AMD and SMCI Earnings Confirm AI Demand, but Nvidia Holds the Key

4 hrs ago

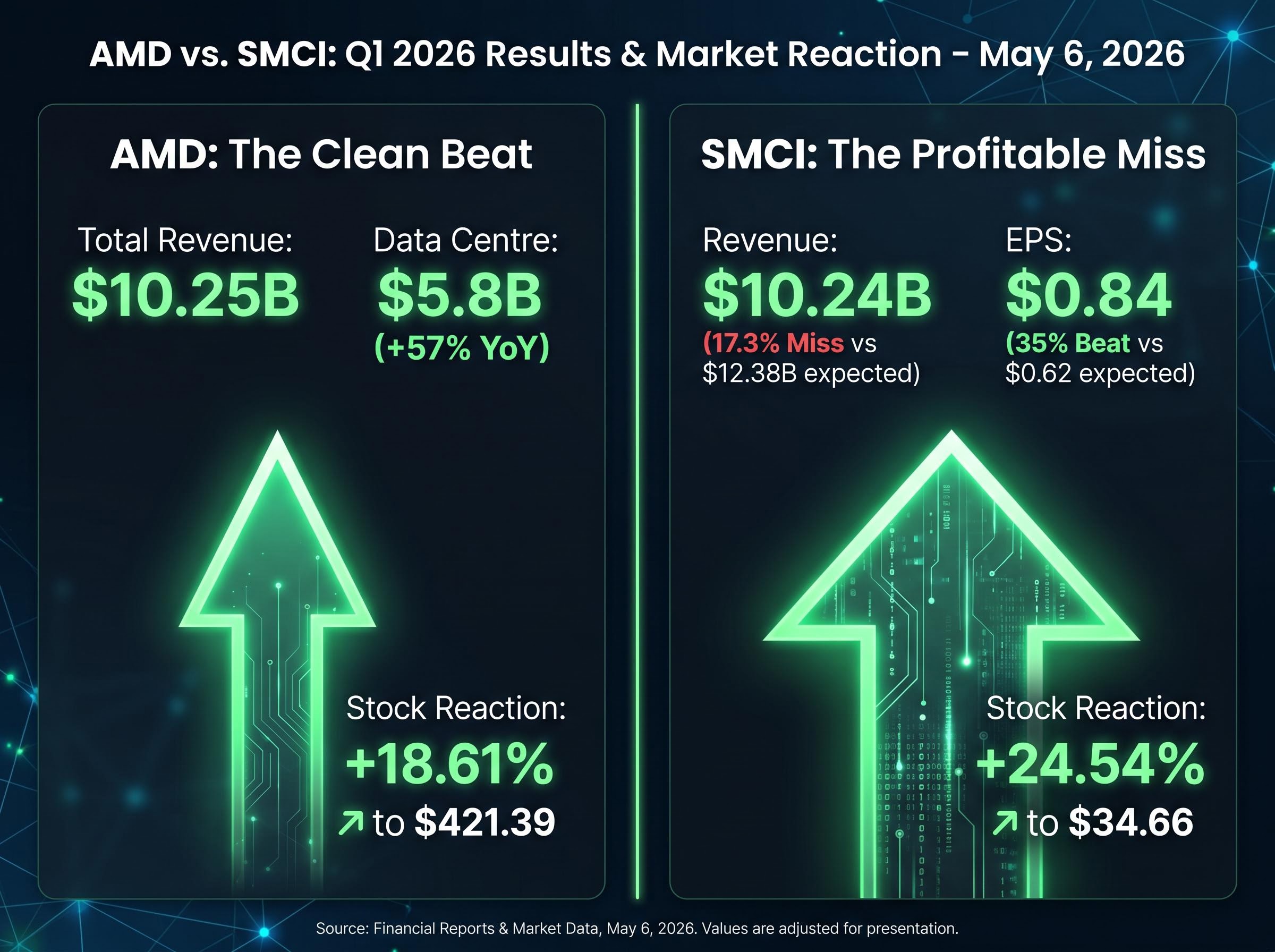

AMD shares surged nearly 19% and Super Micro Computer jumped over 24% in a single session on 6 May 2026, two of the sharpest single-day moves in the AI sector this year. One of those companies beat expectations cleanly. The other missed its revenue target by more than 17%.

The rally that unfolded across 6-7 May is not simply a story about strong earnings. It is a story about what markets chose to reward, what they chose to forgive, and what that selective optimism reveals about the conviction, and the fragility, baked into AI-sector valuations heading into the second half of 2026. This analysis unpacks what the AMD and Super Micro results actually showed, why the market reacted the way it did, and what investors need to weigh before concluding that the rally has durable legs.

AMD reported Q1 2026 total revenue of $10.25 billion with adjusted earnings per share of $1.37. The data centre segment delivered $5.8 billion, up 57% year-over-year, driven by EPYC processor demand and accelerating AI infrastructure spending. Management guided Q2 2026 revenue to approximately $11.2 billion, signalling continued momentum.

Super Micro Computer told a different story. Revenue came in at $10.24 billion against a consensus estimate of $12.38 billion, a miss of approximately 17.3%. Yet the company’s adjusted EPS of $0.84 beat the $0.62 consensus by 35% on the bottom line.

| Company | Key Metric | Expected | Actual | Result |

|---|---|---|---|---|

| SMCI | Revenue | $12.38B | $10.24B | Miss (–17.3%) |

| SMCI | EPS | $0.62 | $0.84 | Beat (+35%) |

| AMD | Total Revenue | — | $10.25B | Strong |

| AMD | Data Centre Revenue | — | $5.8B (+57% YoY) | Strong |

| AMD | Q2 2026 Guidance | — | ~$11.2B | Bullish |

The stock moves reflected a market that treated the two results as a single, bullish event:

A rally built on a clean AMD beat and a mixed SMCI result is a structurally different signal than a uniform sector sweep. That distinction matters for what comes next.

SMCI‘s 17.3% revenue shortfall would, in most quarters, send a stock sharply lower. Instead, the 24.5% surge reflected a market that had already priced in a high threshold for disappointment on the top line and was waiting for any signal that profitability remained intact.

That signal arrived in the form of the $0.84 EPS print, 35% above the $0.62 consensus. Investors read the result as evidence that Super Micro could convert AI-related demand into earnings even when revenue delivery lagged, and that forward guidance supported a recovery trajectory. In an environment where expectations had been compressed by prior volatility, even mixed results triggered outsized buying.

Capital.com analyst Kyle Rodda characterised the broader AI-driven sentiment as having “re-emerged” and being grounded in “fundamental earnings performance rather than speculation alone.”

The logic is coherent in the short term. Whether it is sound over a longer horizon is a separate question. A market that forgives large revenue misses on profitability grounds may be underpricing execution risk, particularly if SMCI‘s top-line shortfall reflects supply chain constraints or demand timing issues that persist into future quarters. The reaction function tells investors something specific about the current AI trade: confidence in the long-run demand thesis is strong enough that profitability trajectory matters more to participants than near-term revenue delivery.

AMD‘s data centre segment is the single most important number in the 6-7 May earnings cycle for reading the AI infrastructure thesis. $5.8 billion in quarterly revenue, growing at 57% year-over-year, provides concrete evidence that AI infrastructure spending is accelerating rather than plateauing.

Three data points constitute the core of the infrastructure demand case:

According to Capital.com, S&P 500 earnings growth is approaching 30% for the current quarter, led by large-cap technology. That figure contextualises AMD‘s results within a broader earnings environment where AI-exposed companies are carrying a disproportionate share of index-level growth.

The infrastructure thesis is not speculative at this stage. It is supported by revenue delivery. The question investors face is whether the growth rates being priced into forward valuations can be sustained as the initial infrastructure buildout matures and comparisons become harder in subsequent quarters.

Concentration risk describes what happens when a small number of large-cap technology companies drive a disproportionate share of index returns and earnings growth. When index-level gains depend heavily on a narrow group of names, the performance of a broad market portfolio becomes tightly linked to the fortunes of those specific companies, even if an investor holds hundreds of stocks through an index fund.

The S&P 500 closed near 7,365 following a 1.46% prior-session gain, with the Nasdaq Composite near 25,839, up approximately 2.02%. Both figures are strong. Both are contingent on a narrow leadership group continuing to deliver.

Capital.com’s Kyle Rodda described current valuations as “less extended than they had been the prior year,” stopping short of characterising conditions as irrational but noting that concentration risk remains a factor.

It is worth noting that no major bearish revisions from large investment banks were identified in 6-7 May reporting. That absence is itself a data point: the sell-side has not yet moved to challenge the rally’s foundations.

“Less extended than last year” does not mean cheap. It means the multiple compression from 2025‘s peak has reduced but not eliminated valuation risk. Forward price-to-earnings ratios for AI-exposed names remain above long-term historical averages, even if they have pulled back from the extremes reached during the initial AI enthusiasm cycle. With S&P 500 earnings growth approaching 30%, the question is whether this pace is sustainable or whether it reflects a peak concentration of AI-driven outperformance that normalises in subsequent quarters, bringing valuations back under pressure.

The 6-7 May session gains were not solely AI-driven. The S&P 500 and Nasdaq Composite closing at all-time highs was also shaped by optimism around advancing U.S.-Iran peace negotiations, which created a dual tailwind alongside the earnings results.

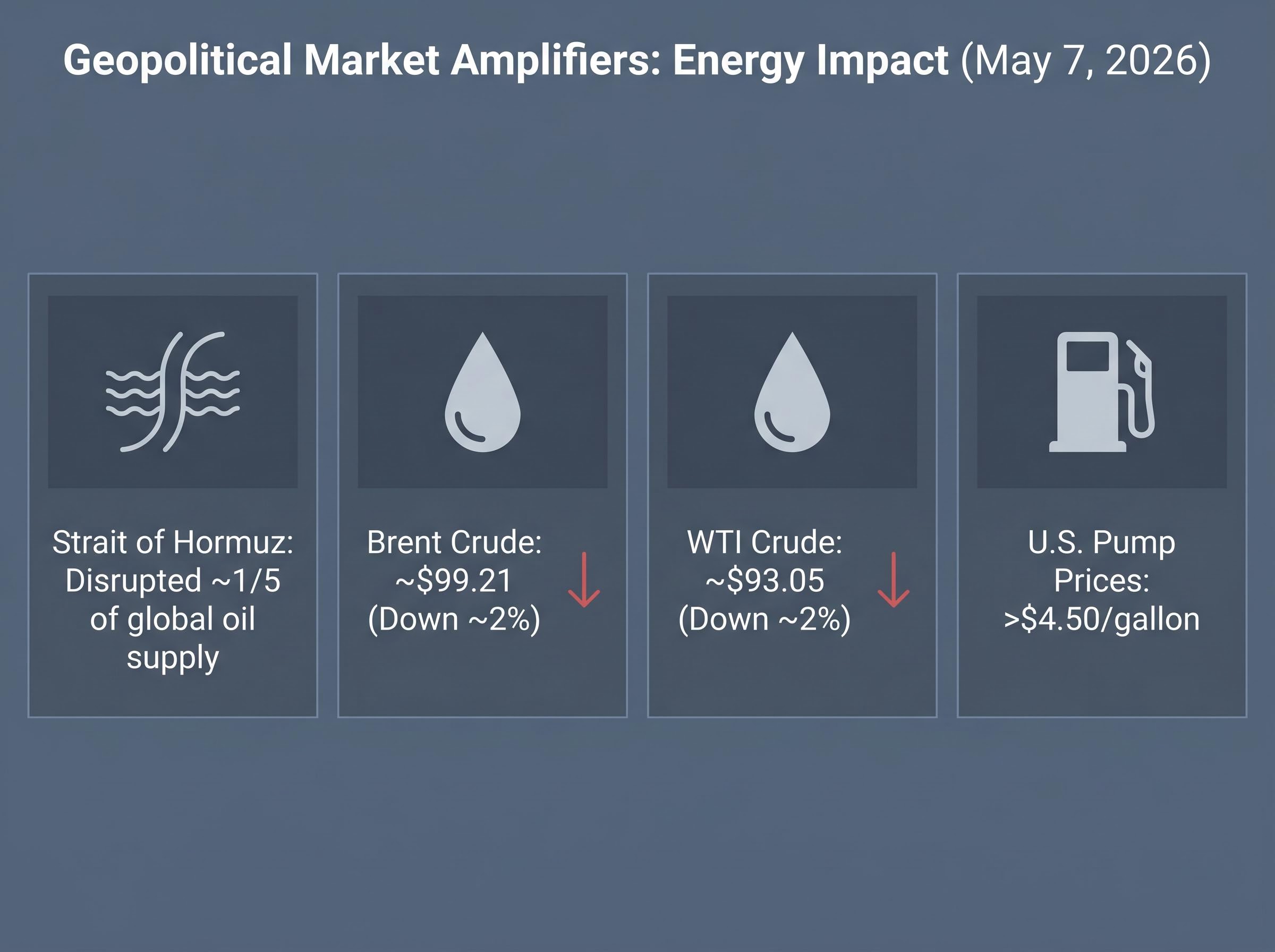

Washington and Tehran have been working through intermediaries on a preliminary framework, with formal talks anticipated in Pakistan and Iran’s response to mediators expected by 7 May. The Strait of Hormuz had been effectively closed for several weeks, disrupting roughly one-fifth of global oil supply and pushing energy costs higher across the economy.

Key macro data points for context:

A durable peace agreement could pull oil prices back further, reducing cost pressure on the broader economy and extending the risk-on environment. Investors need to disaggregate the two catalysts at work: the AI earnings signal reflects fundamentals, while the geopolitical relief reflects risk removal. Only one of those is reliably repeatable. If negotiations stall or collapse, the macro tailwind reverses, and the market’s task becomes determining whether the AI earnings case alone can sustain current index levels.

Two legitimate pillars support the 6-7 May rally. AMD‘s data centre results provide genuine fundamental evidence that AI infrastructure demand is converting into revenue and profitability at scale. Simultaneously, geopolitical relief from advancing U.S.-Iran negotiations removed a meaningful macro headwind that had been weighing on sentiment and energy costs.

The complications are equally present. SMCI‘s 17.3% revenue miss, and the market’s willingness to overlook it, raises questions about how much execution risk is being discounted. Earnings growth approaching 30% for the S&P 500 is concentrated in a narrow cohort of names, and the durability of that concentration has not been tested by a significant earnings disappointment from one of the leaders.

Three forward-looking signals will determine whether the current optimism is warranted in the months ahead:

The AI sector’s foundations are stronger than they were a year ago. The question is whether the market’s current pricing already reflects that improvement, or whether there is still room for the fundamentals to catch up to the enthusiasm.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Concentration risk in AI stocks refers to a situation where a small number of large-cap technology companies drive a disproportionate share of index returns and earnings growth. When an investor holds a broad index fund, their portfolio performance becomes tightly linked to the fortunes of those specific companies, even if hundreds of other stocks are included.

Super Micro's adjusted EPS of $0.84 beat the $0.62 consensus by 35%, signalling that the company could convert AI-related demand into earnings even when revenue delivery lagged. Investors interpreted the profitability beat and forward guidance as evidence of a recovery trajectory, which outweighed the top-line miss in the current market environment.

AMD reported data centre revenue of $5.8 billion, up 57% year-over-year, driven by EPYC processor demand and accelerating AI infrastructure adoption. Management guided Q2 2026 revenue to approximately $11.2 billion, reinforcing the view that AI infrastructure spending is accelerating rather than plateauing.

Advancing U.S.-Iran peace negotiations created a geopolitical tailwind alongside the earnings results by raising expectations that the Strait of Hormuz could reopen, which had been effectively closed for several weeks and was disrupting roughly one-fifth of global oil supply. Brent crude fell approximately 2% on 7 May, reducing cost pressure on the economy and amplifying the risk-on sentiment already driven by strong AI earnings.

The three key signals to monitor are whether AMD delivers on its Q2 2026 revenue guidance of approximately $11.2 billion, whether Super Micro's revenue recovers toward consensus expectations or the Q1 shortfall proves persistent, and whether a durable U.S.-Iran agreement causes oil prices to normalise and removes the geopolitical premium from the broader market.