Why a Rising AUD Is Quietly Eroding Your International ETF Returns

3 hrs ago

With AUD 44.2 billion sitting in a single Vanguard ETF and Australian investors funnelling record amounts into index funds, the question for 2026 is not whether to use ETFs but which ones actually suit a decade-long horizon. The ASX offers dozens of internationally focused exchange-traded funds, yet the differences between them matter more than most investors realise. A fund tracking 500 US companies and a fund spanning thousands of developed-market names serve different portfolio functions entirely.

Australian investors face a concentrated domestic market dominated by banks and miners, and a currency that can erode real returns over time. International ETFs listed on the ASX address both problems in a single trade, offering diversification across geographies, sectors, and currencies without the complexity of offshore accounts or foreign brokerage. What follows profiles three ASX-listed ETFs that long-term investors should understand in 2026: IVV, IXI, and VGS. Each is assessed on what the fund does, how it has performed, what it costs, and which investor profile it suits.

Australian equities represent roughly 2% of global market capitalisation. For investors holding only domestic shares, 98% of the world’s investable opportunity set sits outside the portfolio.

International ETF inflows reached $6.9 billion across the Australian market in Q1 2026 alone, the quarter in which international funds overtook domestic ETFs as the most purchased category on record, a structural reorientation driven by RBA rate divergence, a strengthening Australian dollar, and growing conviction around geographic diversification.

That concentration gap is compounded by sector imbalance. Financials and materials dominate the ASX, leaving Australian investors structurally underexposed to technology, healthcare, and consumer sectors at the scale available in US and European markets.

ASX-listed international ETFs offer the most friction-free solution. Three structural advantages stand out:

The ATO guidance on AMIT tax treatment specifies how CGT discounts are applied at the trust level and how trustees must report foreign capital gains alongside associated foreign tax paid, giving Australian investors the information needed to calculate foreign income tax offsets from international ETF distributions.

Over a 10-plus-year horizon, breadth and low costs compound more reliably than short-term tactical positioning. That is the selection lens applied to the three funds below.

One fund. 500 companies. A management expense ratio that rounds to almost nothing.

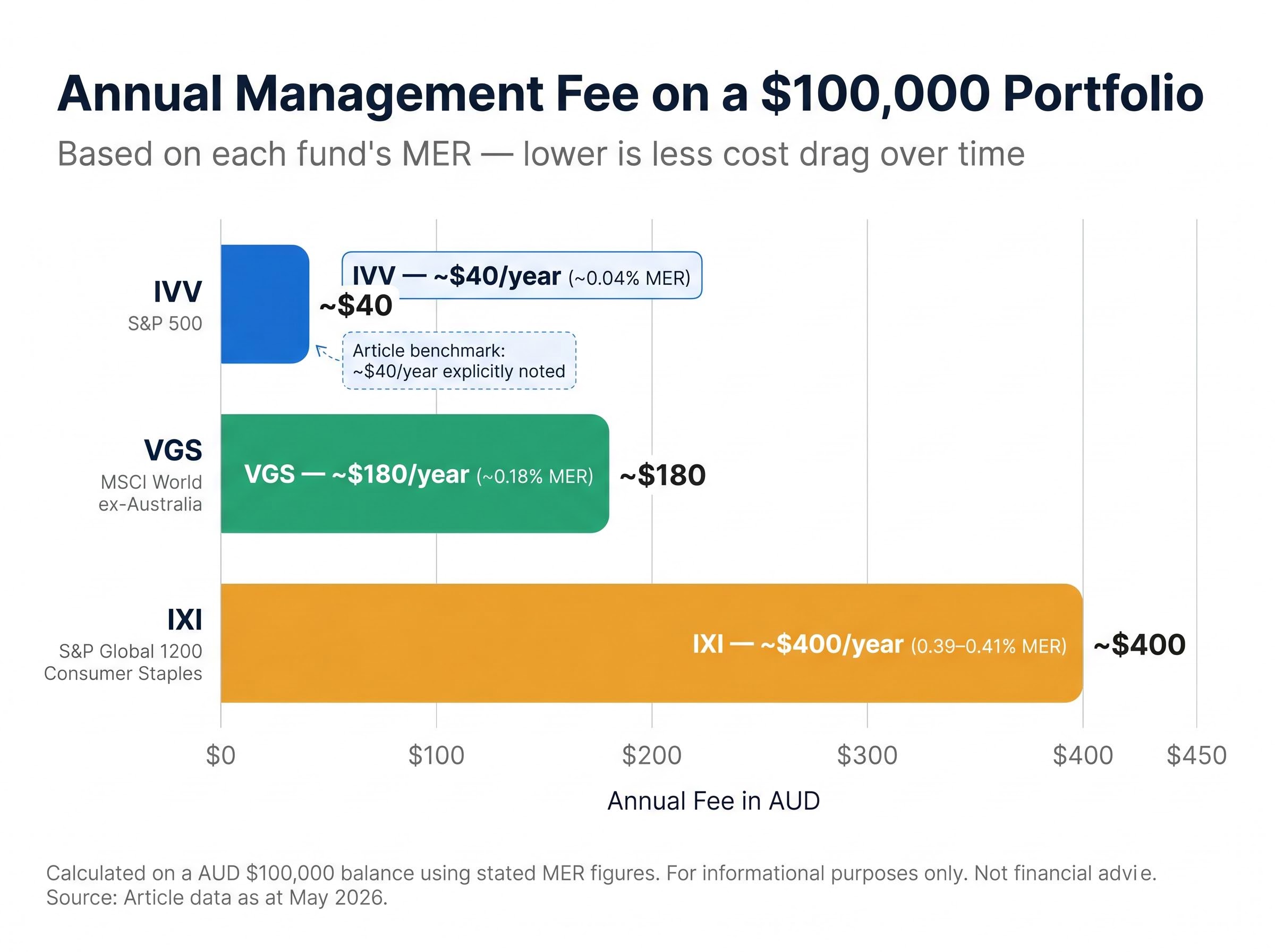

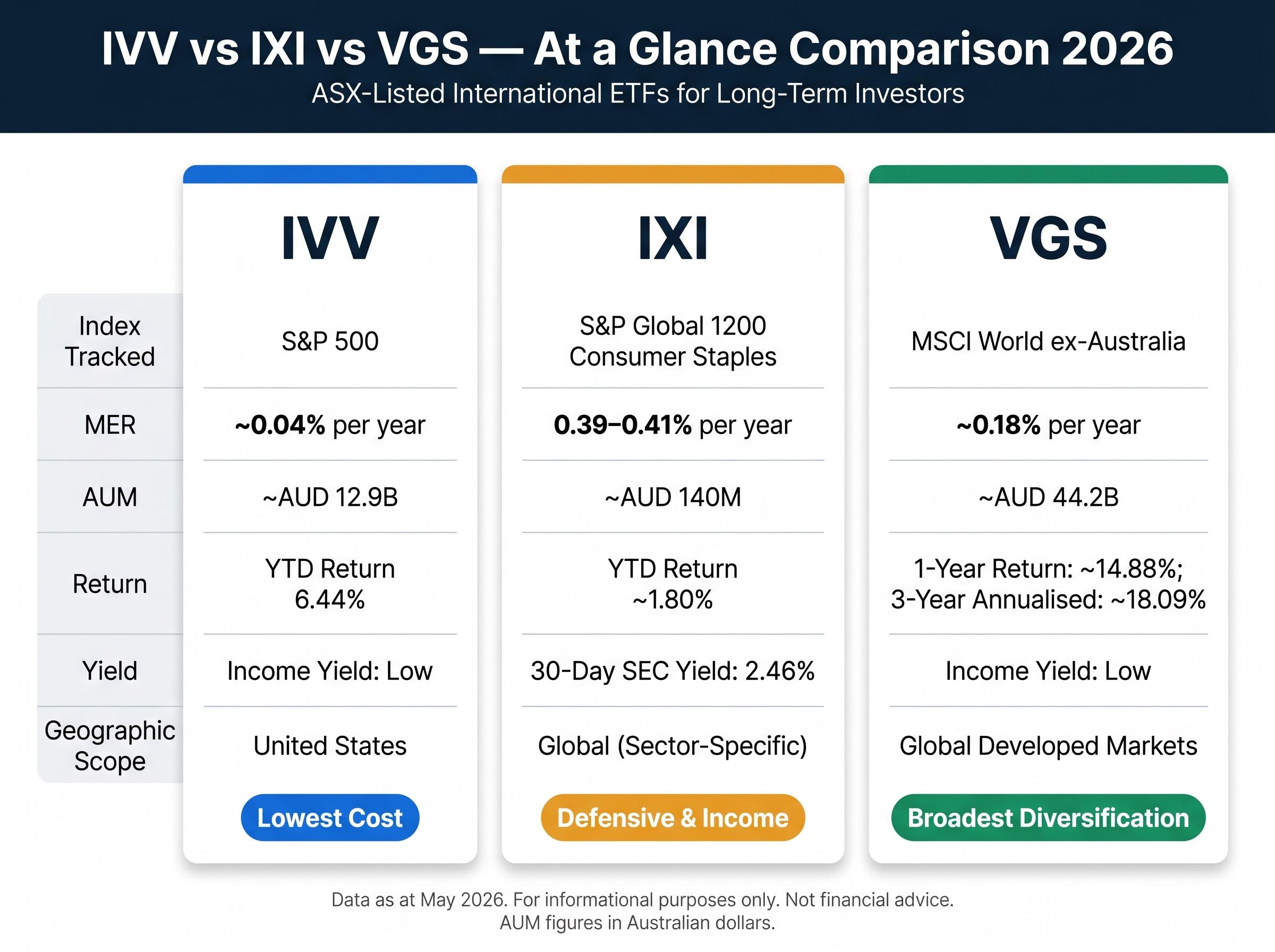

IVV tracks the S&P 500, the index of the 500 largest publicly listed US companies. Its appeal starts with cost: a MER of approximately 0.04% makes it among the cheapest equity ETFs available on the ASX.

On a $100,000 balance, a 0.04% MER equates to roughly $40 per year in management fees, a cost benchmark that few competing products match.

The fund is not purely a technology bet, despite popular perception. Its sector spread covers technology, healthcare, financials, consumer discretionary, and industrials. Holdings include Microsoft, Amazon, and Berkshire Hathaway, names that anchor the fund’s credibility, but the breadth across 500 constituents dilutes single-stock concentration risk considerably.

With AUM of approximately AUD 12.9 billion as of 5 May 2026, IVV carries the scale and liquidity that make it practical for regular contribution strategies such as dollar-cost averaging, where tight bid-ask spreads matter over time.

| Index Tracked | MER | AUM | YTD Return | Key Holdings |

|---|---|---|---|---|

| S&P 500 | ~0.04% | ~AUD 12.9B | 6.44% | Microsoft, Amazon, Berkshire Hathaway |

For Australian investors with no US equity exposure, IVV is the most cost-efficient starting point available on the ASX.

IXI exists for the moments when growth assets sell off and portfolios need a component that holds its ground. The fund tracks the S&P Global 1200 Consumer Staples Index, a collection of companies that sell food, beverages, household goods, and personal care products, items consumers purchase regardless of economic conditions.

That defensive profile came at a price in 2025. Investor rotation into AI-exposed technology names pulled capital away from consumer staples, and IXI underperformed the broader market. Its YTD return of approximately 1.80% as of 4 May 2026 reflects that lingering headwind.

The honest question is whether the underperformance creates opportunity. Three tailwinds have shifted the balance heading into the second half of 2026:

The fund’s top holdings include Costco (approximately 4-5%), Walmart (approximately 4%), PepsiCo (approximately 3-4%), Procter & Gamble, and Nestlé, businesses with global scale and resilient revenue streams. The 30-day SEC yield of 2.46% as of 31 March 2026 adds an income component that neither IVV nor VGS matches.

For investors weighing total return versus dividend income as a primary objective, backtested data from 2016 to 2025 shows a total market portfolio returning 10.49% annualised against 9.43% for a dividend-focused portfolio, a gap that compounds to roughly $116,000 in additional wealth on a $100,000 investment over 20 years and reframes the appeal of IXI’s 2.46% yield relative to the higher-growth alternatives.

| Index Tracked | MER | AUM | YTD Return | 30-Day Yield |

|---|---|---|---|---|

| S&P Global 1200 Consumer Staples | 0.39-0.41% | ~AUD 140M | ~1.80% | 2.46% |

IXI suits investors who want a counterweight to higher-growth holdings, particularly those managing sequence-of-returns risk over a long horizon where a single sharp drawdown can permanently impair compounding.

IVV goes deep into one market. VGS goes wide across many. The distinction matters more than most investors appreciate.

VGS tracks the MSCI World ex-Australia Index, covering developed markets across North America, Europe, and Japan. It holds US equities (overlapping with IVV to a degree), but distributes risk across thousands of international companies. The result is genuine geographic breadth rather than concentration in a single economy.

With AUM of approximately AUD 44.2 billion as of 31 March 2026, VGS is the largest fund in this comparison and one of the most widely held ETFs on the ASX, a measure of the conviction Australian investors have placed in it as a long-term core holding.

Currency diversification adds a second layer of risk management. VGS provides exposure to EUR, JPY, GBP, and USD simultaneously, reducing dependence on AUD and any single currency’s trajectory.

The fund’s top holdings, Apple, NVIDIA, and JPMorgan Chase, anchor its credibility, but VGS’s value lies in its breadth. A 1-year return of approximately 14.88% and a 3-year annualised return of approximately 18.09% reflect the compounding advantage of broad international exposure over a multi-year window.

| Index Tracked | MER | AUM | 1-Year Return | 3-Year Annualised |

|---|---|---|---|---|

| MSCI World ex-Australia | ~0.18% | ~AUD 44.2B | ~14.88% | ~18.09% |

For investors who want a single-fund international core without constructing a multi-ETF portfolio, VGS is the most straightforward option on the ASX. Its MER of 0.18% sits higher than IVV’s 0.04%, but the cost buys exposure across dozens of markets rather than one.

Three funds, three distinct functions. The strongest portfolios are assembled from deliberate choices about what gap each holding fills.

| Fund | Best Suited For | MER | Income Focus | Geographic Scope |

|---|---|---|---|---|

| IVV | Cost-sensitive investors wanting maximum US exposure | ~0.04% | Low | US only |

| IXI | Investors prioritising capital preservation and income | 0.39-0.41% | Moderate (2.46% yield) | Global (sector-specific) |

| VGS | Investors seeking a single-fund international core | ~0.18% | Low | Global developed markets |

IVV and VGS can overlap, since VGS holds US equities as part of its broader index. The difference is concentration preference: IVV is a pure US bet at the lowest possible cost, while VGS spreads that exposure across multiple developed economies. IXI sits independently as a sector allocation rather than a geographic one.

One consideration often missed: none of these three funds pass franking credits, since all invest internationally. Australian tax residents who rely on franked income from domestic equity holdings should factor this into their portfolio design.

Before selecting, three questions help clarify the decision:

The 50% CGT discount applies to units in all three funds when held for more than 12 months, reinforcing the structural advantage of a long holding period. The MER gap between IVV at 0.04% and VGS at 0.18% is modest in percentage terms but compounds meaningfully on large balances over decades.

ETF fee compounding over a 30-year horizon can produce a terminal wealth divergence of approximately $575,972 between two funds with fees separated by less than 1% per annum, which reframes the MER gap between IVV at 0.04% and VGS at 0.18% as a genuine long-term consideration rather than a negligible rounding difference.

Each of these funds serves a distinct long-term function: IVV for cost-efficient US growth exposure, IXI for defensive stability and income, and VGS for genuinely broad international diversification. That clarity of purpose has not changed with the market environment of 2026, where macro uncertainty and periodic volatility have reinforced rather than weakened the case for geographic breadth and sector diversification.

The investors best positioned for what comes next are those who define their holding period in decades and match fund selection to their actual portfolio gaps, rather than reacting to 12-month return tables. Recent performance is a data point, not a decision framework.

For readers wanting to model how these three funds fit within a broader compounding framework, our dedicated guide to long-term wealth accumulation walks through six evidence-based principles including equity return history since 1802, the dollar-gain acceleration in a portfolio’s second decade, and how tax-sheltered structures such as superannuation amplify every basis point of MER saved.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

IVV, IXI, and VGS are three standout ASX-listed ETFs for long-term investors: IVV offers low-cost S&P 500 exposure at a 0.04% MER, VGS provides broad developed-market diversification across dozens of countries at 0.18%, and IXI delivers defensive consumer staples exposure with a 2.46% yield.

IVV tracks the S&P 500 and concentrates exposure in the 500 largest US companies at a very low 0.04% MER, while VGS tracks the MSCI World ex-Australia Index and spreads risk across thousands of companies in North America, Europe, and Japan at a 0.18% MER.

ASX-listed international ETFs can be bought and sold through any standard Australian broker, settle in Australian dollars without manual currency conversion, and typically qualify for AMIT tax treatment, which provides access to the 50% CGT discount for units held longer than 12 months.

None of the three funds pass franking credits to investors because all three invest internationally rather than in Australian equities, which is an important consideration for Australian tax residents who rely on franked income from domestic holdings.

VGS carries a MER of approximately 0.18%, which is higher than IVV's 0.04% but buys exposure across dozens of developed markets rather than just the US; research cited in the article shows that fee differences of less than 1% per annum can produce a terminal wealth divergence of approximately $575,972 over a 30-year horizon.