Why Seeing Machines Trades Below 5p Despite EU Mandate Wins

3 hrs ago

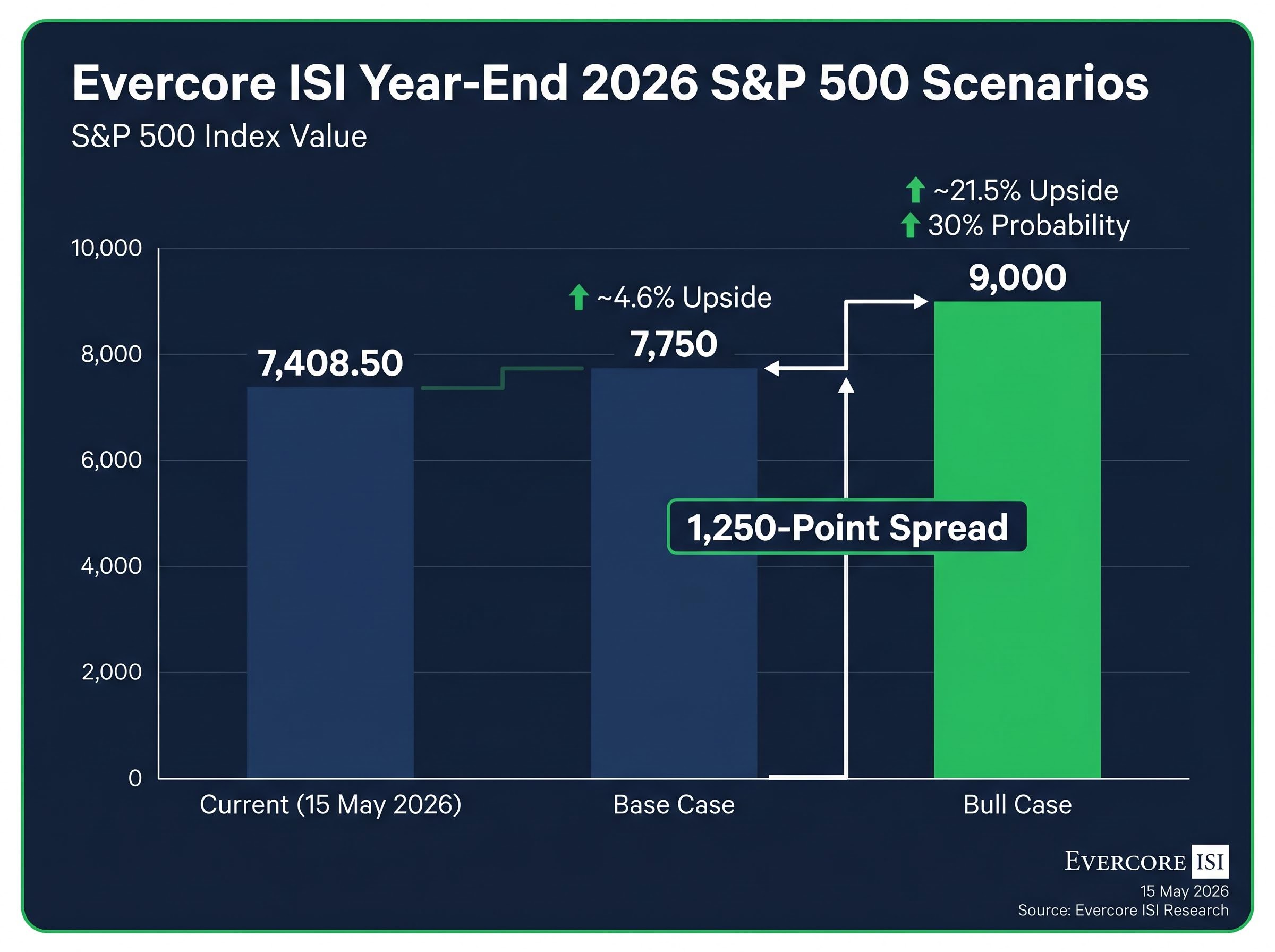

Julian Emanuel at Evercore ISI just assigned a 30% probability to the S&P 500 reaching 9,000 by year-end 2026. With the index closing at 7,408.50 on 15 May 2026, that implies 21.5% upside in roughly seven months.

Emanuel’s note, published 18 May 2026, arrives as Wall Street digests an unusual confluence of forces: AI-driven earnings momentum, a post-tariff market recovery, and growth outperforming value by nearly 7 percentage points in April alone. This is not a routine price-target revision. It frames the current environment as one where the distribution of possible outcomes is meaningfully wider than standard models anticipate, in both directions.

What follows breaks down the specific conditions Emanuel says must materialise for the 9,000 scenario to unfold, how Evercore recommends positioning for it, and what serious risks stand in the way.

The starting point is the gap between Evercore’s two scenarios. The base case targets 7,750 by year-end, representing approximately 4.6% upside from the 15 May close. The bull case targets 9,000, a 21.5% gain from the same level. The 1,250-point spread between those two numbers is not a rounding exercise; it represents a structurally different market regime if the upper scenario materialises.

Key figure: Julian Emanuel assigns a 30% probability to the S&P 500 reaching 9,000 by year-end 2026. That is not a remote tail scenario. It is a one-in-three chance, weighted toward three sectors: technology, communication services, and consumer discretionary.

The table below frames what each scenario requires from the current level.

| Scenario | S&P 500 Target | Implied Upside from 7,408 |

|---|---|---|

| Current Level (15 May 2026) | 7,408.50 | — |

| Base Case | 7,750 | ~4.6% |

| Bull Case | 9,000 | ~21.5% |

For investors calibrating equity exposure, understanding where the base case ends and the bull case begins is the first decision. Everything that follows hinges on whether the conditions supporting that upper target are credible.

The Q1 2026 earnings base that underpins Wall Street’s revised targets is unusually strong: the quarter delivered an 84% beat rate and blended EPS growth of 27.7% year-on-year, the highest quarterly result in four years, providing the fundamental floor from which any path to 9,000 must be measured.

Emanuel’s bull case rests on an analogy that is deliberately provocative. He draws a parallel to two periods of sustained equity expansion, the 1920s and the 1990s, and argues the present moment shares their defining features: a productivity disruption arriving at the same time as expansionary monetary conditions.

Three convergent forces underpin the thesis:

The first two created the conditions. The third, in Emanuel’s framework, is the catalyst that separates the current cycle from a standard post-stimulus recovery.

The distinction between AI investment’s GDP contribution and its eventual productivity payoff is central to evaluating this thesis: Q1 2026 data shows technology investment already adding approximately one percentage point to GDP growth, but official BEA methodology likely understates the true hardware contribution by 20-30% due to import accounting conventions.

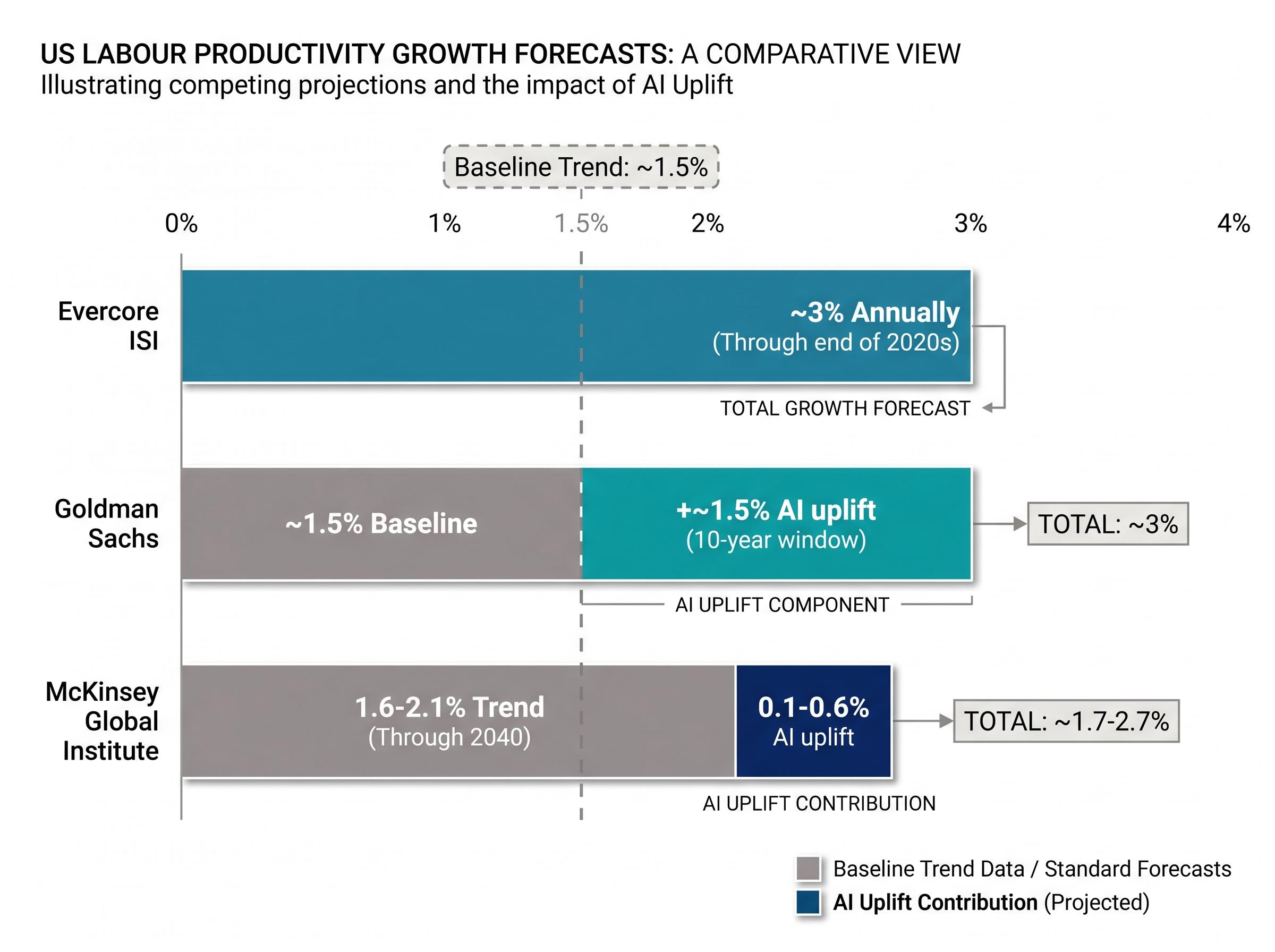

The structural anchor: Evercore ISI projects approximately 3% US labour productivity growth annually through the end of the 2020s. This single assumption is the load-bearing variable of the entire 9,000 case.

The melt-up dynamics in equity markets that Evercore’s bull case implicitly requires are not without institutional precedent: BCA Research independently identifies a scenario above 9,200 driven by the same self-reinforcing loop of AI earnings beats, institutional deployment, and retail capital deployment into leveraged semiconductor positions that powered April’s 8.70% single-month surge.

A 3% sustained rate would roughly double the baseline trend of approximately 1.5%. Goldman Sachs research provides the strongest institutional alignment with that magnitude, estimating AI could raise US labour productivity by approximately 1.5 percentage points annually over a 10-year adoption window. The implied arithmetic (a 1.5% baseline plus a 1.5 percentage point AI uplift) maps directly onto Evercore’s framework.

Goldman does not, however, explicitly endorse 3% through 2030 as a stated forecast. And McKinsey Global Institute arrives at a considerably more conservative estimate: generative AI adds only 0.1-0.6 percentage points to annual productivity growth through 2040, implying a trend of 1.6-2.1%. For 3% to materialise, AI adoption would need to diffuse well beyond mega-cap technology firms, sustained capital investment would need to persist, and regulatory disruption would need to remain minimal. All three conditions holding simultaneously is the bet.

Here is where the note takes an unexpected intellectual turn. Emanuel argues that the tools investors rely on to generate forecasts, including large language models and prediction markets, carry a structural bias he calls “Narrow Consensus.”

Evercore’s characterisation: Large language models and prediction markets alike tend to cluster around consensus estimates, systematically underweighting tail-end scenarios at both extremes of the distribution. Emanuel terms this “Narrow Consensus” bias.

The argument is that these tools reflect collective belief rather than predictive accuracy, particularly for outcomes that are continuous, long-dated, or skewed toward tail risks. Prediction markets, in Emanuel’s view, are good at capturing what the crowd expects but poor at pricing what the crowd has not yet imagined.

The implication cuts both ways. The same structural bias that makes 9,000 more plausible than conventional models suggest also raises the probability of a severe downside scenario. Emanuel does not present the wider distribution as a reason for optimism alone. He presents it as a reason the entire range of possible outcomes, up and down, deserves more weight than standard modelling provides.

For Evercore, lasting AI value will come from domain-specific expertise and end-to-end workflow ownership, not generalised AI capability. That distinction matters: it implies the winners of the AI cycle are not yet fully identified, which is itself a reason the outcome distribution is wider than most forecasters acknowledge.

The thesis shifts from argument to execution with a two-part trade structure designed for an environment where outcome dispersion is explicitly wider than normal:

The collar specifically targets two near-term risks Evercore flags as the most likely sources of interim volatility:

The logic of pairing asymmetric upside with a bounded hedge reflects a specific kind of conviction: Evercore’s team believes the destination may be significantly higher, but the road there will not be smooth. April’s market data reinforces the point. S&P 500 growth stocks outperformed value by approximately 7 percentage points that month (growth up roughly 9.5%, value up roughly 2.5%), suggesting capital is already rotating aggressively toward the AI-linked names that would drive the bull case.

A 30% probability on 9,000 means a 70% probability it does not happen. The counterarguments deserve the same specificity as the thesis.

The most contestable number in the forecast is the 3% productivity assumption. McKinsey’s framework provides the institutional benchmark for a more sober estimate:

McKinsey Global Institute projects generative AI adds 0.1-0.6 percentage points to annual productivity growth through 2040, implying a trend rate of 1.6-2.1%, well below Evercore’s 3% target.

The International Monetary Fund has characterised the AI productivity boost as real but highly uncertain in both size and timing, dependent on diffusion rates, the regulatory environment, and complementary capital investment. Neither institution endorses anything close to 3% through 2030.

The Penn Wharton Budget Model projections on AI productivity estimate that generative AI’s boost to annual productivity growth will peak at just 0.2 percentage points in 2032, a figure that sits well below both Evercore’s 3% target and even McKinsey’s more conservative range, underscoring how far consensus institutional forecasts sit from the assumption the bull case requires.

Three risk factors stand out:

Concentration risk in mega-cap AI names compounds the valuation concern: Goldman Sachs’s U.S. Equity Sentiment Indicator reached 1.7 in early May 2026, a reading historically associated with below-average S&P 500 returns over the following two to eight weeks, even as the same mega-cap technology cluster driving the bull case delivered 20% revenue growth and 61% profit growth in Q1.

Two takeaways matter more than the number itself. First, the bull case is grounded in a specific, testable productivity thesis: approximately 3% annual US labour productivity growth driven by broad AI adoption. If that number proves correct, the earnings expansion needed to support 9,000 follows logically. If it does not, the base case of 7,750 is the more likely destination. Second, Evercore’s recommended positioning, calls for upside paired with a collar for protection, is designed for uncertainty rather than conviction. It is a structure that profits from the bull case without requiring it.

The one variable worth watching as a leading indicator: early signs of AI-driven productivity gains diffusing beyond mega-cap technology firms into the broader economy. If that diffusion begins to show up in quarterly earnings or industry-level productivity data through the second half of 2026, the 9,000 thesis gains credibility. If it does not, the market at 7,408 is already pricing a meaningful amount of optimism.

Evercore’s note, published 18 May 2026, does not ask investors to believe 9,000 will happen. It asks them to position for a world where the range of outcomes is wider than most models capture, and to do so with instruments that respect both ends of that range.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Evercore ISI has two scenarios for year-end 2026: a base case of 7,750 (approximately 4.6% upside from the 15 May 2026 close of 7,408.50) and a bull case of 9,000 (approximately 21.5% upside), with Julian Emanuel assigning a 30% probability to the higher target.

Evercore's 9,000 bull case requires approximately 3% annual US labour productivity growth driven by broad AI adoption, sustained capital investment, and AI productivity gains diffusing beyond mega-cap technology firms into the wider economy.

Evercore recommends a two-part structure: long-dated call options on AI-linked equities and the QQQ ETF for asymmetric upside exposure, paired with a collar strategy on the SPY ETF to limit downside risk from oil price movements and interest rate shifts.

Evercore's Julian Emanuel argues that large language models and prediction markets systematically underweight tail-end outcomes at both extremes of the distribution, clustering around consensus estimates and failing to price scenarios the crowd has not yet imagined.

McKinsey Global Institute projects generative AI adds only 0.1-0.6 percentage points to annual productivity growth through 2040, implying a trend of 1.6-2.1%, while the Penn Wharton Budget Model estimates a peak boost of just 0.2 percentage points in 2032, both well below Evercore's 3% assumption.