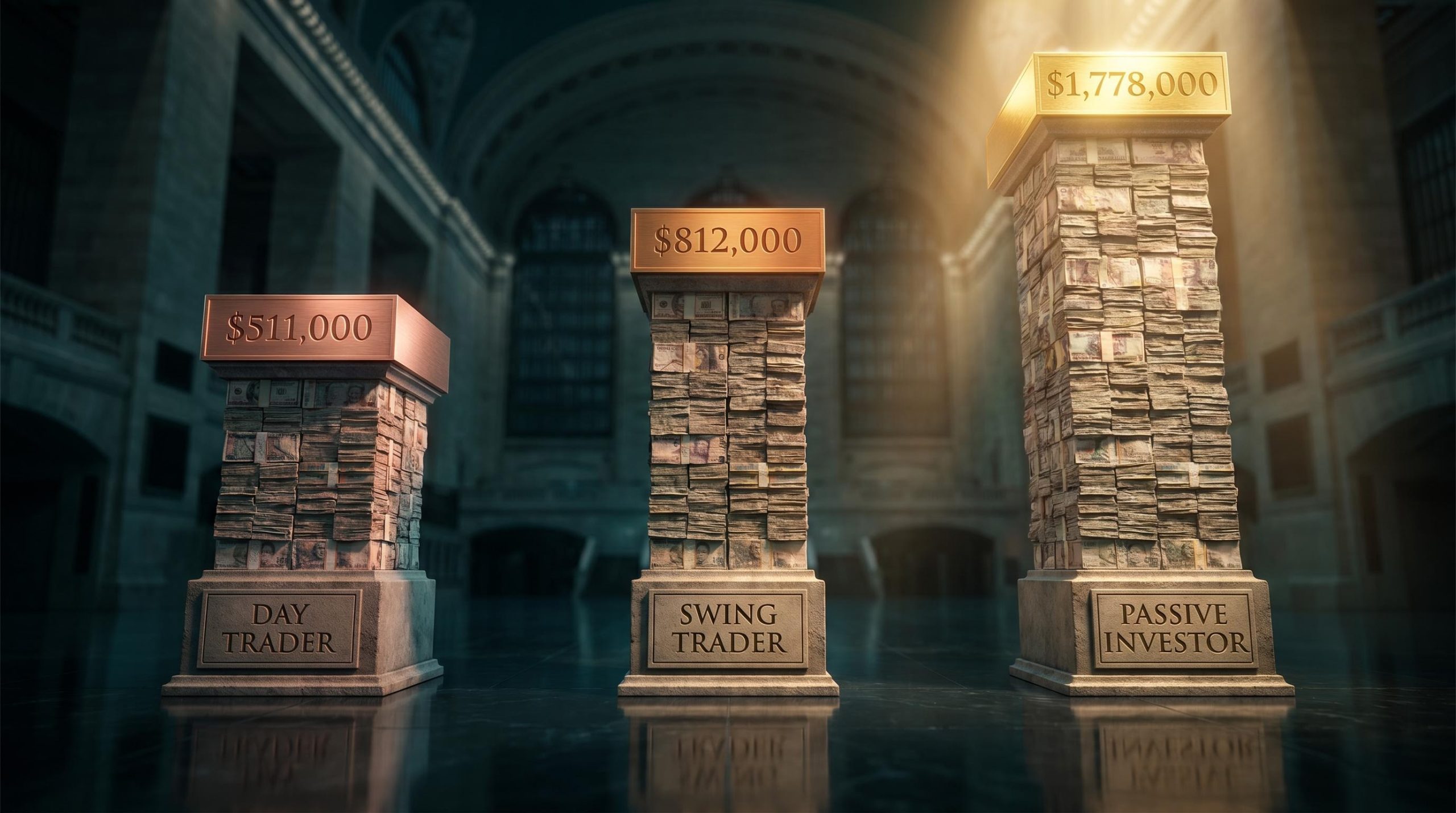

Three investors start at age 30. Each earns $75,000 a year. Each contributes $1,000 a month to a taxable brokerage account and keeps it up for 30 years. At age 60, one finishes with roughly $1.78 million. Another finishes with $812,000. The third, despite outperforming the vast majority of active traders, finishes with $511,000. The only variable that changed was how often they traded. The comparison between day trading, swing trading, and long-term index investing is one of the most searched topics in personal finance, yet most treatments stay at the level of generalisation. What follows is a controlled, three-investor scenario with five-year portfolio milestones, a structural cost breakdown covering taxes, friction, and timing, and a decision framework built on the numbers rather than around them.

The controlled experiment: three investors, one starting line

The three investors share identical starting conditions: age 30, annual income of $75,000, a $1,000 monthly contribution, and a 30-year horizon to age 60. Total capital contributed across all three is $360,000. The only difference is strategy.

- Day trader: Closes all positions by end of day using technical chart analysis. High frequency, intensive screen time, no overnight exposure.

- Swing trader: Holds positions for days to weeks, targeting short-term price swings. Lower frequency than day trading, compatible with a regular job.

- Passive investor: Buys a single low-cost S&P 500 index fund monthly and holds indefinitely. No timing decisions, no stock selection.

Assumed net annual returns are stated for transparency: passive investor approximately 7%; swing trader 4-5%; day trader 2-3%. No leverage is assumed for the day trader, which is itself a simplification; many real-world day traders use margin, which would amplify losses in adverse conditions.

| Investor | Strategy | Avg. Holding Period | Primary Vehicle |

|---|---|---|---|

| Day trader | Intraday technical trading | Minutes to hours | Individual equities |

| Swing trader | Short-term price swing capture | Days to weeks | Individual equities |

| Passive investor | Buy-and-hold indexing | Years to decades | Low-cost S&P 500 index fund |

Any terminal wealth difference that emerges from this framework reflects strategy performance alone, not savings behaviour, income, or contribution discipline.

When big ASX news breaks, our subscribers know first

What $1,000 a month actually becomes: the 30-year divergence in numbers

At year 5, the portfolios are close enough to seem interchangeable. The passive investor has roughly $75,000. The swing trader sits at approximately $68,000. The day trader trails slightly at $63,000. The gaps are modest, barely worth remarking on.

By year 15, compounding begins to pull the paths apart. The passive investor reaches approximately $373,000; the swing trader, $264,000; the day trader, $213,000. The absolute gap between passive and day trading has grown to $160,000.

The passive investor in this scenario crosses the portfolio crossover point somewhere around year 17, when annual market gains begin to permanently exceed the $12,000 yearly contribution, at which stage the portfolio becomes largely self-sustaining regardless of whether the investor continues contributing.

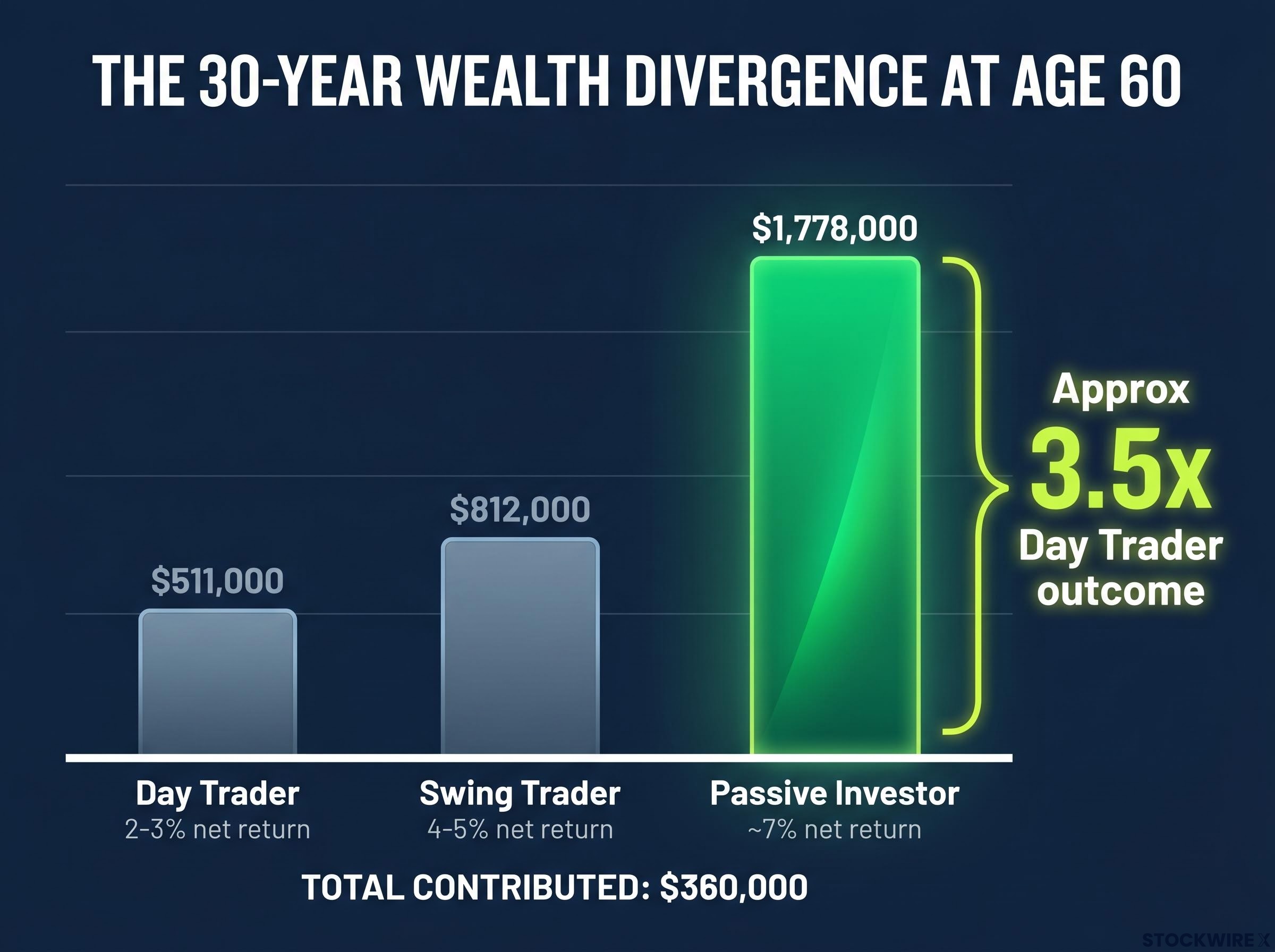

From year 20 onward, the divergence accelerates sharply. The passive portfolio crosses $656,000, then $1,095,000 at year 25, and reaches approximately $1,778,000 at year 30. The day trader, meanwhile, finishes at roughly $511,000. The swing trader lands near $812,000.

| Year | Day Trader | Swing Trader | Passive Investor |

|---|---|---|---|

| 5 | ~$63,000 | ~$68,000 | ~$75,000 |

| 10 | ~$134,000 | ~$154,000 | ~$192,000 |

| 15 | ~$213,000 | ~$264,000 | ~$373,000 |

| 20 | ~$302,000 | ~$499,000 | ~$656,000 |

| 25 | ~$400,000 | — | ~$1,095,000 |

| 30 | ~$511,000 | ~$812,000 | ~$1,778,000 |

One detail matters more than any row in this table: the day trader scenario assumes the investor outperforms approximately 80% of all active traders. A landmark study by Barber, Lee, Liu, and Odean, examining tens of thousands of Taiwanese day trading accounts, found that over 80% lost money net of fees, and only a small fraction achieved persistent excess returns. The $511,000 outcome is not a cautionary tale about a bad trader. It is an optimistic scenario.

The passive investor finishes with approximately 3.5 times the day trader’s terminal balance, despite contributing the same $360,000 over 30 years.

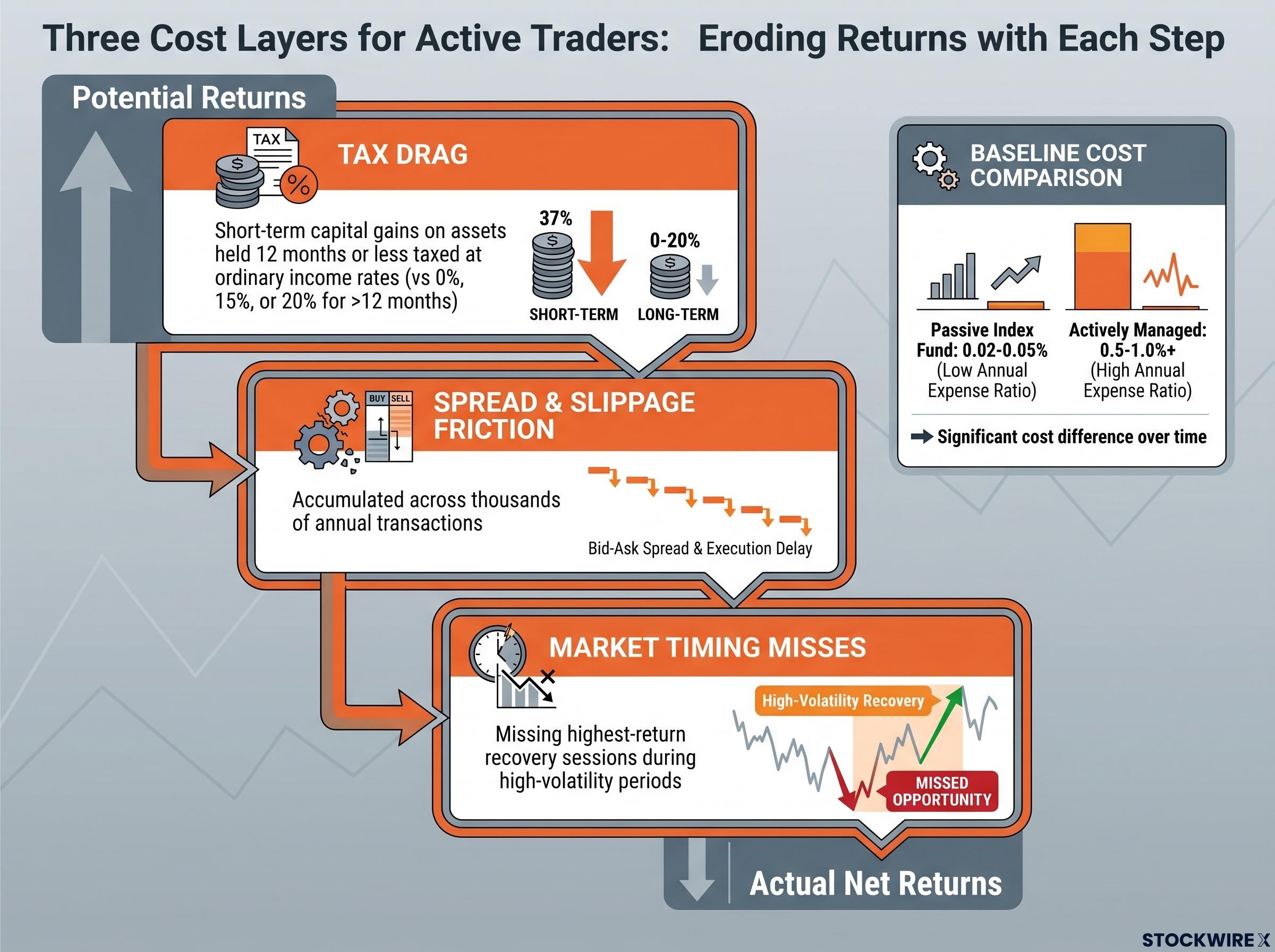

Why the IRS takes a bigger cut from traders than from buy-and-hold investors

Three structural mechanisms explain why the gap opens so relentlessly. Taxes are the first and most underappreciated.

How the short-term rate applies to most swing trades, not just day trades

U.S. capital gains tax distinguishes between short-term and long-term treatment. Assets held for 12 months or less are taxed at ordinary income rates, the same rates applied to salary and wages. Assets held for more than 12 months qualify for preferential federal rates of 0%, 15%, or 20%, depending on taxable income.

Day traders realise gains within hours. The short-term rate applies to virtually every transaction. Swing traders hold for days to weeks, but “days to weeks” is still well inside the 12-month window. Qualifying for long-term treatment requires holding past the one-year mark, a requirement structurally incompatible with an active rotation strategy.

The IRS capital gains tax treatment distinguishes between short-term gains taxed at ordinary income rates and long-term gains qualifying for preferential rates of 0%, 15%, or 20%, with the one-year holding threshold being the structural dividing line that active traders almost never cross.

The compounding brake: what annual tax payments cost over 30 years

The passive investor controls when taxable events occur and typically defers realisation for years or decades. This deferral has a compounding effect that accumulates over the full investment horizon:

- Every dollar paid in taxes early in the period is a dollar that stops compounding for the remainder of the 30 years.

- Gains on unrealised positions in the passive portfolio continue compounding on the full pre-tax amount year after year.

- The active trader’s annual tax payments function as a recurring withdrawal from the compounding base, a brake applied every year for three decades.

The tax advantage is not incidental. It is structural, and it widens with every passing year.

The passive investor’s tax deferral advantage assumes current law remains stable, but unrealized capital gains tax proposals at the federal level, including constitutional questions left open by Moore v. United States in 2024, represent a tail risk that long-term investors and their advisers should monitor when stress-testing 30-year projections.

Transaction costs and market timing: the two drags that finish what taxes start

Taxes remove capital from the compounding base annually. Transaction friction and timing failures compound the damage.

Even with near-zero commissions, bid-ask spreads and slippage apply to every trade. These costs do not appear on brokerage statements, but they erode returns as reliably as any explicit fee. A day trader executing thousands of transactions per year accumulates friction that, over a 30-year period, consumes a meaningful share of gross returns.

The third drag is market timing. Research on S&P 500 returns over multi-decade periods consistently shows that missing just a handful of the best trading days dramatically reduces total returns. Those best days tend to cluster during high-volatility periods, precisely when cautious or active traders are most likely to be defensively positioned or sitting in cash.

Research consistently shows the best days in U.S. equity markets cluster during the most volatile periods, when cautious or active traders are least likely to be fully invested.

The passive investor sidesteps all three mechanisms. A low-cost index fund carries expense ratios as low as 0.02-0.05% annually, compared with 0.5-1.0% or more for actively managed funds. There are no spreads on monthly contributions, no slippage, and full participation in every recovery rally. Ranked by typical magnitude for an active day trader, the three cost layers are:

- Tax drag from short-term capital gains treatment on every realised gain

- Spread and slippage friction accumulated across thousands of annual transactions

- Market timing misses during the highest-return recovery sessions

Why swing trading still falls short: the wealth gap that a moderate approach cannot close

Swing trading’s appeal is understandable. It demands less screen time than day trading. It involves fewer transactions. It reduces direct friction costs.

What swing trading gets right

Lower transaction frequency does reduce friction costs relative to day trading. There is no requirement for full-time market monitoring, making it compatible with salaried employment. For time-constrained investors who feel drawn to active strategies, swing trading appears to offer the best of both worlds.

What swing trading still gets wrong

The two most structurally damaging drags remain fully intact:

- Short-term tax treatment persists. A rotation cadence of days to weeks keeps the vast majority of realised gains inside the 12-month window, meaning ordinary income rates apply just as they do for day trading.

- Market timing exposure continues. Every entry and exit decision is subject to the same best-day problem that erodes day trading returns. Missing a recovery session because a position was closed a week earlier has the same compounding cost regardless of trade frequency.

The swing trader in this scenario finishes at approximately $812,000. The passive investor finishes at approximately $1,778,000. The gap is roughly $966,000, representing an effective annual return of 4-5% net versus the passive investor’s approximately 7%. “Less bad than day trading” is a real advantage, but it still compounds into nearly a million dollars of foregone retirement wealth.

A strategy framework for American investors who want to act on this data

The data points toward a clear baseline: passive index investing in a low-cost S&P 500 fund is the appropriate primary retirement vehicle for most American investors. The $1.78 million terminal value from identical contributions is the benchmark against which any alternative strategy should be measured.

The passive strategy only delivers its full compounding advantage when the investor stays consistently invested: research on index fund investing shows that approximately 60% of new investors exit the market around year six, forfeiting compounding gains that accelerate most sharply in years 10 through 30.

For investors who want to trade actively, a tiered framework grounds the decision:

- Establish the passive index base. A low-cost S&P 500 index fund, purchased monthly, forms the retirement core.

- Build emergency reserves and cover financial obligations. Core bills, emergency fund, and foundational index position must be fully in place.

- Allocate only discretionary capital to active strategies. Day trading or swing trading should be funded from a small, ring-fenced allocation the investor can afford to lose entirely. This is not retirement capital.

The Barber et al. finding bears repeating: the $511,000 day trader outcome represents a top-20% performer. A typical day trader’s result would be substantially worse.

Day trading also carries an opportunity cost that rarely enters the calculation. The screen time required to trade actively, often several hours per day, represents time that could be spent earning income, building skills, or simply living. The passive strategy that produced the highest terminal wealth required near-zero ongoing attention.

| Strategy | Recommended Role in Portfolio | Key Condition |

|---|---|---|

| Passive indexing | Primary retirement vehicle | Low-cost S&P 500 fund, held for decades |

| Swing trading | Small discretionary allocation only | Funded with capital the investor can afford to lose entirely |

| Day trading | Small discretionary allocation only | Same as swing trading, with realistic assessment of time costs |

The number that matters most is the one you end up with at 60

Over 30 years, $360,000 in identical contributions produced $1,778,000 for the passive investor, $812,000 for the swing trader, and $511,000 for the day trader. Those figures are the only scorecard that matters for retirement outcomes.

The passive strategy’s greatest advantage may be its simplicity. There are no timing decisions to second-guess, no tax-optimisation errors to correct, no discipline failures during volatile sessions. It simply compounds, year after year, on the full pre-tax base.

The variables that matter most are the ones every investor controls directly: time horizon, contribution rate, and whether the capital stays invested long enough for compounding to do its work.

For investors ready to move from this comparison to concrete implementation, our dedicated guide to long-term investment strategies covers dividend investing, index ETFs, bonds, and buy-and-hold methods with portfolio construction guidance grounded in 150 years of S&P 500 return data.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.