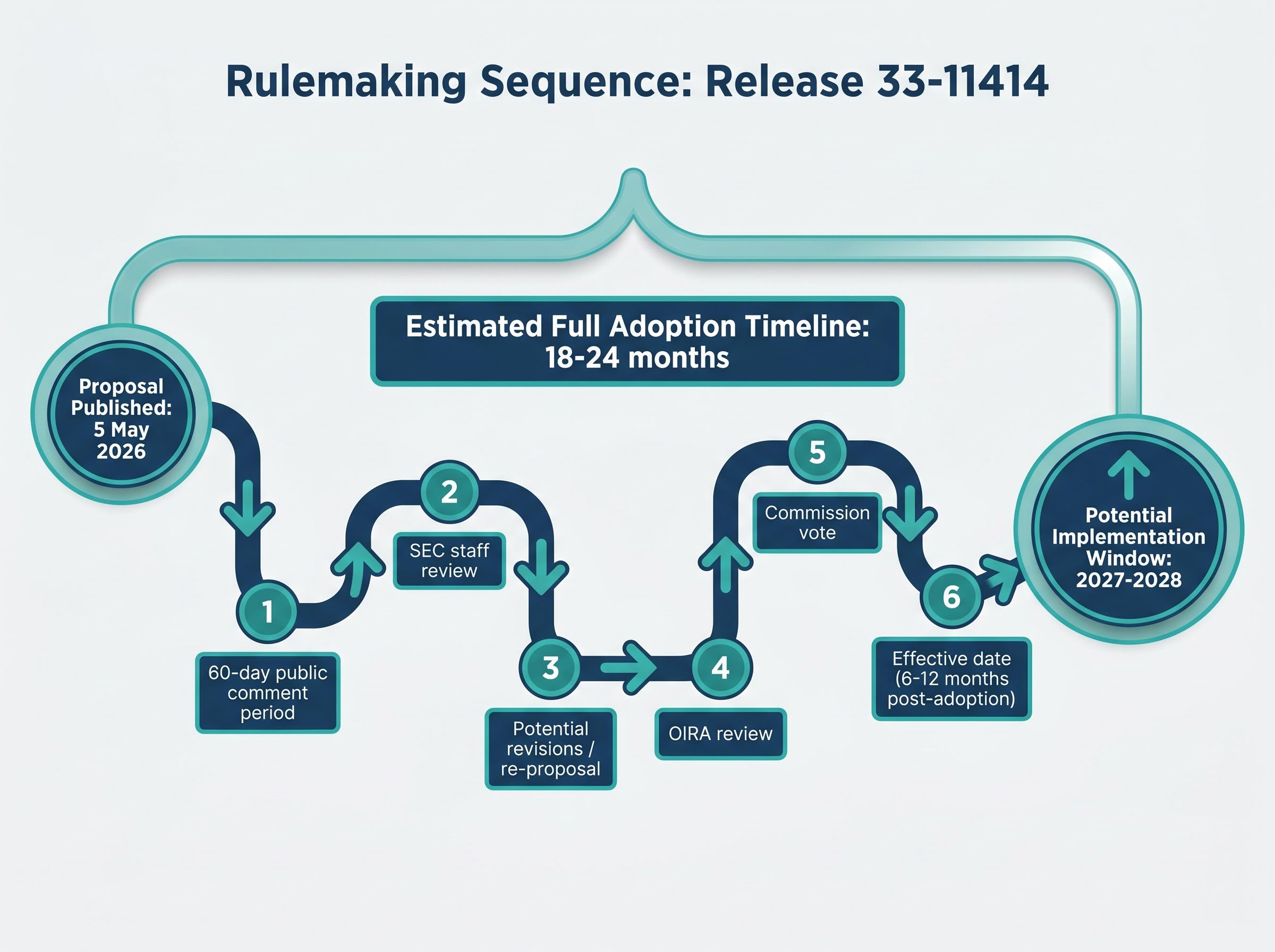

The proposal is live, but the distance between a proposal and a final rule is measured in years, not months.

The public comment period runs for 60 days from the date of publication in the Federal Register. The exact closing date depends on when the Federal Register formally publishes release 33-11414; readers should verify the confirmed date directly through the SEC docket rather than relying on third-party estimates.

The rulemaking sequence from here follows a defined path:

Chair Atkins noted that OIRA clearance was obtained prior to the proposal’s release. A realistic full adoption timeline runs 18-24 months from the proposal date, placing potential implementation in the 2027-2028 window, though this projection depends on comment volume and political priorities.

Readers tracking this proposal should verify the confirmed Federal Register publication date and comment deadline through the SEC docket at sec.gov.

Specific signals worth monitoring during the comment period include the volume and sourcing of institutional investor opposition, whether Congress signals support or resistance, and whether any companies publicly pre-commit to opting in or out.

The proposal is serious, the case for change is coherent, and the opposition is substantive. What it is not, yet, is a rule. No company can lawfully opt into semiannual reporting until the full rulemaking cycle concludes, a process that could take until 2027 or 2028 and could result in material revisions to the proposal as published.

The core investor decision framework remains unchanged from yesterday’s filing: 8-K event disclosure stays mandatory, but the removal of structured periodic financial windows is the real transparency question. The comment period is not a spectator process. It is a direct channel to influence the final rule’s shape.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements regarding the proposal’s projected timeline and potential adoption are speculative and subject to change based on regulatory developments and political priorities.

The SEC proposed on 5 May 2026 to allow eligible U.S. public companies to replace their quarterly Form 10-Q filings with a new semiannual Form 10-S, reducing mandatory periodic filings from four per year to two while keeping annual 10-K and material event 8-K requirements unchanged.

Any domestic public company subject to Exchange Act reporting under Sections 13(a) or 15(d) that currently files Form 10-Q is eligible, including large accelerated filers, accelerated filers, non-accelerated filers, emerging growth companies, and smaller reporting companies, with no size or revenue threshold required.

A company reverts to quarterly reporting simply by leaving the semiannual election checkbox unmarked on its next annual Form 10-K, with no advance notice required, though any change only takes effect at the start of the following fiscal year.

A realistic full adoption timeline runs 18-24 months from the 5 May 2026 proposal date, placing potential implementation in the 2027-2028 window, subject to comment volume, possible revisions, and political priorities.

The United Kingdom, European Union, and Australia all operate on semiannual plus annual reporting frameworks, with the EU formally removing mandatory quarterly reporting in 2007 under its Transparency Directive, making the U.S. currently the most frequent mandatory reporter among major markets.