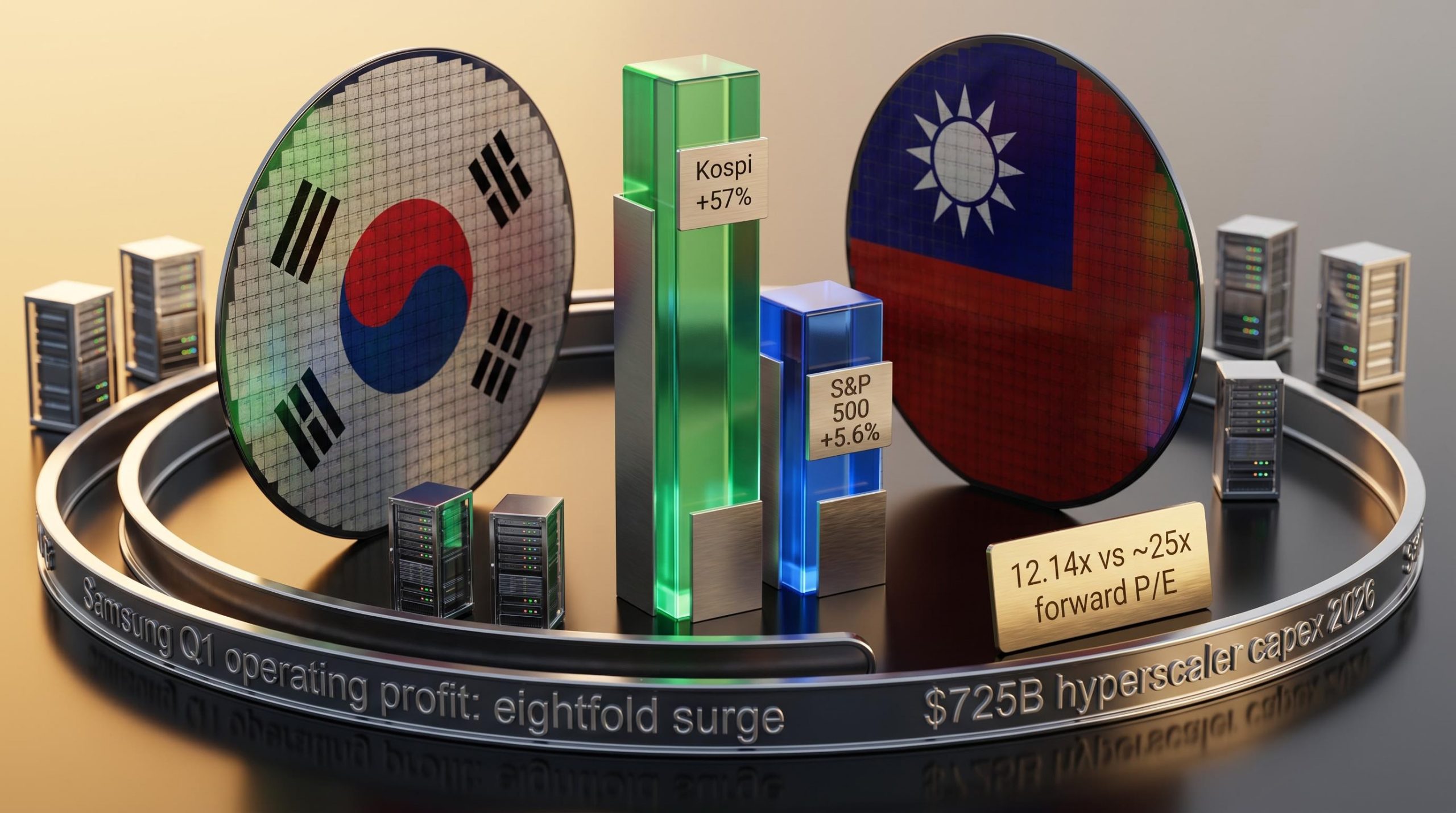

In the first four months of 2026, South Korea’s Kospi gained approximately 57% while the S&P 500 rose roughly 5.6%. That is not a rounding error or a currency anomaly. It is the visible surface of a structural shift in where artificial intelligence capital is flowing and who captures it.

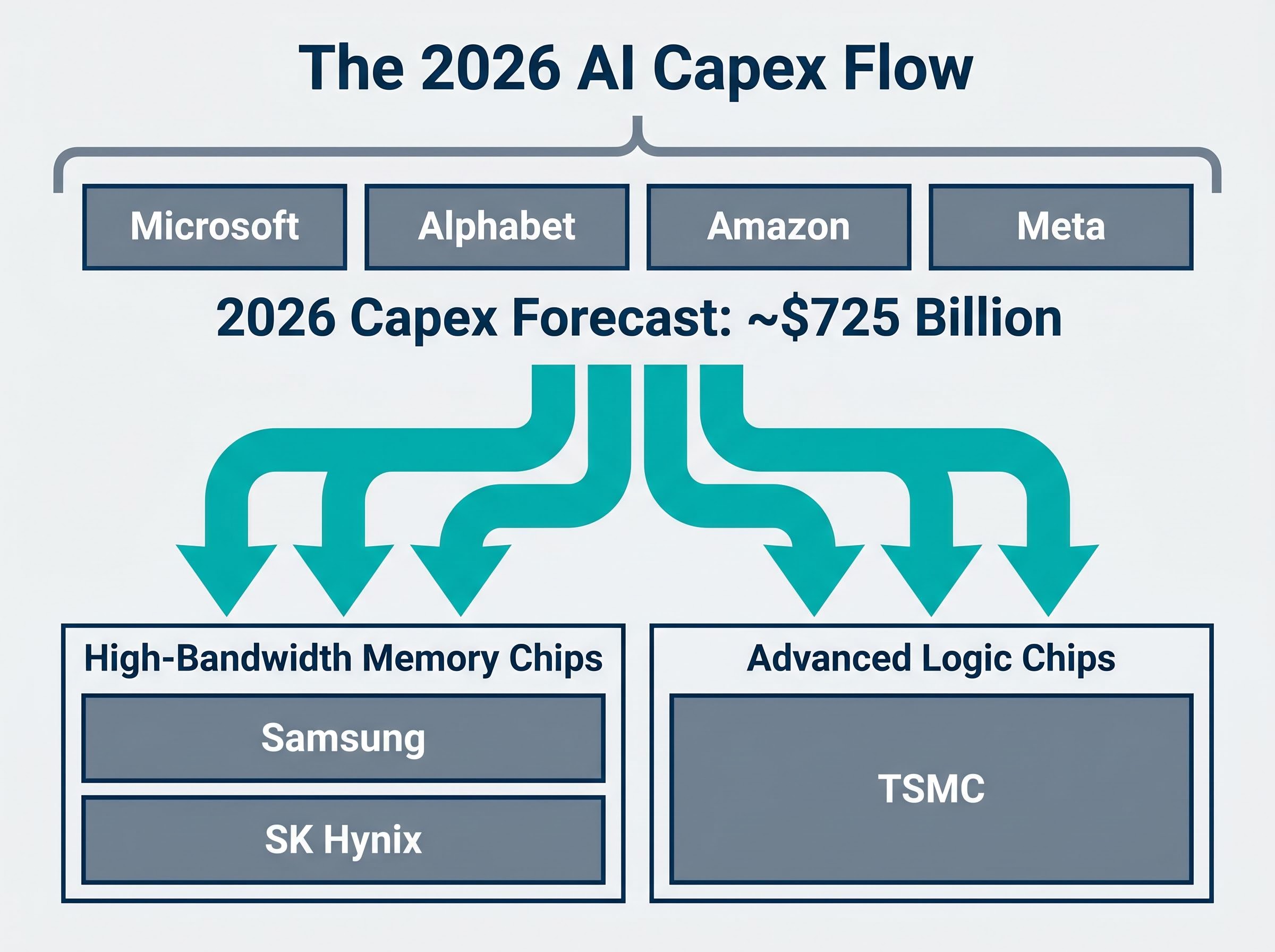

Global hyperscalers, Microsoft, Alphabet, Amazon, and Meta, have collectively revised their 2026 capital expenditure forecasts upward to approximately $725 billion. The primary recipients of that spending are not American software companies. They are semiconductor fabricators and memory chip manufacturers concentrated in South Korea and Taiwan, whose hardware forms the physical substrate on which every AI model runs.

What follows is an analysis of the investment logic behind Asian tech outperformance: the company-level earnings evidence, the valuation case, the structural factors that could sustain or undermine the trade, and the risks global investors must weigh. The aim is a coherent framework for evaluating North Asian tech exposure within an AI-driven global portfolio.

The $725 billion catalyst: how hyperscaler AI spending created a hardware dividend in Asia

The spending decisions were made in boardrooms in Redmond, Mountain View, Seattle, and Menlo Park. The money landed in Seoul and Taipei.

Four companies are driving the capital wave:

- Microsoft: expanded AI data centre buildout across multiple continents

- Alphabet: accelerated custom chip and cloud infrastructure investment

- Amazon: increased AWS capacity spending tied to generative AI workloads

- Meta: scaled compute requirements for large language model training

Their combined 2026 capex forecast of approximately $725 billion functions as a floor rather than a ceiling, given that each has revised projections upward since the start of the year. The downstream recipients are concentrated: training and inference workloads require high-bandwidth memory chips from Samsung and SK Hynix, and advanced logic chips fabricated by TSMC. These are not commodity suppliers with dozens of competitors. They are a small group of manufacturers whose capacity constrains the pace of AI deployment.

The scale of AI infrastructure spending now represents approximately 2% of US GDP, with roughly 75% of the capital directed toward physical hardware and data centre construction rather than software, a ratio that structurally favours fabricators and memory suppliers over application developers.

The earnings confirmation arrived in rapid succession. SK Hynix reported strong first-quarter 2026 results on 23 April 2026, driven by soaring AI memory chip prices. One week later, the evidence sharpened further.

Samsung reported first-quarter 2026 operating profit surging more than eightfold, disclosed on 30 April 2026, marking a milestone earnings event driven by sustained AI-linked memory demand.

As of January 2026, TSMC and Samsung had already gained 8-16% year-to-date; the first-quarter earnings season accelerated those gains considerably. The demand cascade from hyperscaler capex to chip supplier revenue is now empirically verifiable, not speculative.

When big ASX news breaks, our subscribers know first

From Seoul to Taipei: what the earnings scoreboard reveals about AI’s geography

The earnings data from North Asia is not a collection of isolated wins. It is a coordinated body of evidence pointing to a regional earnings acceleration that outpaces its American peers by a wide margin.

| Benchmark | EPS Growth Forecast (12-month, as of Jan 2026) | YTD Equity Gain (2026) |

|---|---|---|

| South Korea benchmark | +79% | ~57% (Kospi) |

| Taiwan benchmark | +36% | ~34% (Taiex) |

| Nasdaq | +28% | ~5.6% (S&P 500) |

| Samsung | Eightfold Q1 profit surge | ~84% |

When South Korean benchmark earnings are forecast to grow at nearly three times the Nasdaq rate, the Kospi’s outperformance over the S&P 500 becomes less surprising and more predictable. The gap between the earnings trajectories and the equity performance is, if anything, consistent rather than anomalous.

Company-level confirmation: Samsung, TSMC, and SK Hynix

Samsung’s first-quarter 2026 operating profit surge of more than eightfold was the single most striking data point of the earnings season, reflecting the pricing power of AI-linked memory at scale. The company’s full-year 2026 gain of approximately 84% prices in continued demand, yet the earnings growth rate has so far kept pace with the share price appreciation.

TSMC drew approximately six brokerage price-target upgrades since the start of 2026, a signal of institutional conviction in the foundry’s forward profitability. Its structural position as the dominant advanced logic fabricator means it benefits regardless of which specific AI application or model architecture wins adoption.

SK Hynix reported first-quarter results on 23 April 2026 that confirmed soaring AI memory chip prices, completing a three-company, two-country earnings window that constitutes sector-wide validation rather than single-stock noise.

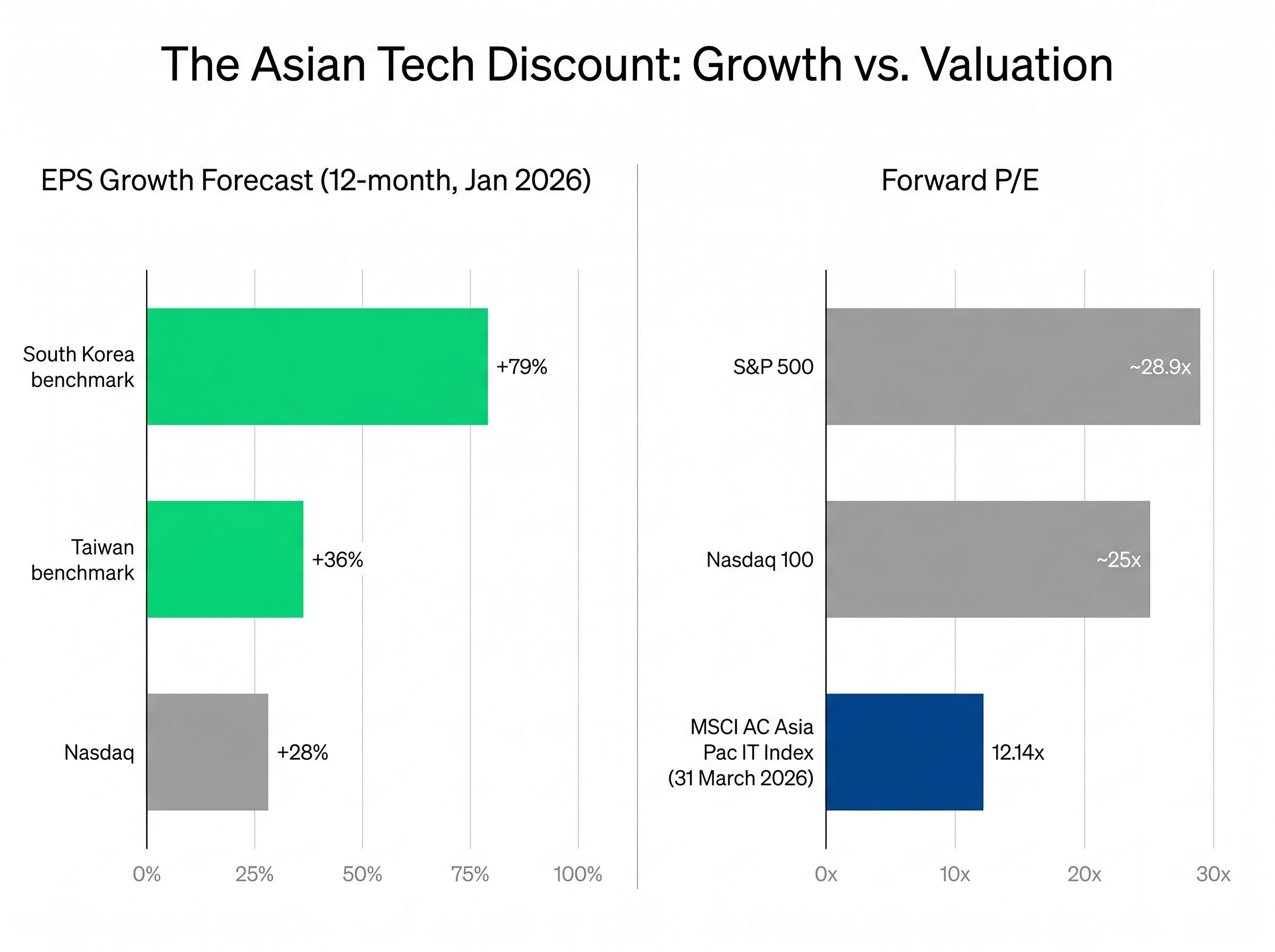

Why Asian tech trades at half the multiple of its American peers

A sector growing earnings at nearly three times the pace of the Nasdaq, yet trading at half the forward multiple, presents an apparent contradiction. The numbers are stark.

| Benchmark | Forward P/E | YTD Performance (2026) |

|---|---|---|

| MSCI AC Asia Pac IT Index | 12.14x | Outperforming Nasdaq since end-2024 |

| Nasdaq 100 | ~25x | ~5.6% |

| Philadelphia Semiconductor Index | ~25x | Trailing Asian tech peers |

| S&P 500 | ~28.9x | ~5.6% |

The MSCI AC Asia Pacific Information Technology Index trades at a forward price-to-earnings ratio of 12.14x as of 31 March 2026, compared with approximately 25x for both the Nasdaq 100 and the Philadelphia Semiconductor Index.

The MSCI AC Asia Pacific IT Index factsheet, published as of 31 March 2026, places the forward P/E at 12.14x, providing the primary index-level data point that anchors the valuation gap argument against the Nasdaq 100’s approximately 25x multiple.

The discount is not new, and it is not accidental. Three structural forces compress Asian tech multiples relative to American peers: geopolitical risk premia (particularly around Taiwan), the perception that semiconductor earnings are cyclical rather than secular, and home-market investor bias that keeps global allocations to Asian tech below what earnings growth would otherwise justify.

Goldman Sachs strategists are positioned overweight on Korean and Taiwanese tech, including TSMC and Samsung, specifically on this valuation-plus-earnings-growth argument. The firm maintains overweight positioning across Korea, China, and India. The iShares MSCI Emerging Markets ETF recorded net inflows of approximately $15 billion year-to-date through May 2026, suggesting institutional capital is acting on the same thesis.

A company growing earnings at twice the rate of its peers while trading at half the multiple is the fundamental definition of a value-growth combination. That the gap persists even after strong 2026 performance is what keeps the institutional rotation analytically defensible.

Understanding why South Korea and Taiwan sit at the centre of the AI hardware trade

The performance numbers reflect an industrial reality: South Korea and Taiwan manufacture products that cannot be easily sourced elsewhere, and AI has intensified demand for precisely those products.

The supply chain runs in a specific sequence:

- Hyperscalers allocate capex to AI infrastructure

- Data centres require advanced processors and accelerators

- Those processors depend on advanced logic chips fabricated by TSMC

- Training those AI models requires high-bandwidth memory (HBM) from Samsung and SK Hynix

- Earnings growth at these suppliers flows into index returns for Korean and Taiwanese benchmarks

This sequence is not a temporary alignment. Gary Tan of Allspring Global Investments has framed AI as a multiyear secular growth driver, placing North Asia at the forefront for the medium term. South Korea sources approximately 70% of crude oil imports from the Middle East, which makes the AI-driven export revenue from semiconductors an increasingly significant counterweight in the national economic profile.

Advanced logic: TSMC’s foundry advantage

A chip foundry manufactures semiconductor chips designed by other companies, functioning as a contract manufacturer for processors, graphics chips, and AI accelerators. TSMC leads this field with its advanced process nodes (3nm and progressing toward 2nm), which are manufacturing techniques that pack more computing power into smaller chip areas. Replicating this capability requires billions in capital expenditure and years of engineering iteration, which is why competitors remain well behind.

For investors, TSMC’s position offers a form of foundry agnosticism: it profits regardless of which AI chipmaker or AI application wins, because nearly all paths to AI deployment require its fabrication services.

High-bandwidth memory: South Korea’s HBM position

High-bandwidth memory (HBM) is a type of memory chip specifically designed for the massive data throughput that AI model training demands. It stacks memory layers vertically to achieve data transfer speeds that conventional memory cannot match.

Samsung and SK Hynix hold dominant combined market share in HBM, and both have reported that memory pricing has been particularly strong through 2025-2026 as AI training infrastructure buildouts outstrip available supply. This pricing dynamic has driven the profit surges visible in both companies’ recent quarterly results.

AI-driven supply constraints extend beyond HBM and advanced logic into the broader storage market, where major hardware suppliers sold out production capacity through 2026 and enterprise hardware prices for high-capacity models surged up to 60%, with further increases projected, a pattern that confirms the demand shock from hyperscaler spending is propagating across the entire hardware stack rather than concentrating at the highest-specification layers.

What could break the trade: geopolitical fault lines and macro pressure points

The valuation discount on Asian tech is not irrational. It prices real risks, and those risks deserve the same analytical weight as the bull case.

Four categories of risk warrant monitoring:

- Taiwan geopolitical escalation: The most structurally significant tail risk. Vey-Sern Ling of Union Bancaire Privée flagged Taiwan geopolitics as a primary concern in commentary timed to April 2026 market developments. The easing of war-tension rhetoric in April 2026 was itself a catalyst for the latest fund inflow wave into Asian AI stocks; a reversal of that easing would trigger the opposite flow.

- AI capex pullback by hyperscalers: If Microsoft, Alphabet, Amazon, or Meta revise spending guidance downward, the demand catalyst underlying the entire thesis reverses. The $725 billion figure is a projection, not a commitment.

- U.S.-China trade policy volatility: Tariff uncertainty remains a persistent source of volatility for the broader emerging market tech complex, with Chinese equities particularly exposed but regional sentiment also affected.

- South Korean domestic political risk: Analysts have flagged domestic political developments as a secondary factor that could affect investor confidence in Korean markets.

The hardware capex cycle is projected to push hyperscaler capital expenditures from approximately 50% of operating cash flow in 2024 to 90% by 2027, a reallocation so large that software monetisation lag, where application revenue fails to keep pace with hardware deployment, has emerged as the primary near-term risk to the spending trajectory that drives Asian chip supplier revenues.

Taiwan Strait tensions ranked as the top geopolitical risk for 2026 by a prominent Chinese think tank, a designation that connects directly to the valuation discount embedded in Asian tech multiples and helps explain why institutional investors treat the 12.14x forward P/E as compensation for tail risk rather than a straightforward mispricing.

No specific new Taiwan Strait or U.S.-China policy developments have been independently confirmed as of early May 2026. This is an area where real-time monitoring remains necessary. The 12.14x forward P/E on Asian tech is partly a rational risk premium for these contingencies, and treating the low multiple as a free lunch would ignore what it prices in.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The valuation gap is still open, and the earnings cycle is still running

The analytical thread connects: hyperscaler AI capex creates concentrated demand at a small number of North Asian chip manufacturers; those manufacturers report earnings growth that outpaces American tech peers by wide margins; and despite that growth, Asian tech trades at roughly half the forward multiple of the Nasdaq.

The broader emerging markets picture reinforces the pattern. The MSCI Emerging Markets Index is up approximately 14% in 2026, compared with roughly 5.6% for the S&P 500. The Kospi’s 57% gain and the Taiex’s 34% advance are the most visible expressions of that divergence, and the iShares MSCI Emerging Markets ETF’s approximately $15 billion in year-to-date net inflows suggests institutional capital recognises the rotation.

The thesis rests on three pillars:

- Capex catalyst: $725 billion in hyperscaler AI spending flowing to a concentrated group of Asian suppliers

- Earnings confirmation: Q1 2026 results from Samsung, TSMC, and SK Hynix validated the demand trajectory

- Valuation gap: Asian tech at 12.14x forward P/E versus 25x for U.S. equivalents, with faster earnings growth

The risks, particularly Taiwan geopolitics and the possibility of capex revisions, are real and not priced to zero. Both Goldman Sachs and Allspring Global Investments have characterised this as a multiyear trade rather than a single-quarter event, which means the question for investors is not whether the data supports engagement but at what risk weight and entry point.

For investors considering how to access the North Asian tech thesis through exchange-traded funds, our dedicated guide to ASX Asia ETF selection examines three funds, VAE, IAA, and ASIA, which delivered a 46-percentage-point spread in one-year returns, covering how index construction differences, fee compounding, and unintended TSMC concentration across multiple holdings affect risk-adjusted outcomes.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.