Why 30% Recession Odds Are Harder to Trade Than 60%

9 hrs ago

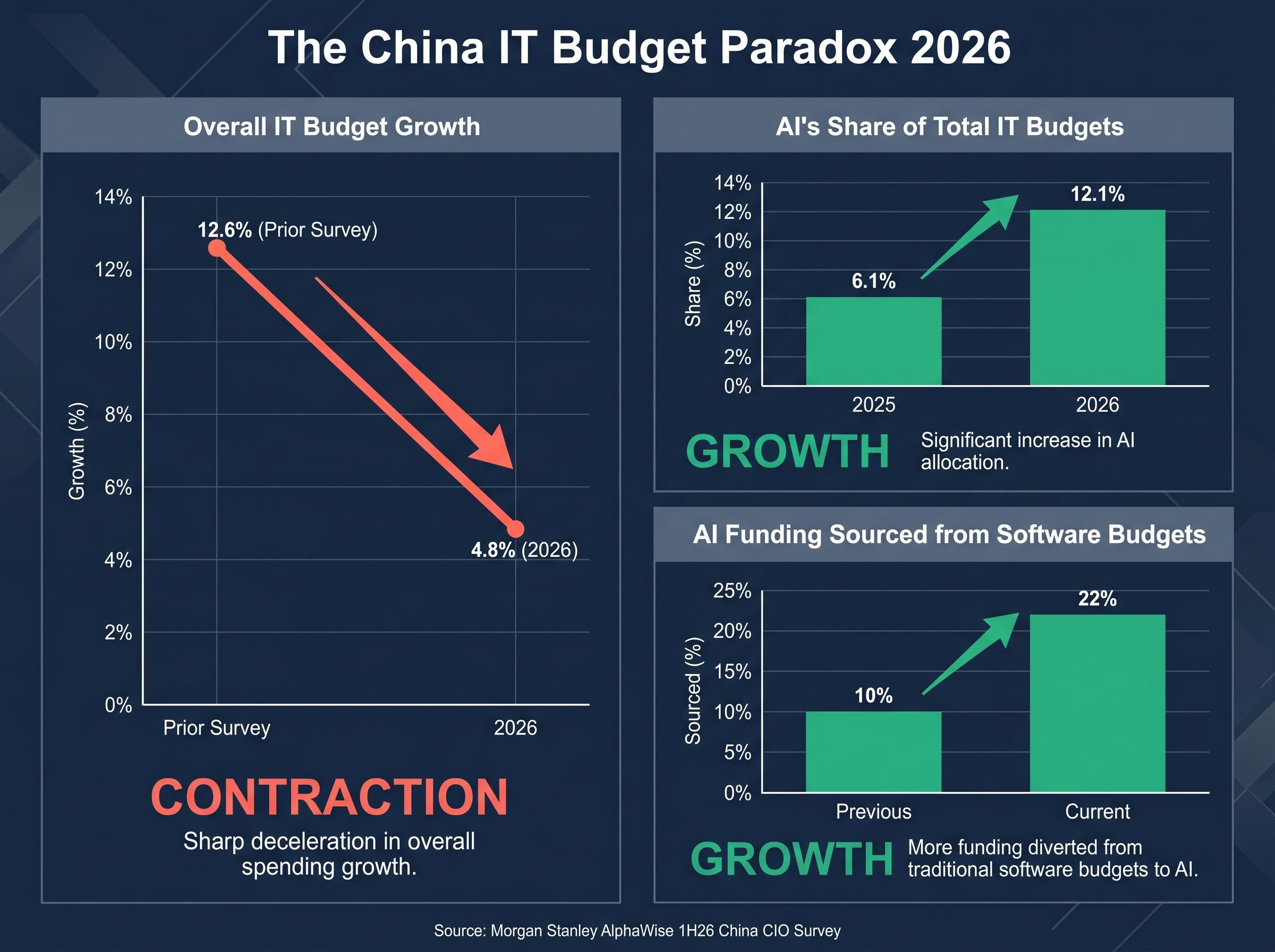

Chinese IT budget growth just hit its lowest point since Morgan Stanley began tracking it in 2020, collapsing from 12.6% to 4.8% in a single survey cycle. At the same time, artificial intelligence’s share of those same budgets is set to nearly double. The contradiction is sharper than it appears. The Morgan Stanley AlphaWise 1H26 China CIO Survey, conducted across 60 chief information officers in March and April 2026 and published today, surfaces a structural tension that carries direct implications for investors in Chinese technology, global enterprise software, and AI infrastructure. This is not a stagnation story. It is a forced reallocation of constrained capital toward AI at the expense of conventional IT categories. What follows unpacks the compression driving headline budgets lower, how AI is cannibalising legacy software spending, what the broad push of AI project timelines to 2027 signals about near-term revenue recognition, and which competitive positions stand to benefit most from the shift.

4.8%: The revised IT budget growth forecast for 2026, down from 12.6% in the prior survey, a record low for the series dating to 2020.

The two headline figures from the Morgan Stanley survey sit in apparent contradiction. Consider them side by side:

Investors anchoring valuation models to aggregate IT budget growth as a proxy for Chinese tech demand will misread the signal. The headline contraction and the AI surge are not contradictory. They are the same phenomenon viewed from different angles: a shrinking overall pool in which AI is claiming a rapidly expanding share. The remainder of this analysis disaggregates the paradox rather than papering over it, tracing the compression to its causes and the reallocation to its investor implications.

Three distinct pressure categories are suppressing overall IT budgets. Each operates on a different timeline, which matters for investors assessing how long the compression persists:

The BIS revised licensing policy for semiconductor exports to China, announced in January 2026, shifted advanced chip approvals including Nvidia H200 and AMD MI325X shipments to a case-by-case review process under specific security requirements, formalising the supply constraints that CIOs are now factoring into their compute procurement timelines.

The severity of the drop deserves emphasis. A decline from 12.6% to 4.8% in a single survey cycle is not a modest deceleration. It reflects a convergence of pressures that, taken together, have made CIOs more cautious than at any point in the survey’s history.

Geopolitical and deflationary pressures may persist for multiple years. Technology uncertainty, however, could resolve faster once dominant AI platforms emerge, altering the recovery trajectory for IT budgets along a different timeline.

The Morgan Stanley survey identifies a counterintuitive dynamic: CIOs are deferring non-AI IT commitments partly because the AI landscape is evolving too quickly to confidently lock in multi-year software contracts alongside new AI platforms. The risk of stranding capital on a platform that loses relevance within 18 months is real enough to slow procurement cycles across conventional IT categories.

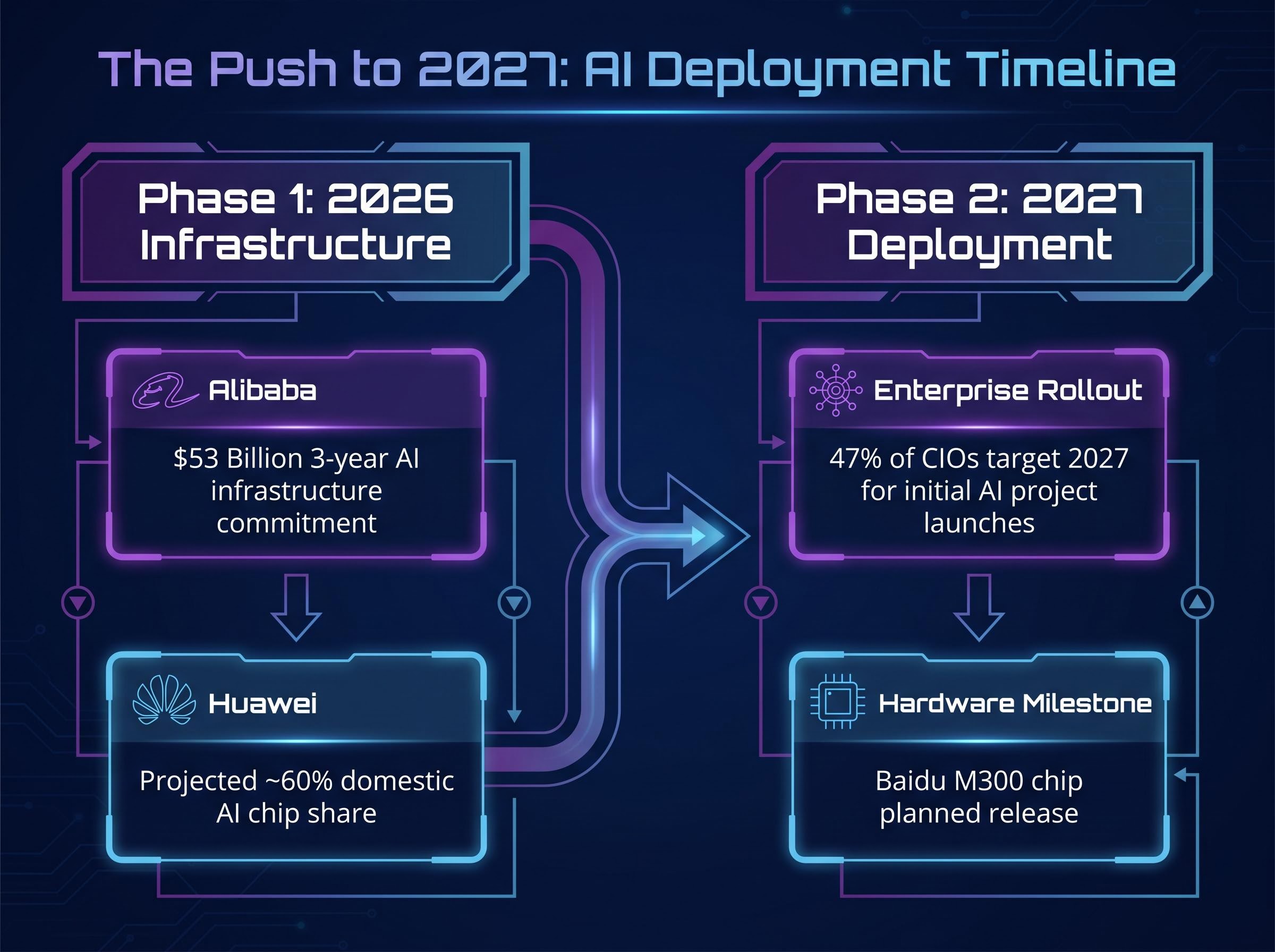

This caution extends into AI deployment itself. 47% of CIOs are now targeting 2027 for initial AI project rollouts, suggesting that even within the AI budget expansion, enterprises are building infrastructure now but deferring full-scale deployment until compute availability and platform maturity improve.

The numbers tell the story before the analysis needs to.

| Category | Prior Survey | Current Survey | Direction |

|---|---|---|---|

| AI share of IT budgets | 6.1% | 12.1% | Up |

| AI funding from software budgets | 10% | 22% | Up |

| Software share of AI spending | 46-47% | 40% | Down |

| CIO AI priority ranking | 30% | 37% | Up |

The share of AI funding sourced from existing software budgets more than doubled, from 10% to 22%. This is the most structurally significant single data point in the survey: AI spending growth is not incremental. It is being funded by cannibalising existing software line items within constrained overall budgets.

Software’s portion of total AI spending declined to 40%, down from 46-47% in earlier surveys, with hardware’s share increasing correspondingly. Global software budget growth in Asia is projected at approximately 4.1%, providing a comparison baseline that shows China’s dynamic is more severe than the regional norm.

For investors holding positions in legacy enterprise software vendors with China exposure, this is a structural headwind rather than a cyclical one. The reallocation reflects a permanent architectural change in how Chinese enterprises build their technology stacks, compounded by localisation mandates and algorithm reviews that limit foreign vendors’ ability to participate in the AI upside.

The hardware and software divergence playing out in China’s enterprise budgets has a direct parallel in global equity markets, where the Morningstar Global Semiconductor Equipment index gained 47.6% year-to-date in 2026 while the Software Applications index fell 22.7%, a spread of more than 70 percentage points that maps precisely to the cannibalisation pattern visible in the CIO survey data.

47% of CIOs now target 2027 for their initial AI project launches. This is not a minor scheduling adjustment. It represents a majority position among surveyed CIOs and signals a broad deferral of AI revenue recognition for vendors.

The causal chain is identifiable:

Alibaba’s approximately $53 billion three-year AI infrastructure commitment confirms that the capex cycle is underway. Citi raised its 2026-2030 global AI capex estimate to $8.9 trillion, contextualising China’s infrastructure buildout within a broader investment wave. The spending is real. The revenue is later.

Huawei’s Ascend series is projected to capture approximately 60% of China’s domestic AI chip market in 2026, positioning it as the primary enabler of the 2027 deployment wave. Huawei’s execution on chip production and ecosystem development is the critical path variable for the entire enterprise AI timeline.

Asian chipmakers and AI infrastructure producers are capturing a disproportionate share of the global capex wave: the MSCI AC Asia Pacific IT Index trades at a forward P/E of 12.14x, roughly half the Nasdaq 100’s multiple, despite earnings growth forecasts running nearly three times faster, a valuation gap that reflects both the opportunity and the geopolitical risk premium embedded in China-adjacent supply chains.

Baidu’s M300 chip, planned for 2027 through its Kunlunxin subsidiary, represents a secondary milestone for enterprises that require training-grade domestic compute. Until these domestic compute platforms reach sufficient scale, the gap between AI infrastructure investment and AI application revenue will persist.

Investors pricing AI monetisation into Chinese tech earnings in 2026 are likely early. The survey data suggests 2027 is the more realistic inflection point, shifting the relevant valuation horizon forward by roughly 12 months.

For investors watching the reallocation from the hardware side, AI capex sustainability is the central risk question: the four largest hyperscalers are collectively spending $610 billion to $650 billion in 2026, nearly double 2024 levels, and investor scrutiny is shifting from infrastructure deployment volumes to proof of commercial software monetisation and return on investment.

The CIO survey data maps a differentiated competitive picture that diverges from brand recognition rankings.

Alibaba emerges as the primary beneficiary. CIOs choosing Alibaba for AI deployment assistance rose to 41%, up from 32% in the prior survey. 30% of CIOs expect Alibaba to capture the greatest incremental AI expenditure in fiscal 2026, placing it first among all respondents. ByteDance’s Doubao model ranked second, with 27% of CIOs selecting it for greatest incremental spend.

More than 50% of CIOs anticipate cloud service prices will increase over the next 12 months, a tailwind for both Alibaba Cloud and ByteDance’s cloud infrastructure operations.

DeepSeek’s projected market share gain fell to 18% of CIOs selecting it, down sharply from 33% in the preceding survey. The decline reflects DeepSeek’s research-oriented posture and slower release cadence rather than a broad loss of credibility, but the directional shift is notable.

| Company | CIO AI Deployment Preference | Expected AI Spend Capture | Key Competitive Rationale |

|---|---|---|---|

| Alibaba | 41% (up from 32%) | 30% (ranked 1st) | Cloud infrastructure scale, $53B+ AI investment commitment |

| ByteDance | Strong (Doubao model) | 27% (ranked 2nd) | Model development momentum, cloud infrastructure growth |

| Huawei | Hardware-led positioning | ~60% domestic AI chip share | Ascend chip ecosystem, beneficiary of Nvidia supply disruption |

| DeepSeek | 18% (down from 33%) | Declining CIO selection | Research-focused posture, slower commercial release cadence |

The survey creates a granular basis for position sizing across Chinese tech names that aggregate sector exposure alone cannot provide.

China’s AI budget doubling is occurring within a global AI capex supercycle. Citi’s $8.9 trillion estimate for 2026-2030 global AI capital expenditure frames the scale. China’s total AI investment reached an estimated $125 billion in 2025, with the trajectory extending into 2026-2027. U.S. private AI investment stood at $285.9 billion in 2025 versus China’s $12.4 billion in private investment, illustrating the structural gap that Chinese state and hyperscaler capital is attempting to bridge.

China’s infrastructure buildout is unfolding inside a global AI capex supercycle in which Amazon, Microsoft, Alphabet, and Meta collectively spent $130 billion on AI capital expenditure in Q1 2026 alone, with full-year combined projections reaching $725 billion and a $1 trillion annual run rate targeted for 2027.

For global enterprise software vendors with China revenue exposure, the cannibalisation dynamic operates alongside regulatory constraints. Localisation mandates for data storage and algorithm reviews limit the ability of foreign vendors to capture the AI upside even as their legacy revenue lines face budget reallocation.

China’s AI market is undergoing a genuine structural shift. The Morgan Stanley survey data makes that unambiguous. The revenue inflection, however, is approximately 12 months further out than current market pricing implies for most AI plays.

Three structural dynamics make this durable rather than cyclical: macro-driven budget compression that forces prioritisation, software-to-AI cannibalisation that permanently redirects enterprise spending, and a delayed deployment timeline anchored to domestic compute readiness.

– Overall IT budget growth: 4.8% (record low) – Projected AI share of IT budgets: 12.1% (near doubling) – AI funding sourced from software budgets: 22% (cannibalisation acceleration) – CIOs targeting 2027 deployment: 47% – Alibaba CIO preference rating: 41% (clearest single-name signal)

The opportunity is real. The timing is later than the capex headlines suggest. The winners are identifiable from the survey data, with Alibaba’s 41% CIO preference rating standing as the clearest single-name signal in the dataset. Investors positioned to avoid both errors, dismissing the China AI story based on headline budget compression or overweighting near-term revenue potential based on infrastructure announcements, stand to capture the reallocation’s value on the more realistic 2027 timeline.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced are subject to market conditions and various risk factors. Forward-looking statements, including AI deployment timelines and budget forecasts, are based on survey data and are subject to change based on market developments and policy shifts.

—

China's AI market is undergoing a structural reallocation: overall IT budget growth has fallen to a record-low 4.8%, but AI's share of those budgets is projected to nearly double from 6.1% to 12.1% in 2026, according to the Morgan Stanley AlphaWise 1H26 China CIO Survey of 60 chief information officers.

Three pressures are compressing overall IT budgets: U.S. export controls restricting advanced semiconductor supply, domestic deflationary conditions reducing corporate commitment to multi-year contracts, and rapidly shifting AI platforms making CIOs reluctant to lock in conventional software spending alongside new AI platforms.

Alibaba leads with 41% of CIOs selecting it for AI deployment assistance and 30% expecting it to capture the greatest incremental AI spend; ByteDance ranks second at 27%, while Huawei is positioned to capture approximately 60% of China's domestic AI chip market through its Ascend series.

47% of CIOs are targeting 2027 for their initial AI project launches, meaning revenue recognition for software-layer and application-layer vendors is likely pushed out by roughly 12 months relative to current market pricing, as GPU supply constraints and domestic compute readiness remain limiting factors.

The share of AI funding sourced directly from existing software budgets more than doubled from 10% to 22% in a single survey cycle, and software's portion of total AI spending fell to 40% from 46-47%, meaning AI growth is being funded by cutting conventional enterprise software line items rather than through incremental budget increases.