A technology company that has spent two decades building its core product now advises the regulatory body that mandates that product, counts a 19.9% strategic shareholder in one of Japan’s largest industrial conglomerates, and still trades at a share price below 5 pence. That tension sits at the centre of the Seeing Machines investment question. EU General Safety Regulation mandates for driver monitoring systems (DMS) are now in force, converting a discretionary automotive technology into a compliance requirement for every new vehicle sold in Europe. Seeing Machines and Smart Eye occupy the narrow field of credible independent specialist vendors positioned to capture that mandated demand. Yet the market has not rewarded this structural positioning with a valuation that reflects the shift. What follows examines whether the tailwinds are real and durable, what the near-term financing risk means for per-share outcomes, and how to frame the geographic expansion optionality without over-counting it.

What EU safety regulation actually did to the DMS market

Most investors treat regulation as background noise, a box-ticking exercise that confirms demand already in motion. The EU’s revised General Safety Regulation (GSR) did something structurally different. It converted driver monitoring from a discretionary technology spend into a compliance line item, shifting the commercial question from “should OEMs buy this?” to “which vendor should they use?”

The mandate operates in two phases:

| Requirement | New vehicle types | All new registrations |

|---|---|---|

| Driver Drowsiness and Attention Warning (DDAW) | July 2022 | July 2024 |

| Advanced Driver Distraction Warning (ADDW) | July 2024 | July 2026 |

The second phase, ADDW for all new registrations, takes effect next month. Every new car, truck, and bus sold in Europe from July 2026 must include advanced distraction monitoring capability.

The regulation mandates the functionality category, not a specific vendor or camera architecture. Market share must still be earned. But the addressable market floor has been hardened in a way that OEM budget cycles and consumer sentiment cannot erode. Seeing Machines’ advisory role to Euro NCAP on DMS standards compounds this positioning, giving the company structural influence over the framework that governs its own market.

EU Regulation 2019/21444523) established the binding legal framework under which ADDW systems must be fitted to all new vehicle registrations from July 2026, converting what had been an optional safety feature into a non-negotiable compliance requirement for every OEM selling into European markets.

When big ASX news breaks, our subscribers know first

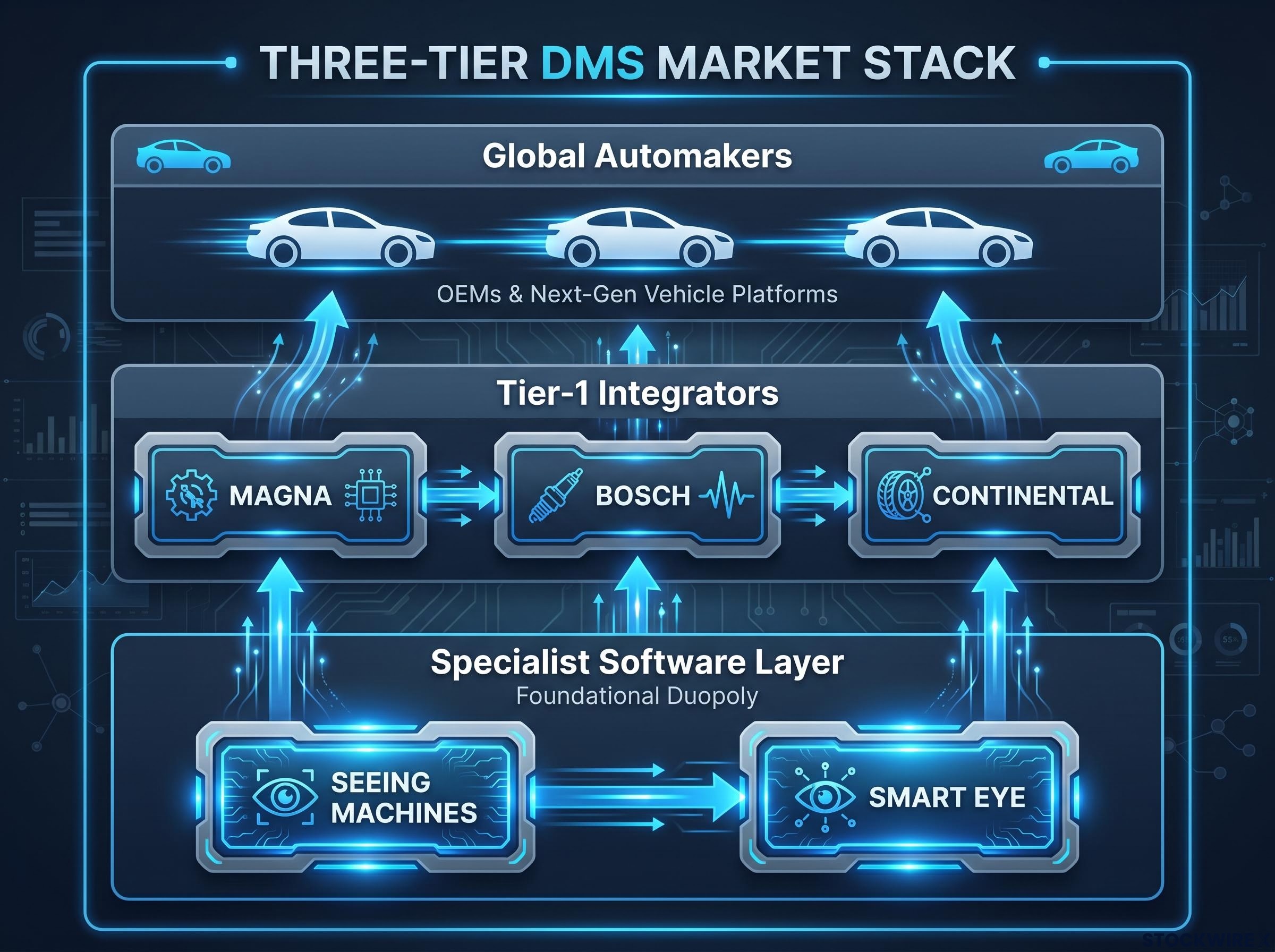

Why a duopoly forms at the software layer (and what that means for moats)

The “duopoly” label applied to Seeing Machines and Smart Eye requires precision. It describes one layer of a three-tier stack, not market invincibility.

At the top, global automakers select DMS solutions, typically via their Tier-1 suppliers. In the middle, Tier-1 integrators such as Magna, Bosch, and Continental architect full system modules. At the specialist software layer, Seeing Machines and Smart Eye operate as the two credible independent DMS/OMS vendors with multiple OEM programme wins.

The field has narrowed at this layer for three reinforcing reasons:

- Integrated hardware-and-software approach: Seeing Machines delivers a combined solution that reduces OEM integration complexity, distinct from Smart Eye’s software-only model

- False-positive alert performance: OEMs treat excessive false alerts as a reputational and customer-experience liability, making system robustness a commercially decisive differentiator

- OEM validation stickiness: Long, conservative validation cycles mean that once a supplier’s models are integrated into a production programme, switching costs are genuinely high due to safety certification and vehicle homologation requirements

The genuine medium-term threat comes from one layer above. Tier-1 suppliers often prefer modular solutions they can control across multiple OEMs, and some may build internal DMS stacks that are “good enough” to avoid dependency on a small IP vendor.

The Data Advantage: How it Strengthens Seeing Machines’ Moat

Seeing Machines has operated for approximately 20 years in mining, trucking, and heavy industry fleet environments, generating large volumes of real-world behavioural data across diverse edge cases: lighting conditions, population demographics, vehicle types, and geographic environments.

The strength of this advantage requires careful framing. Moats in machine learning depend on labelling quality and edge-case coverage, not raw data volume alone. Both Seeing Machines and Smart Eye hold significant proprietary datasets, and public data do not allow a precise head-to-head comparison. The defensible claim is that historical fleet deployments give Seeing Machines a material data and validation advantage against new entrants specifically, reinforced by the regulatory and certification friction that makes validated contracts long-lived.

Understanding the royalty model: how Seeing Machines actually gets paid

The revenue mechanics sit in two segments with distinct economics:

The OEM segment generates software licence royalties and non-recurring engineering (NRE) revenue, delivered via Tier-1 automotive suppliers. A royalty is a per-unit fee paid each time a vehicle containing the company’s software rolls off the production line. The pathway from design win to cash flow follows a specific sequence:

- Seeing Machines wins a design competition at the Tier-1 level

- The Tier-1 integrates the DMS software into an OEM vehicle programme

- The OEM ramps production into regulated markets

- Per-unit royalty payments flow back to Seeing Machines on every vehicle sold

The Aftermarket segment sells retrofit monitoring systems directly to commercial fleet and off-road operators in trucking, mining, and heavy industry. Customer economics are straightforward: incident reduction, insurance premium savings, and regulatory compliance returns make the product ROI-positive for buyers.

Aftermarket monitoring revenue rose 9% to US$13.6m in FY2025, a positive signal within an otherwise declining consolidated top line, indicating segment-level momentum independent of OEM timing.

Understanding the NRE-to-royalty transition, where upfront engineering work converts into recurring per-unit income, is the conceptual foundation for the free cash flow (FCF) projections that follow.

Navigating the Financial Disconnect: Potential vs. Reality

The FY2025 financials do not yet reflect the structural positioning. Revenue came in at US$62.3m, down from US$67.6m in FY2024, a decline of approximately 7.8% year-on-year. The company remained loss-making. Cash at 30 June 2025 stood at US$22.6m, implying less than 12 months of runway at reported burn rates.

The OEM segment drove the consolidated revenue reduction while the Aftermarket business grew. The business has not yet inflected into a clearly accelerating growth trajectory.

Against this, independent analysis has projected FCF for FY2027 at US$30-40m in a base case and US$25-30m in a conservative case. At an enterprise value below US$300m, these projections imply a forward FCF multiple of approximately 8-12 times on the automotive royalty business.

| Metric | FY2024 | FY2025 | FY2027 (projected) |

|---|---|---|---|

| Revenue | US$67.6m | US$62.3m | N/A |

| Cash position | N/A | US$22.6m | N/A |

| FCF (base case) | N/A | Loss-making | US$30-40m |

| FCF (conservative) | N/A | Loss-making | US$25-30m |

These FCF projections are sourced from independent analysis and should be treated as scenario analysis, not reported guidance. They require OEM programme ramp timing to materialise on schedule, making them aggressive-to-optimistic rather than conservative.

The gap between structural positioning and financial delivery is the variable that determines whether the current share price of approximately 4.3 pence (implied market cap of approximately £200-220m) represents an opportunity or a warning.

The Convertible Note: A Capital Structure Challenge, Not an Operating Issue

The convertible note, approximately US$47.5m issued in October 2022 via Magna and maturing October 2026, is a financing risk. It concerns capital structure and dilution, not whether DMS demand is real or whether Seeing Machines wins contracts.

The company has secured receivables facilities and is actively progressing refinancing options. Its contracted OEM programme base and growing royalty revenue represent a materially stronger credit position than at the time of issuance, when no proven royalty cash flow base existed. Independent analysis has estimated the company could generate US$20-30m in annual cash flow from contracted royalty programmes, providing a repayment capacity foundation.

Two hard constraints prevent the convertible from being dismissed entirely:

- Cash runway: Less than 12 months of runway based on reported burn means limited buffer if execution slips or refinancing takes longer than expected

- Capital market conditions: If equity markets are weak or credit spreads wide at refinancing time, the company could face dilutive equity issuance even if the underlying business trajectory is positive

What refinancing scenarios mean for shareholders

Three outcomes are possible, each with distinct per-share implications. A clean debt refinancing would be least dilutive, preserving equity upside for existing shareholders. A convertible or equity hybrid instrument would introduce moderate dilution but keep the capital structure manageable. A distressed equity raise, the worst-case scenario, would be the most dilutive and would compress per-share returns even if the operating story broadly plays out.

Management’s improved contracted royalty base relative to 2022 issuance conditions should reduce refinancing cost. Capital market cooperation remains a necessary but not sufficient condition for the most favourable outcome.

A convertible bond refinancing that extends maturity and preserves non-dilutive terms represents the most favourable structural outcome available to companies in this position; Telix Pharmaceuticals executed exactly this in April 2026, replacing its 2029 notes with 2031 bonds at a coupon of 1.50-1.75% and a conversion premium above 35%, a benchmark for what disciplined refinancing can achieve when the underlying credit story is strong.

Global Horizons: Valuing US and Asian Expansion Opportunities with Discipline

The EU is the only fully regulatory-driven DMS market today. Geographic expansion represents layered probability, not a uniform tailwind.

| Region | Current status | Direction of travel | Investor framing |

|---|---|---|---|

| EU | Binding mandate in force | Full phase-in by July 2026 | Base case |

| UK | Moving toward EU alignment | DMS requirements likely | Near-term optionality |

| Japan | ADAS regulations tightening | No nationwide GSR equivalent | Medium-term optionality |

| US | No binding federal mandate | NHTSA and Congressional discussions | High-impact optionality |

The US is the high-impact scenario. The market is approximately three times the size of Europe’s automotive market. If binding federal DMS mandates materialise, the addressable market would expand dramatically. Independent analysis places this in the upside case (approximately 3x return) rather than the base case (approximately 2x over 12-18 months).

NHTSA’s information collection on contextual DMS, initiated under the Infrastructure Investment and Jobs Act’s directive to address impaired driving prevention technology, signals regulatory intent without yet constituting a promulgated federal motor vehicle safety standard, placing a binding US mandate firmly in the probability-weighted upside column rather than the base case.

That framing discipline matters for position sizing. Over-counting geographic optionality is one of the most common errors in small-cap technology investment analysis. Non-EU upside belongs in the return scenario framework, not the base-case valuation.

Valuation Disparity: Unpacking the Market’s 4.3 Pence Price Tag

At approximately 4.3 pence, the market is pricing Seeing Machines as a loss-making, capital-dependent small-cap. The structural tailwinds, a mandated demand floor in Europe, a narrow specialist field, two decades of data and validation moat, Mitsubishi’s 19.9% stake validating the platform, and Magna Tier-1 embeddedness, are not fully reflected. Neither are the execution risks: revenue not yet accelerating, the 2026 convertible, and Tier-1 competitive pressure.

Independent analysis places the base-case return at approximately 2x and the upside case at approximately 3x if fleet ramps and US mandates materialise. Four indicators will determine which scenario unfolds over the next 12-24 months:

- OEM royalty revenue trajectory: Evidence that royalty streams are scaling and offsetting NRE dependency

- 2026 convertible resolution terms: Pricing, covenants, and equity issuance requirements

- First positive FCF reporting period: The milestone that validates the structural-to-financial transition

- Non-EU regulatory mandate developments: US, UK, or Asian DMS mandates or quasi-mandates

Position sizing discipline: Independent analysis suggests low-to-mid single-digit percentage portfolio weight, reflecting the genuine asymmetric upside alongside the real capital structure and execution risks.

Conclusion: Execution Remains Key for a Strong Thesis

The structural tailwinds are real and durable. EU mandates have hardened the demand floor, a narrow specialist field limits share erosion, and two decades of data and validation create meaningful switching costs. The gap between that positioning and financial delivery remains the central investor question.

The investment case works if the convertible is refinanced without severe dilution, OEM royalty ramp accelerates through FY2026-2027, and US mandate discussions progress. It does not work if revenue continues to stall, dilution compresses per-share outcomes, or Tier-1 internal solutions erode the specialist moat faster than expected.

A small-cap, loss-making, capital-dependent company with genuine regulatory tailwinds and a defensible competitive position is not a binary bet. It requires position sizing discipline and active monitoring rather than passive holding.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced in this article are sourced from independent analysis and are subject to market conditions and various risk factors.

—