While Nvidia commands a $4.8 trillion market cap and Broadcom’s AI chip revenue doubled year-over-year, one of the original architects of the AI revolution trades at just 29x earnings, cheaper than every other member of the Magnificent Seven.

Alphabet’s Q1 2026 earnings, released in late April 2026, gave investors a detailed look at how the company monetises artificial intelligence across multiple verticals. The results were striking: Google Cloud grew 63% year-over-year, outpacing both Azure (40%) and AWS (28%), while Waymo crossed 500,000 autonomous rides per week. Most investors still frame Alphabet as a search-and-advertising business with AI upside. The Q1 data suggests that framing is increasingly obsolete.

What follows is an analysis of why Alphabet’s structure as a multi-vertical AI company makes it a fundamentally different kind of bet than the semiconductor plays dominating AI headlines, what the numbers say about where value is building, and what risks investors should weigh before acting.

The cloud race has a new leader, and it is not who most investors expected

For most of the past decade, the cloud infrastructure rankings have been stable: Amazon AWS first, Microsoft Azure second, Google Cloud third. Q1 2026 disrupted that ordering on the metric that matters most to growth investors: the rate of acceleration.

Google Cloud posted $20.0 billion in quarterly revenue, up 63% year-over-year. Azure grew 40%. AWS grew 28%. The gap is not marginal.

CRN’s Q1 2026 cloud earnings comparison, citing Synergy Research Group market share data, confirms Google Cloud’s 63% growth rate against Azure’s 39% and AWS’s 28%, validating the competitive gap as a structural shift rather than a one-quarter statistical anomaly.

| Provider | Q1 2026 YoY Growth | Q1 2026 Revenue | Cloud Backlog |

|---|---|---|---|

| Google Cloud | 63% | $20.0B | $460B+ |

| Microsoft Azure | 40% | N/A | N/A |

| Amazon AWS | 28% | N/A | N/A |

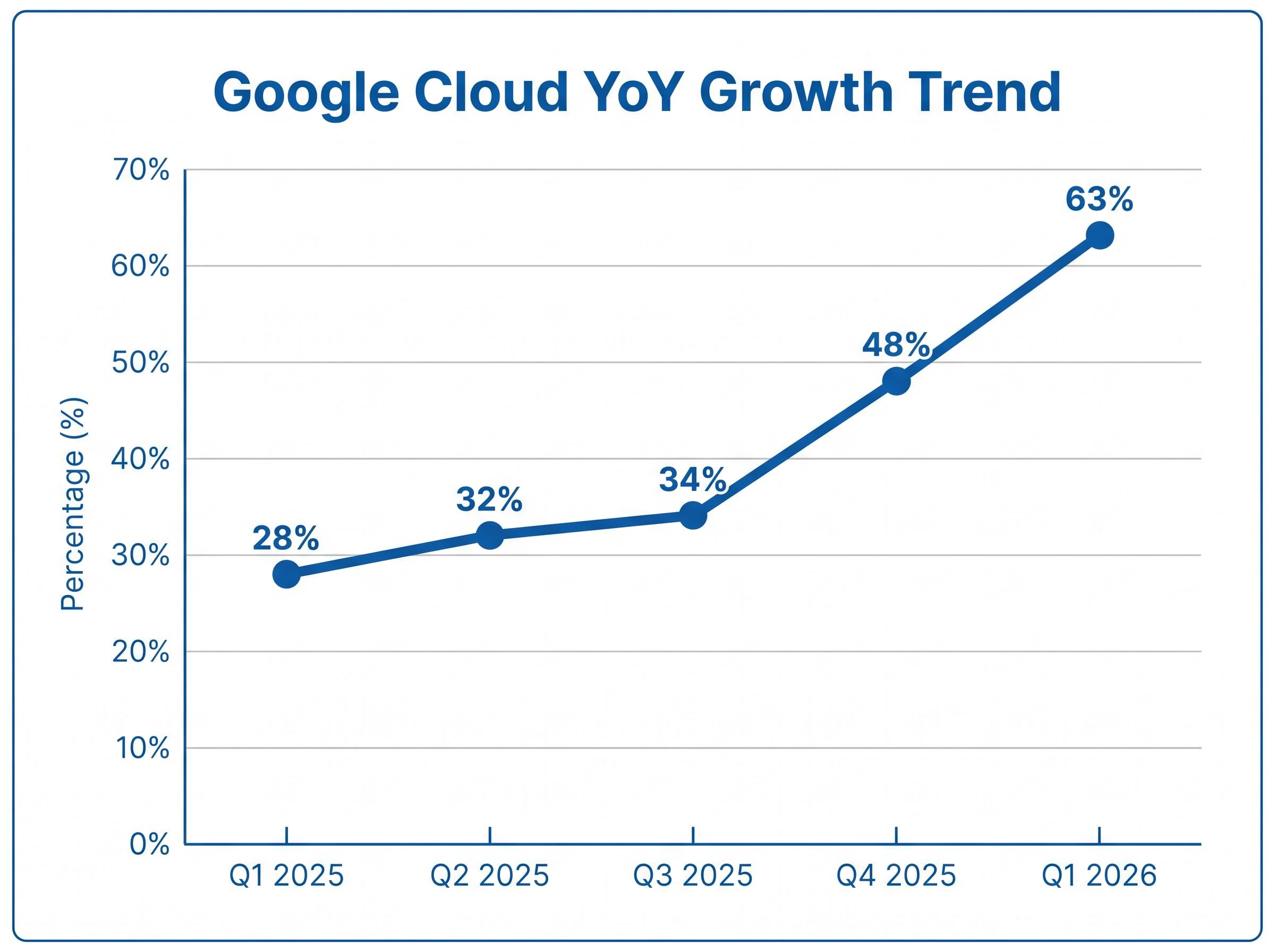

This is not a one-quarter anomaly. The acceleration has been sustained across five consecutive quarters:

The divergent market reactions to Q1 2026 earnings across the hyperscaler group reveal how differently investors are now pricing each company’s path from infrastructure spending to revenue, with Alphabet surging on Cloud acceleration while Meta fell more than 9% despite posting 33% revenue growth.

- Q1 2025: 28% YoY

- Q2 2025: 32% YoY

- Q3 2025: 34% YoY

- Q4 2025: 48% YoY

- Q1 2026: 63% YoY

Enterprise AI adoption is the driver. Gemini processes over 16 billion tokens per minute, and management noted that customer demand continues to exceed capacity. Cloud is now Alphabet’s highest-momentum segment, and the growth rate gap over competitors is widening, not narrowing.

When big ASX news breaks, our subscribers know first

What Alphabet’s AI investment actually looks like under the hood

Comparing Alphabet to Nvidia on a per-chip basis misses the structural difference between the two companies. Nvidia sells the silicon that powers AI workloads. Alphabet monetises AI through the end markets themselves: cloud services, search advertising, and autonomous mobility. The revenue base is fundamentally different.

Alphabet sits in an unusual structural position within the AI trade: the hardware versus software divergence that has produced a 70-percentage-point performance gap between semiconductor equipment and software applications in 2026 does not map cleanly onto a company that owns both cloud infrastructure and the AI models running on it.

That distinction starts with technical depth. Google Brain, now merged into Google DeepMind, developed the Transformer architecture that underpins most major large language models, including OpenAI’s models. Alphabet did not simply adopt AI; its research teams built the foundational framework the broader industry runs on. Gemini, ranked among the most capable AI models currently available according to analyst coverage, now functions simultaneously as a consumer product and a cloud infrastructure offering, meaning AI investment flows through multiple Alphabet revenue lines at once.

Advertising still represents approximately 72% of Alphabet’s revenue, providing the financial base that funds AI infrastructure at the current scale. Understanding how the company earns from AI, rather than simply how much it spends on it, is necessary for evaluating whether the current valuation captures the full scope of AI monetisation.

Search is not the liability the bears assumed

The bear case against Alphabet’s core business centres on AI-powered search alternatives. ChatGPT and Perplexity AI are named as competitive threats in Alphabet’s own annual report filings.

Q1 2026 counter-signal: Search revenue grew approximately 19% year-over-year, with AI integrations appearing to extend search engagement rather than reduce it.

The Q1 data suggests AI is currently enhancing Search activity, not cannibalising it. That may change over a longer horizon, but the disruption thesis has not materialised in the revenue figures to date.

Waymo and quantum computing: two long-horizon bets embedded in one stock

Waymo crossed 500,000 fully autonomous rides per week as of the Q1 2026 earnings disclosure. That figure represents operational scale, not speculative potential. Riders are completing half a million trips weekly in vehicles with no human driver.

The cost side is less flattering. Waymo continues to generate a drag on near-term profitability, and infrastructure and operational costs are expected to pressure margins through 2026. Analyst projections suggest Waymo could become a meaningful revenue generator by the end of the decade, but the timeline is measured in years, not quarters.

Google Quantum AI: frontier positioning, not near-term earnings driver

Alphabet’s quantum computing division made two notable moves in April 2026:

- 25 April 2026: Google Quantum AI began accepting proposals for early access to the Willow quantum processor.

- 18 April 2026: Announced expansion into neutral atom computing.

Both represent positioning plays for a technology with a decade-plus commercialisation horizon. Alphabet’s competitive standing in quantum relative to IBM and Microsoft remains an open question that investors should monitor through independent research sources such as Gartner or IDC.

The framing that matters for both divisions is asymmetric optionality. The core advertising and cloud businesses already support the stock at current prices. Waymo and quantum computing represent upside if they scale, with limited additional downside if they do not, because investors are not paying a separate premium for either.

The valuation case: cheapest of the Magnificent Seven, but not without conditions

Alphabet trades at approximately 29x earnings on 15-20% growth. That is the lowest multiple among the Magnificent Seven on this basis. As of 5 May 2026, GOOGL traded at approximately $383, with a market capitalisation of roughly $4.6 trillion.

Alphabet’s $4.6 trillion market capitalisation places it inside one of the most structurally significant valuation clusters in equity market history; megacap tech concentration at this scale means index investors hold a larger implicit bet on a handful of AI outcomes than most portfolio construction frameworks were designed to accommodate.

Analyst consensus: 89% of analysts (59 of 66 surveyed by S&P Global) rated Alphabet a buy or strong buy as of April 2026. The 12-month consensus price target sits at $403, with a high target of $515.

The post-Q1 2026 earnings surge of approximately 10% reflected confidence in Cloud and AI momentum. The quarterly dividend of $0.22 per share, increased 5% in 2026, marks a second consecutive annual increase.

| Metric | Alphabet (GOOGL) | Nvidia (NVDA) | Broadcom (AVGO) |

|---|---|---|---|

| Market Cap | ~$4.6T | ~$4.8T | N/A |

| P/E (approx.) | ~29x | Higher multiple | Higher multiple |

| Buy Rating % | 89% | N/A | N/A |

| 12-Month Target Upside | ~5% (to $403) | N/A | N/A |

The complication is capex. 2026 guidance was raised to $180-190 billion (from a prior $175-185 billion estimate), with the mix split approximately 60% servers and 40% data centres and networking. Depreciation rose 38% to $21.1 billion in 2025. Q1 2026 capex alone was $35.7 billion. Free cash flow compression is real, and whether the valuation discount represents mispricing or justified caution depends on how investors assess AI monetisation timing.

The next major ASX story will hit our subscribers first

The risks that make this thesis conditional, not certain

Four primary risk categories apply to Alphabet’s AI investment case:

- Advertising revenue concentration: approximately 72% of total revenue

- Antitrust and regulatory overhang: DOJ appeal on search monopoly ruling

- Capex-to-monetisation timing mismatch: $180-190 billion in 2026 spending

- AI competitive threats to Search: ChatGPT, Perplexity AI named in Alphabet’s own risk filings

Advertising concentration is the most straightforward. Nearly three-quarters of Alphabet’s revenue comes from a single business model. Q1 2026 showed the segment accelerating, but a cyclical downturn or structural shift in advertiser spending would compress the financial base that funds everything else.

The DOJ is appealing the search monopoly ruling for tougher remedies. The $32 billion Wiz acquisition, Alphabet’s largest-ever deal, closed in March 2026 after EU antitrust approval in February 2026, but the broader regulatory environment remains adversarial. Realistic near-term scenarios range from behavioural remedies affecting default search agreements to structural remedies that could alter distribution.

The DOJ press release on Google search remedies confirms that the department pursued a remedies trial in May 2025 following the August 2024 monopolisation finding, with the appeal seeking structural outcomes that go beyond the behavioural remedies initially considered.

The most substantive bear case is timing. The risk is not that AI fails. The risk is that the payoff timeline for $180-190 billion in annual capex extends beyond what current free cash flow can comfortably absorb, particularly with depreciation climbing and 2027 capex expected to increase again. Waymo and infrastructure costs add further margin pressure through 2026.

The hyperscaler capex trajectory across Amazon, Microsoft, Alphabet, and Meta is accelerating toward a $1 trillion annual run rate by 2027, a scale that raises structural questions about debt financing sustainability and whether AI revenue conversion can keep pace with the infrastructure commitments already locked in.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Alphabet’s AI bet is already paying off, and the portfolio is just getting started

The Q1 2026 data points toward a company where AI monetisation is simultaneously visible in current earnings, expanding in optionality, and underpriced relative to peers. FY2025 revenue reached $403 billion, up 15% year-over-year. Q1 2026 consolidated revenue hit $109.9 billion (up 22% YoY), with net income of $62.58 billion and EPS of $5.11.

Forward indicator: Google Cloud’s backlog of over $460 billion represents the single most forward-looking data point in Alphabet’s earnings disclosure, a contracted revenue pipeline that has nearly doubled.

The investment case does not depend on chip cycle timing, GPU pricing, or hyperscaler capex decisions made by other companies. It depends on whether Alphabet can convert infrastructure spending into durable revenue growth across cloud, search, and autonomous mobility simultaneously. Three metrics will determine whether that conversion is on track in coming quarters: Cloud revenue trajectory, Waymo ride volume growth, and whether capex-to-revenue ratios begin to normalise as the infrastructure build-out matures.

2027 capex is expected to increase again, which means the investment cycle has not yet peaked. Investors who wait for the thesis to become fully reflected in the share price may find themselves buying at a materially higher multiple. The compounding, based on Q1 2026 evidence, is already underway.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.