June US Inflation Report Hits as Fed Sits 9-9 on Rate Hikes

2 hrs ago

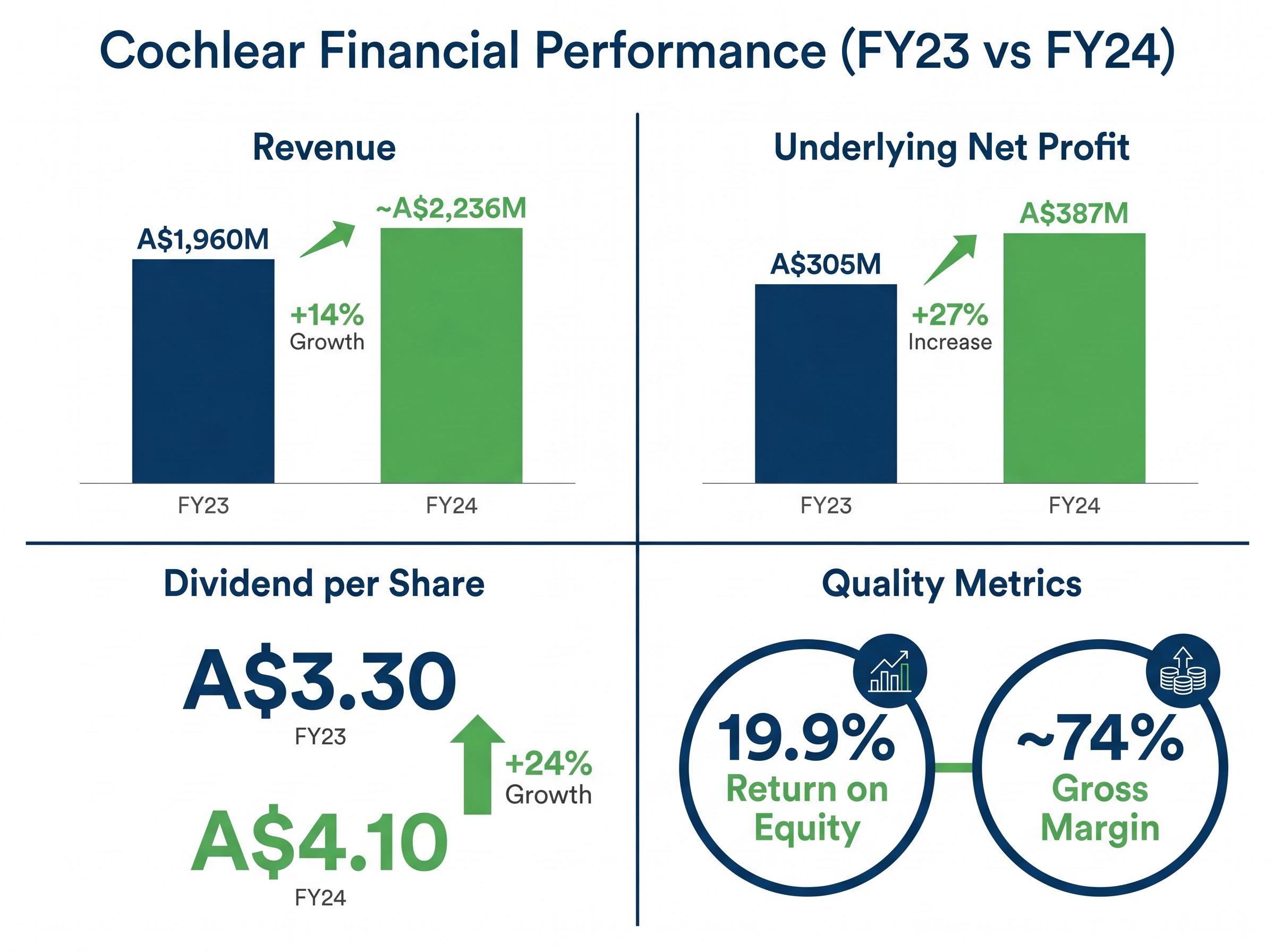

Cochlear has delivered 14.3% annualised revenue growth over three years and a return on equity of 19.9%, yet its share price sits near a multi-year low in May 2026. For a business generating 74% gross margins, expanding net profit, and increasing dividends at 24% year-on-year, the disconnect between operational performance and market price is striking. The ASX Healthcare sector has declined approximately 34% year-to-date, dragging high-quality names down alongside weaker peers. Cochlear, one of Australia’s most globally recognised medical device companies, has not been spared. This Cochlear stock analysis breaks down the company’s business model, verified financial performance, the forces driving share price weakness, what analyst consensus currently signals, and the risks and opportunities investors should weigh before forming a view.

Cochlear designs, manufactures, and distributes implantable hearing devices across three product categories:

Founded in Sydney in 1981, the company now employs more than 5,000 people across 50-plus countries. In July 2025, it launched the Nucleus Nexa System, described as the world’s first smart cochlear implant system.

More than 750,000 devices have been implanted globally, and each one creates a multi-decade commercial relationship. Patients return for processor upgrades, accessories, and clinical services long after the initial surgery. This installed base dynamic buffers new-unit volume volatility and supports margin stability over time, providing a revenue floor that pure device-sale businesses lack.

The growth trajectory through FY24 tells a consistent story. Revenue rose from approximately A$1,960 million in FY23 to approximately A$2,236 million in FY24, representing the 14.3% annualised rate sustained over three years. Underlying net profit climbed 27% from A$305 million to A$387 million over the same period. Gross margins held at approximately 74%, and the return on equity reached 19.9%.

These are not the financials of a business in structural decline.

| Metric | FY23 | FY24 | Change | Note |

|---|---|---|---|---|

| Revenue | A$1,960M | ~A$2,236M | ~+15% | FY24 figure flagged for verification against ASX filing |

| Underlying Net Profit | A$305M | A$387M | +27% | |

| Gross Margin | ~73% | ~74% | +1ppt | |

| Return on Equity | 19.9% | Most recently reported period | ||

| Dividend per Share | A$3.30 | A$4.10 | +24% | ~69% payout ratio |

The HY24 result (half-year ended 31 December 2023) showed revenue of A$1,113.4 million, up 25% reported and 20% in constant currency, reinforcing the growth trajectory visible in full-year numbers.

FY25 guidance: Management has guided for revenue growth of approximately 10% and underlying profit of A$410 million to A$430 million, implying a 6-11% increase on FY24. This forward view suggests the company expects growth to moderate but remain firmly positive.

For a growth-oriented ASX company, a 19.9% ROE comfortably clears the 10% threshold commonly used to distinguish high-quality businesses. Combined with 74% gross margins and a rising dividend, the financial profile raises a pointed question: why is the market pricing this business where it is?

The answer starts with the sector, not the company. The ASX Healthcare sector has fallen approximately 34% year-to-date in 2026, according to MarketIndex.com.au. That broad-based de-rating has compressed valuations across the cohort, pulling quality names lower alongside weaker peers.

Four forces are weighing on Cochlear’s price:

The China rare earth disruption is not a theoretical risk. Cochlear implants contain specialised magnets, and restricted supply of rare earth materials directly affected production and shipment timelines in the first quarter. The AFR reported approximately 5-7% delivery delays during this period.

Short interest in the 4-5.7% range signals that professional market participants are actively positioning against a near-term recovery. This does not guarantee further downside, but it does indicate a degree of institutional scepticism that sits at odds with the more optimistic retail commentary circulating on forums and social media. Competitor momentum also added pressure: Advanced Bionics (owned by Sonova) delivered strong US earnings in April 2026, drawing attention to market share dynamics.

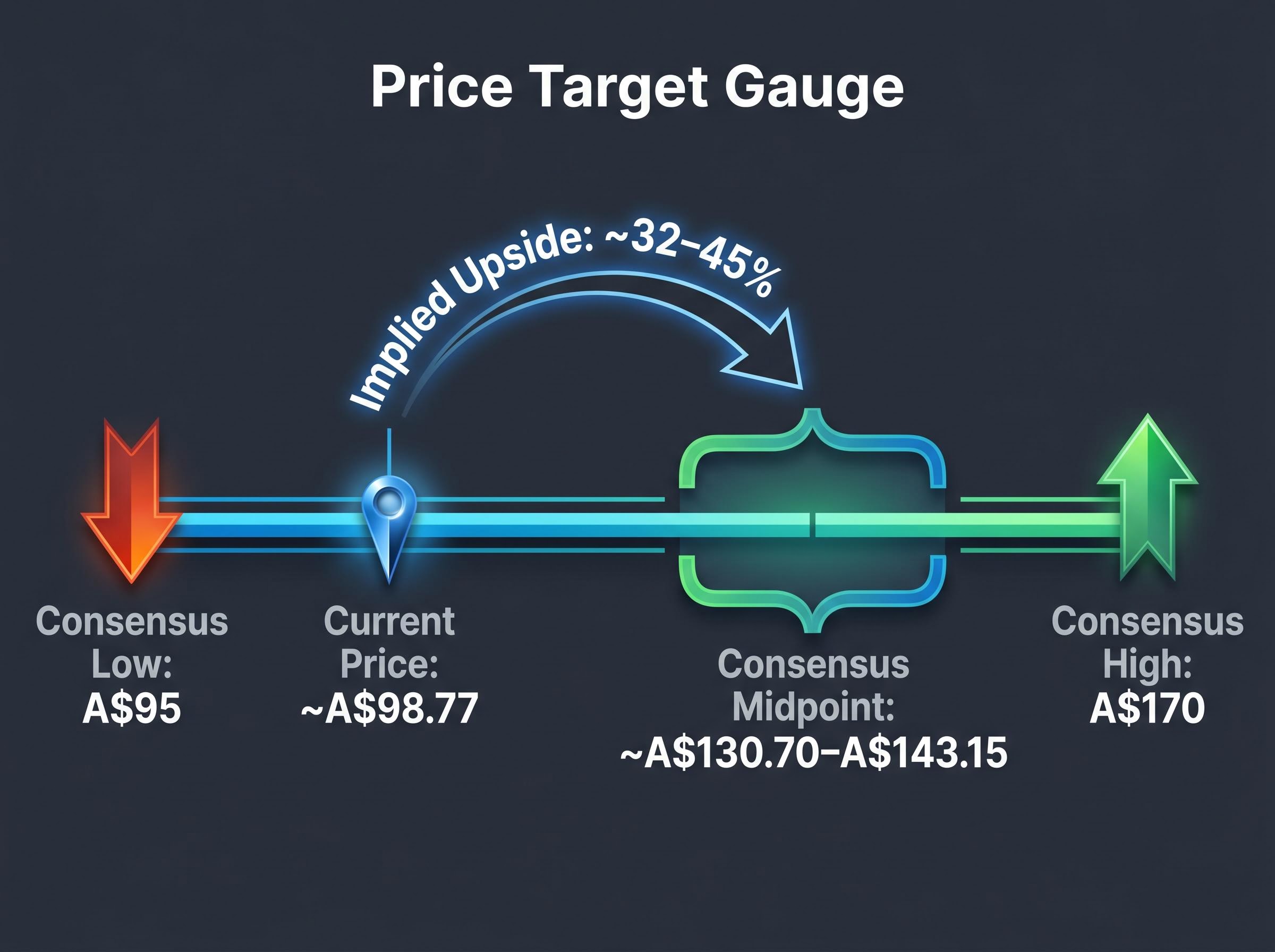

Verified consensus data from MarketScreener and AlphaSpread places the analyst price target range at approximately A$130.70 to A$143.15, against a current share price of approximately A$98.77. The AFR recorded a low of A$99.58 on 22 April 2026.

| Current Price | Consensus Low | Consensus Midpoint | Consensus High | Implied Upside (Midpoint) |

|---|---|---|---|---|

| ~A$98.77 | A$95 | ~A$130.70–A$143.15 | A$170 | ~32–45% |

The dispersion matters more than the midpoint. At the low end (A$95), some analysts see fair value close to where COH currently trades. At the high end (A$170), the implied upside is substantial. Ratings include both Hold and Overweight assessments, and the spread reflects a genuine valuation debate rather than consensus clarity.

Investors should note that some widely circulated broker figures and analyst attributions could not be independently verified during research for this article. Accessing broker research directly for current recommendations remains preferable to relying on aggregated commentary.

Divergent institutional conviction: Vanguard filed as an initial substantial holder on 11 February 2026, while AustralianSuper ceased being a substantial holder in April 2026. Two of the largest institutional investors in Australia reached opposite conclusions at similar price levels, underscoring the lack of consensus on COH’s near-term trajectory.

The company’s market capitalisation sits at approximately A$6.46 billion across 65,398,681 shares outstanding.

A cochlear implant is a surgically implanted electronic device that directly stimulates the auditory nerve, bypassing damaged parts of the inner ear. It is prescribed by clinicians, requires surgery for placement, and is covered by Medicare in both Australia and the United States. It is not a hearing aid.

That clinical distinction shapes everything about Cochlear’s competitive position. Hearing aids are increasingly available over the counter following regulatory changes in multiple markets. Cochlear implants remain clinician-prescribed, surgically delivered, and subject to clinical selection criteria. This creates higher barriers to entry for competitors and reduces the price sensitivity that characterises consumer hearing devices.

The surgical selection process limits the addressable patient pool, but the patients who do receive implants become long-term customers through the processor upgrade cycle. This is fundamentally different from a one-time consumer purchase. The clinical relationship, the switching costs of an implanted device, and the Medicare reimbursement pathways create a protected commercial moat.

Three structural demand drivers support the category over the long term:

The Nucleus Nexa System, launched in July 2025, represents the company’s current flagship innovation and positions it to capture upgrade demand from the existing installed base while attracting new patients with improved technology.

The bull case and the bear case both rest on verified data, and the tension between them is unresolved.

Arguments supporting the investment case:

Arguments for caution and ongoing monitoring:

Quality anchor: A return on equity of 19.9% comfortably exceeds the 10% threshold commonly used to screen for high-quality ASX growth stocks. ROE alone does not determine whether current price levels represent an attractive entry point, but it does confirm the business quality that underpins the valuation debate.

Investors should monitor HY25 results (Appendix 4D filed 13 February 2026, with specific figures requiring direct verification), RBA rate decisions, China regulatory and supply chain developments, and any shifts in substantial holder filings.

Cochlear’s operational metrics, including double-digit revenue growth, 19.9% ROE, 74% gross margins, and 24% dividend growth, describe a genuinely high-quality business. Verified market data tells a different story at the price level: approximately A$98.77, a 34% sector decline, and short interest between 4-5.7%.

The gap between fundamentals and price is real, but it does not resolve automatically. Macro rate conditions, supply chain risks, and analyst disagreement about fair value are legitimate reasons the compression may persist. Investors conducting their own research should verify current price, broker consensus, and HY25 financial results directly from ASX-lodged filings rather than relying on secondary aggregators, given the significant data quality issues identified in circulating research on COH.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A cochlear implant is a surgically implanted electronic device that directly stimulates the auditory nerve, bypassing damaged parts of the inner ear, and is clinician-prescribed and Medicare-covered. Unlike hearing aids, which amplify sound and are increasingly available over the counter, cochlear implants require surgery and clinical selection criteria, creating higher barriers to entry for competitors.

Cochlear's share price decline is driven primarily by a broad ASX Healthcare sector de-rating of approximately 34% year-to-date in 2026, combined with a high interest rate environment, China rare earth supply chain disruptions causing shipment delays, and elevated short interest of around 4-5.7% of shares outstanding.

Verified consensus data places the analyst price target range at approximately A$130.70 to A$143.15, against a share price of around A$98.77, implying a midpoint upside of roughly 32-45%, though some analysts see fair value closer to the current price at a consensus low of A$95.

Cochlear's return on equity stands at 19.9%, comfortably exceeding the 10% threshold commonly used to identify high-quality ASX growth stocks. A high ROE indicates the company is generating strong profits relative to shareholder equity, confirming the underlying business quality even as the share price trades near multi-year lows.

Key risks include ongoing China rare earth export restrictions that caused approximately 5-7% shipment delays in Q1 2026, the RBA cash rate of 4.35% continuing to compress growth stock valuations, short interest remaining elevated at 4-5.7%, and analyst disagreement about fair value with some targets sitting near current price levels.