Why Seeing Machines Trades Below 5p Despite EU Mandate Wins

12 mins ago

SpaceX completed the largest IPO in history on 12 June 2026, pricing shares at $135 and opening the market to a company valued at approximately $1.77 trillion. By the time most retail investors checked their brokerage accounts, the stock had already climbed past $161. The question now is not whether SpaceX has built something extraordinary. The reusable rockets, the satellite internet constellation, the government contracts: all of it is real. The question is whether buying SPCX stock at these prices represents a sound investment decision, or whether the smarter move is patience. What follows is a breakdown of the analyst evidence on both sides, an explanation of what the financials actually mean for someone weighing a position, and a practical framework for deciding whether SPCX belongs in a portfolio right now.

At $161 per share, an investor is paying for a company that generated $18.7 billion in revenue during 2025 and reported a GAAP net loss of approximately $4.9 billion over the same period. SpaceX is not yet profitable at the company level.

The implied IPO valuation of $1.77 trillion against that revenue base produces a price-to-revenue multiple of roughly 95x. For context, that is not a technology-sector norm. It is not even a high-growth technology-sector norm. It is a multiple that embeds decades of compounding growth into the price before a single quarter of public earnings has been reported.

| Metric | Figure |

|---|---|

| IPO price per share | $135 |

| First-day trading price | Above $161 |

| Implied IPO valuation | $1.77 trillion |

| 2025 revenue | $18.7 billion |

| 2025 GAAP net loss | ~$4.9 billion |

| Price-to-revenue multiple | ~95x |

“At roughly 95 times 2025 revenue, SpaceX’s IPO multiple is described by analysts as ‘very demanding for any company.'”

That multiple is the central tension of the investment case. The rest of this analysis examines whether the business underneath it can justify it.

The valuation is demanding. Sophisticated investors are buying anyway. Understanding why requires separating the business strengths into what is generating revenue today and what represents a longer-horizon bet.

SpaceX holds a dominant position in commercial rocket launch and cargo delivery, built on reusable rocket technology that structurally lowers costs relative to traditional providers. That cost advantage is not a one-quarter phenomenon; it is an engineering moat that competitors have struggled to replicate over a decade. Morningstar assigns the company a narrow economic moat rating, affirming the durability of its competitive position.

Starlink, the satellite internet division, adds a recurring revenue engine across consumer, enterprise, and government markets. This is what distinguishes SpaceX from a pure launch company. Launch contracts are lumpy and cyclical. Starlink subscriptions are predictable and diversified across customer segments.

The tension between Starlink’s recurring subscriber revenue and the lumpier, contract-driven launch business is easier to see when the SpaceX revenue segments are disaggregated: launch services, Starlink broadband, Direct-to-Cell wholesale infrastructure, and early-stage AI compute each carry different growth rates, margin profiles, and valuation methodologies that a single headline revenue figure obscures.

The three pillars of the bull case:

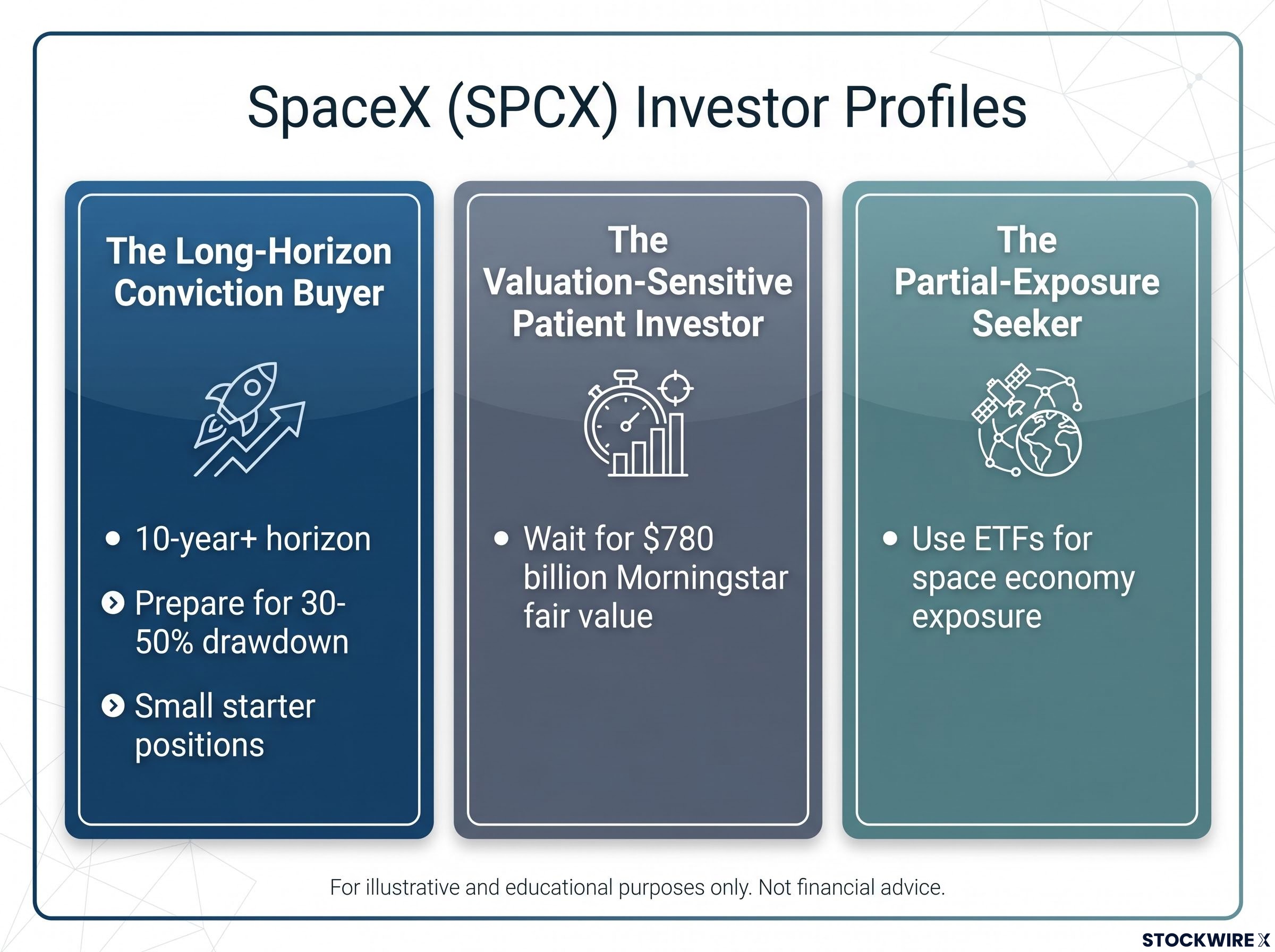

Morningstar’s analysis frames the third pillar carefully. The moat rating reflects what SpaceX has built today. The optionality sits on top: if a broader space economy develops around satellite infrastructure, in-orbit services, and next-generation launch capabilities, SpaceX holds the positions most likely to capture value. That optionality is real, but it is also the part of the thesis most dependent on assumptions that cannot be verified in 2026. Space-themed and innovation-focused ETFs are expected to add SPCX to their holdings as the stock matures, creating an additional structural demand driver over time.

Morningstar values SpaceX at approximately $780 billion. The IPO priced the company at $1.77 trillion. That gap is not a rounding error. It implies the stock would need to fall roughly 56% just to reach what one of the most respected independent research firms considers fair value.

“Worth about half of what it’s being sold at in the IPO.”

The discomfort among analysts is not about the business. It is about what the price demands. At 95x revenue with no GAAP profitability, today’s stock price requires a sequence of outcomes that must largely go right for the investment to work from here.

The specific execution requirements analysts identify:

The small analyst sample available on Investing.com (five analysts, two Buy, one Sell) underscores how early and contested the coverage is. The consensus rating label says “Buy,” but the valuation commentary from Morningstar and independent analysts tells a more cautious story. A loss-making, capital-intensive company trading at this multiple leaves very little margin for any of those execution requirements to slip.

The pattern is well-documented. High-profile growth companies that list without profits tend to experience significant drawdowns in their first years as public companies. This is not a commentary on business quality. It is a function of how markets reprice expectations once the IPO narrative meets quarterly reporting.

IPO cohort underperformance across the 1980-2024 dataset averages a 3.3% annual drag relative to comparably sized established peers, and critically, that figure holds even when the underlying businesses ultimately succeed; the mechanism is not business failure but the price paid at the moment of maximum public excitement.

IPO pricing captures peak optimism. The roadshow, the media coverage, the first-day pop: all of it concentrates buying demand into a narrow window. What follows is a longer period where the market calibrates that optimism against actual earnings reports, actual subscriber growth, actual capital expenditure, and actual regulatory developments.

“Without current earnings, there is no traditional valuation floor to slow a selloff if sentiment shifts.”

For a company like SpaceX, which has no GAAP earnings, the absence of an earnings-based valuation floor is particularly consequential. In a drawdown, earnings-positive companies find support where the price falls enough that the earnings yield becomes attractive to value buyers. Pre-profit companies lack that mechanism.

The conditions that typically trigger post-IPO repricing:

A 30-50% or greater drawdown from peak levels is a realistic near-term scenario, consistent with prior IPO cycles for companies at a similar stage. That does not mean the long-term thesis is wrong. It means investors should be financially and psychologically prepared for that volatility before committing capital.

The question of whether to buy SPCX is not one question. It is three different questions, depending on the investor asking.

For investors who fit the partial-exposure profile and want to act today rather than wait, our dedicated guide to accessible space stocks covers eight publicly traded names including Rocket Lab, Intuitive Machines, and AST SpaceMobile, each with no lockup periods or accreditation requirements, alongside the ARKX ETF as a diversified baseline for space economy exposure.

If the answers to those questions are not clear or comfortable, the analyst evidence supports patience rather than urgency at current prices.

Nothing in the analyst evidence disputes what SpaceX has built. The reusable launch technology, the Starlink subscriber base, the government contracts, the narrow economic moat: all of it is real and well-documented. The caution is specifically about the price being paid for those assets and the execution dependency that price embeds.

Investors who buy at IPO levels and hold for a decade may still be rewarded. This analysis does not rule that out. It quantifies the assumptions required for that outcome and notes that Morningstar’s $780 billion fair value estimate implies the stock would need to fall by more than half to reach what independent analysis considers reasonable value.

“Overpaying for shares can be costly. Waiting for a pullback may be the most prudent approach for most investors at current IPO prices.”

That observation, from Jaz Harrison of Rask Media on 13 June 2026, captures the analytical distinction cleanly. A remarkable company and a remarkable investment are not the same thing. Morningstar’s $780 billion estimate provides a concrete watchpoint: if SPCX trades meaningfully toward that level, the investment case becomes substantially more compelling for a wider range of investors.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

SpaceX priced its IPO at $135 per share on 12 June 2026, implying a valuation of approximately $1.77 trillion. Shares opened above $161 on the first day of trading, placing the stock at roughly 95 times the company's 2025 revenue of $18.7 billion.

No. SpaceX reported a GAAP net loss of approximately $4.9 billion in 2025, meaning it is not yet profitable at the company level. The absence of GAAP earnings means there is no traditional earnings-based valuation floor to support the stock price if sentiment deteriorates.

Morningstar values SpaceX at approximately $780 billion, which is roughly 56% below the IPO valuation of $1.77 trillion. The firm assigns the company a narrow economic moat, affirming the durability of its competitive position, but considers the IPO price well above fair value.

Retail investors can gain partial exposure through space-themed and innovation-focused ETFs that are expected to add SPCX to their holdings over time, as well as through publicly traded names such as Rocket Lab, Intuitive Machines, and AST SpaceMobile, which carry no lockup periods or accreditation requirements.

The main risks include a 95x revenue multiple with no GAAP profitability, a Morningstar fair value estimate roughly 56% below the IPO price, the historical pattern of high-profile pre-profit IPOs experiencing 30-50% or greater drawdowns, and the execution dependency built into a price that requires Starlink scaling, Starship delivery, and regulatory stability all to proceed without significant setbacks.