What JEPI Actually Is and Whether It Fits Your Portfolio

3 hrs ago

JP Morgan’s entry into the FLEX options space with ROCQ and ROCY signals that the category has matured enough for the largest issuers to compete on tax structure rather than yield alone. That is a net positive for investors. Expense ratio compression, with ROCQ and ROCY at 0.35% versus the category average near 60-70 basis points, is an early competitive signal that this space may follow the same fee trajectory that compressed costs across passive equity ETFs over the past decade.

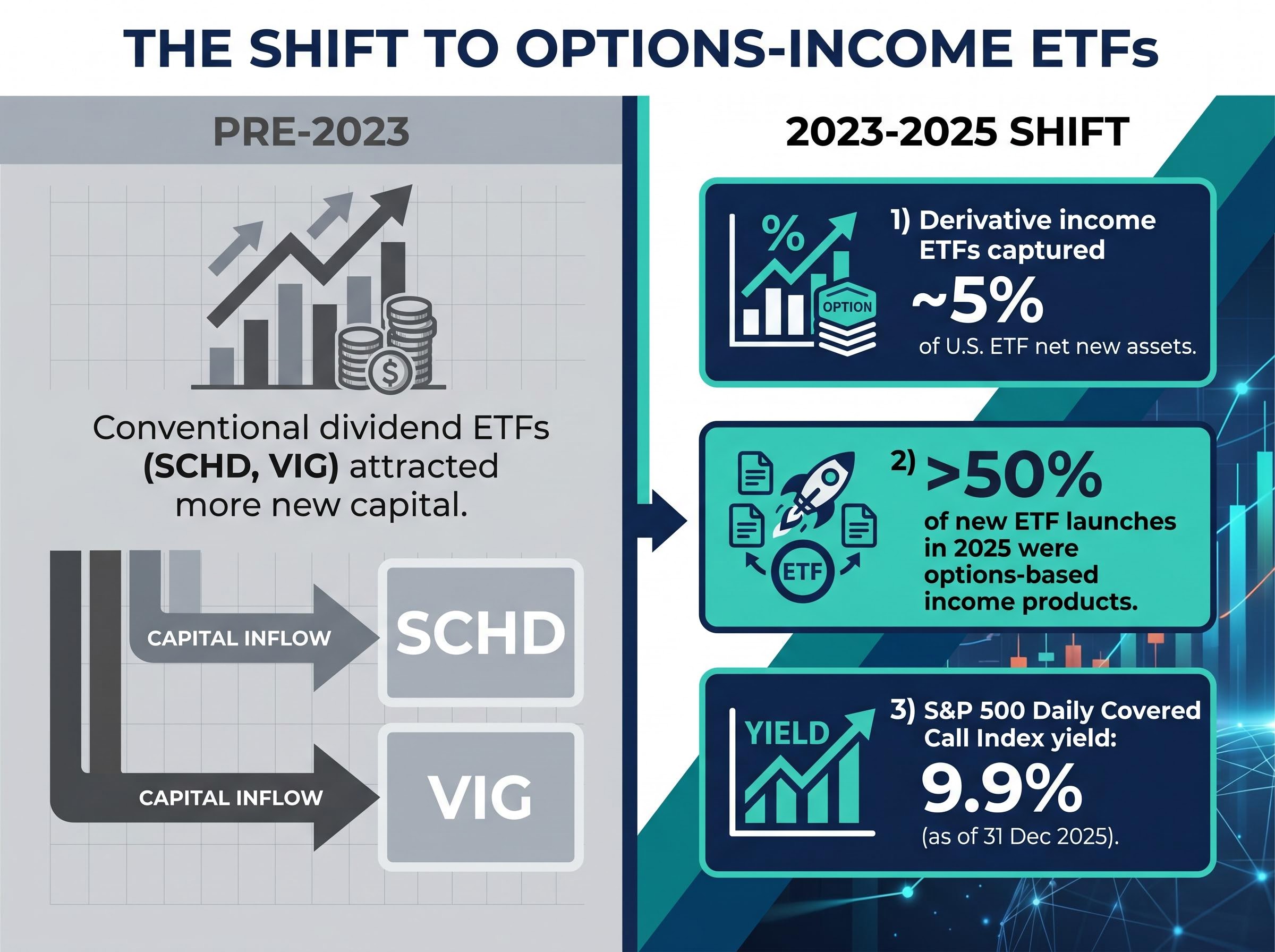

In 2025, more than half of all newly launched ETFs were options-based income products. Not growth funds. Not bond funds. Not traditional dividend vehicles. That single statistic, drawn from JP Morgan research, captures a structural shift in how American retail investors are pursuing income. Since 2023, derivative income ETFs have displaced traditional dividend stalwarts in net new asset flows, and the forces driving that shift are real. So are the trade-offs buried inside the products investors are buying. Not all covered call ETFs are built the same way, and the differences between them carry meaningful tax consequences that headline yield figures never reveal. What follows explains what is driving the trend, how the two dominant structural approaches actually work, what each means for a 1099-DIV at tax time, and how to think about choosing between them for a taxable account.

Before 2023, conventional dividend ETFs like SCHD and VIG attracted more new capital than options-based products in most calendar years. That pattern reversed sharply beginning in 2023, when derivative income ETFs accounted for approximately 5% of U.S. ETF net new assets, a trend that continued through 2024 and 2025.

The reversal was not random. Three conditions converged at the same time:

More than 50% of all new ETF launches in 2025 were categorised as derivative or options income-focused products, according to JP Morgan research attributed to Hamilton Reiner.

The S&P 500 Daily Covered Call Index posted an annualised yield of 9.9% as of 31 December 2025. That figure, roughly three times the yield of a traditional dividend growth fund, explains the gravitational pull. The primary buyers of these products are retail investors, not institutional participants, which means the trend is being driven by individual portfolio decisions rather than by allocators with multi-year mandates.

Understanding whether this represents a durable structural shift or a rate-environment-specific trade matters for how much weight to place on these products over a full market cycle.

The signal an investor sees is a high monthly distribution, often 8-10% annualised. The mechanism that produces it follows a three-step sequence:

Income sources in these funds are three-layered: equity dividends from the underlying holdings, realised capital gains from portfolio turnover, and options premium. In funds like ROCQ and ROCY, at least 80% of fund assets are invested in equity securities of the respective index, with options exposure capped at no more than 20% of fund assets.

The trade-off is direct. When the underlying index rises sharply in a single month, these funds will underperform a plain index fund because gains above the call strike price are forfeited. The call option the fund sold gives the buyer the right to those gains. The fund keeps the premium; the buyer keeps the upside. That exchange is not a flaw in the product. It is the product.

The same call-writing overlay logic that underpins ROCQ and ROCY has also been applied to leveraged structures: leveraged covered call ETFs combine 1.25x equity exposure with a covered call overlay to produce a portfolio delta near 0.92, targeting yields above 13% while retaining close to full participation in underlying index moves during moderate market conditions.

Newer funds use a more sophisticated variant called a call spread. The fund sells an out-of-the-money call at a lower strike price, then buys a further out-of-the-money call at a higher strike price. The net credit (the difference in premium between the two options) is the income generated.

This structure limits the fund’s potential loss from the options position. If the index surges well past both strikes, the purchased call offsets the liability from the sold call. FLEX options, which are customised, exchange-traded, and cleared through the Cboe, allow non-standard expiration dates and strike prices, giving fund managers more precision in constructing these spreads. This is why newer JP Morgan and NEOS products favour the call spread approach over simple covered call writing.

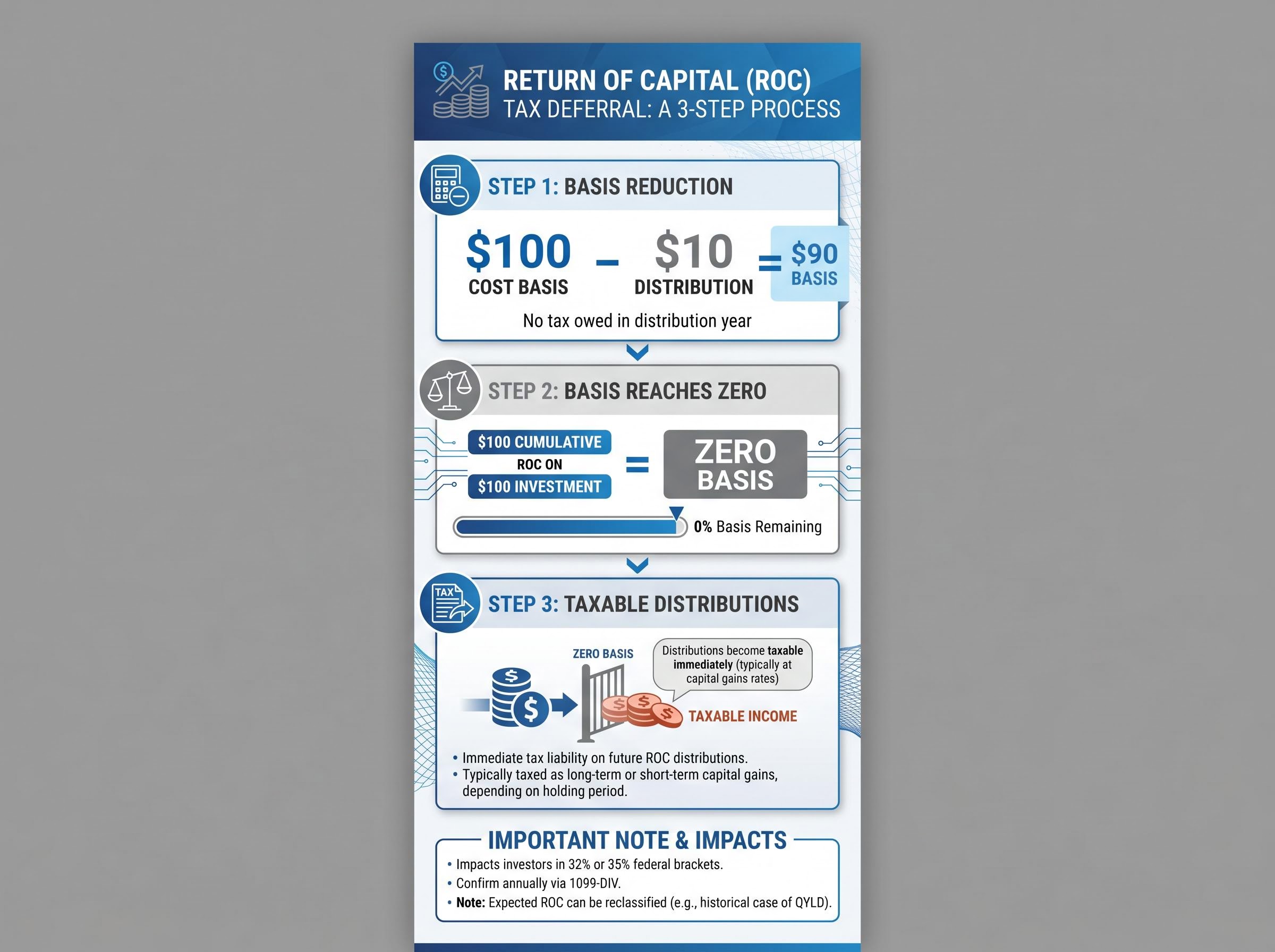

Return of capital does not mean a distribution is tax-free. It means taxation is deferred. The deferral works through a specific sequence that unfolds over the life of the holding.

The IRS guidance on return of capital distributions confirms that ROC payments reduce a shareholder’s cost basis in the fund rather than constituting taxable income in the year received, with the deferred tax liability crystallising only upon sale of the shares or once the basis reaches zero.

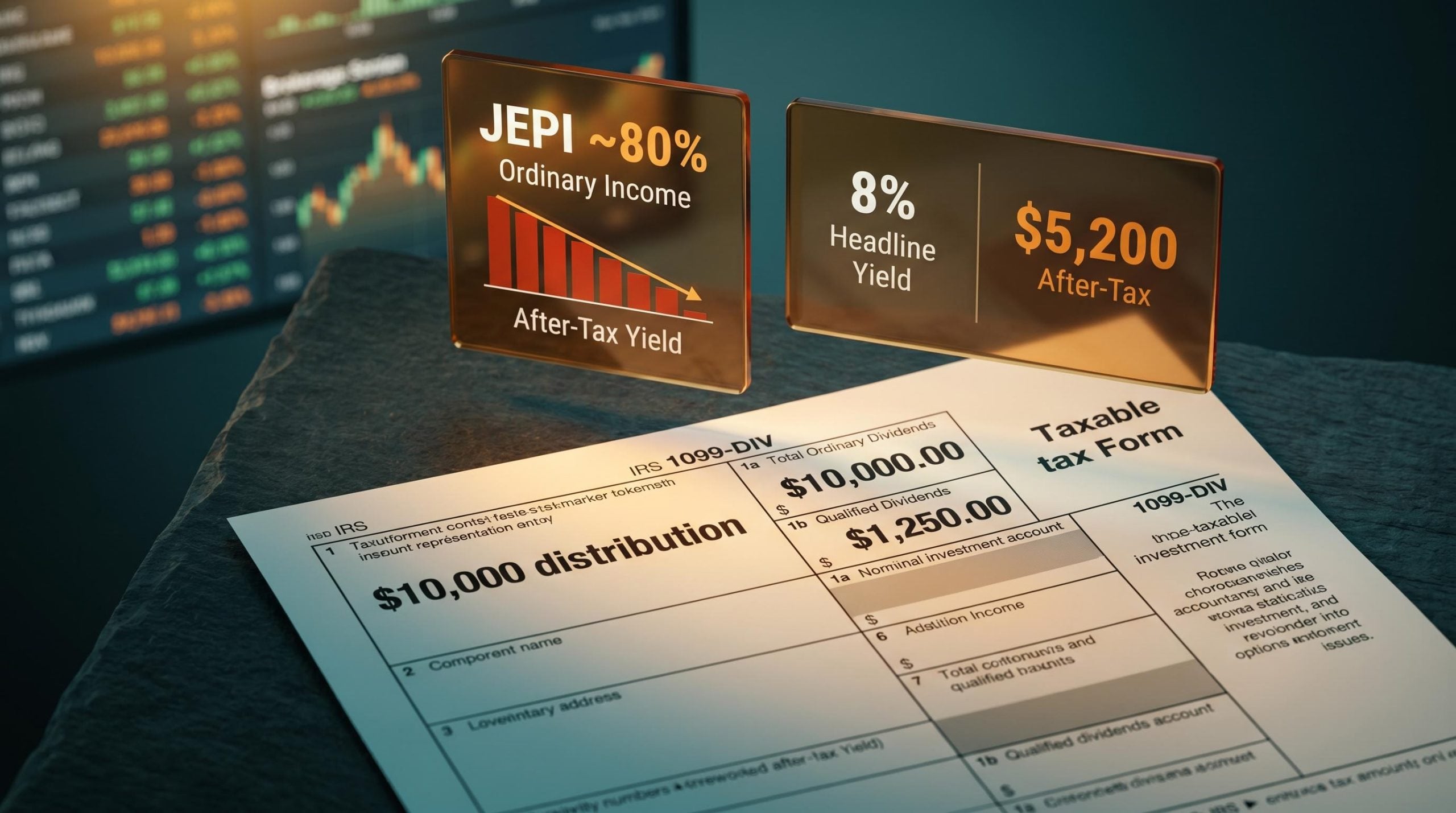

When shares are eventually sold, the lower cost basis results in a larger taxable gain. However, FLEX options-based distributions may ultimately be taxed at long-term capital gains rates, which are more favourable than ordinary income rates for most investors. For an investor in the 32% or 35% federal bracket, the difference between paying ordinary income tax on each distribution versus deferring and eventually paying at long-term capital gains rates can represent hundreds or thousands of dollars annually in after-tax return.

The ROC classification is confirmed annually via the 1099-DIV and is not guaranteed to persist. QYLD serves as a historical case where expected ROC treatment was subsequently reclassified, a reminder that tax character can shift based on fund-level accounting and portfolio activity in any given year.

For investors holding FLEX options-based funds in taxable accounts, monitoring the annual 1099-DIV tax character breakdown is not optional. It is the only way to confirm whether the expected deferral advantage is actually being delivered.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Two architecturally distinct approaches dominate the options-based income ETF space, and the choice between them determines the tax character of every distribution an investor receives.

Equity-linked notes (ELNs) are the mechanism used by JEPI and JEPIQ. Rather than holding options directly, these funds use structured notes whose returns are linked to options performance. The notes generate income that flows through to shareholders as ordinary income on their 1099-DIV. According to JP Morgan fund prospectus data, JEPI distributions are predominantly ordinary income rather than qualified income.

FLEX options are the mechanism used by SPYI, QQQI, GPIQ, ROCQ, and ROCY. These funds hold and exercise exchange-traded customisable options directly, which creates the conditions for distributions to be classified as return of capital (ROC) rather than ordinary income.

JP Morgan’s launch of ROCQ and ROCY in March 2026 was a deliberate product gap fill. Hamilton Reiner, the same portfolio manager responsible for JEPI and JEPIQ, now manages both new funds, giving taxable-account investors a FLEX options alternative within the JP Morgan lineup. Both launched with a 0.35% expense ratio, estimated at roughly half the typical covered call ETF expense ratio of approximately 60-70 basis points. JEPQ held approximately $34.81 billion in assets under management as of early 2026, making it the largest fund among the covered call ETFs in this comparison.

| Fund examples | Options vehicle | Primary distribution character | Expense ratio |

|---|---|---|---|

| JEPI, JEPIQ | Equity-linked notes (ELNs) | ~90% ordinary income | ~0.35% |

| SPYI, QQQI, GPIQ, ROCQ, ROCY | FLEX options (exchange-traded) | Return of capital (ROC) | 0.35%-0.68% |

The structural choice between ELNs and FLEX options is invisible in a fund’s ticker and marketing materials but directly determines how distributions appear on a 1099-DIV.

ETF creation and redemption mechanics give fund issuers a structural tool that mutual funds lack: the ability to swap securities in-kind with authorised participants, which delays the realisation of taxable gains and contributes to the broadly more tax-efficient profile of ETF wrappers relative to comparable managed funds.

Account type is the first question, not yield. In tax-advantaged accounts (Roth IRA, 401k), the ELN versus FLEX distinction is largely irrelevant because distributions are not currently taxable. Yield and total return become the dominant criteria.

For taxable accounts, the decision framework rests on three variables:

ROCQ carries a projected annual distribution yield of approximately 10%, consistent with comparable Nasdaq-focused funds including GPIQ and JEPIQ. ROCY carries a projected yield of approximately 8%, based on comparison with GPIX. Both carry a 0.35% expense ratio, roughly half the category average. JEPQ’s nearly $34.81 billion in assets reflects the depth of investor commitment to the ELN structure despite its less favourable tax profile, a reminder that yield and brand familiarity carry significant weight in investor decision-making.

Neither ROCQ nor ROCY has recorded actual distributions as of May 2026. Waiting for at least one full year of 1099 data before committing significant capital is a reasonable threshold.

Selling an existing position on tax grounds alone may be counterproductive. The tax drag from realising gains on a sale could outweigh the future tax benefit of switching to a FLEX structure, particularly for investors with significant unrealised gains.

A more disciplined transition path is tax loss harvesting: using market downturns to sell positions at a loss, then rotating into ROCQ or ROCY with no immediate tax cost. Given that neither fund has sufficient track record as of May 2026 to confirm consistent ROC treatment, a full immediate transition is premature for most investors.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The proliferation of options-based ETF launches is a response to demonstrated retail demand, not a signal that these products are uniformly suitable. Each new launch requires the same structural evaluation: how does it generate income, how are those distributions classified for tax purposes, and what does it cost?

JP Morgan’s entry into the FLEX options space with ROCQ and ROCY signals that the category has matured enough for the largest issuers to compete on tax structure rather than yield alone. That is a net positive for investors. Expense ratio compression, with ROCQ and ROCY at 0.35% versus the category average near 60-70 basis points, is an early competitive signal that this space may follow the same fee trajectory that compressed costs across passive equity ETFs over the past decade.

The primary buyer base remains retail investors, not institutional, which means marketing claims will continue to outpace structural transparency in many new launches. Every new options-income ETF should be evaluated against three structural questions:

Investors who can answer those three questions are positioned to evaluate any new product on its mechanics rather than defaulting to yield comparisons.

For taxable-account investors, the architectural choice between ELN and FLEX options structures has a larger impact on after-tax returns than headline yield differences of 1-2%. The practical hierarchy is straightforward: account type first, structural tax treatment second, yield and expense ratio third.

ROCQ and ROCY represent a meaningful new option for investors who want JP Morgan’s risk management discipline with a more tax-efficient structure. However, a full evaluation requires at least one year of actual distribution data to confirm that the ROC classification holds across varying market conditions.

The most productive next step is to review current covered call ETF holdings against the structural framework outlined above and to consult the fund’s most recent 1099-DIV tax character breakdown before drawing conclusions about after-tax yield. The yield number is what sells these products. The structure is what determines whether they actually deliver.

For investors who want to understand how product structure drives risk before committing capital to any income ETF, our deep-dive into leveraged ETF reset mechanics explains why the reset period is the single most consequential structural variable in the category, covering how daily-reset compounding differs from embedded leverage and what each means for long-hold investors.

These statements are speculative and subject to change based on market developments and company performance.

—

A covered call ETF holds a portfolio of equities and sells call options against those holdings to collect premium, which is then distributed to shareholders as monthly income, typically yielding 8-10% annualised. The trade-off is that the fund forfeits gains above the call strike price when the underlying index rises sharply.

Return of capital means a distribution reduces your cost basis in the fund rather than being taxed as income in the year received, deferring the tax liability until you sell the shares or your basis reaches zero. For investors in high tax brackets, this deferral can save hundreds or thousands of dollars annually compared to paying ordinary income tax on each distribution.

FLEX options funds hold exchange-traded customisable options directly, which creates conditions for distributions to be classified as return of capital on your 1099-DIV, while equity-linked note (ELN) funds like JEPI use structured notes whose income flows through as ordinary income. This structural difference is invisible in a fund's ticker but directly determines how much tax you owe each year on distributions.

Selling an existing position purely for tax reasons can be counterproductive if you have significant unrealised gains, as the tax cost of selling may outweigh future tax savings. A more disciplined approach is to use tax loss harvesting during market downturns to rotate into ROCQ or ROCY with no immediate tax cost.

Three structural questions matter most: whether the fund uses an ELN or FLEX options structure, whether at least one full year of 1099 data has confirmed the expected return of capital treatment, and how its expense ratio compares to structurally similar products. Yield figures alone are not sufficient to evaluate after-tax returns.