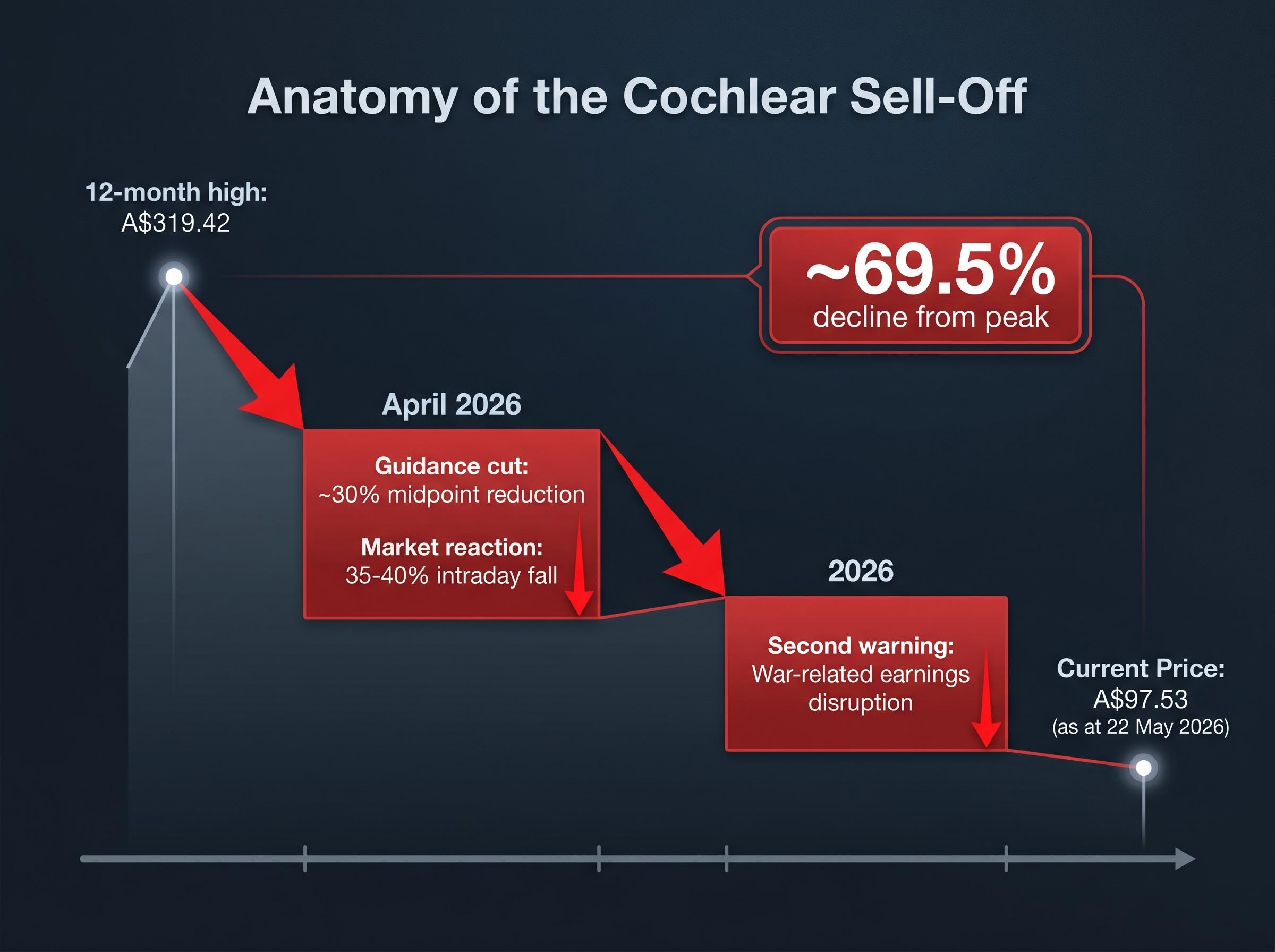

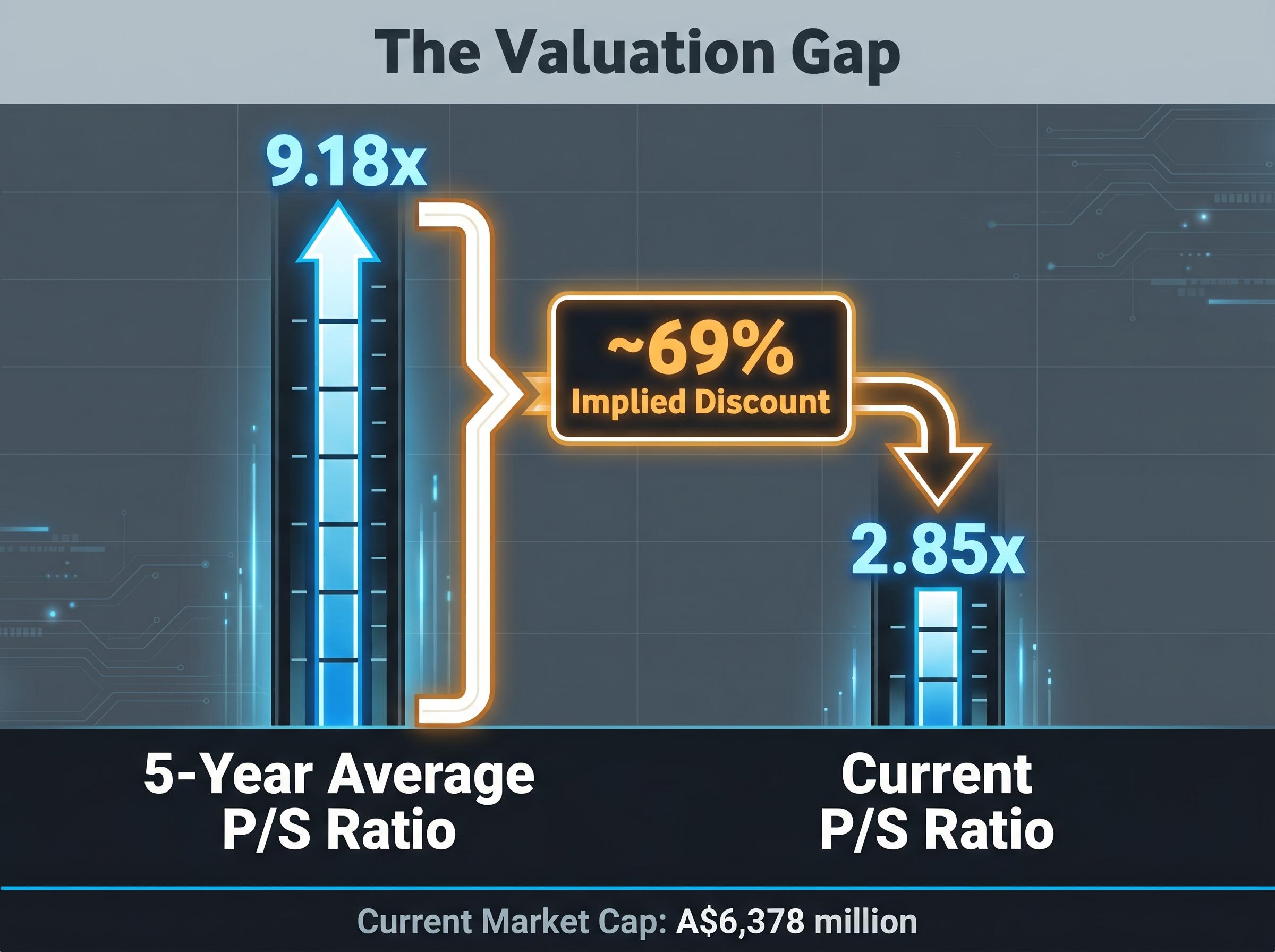

Cochlear’s share price has fallen roughly 62.6% since the start of 2025, a decline so severe it has compressed the stock’s price-to-sales ratio to 2.85x, less than a third of its five-year historical average of 9.18x. For ASX investors, that gap between current valuation and historical norm raises an immediate question: is this a generational discount on a world-leading medical device franchise, or a re-rating that still has further to run? Two profit warnings in 2026, including an April guidance cut of approximately 30% at the midpoint and a separate warning citing war-related earnings disruption, have shaken confidence in a stock that long traded on a premium multiple. The magnitude of the sell-off, including a 35-40% intraday fall on the April announcement, has drawn scrutiny from research houses including Intelligent Investor and Morningstar, alongside commentary from Rask Media and Stocks Down Under. What follows is a structured analysis of the drivers behind the de-rating, the fundamentals that underpin the bull case, and a framework for assessing whether COH belongs in a portfolio at current prices.

What actually drove Cochlear’s 62.6% share price collapse

The sell-off arrived in two distinct waves, each with a different character. Separating them matters, because each carries different implications for recovery probability.

The April 2026 guidance cut

In April 2026, Cochlear slashed its FY26 profit guidance by approximately 30% at the midpoint. The market’s verdict was immediate: the share price fell 35-40% in a single session. According to Rask Media journalist Jaz Harrison, writing on 22 April 2026, the scale of the intraday move reflected the market repricing a stock that had long been valued on the assumption of steady, non-discretionary demand growth.

Stocks Down Under described the event as a “sharp de-rating driven by lower profit guidance” rather than balance sheet distress or product failure.

The expectations gap in earnings reactions explains why Cochlear’s April sell-off exceeded the arithmetic of the guidance cut: the market had priced in a growth trajectory, and the revision did not merely lower profits but signalled that management’s own forward visibility was materially impaired, compounding the multiple compression beyond what the earnings downgrade alone would have justified.

The war-related profit warning

A second, separate profit warning followed, with Cochlear explicitly citing war-related impacts on earnings. Australian business news coverage described shares “plummeting” on the announcement, with the sell-off dragging the broader Australian sharemarket lower.

The two events in summary:

- April 2026 guidance cut: FY26 profit guidance reduced by approximately 30% at the midpoint; share price fell 35-40% intraday.

- Second profit warning (2026): Explicitly cited war-related earnings disruption; contributed to broader ASX weakness.

The cumulative result: a fall from a 12-month high of A$319.42 to approximately A$97.53 as at 22 May 2026, representing a decline of roughly 69.5% from that peak. The first warning was an earnings revision. The second was a geopolitical disruption of uncertain duration. Investors need to weigh each separately before judging whether the damage is permanent.

Cochlear’s April 2026 ASX guidance update published on 22 April 2026 contains the precise downgrade range and management’s stated reasons for the earnings revision, making it the primary reference for investors seeking to verify the approximately 30% midpoint cut figure cited across media coverage.

When big ASX news breaks, our subscribers know first

The business behind the price: what Cochlear actually does and why it has held a premium

Before any valuation assessment, the strength of the underlying franchise deserves its full weight.

Cochlear manufactures cochlear implants, bone-anchored hearing aids (Baha), and associated sound processors. It holds approximately 60% of the global cochlear implant market, according to Morningstar’s 2025 coverage, operating within a tight three-player oligopoly alongside MED-EL and Advanced Bionics (part of the Sonova group). The company has distributed more than 750,000 implantable hearing devices to date, employs approximately 5,500 people across more than 50 countries, and has maintained revenue on an upward trajectory over the prior three years.

The demand drivers are structural and multi-decade in nature. Ageing populations in developed markets are expanding the addressable patient cohort. Improved neonatal hearing screening programmes are accelerating diagnosis. Emerging markets remain under-penetrated. In developed economies, cochlear implants carry standard-of-care status for children with severe-to-profound hearing loss, underpinning demand that is relatively insensitive to economic cycles.

| Region | Revenue share (FY2025) | Demand characteristics |

|---|---|---|

| Americas | 49% | Established reimbursement; stable volumes |

| EMEA | 34% | Public reimbursement and tender-driven |

| Asia-Pacific | 18% | Under-penetrated; tender-driven emerging markets |

Approximately 80% of revenue derives from developed markets, with the remaining 20% from emerging markets where government tenders introduce periodic volume volatility.

Morningstar characterises Cochlear’s competitive advantages as moat-like, citing entrenched surgeon and hospital relationships, strong brand recognition, high switching costs for implanted patients, and regulatory barriers to entry that collectively protect the company’s dominant market position.

That competitive position has not been impaired by the profit warnings. What has been impaired is the market’s confidence in the earnings trajectory that once justified the premium multiple.

Cochlear’s installed base of more than 750,000 implanted devices generates recurring revenue from processor upgrades and accessories, providing a commercial floor that pure device-sale businesses lack, and one that analysts argue makes the earnings trough shallower than the guidance revision headlines suggest.

How to read a price-to-sales ratio and why COH’s current multiple matters

A price-to-sales (P/S) ratio measures how much investors are paying for each dollar of a company’s revenue. It divides the total market capitalisation by annual revenue. For medical device companies where earnings can swing on one-off charges, guidance revisions, or currency movements, the P/S ratio offers a valuation signal that is less distorted by short-term profit volatility than earnings-based multiples like the price-to-earnings ratio.

The real analytical value comes from comparing a stock’s current P/S to its own historical average. When the ratio is well below its long-run norm, it signals either that the market sees permanently lower growth ahead, or that short-term fear has compressed the valuation beyond what fundamentals justify. Distinguishing between those two readings is the central question for COH right now.

Cochlear’s P/S compression from 9.18x to 2.85x represents a valuation discount of approximately 69% relative to its own five-year average, the widest gap in the stock’s recent history.

| Metric | Current | Five-year average |

|---|---|---|

| Price-to-sales ratio | 2.85x | 9.18x |

| Implied discount | ~69% below historical average | |

It is worth noting that the P/S figures cited here have not been independently verified beyond the initial research source. A single valuation ratio, however compressed, cannot substitute for a full valuation framework. Discounted cash flow (DCF) analysis or dividend discount modelling would be required to form a complete view, and investors should treat the P/S signal as a starting point for further research, not a conclusion.

Cochlear’s current market capitalisation sits at approximately A$6,378 million.

The case for and against COH at current prices

The bull case for COH

Four pillars support the argument that COH is a buying opportunity at these levels.

- Dominant market position. Approximately 60% global market share in a three-player oligopoly, reinforced by switching costs that make it difficult for hospitals and patients to move to competitors once implanted.

- Structural demand. Ageing demographics, improved screening programmes, and emerging market under-penetration provide multi-decade growth runways that predate and will outlast the current earnings disruption.

- Non-discretionary standard of care. Cochlear implants are not elective purchases in developed markets. Demand has historically proven resilient through economic downturns.

- Valuation compression. A P/S ratio of 2.85x versus a five-year average of 9.18x represents a historically steep discount. Morningstar’s qualitative moat framing, citing brand strength, switching costs, and regulatory barriers, supports the view that the franchise warrants a premium multiple if earnings normalise.

Intelligent Investor recorded a “price at review” of A$99.58 on 23 April 2026, close to the current price of approximately A$97.53, suggesting the research house’s assessment had not materially shifted in the intervening month. Several commentators, including Rask Media, have framed the sell-off as near-term earnings pressure rather than structural impairment, implying the long-term investment thesis remains intact.

The bear case for COH

Four risks support the argument that the decline could continue.

- Repeated guidance downgrades. Two profit warnings in 2026, including an April cut of approximately 30% at the midpoint, signal that management’s own forward visibility is poor. Back-to-back downgrades erode the credibility premium that supported the stock’s historical multiple.

- Geopolitical uncertainty. The war-related profit warning cited a headwind whose mechanism, duration, and ultimate earnings impact remain unclear. This is not a risk that can be modelled with confidence.

- Permanent multiple re-rating. If the market concludes that Cochlear’s long-run growth rate has structurally moderated, the historically elevated P/S and P/E multiples may not be restored. The current lower multiple could represent a rational repricing rather than a temporary dislocation.

- Tender-driven volatility. The 20% of revenue derived from emerging markets is subject to government tender cycles, introducing lumpiness that amplifies uncertainty during periods of already low earnings visibility.

Guidance credibility signals in earnings releases, including the placement of downgrade disclosures, the specificity of management language in analyst Q&A sessions, and the gap between non-GAAP and GAAP metrics, are the tools investors can use to assess whether a management team’s revised forecasts are conservative or whether further cuts remain likely.

The question that separates the bull and bear cases is precise: is the current earnings pressure cyclical and geopolitically driven, meaning it will reverse when the external shocks fade, or does it reflect a structural moderation in Cochlear’s growth rate that justifies a permanently lower multiple?

What investors should do before acting on a beaten-down stock like COH

At a share price of approximately A$97.53, the cost of acting on incomplete information is asymmetric. A structured research process protects against both reflexive panic selling and reflexive bargain hunting.

- Verify the guidance figures directly. Read Cochlear’s April 2026 ASX guidance update to confirm the precise downgrade range. The approximate 30% midpoint cut cited in media coverage should be cross-referenced against the company’s own announcement.

- Review the H1 FY2026 results release. Specific half-year revenue, net profit, and implant volumes provide a clearer picture of the earnings trajectory than media summaries alone.

- Apply a full valuation framework. A single P/S ratio, particularly one that has not been independently verified, cannot support a sizing decision. Discounted cash flow analysis or professional advice is warranted before committing capital to a stock with this level of near-term uncertainty.

- Assess portfolio weighting and risk tolerance. A stock facing two profit warnings and an active geopolitical headwind of unknown duration warrants careful position sizing. Mean reversion is not guaranteed, and the timeline for any recovery is uncertain.

- Note the limitations of available research. Named broker price targets from Macquarie, UBS, Citi, and others are behind paid terminals. Intelligent Investor and Morningstar maintain live coverage, but their full recommendation levels and fair value estimates sit behind paywalls.

For investors who want to move beyond the P/S ratio and apply a full valuation framework to COH, our dedicated guide to ASX stock valuation methods covers when to use dividend yield, price-to-sales, discounted cash flow, and comparable transaction analysis, with worked examples drawn from ASX-listed companies including Sonic Healthcare.

COH at A$97.53: deeply discounted franchise or a falling knife?

The tension at the heart of this stock is self-reinforcing. The same factors that justify caution, two profit warnings, geopolitical uncertainty, and an unknown earnings floor, are precisely what have created the valuation compression that makes COH analytically interesting. A P/S of 2.85x against a five-year average of 9.18x does not happen to a 60% global market share medical device leader without serious cause for concern.

The question is not whether COH is cheap. It is whether the cheapness reflects a temporary dislocation or a permanent repricing of what the franchise is worth.

The next material data points will begin to separate the two readings. Full-year FY2026 results, any further guidance updates, and the resolution or continuation of the geopolitical disruption that triggered the second warning will collectively determine whether this is a value trap or the entry point that long-term investors remember. Until those catalysts arrive, the price alone is not an answer.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections and valuation metrics cited are subject to market conditions and various risk factors.