Samsung Rout Anchors Global Selloff as Bonds and Stocks Fall Together

6 mins ago

Brent crude surged close to $108.75 per barrel during trading on 15 May 2026, a near-3% single-day jump that capped weeks of accumulating geopolitical pressure on global oil markets. The rally is not a one-day shock. It is the latest expression of a supply crisis that began on 2 March 2026, when the Strait of Hormuz, the world’s most consequential oil chokepoint, was effectively closed following U.S. and Israeli strikes on Iran. President Trump’s public statement that the United States does not require the strait to remain open has since added a fresh layer of uncertainty about Washington’s appetite for a negotiated resolution. What follows explains the mechanics behind the surge, why analysts are increasingly flagging demand destruction as a counterforce to further price gains, and what the path forward looks like under different diplomatic scenarios.

The Strait of Hormuz has been effectively closed for more than ten weeks. The closure, triggered by U.S. and Israeli military strikes on Iran on 2 March 2026, is not a risk scenario or a threat of disruption. It is a confirmed, ongoing blockage of the single most important maritime oil transit route on the planet.

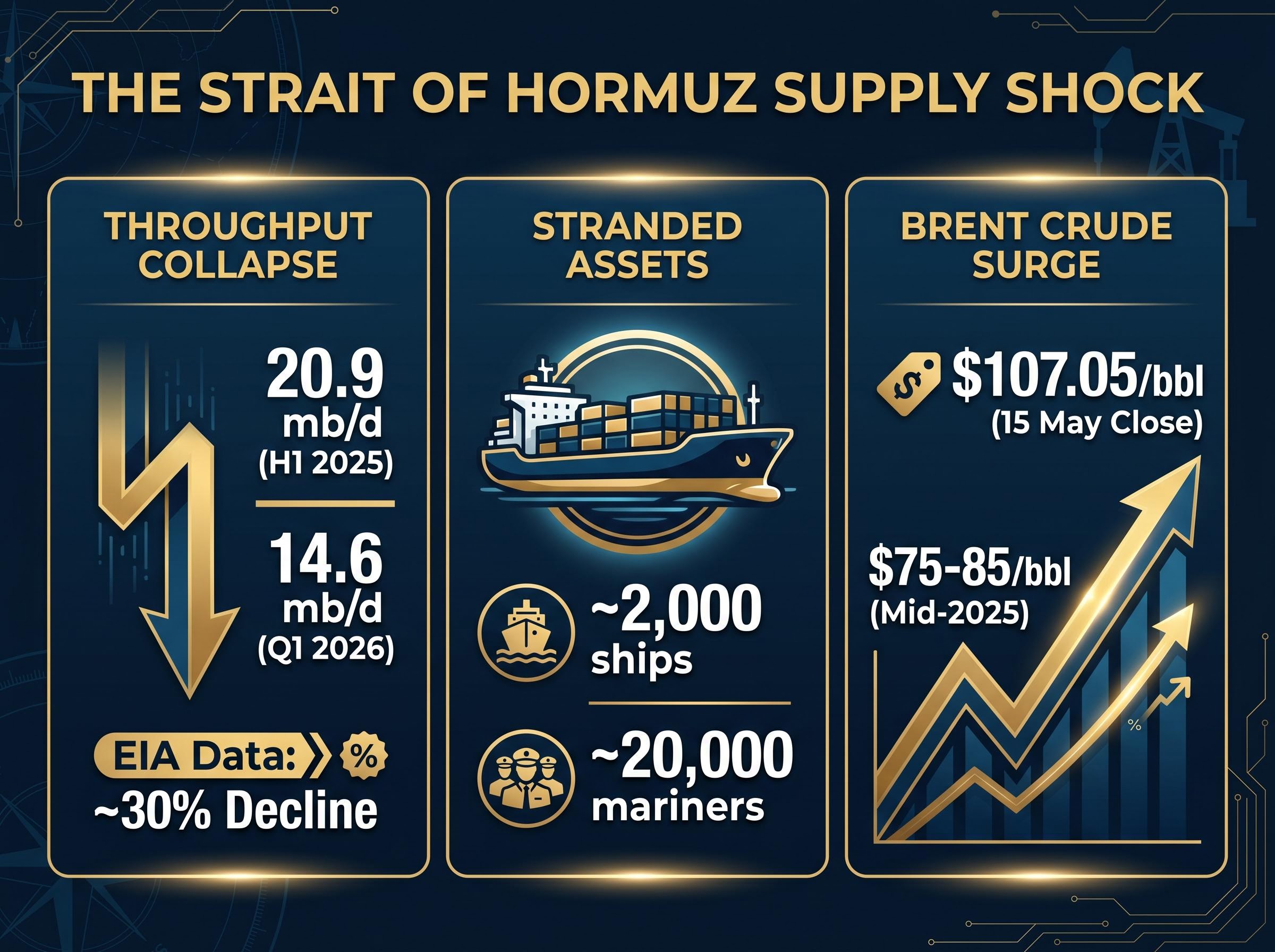

The scale is visible in the throughput data. Pre-crisis, the strait handled an average of approximately 20.9 million barrels per day (mb/d) of crude and condensate during the first half of 2025. By the first quarter of 2026, flows had fallen to approximately 14.6 mb/d, a decline of nearly 30%, according to U.S. Energy Information Administration (EIA) figures.

The EIA transit volume data for the Strait of Hormuz confirms the waterway’s structural importance to global supply chains, with pre-crisis figures placing daily crude and condensate flows at roughly one fifth of world consumption, a concentration that leaves no viable substitute routing capable of absorbing a full closure at scale.

Strait of Hormuz flows fell to approximately 14.6 mb/d in Q1 2026, down nearly 30% from the pre-crisis baseline of 20.9 mb/d, per EIA data.

The human and logistical toll compounds the supply picture. Approximately 2,000 ships and 20,000 mariners remain stranded, and current reports suggest the strait may not fully reopen until the second half of 2026.

| Metric | Pre-crisis | Current (Q1 2026) |

|---|---|---|

| Hormuz throughput | ~20.9 mb/d | ~14.6 mb/d |

| OPEC+ production | Pre-crisis baseline | Down ~30% |

| Brent crude | ~$75-85/bbl (mid-2025 range) | $107.05/bbl (15 May close) |

The Strait of Hormuz is a narrow waterway connecting the Persian Gulf to the Gulf of Oman. It is the only sea route through which Gulf oil producers, including Saudi Arabia, Iraq, the UAE, and Kuwait, can move crude to the open ocean and onward to global markets. In normal conditions, it carries roughly one fifth of global daily oil supply, making it the single most concentrated point of energy infrastructure risk in the world.

Saudi Arabia and the UAE have been rerouting some exports via overland pipelines and alternative maritime routes that bypass the strait. These alternatives provide a partial offset, but pipeline infrastructure was never built to replace the full volume that moved by sea. The compensation is structurally limited.

A closure is qualitatively different from elevated risk. When the strait is shut, insurers exit coverage for the region, tanker operators stop routing vessels through, and the physical infrastructure of global oil logistics breaks down. Even a diplomatic resolution would not immediately restore normal flows. Three barriers stand between any announced reopening and actual normalisation:

Diplomatic channels are active. Iran is reviewing a U.S. proposal aimed at ending the conflict, and parallel U.S.-brokered talks between Israel and Lebanon were under way around 14-15 May. President Trump and Chinese President Xi Jinping met at a summit in Beijing on 14 May 2026, where both leaders expressed interest in resolving the Iran conflict, though no concrete outcomes emerged.

The diplomatic gap, however, remains wide. Iran has publicly stated three conditions for any agreement:

The diplomatic breakdown on 11 May, when Trump rejected Iran’s nuclear counteroffer and Brent surged more than 3% in a single session, established the price baseline from which the 15 May rally extended, making the sequence of failed negotiating rounds the direct precursor to current market levels.

The sovereignty demand poses a particular difficulty. Publicly acknowledging Iranian sovereign control over an international shipping lane would set a precedent that Washington has historically refused to entertain, and the political cost of doing so in the current environment would be substantial.

President Trump has stated he is “losing patience” with Iran and that the United States does not require the Strait of Hormuz to remain open. Deutsche Bank strategists flagged this rhetoric as a factor that caused oil markets to lose upward momentum, introducing fresh uncertainty about the ceiling for geopolitical risk premiums.

The diplomatic timeline is the single most consequential variable for energy prices. Until Iran’s conditions and Washington’s red lines move closer together, the supply disruption persists.

The disruption is no longer confined to the commodity markets. It has moved into balance sheets, fuel invoices, and sector-level earnings guidance.

OPEC+ production fell to a new low in April 2026, declining approximately 30% from pre-crisis levels, according to a Reuters survey dated 11 May 2026. The bloc’s heavy dependence on Strait of Hormuz export routing means that even members with spare production capacity cannot move barrels to market at pre-crisis rates. Saudi Arabia and the UAE continue rerouting via pipeline and alternative maritime routes, but these channels provide only a partial offset.

Emergency reserve releases totalling approximately 280 million barrels have failed to halt the inventory drawdown, with global stocks drawing at 8.5 million barrels per day in Q2 2026 and usable buffer estimated at only around 800 million barrels by JPMorgan, a combination that strips governments of the policy lever most commonly cited as a backstop against supply disruption.

| Metric | Pre-crisis level | Current level |

|---|---|---|

| Hormuz daily flows | ~20.9 mb/d | ~14.6 mb/d (Q1 2026) |

| OPEC+ output | Pre-crisis baseline | Down ~30% (April 2026) |

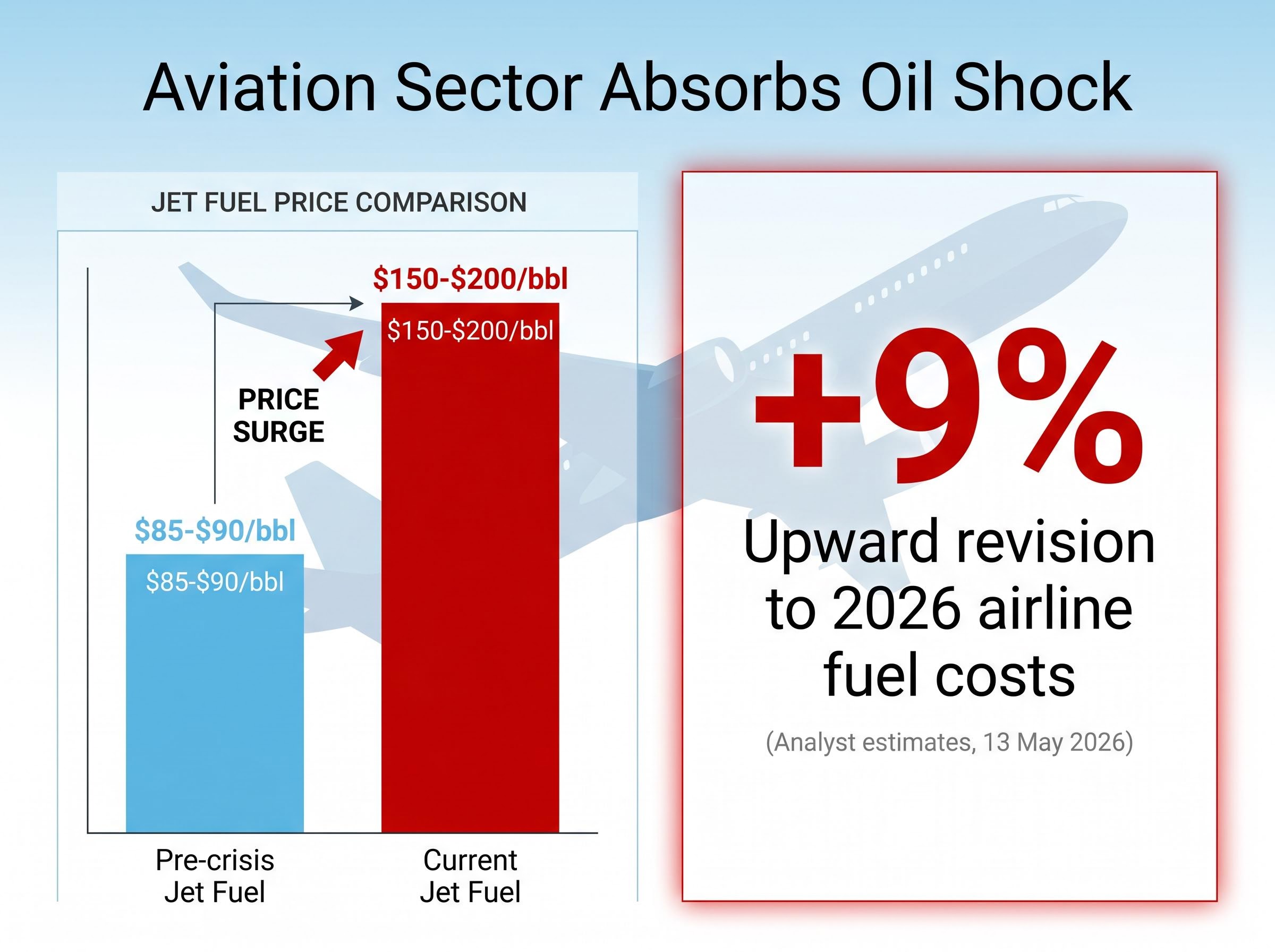

| Jet fuel price | ~$85-90/bbl | ~$150-200/bbl |

The transmission to downstream sectors is already quantifiable. Jet fuel prices have surged from a pre-crisis range of approximately $85-90 per barrel to $150-200 per barrel, roughly doubling input costs for the global aviation industry.

Analyst estimates dated 13 May 2026 show that 2026 airline fuel cost expectations have been revised upward by approximately 9% as a direct consequence of the crude oil surge. Carriers with limited forward hedging at pre-crisis price levels face the sharpest margin exposure, as they are absorbing the full spot-market increase with no contractual cushion. Retail fuel prices are also elevated globally, though precise per-litre figures vary by region and are not yet uniformly available from open sources.

The analytical tension at the centre of the oil market outlook is genuine, and both sides of the argument carry weight.

PVM Oil Associates analyst Tamas Varga has observed that market attention is progressively shifting toward potential demand destruction, which helps explain why oil prices have shown hesitancy to revisit prior peaks even as inventories remain extremely low.

Brent crude reached an intraday high of $108.75 per barrel on 15 May 2026 before closing near $107.05. West Texas Intermediate (WTI) crude settled at approximately $104.42 per barrel. The day’s move represented a gain of roughly 3%, building on a broader weekly advance.

J.P. Morgan has forecast Brent in the low $100s through 2026 under a scenario where the strait reopens around June 2026. Current prices are already testing the upper boundary of that range, which suggests the market is pricing in either a delayed reopening or a higher sustained risk premium than J.P. Morgan’s base case assumes.

Six simultaneous cushioning mechanisms, including strategic reserve drawdowns, Chinese stockpile resales, and sanctions waivers, have kept Brent below the $150-$200 forecasts that circulated when the closure began, but each of these offsets is capacity-constrained and cannot absorb an escalation in disruption duration indefinitely.

The escalation scenario remains live. If diplomatic talks collapse and military posturing intensifies, further price increases are possible. But the demand destruction dynamic places a real ceiling on how far prices can run. At some point, elevated energy costs reduce industrial output, suppress consumer spending, and erode the very demand that supports the price. Deutsche Bank strategists noted that markets lost upward momentum after Trump’s statement that the U.S. does not require the strait to remain open, a signal that geopolitical uncertainty can cut both ways.

The contest between supply fear and demand destruction is not theoretical. It is the mechanism that will determine the price path from here.

The current price environment reflects more than the physical supply gap. Embedded risk premiums tied to diplomatic uncertainty, insurance market dislocation, and tanker routing disruption will persist beyond any ceasefire announcement. Even a reopening of the strait would not immediately normalise flows, given the vessel backlog, insurance re-entry timelines, and infrastructure assessments required before full operations resume.

The Hormuz risk premium embedded in current Brent prices reflects more than the physical barrel shortfall; VLCC daily hire rates tracking around $110,000 per day and the near-total withdrawal of commercial war risk insurance represent a structural repricing of maritime energy logistics that will decompress slowly even after any ceasefire announcement.

Three variables will determine what happens next:

Supply fears are real and grounded in verified data. But a price that outruns economic tolerance will eventually generate its own correction. That tension is not a forecast. It is the framework through which every future Hormuz headline should be read.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including analyst forecasts and diplomatic scenario assessments, are speculative and subject to change based on market developments and geopolitical conditions.

The Strait of Hormuz is a narrow waterway connecting the Persian Gulf to the Gulf of Oman, carrying roughly one fifth of global daily oil supply. Its closure since 2 March 2026 has cut throughput by nearly 30%, from approximately 20.9 million barrels per day to 14.6 million barrels per day, directly driving the surge in global crude prices.

Brent crude reached an intraday high of $108.75 per barrel on 15 May 2026, driven by the continued closure of the Strait of Hormuz, a 30% drop in OPEC+ production, failed diplomatic negotiations between the U.S. and Iran, and rapidly depleting global strategic reserves.

Iran has publicly stated three conditions for any agreement: U.S. reparations for damages from the strikes, comprehensive sanctions relief, and formal recognition of Iranian sovereignty over the Strait of Hormuz. The sovereignty demand is considered the most difficult obstacle, as Washington has historically refused to acknowledge Iranian control over an international shipping lane.

Jet fuel prices have roughly doubled from a pre-crisis range of approximately $85-90 per barrel to $150-200 per barrel, and analyst estimates from 13 May 2026 show that 2026 airline fuel cost expectations have been revised upward by approximately 9%. Carriers with limited forward hedging face the sharpest margin exposure.

Even after a diplomatic resolution, normalisation would require sequencing and inspecting approximately 2,000 stranded vessels, marine insurers reassessing risk and reissuing coverage (a process taking weeks), and physical inspection of port and loading facilities before full operations can resume.