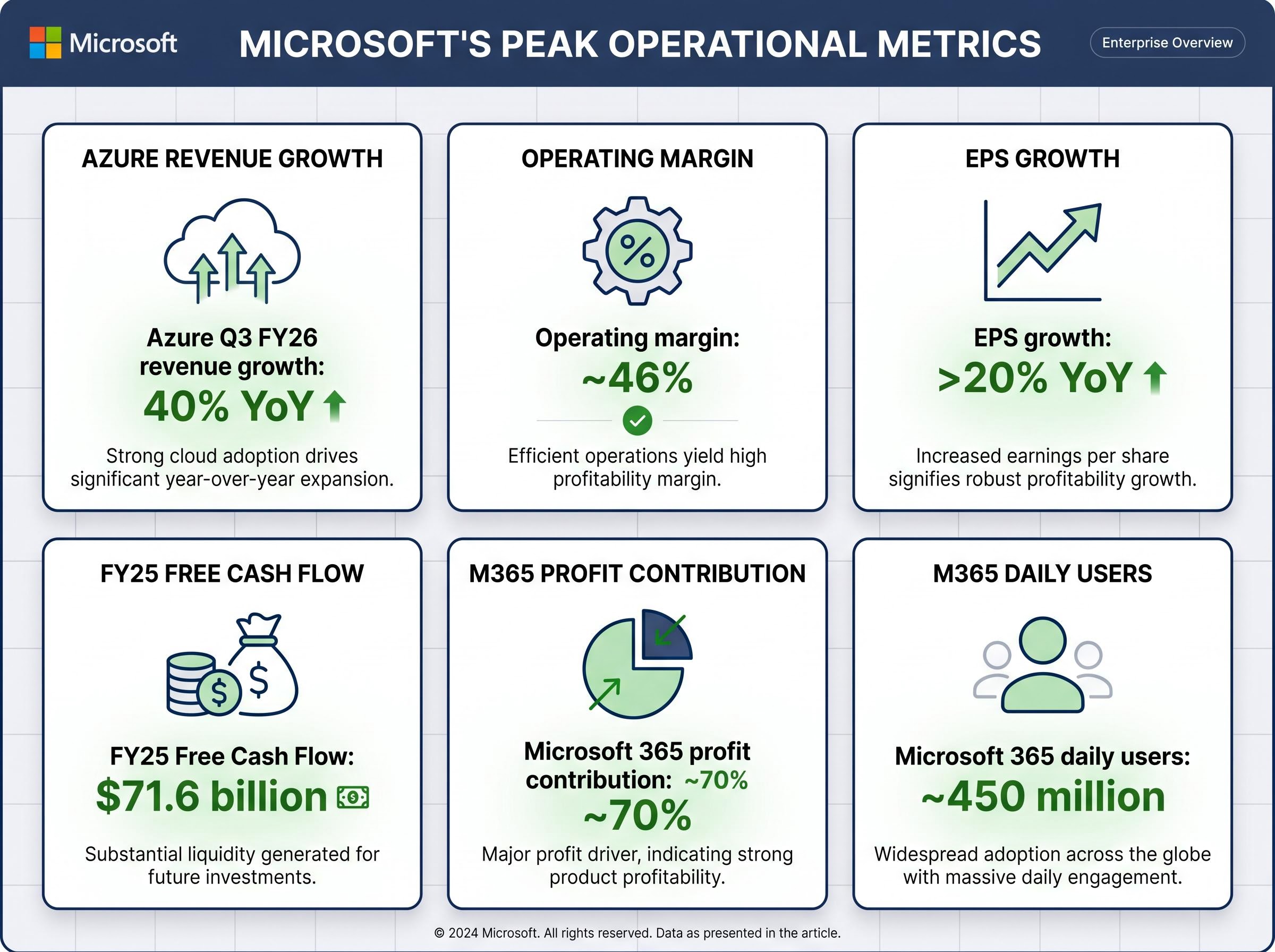

Azure grew 40% year-over-year in Q3 FY26. Microsoft’s operating margins sit near 46%. Bill Ackman recently swapped his Alphabet stake for a comparable Microsoft position. The headline story for Microsoft stock looks difficult to argue with.

Strong current results, however, can obscure structural risks that have not yet surfaced in reported metrics. Two specific risks, each operating on a different time horizon, remain largely absent from mainstream coverage of Microsoft as an investment. The first is the degree to which Azure’s growth rate depends on a single partner relationship. The second is the longer-term possibility that agentic AI quietly dissolves the bundling logic that makes Microsoft 365 so profitable.

What follows is a breakdown of both risks, the mechanics behind each, and the framework investors should weigh when deciding whether Microsoft at roughly 21-22 times forward earnings is genuinely attractive or optimistically priced.

Why Microsoft’s financial results deserve a closer read right now

The surface-level numbers are strong across every segment that matters:

- Azure revenue growth: 40% year-over-year in Q3 FY26 (39% in constant currency), accelerating from 39% in Q2 FY26

- Revenue growth of 15% in constant currency (18% as reported) in the most recent quarter

- Operating margin of approximately 46%; earnings per share growth above 20% year-over-year

- Full-year free cash flow (FCF) of $71.6 billion for FY25

- Microsoft 365 contributing roughly 70% of overall company profits, with approximately 450 million daily users

These are not the numbers of a business under pressure. They are the numbers of a company executing at or near peak operational efficiency.

The capex surge as an early signal

Beneath the headline metrics, quarterly FCF contracted by roughly 22% in the most recent period as capital expenditures approximately doubled year-over-year. That is not merely a financial detail. It is an indicator of the scale of the bet Microsoft is placing on AI infrastructure, and it sets the stakes for both risks that follow.

When big ASX news breaks, our subscribers know first

What drives Azure’s 40% growth rate, and why the source matters

Microsoft does not publish Azure revenue in absolute dollar terms. It reports “Azure and other cloud services” growth as a percentage within the Intelligent Cloud segment. This reporting methodology matters because it makes it difficult to determine precisely how much of that 40% growth rate is attributable to any single customer.

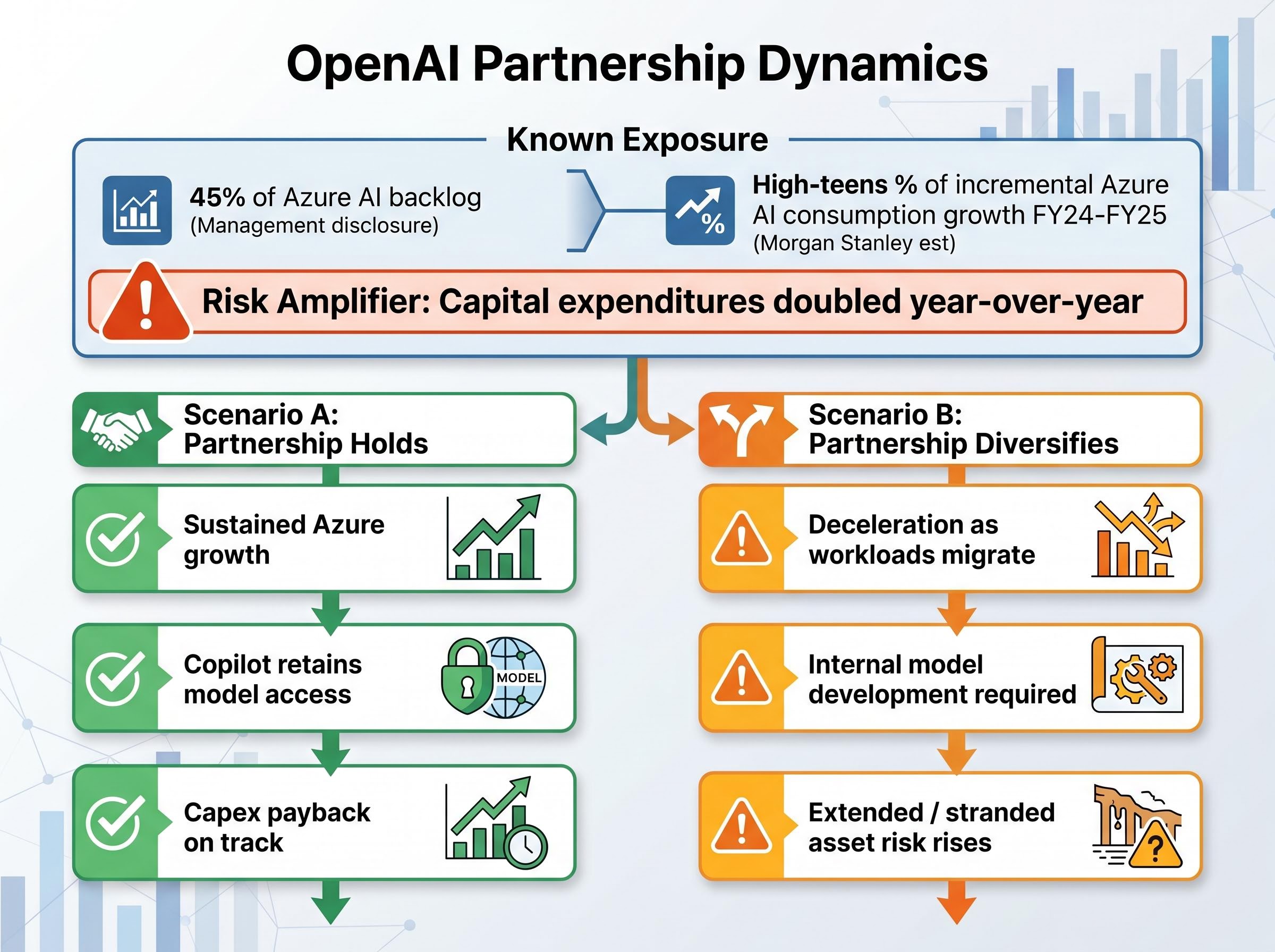

Three distinct data signals point toward meaningful concentration in OpenAI:

- Microsoft management disclosed in an earlier earnings call that approximately 45% of Azure’s AI-related backlog was attributable to OpenAI at one point

- Morgan Stanley analysis, summarised in financial press during 2024-2025, extrapolated that OpenAI-related workloads could represent a “high-teens percentage” of incremental Azure AI consumption growth in FY24-FY25

- Commercial bookings declined approximately 4% in the most recent quarter, with management noting contract timing related to the OpenAI relationship as a contributing factor

Morgan Stanley characterised OpenAI as representing a “high-teens percentage” of incremental Azure AI consumption growth during FY24-FY25, based on backlog disclosures and consumption modelling.

No precise, publicly accessible figure exists for the exact percentage of Azure’s total current revenue growth attributable to OpenAI workloads. The available data is directional rather than definitive. But the direction is clear: Azure’s most important growth engine has meaningful exposure to one partner’s infrastructure decisions.

Understanding the OpenAI partnership as both asset and liability

The Microsoft-OpenAI relationship is a multi-year infrastructure arrangement under which OpenAI’s core commercial services run on Azure. High-profile Microsoft products, including Copilot and earlier iterations of Bing Chat, have been built on OpenAI models. This is the partnership that most analysts cite as Microsoft’s primary AI competitive advantage.

The same structure that powers the advantage creates the exposure. Reports in The Information and Wired during 2024-2025 described OpenAI developing independent infrastructure capabilities and exploring other cloud relationships. No authoritative report has confirmed a meaningful shift of production workloads away from Azure, but the strategic direction is worth monitoring.

OpenAI governance risks add a further layer of uncertainty to the partnership dynamic: a House Oversight Committee investigation into Sam Altman’s conflict-of-interest profile and an unresolved 2024 SEC probe are precisely the kinds of institutional overhangs that could complicate the commercial relationship or accelerate OpenAI’s incentive to diversify its infrastructure dependencies.

The asymmetry is what matters. If the partnership holds, it sustains Azure’s growth rate and supports the AI product roadmap. If it diversifies, Microsoft faces both revenue deceleration in its fastest-growing segment and the risk of underutilised AI data centre infrastructure during a capex cycle that has already roughly doubled.

| Scenario | Azure growth impact | AI product continuity | Capex payback |

|---|---|---|---|

| Partnership holds | Sustained at or near current rates | Copilot and AI features retain model access | On track with current assumptions |

| Partnership diversifies | Deceleration as workloads migrate | Internal model development required | Extended; stranded asset risk rises |

Capital expenditures roughly doubling year-over-year means the financial exposure to any demand shortfall is not theoretical. It is already committed.

How agentic AI could reshape the integrated value of Microsoft 365

Microsoft 365’s durability as a business does not rest on the quality of any individual application. It rests on bundled compliance, security, integration, and switching costs that make it deeply embedded in enterprise IT environments. That bundling logic is what supports approximately 70% of Microsoft’s overall profits across roughly 450 million daily users.

The risk is not that a better word processor appears. The risk is that task-oriented AI agents begin orchestrating whichever tools are most effective for a given workflow, potentially bypassing the integration lock-in that keeps enterprises inside the bundle.

What reinforces the bundle today:

- Unified compliance and security across applications

- Deep integration between Outlook, Teams, Word, Excel, and SharePoint

- High switching costs for large enterprises with years of embedded workflows

- IT procurement inertia favouring single-vendor consolidation

What agents could theoretically change:

- Task-centric workflows that select tools dynamically, reducing reliance on any single suite

- Lower switching costs if agents abstract away the application layer

- Point solutions competing more effectively when integration is handled by an orchestration layer

- “Thin” application front ends that commoditise the underlying productivity software

It is worth stating clearly: no 2024-2025 surveys, analyst reports, or case studies show enterprises de-bundling Microsoft 365 because of agentic AI adoption. Gartner’s public conference materials describe agentic AI as early-stage, primarily in pilots and proof-of-concept deployments. The risk is structural and forward-looking, not empirical.

Enterprise AI adoption data as of April 2026 shows agentic AI deployment sitting at just 17% among enterprises, with 70-80% of AI pilots failing before reaching production, figures that simultaneously reduce the near-term urgency of the Microsoft 365 bundle disruption risk and highlight that the window for Microsoft’s Copilot upsell strategy to cement enterprise loyalty may be longer than the structural argument implies.

Gartner’s Hype Cycle for Agentic AI places AI agent development platforms at the Peak of Inflated Expectations with a 2-5 year timeline to mainstream adoption, a classification that supports the article’s framing of agentic disruption as a structural risk on a longer horizon rather than an immediate earnings-cycle threat.

Microsoft’s hedge: embedding agents inside the bundle

Microsoft’s direct response is Copilot for Microsoft 365, which automates cross-application workflows and is sold as an add-on or bundled feature in higher-tier SKUs. Enterprise CIO commentary during 2024-2025 consistently framed Copilot as a reason to deepen Microsoft 365 commitment, not exit it.

The strategic logic is sound. Turning the agentic threat into an upsell mechanism is precisely what an incumbent with Microsoft’s distribution advantages should do. The caveat is that this strategy depends on Microsoft maintaining model leadership within the bundle, which circles directly back to the OpenAI dependency. The two risks are not independent of each other.

What investors should understand about risks that do not appear in reported results

Some risks surface in quarterly earnings: revenue misses, margin compression, customer churn. Others do not appear in any reported metric until the repricing has already begun. Latent structural risk, where the mechanism of harm exists but the evidence of damage does not yet show up in financials, is a category investors tend to underweight precisely because the current numbers look strong.

Both risks analysed here fit this profile. No reported metric currently shows Azure revenue decelerating due to OpenAI diversification. No seat count data shows Microsoft 365 erosion from agentic adoption. Yet each risk operates on a mechanism that could compound before it becomes visible in earnings releases.

Bernstein analysts have warned that if AI monetisation ramps slower than expected, returns on invested capital across hyperscaler capex programmes could come under pressure, a framing that applies directly to Microsoft’s doubled capital spending.

At approximately 21-22 times forward earnings, Microsoft is not priced at a deep discount that would provide a large margin of safety against these scenarios. Ackman’s entry at this valuation level represents a bullish data point; his thesis rests on Microsoft’s durable competitive position and AI monetisation trajectory. Base-case analyst return estimates sit at approximately 10% annually, with bull-case projections in the low-to-mid teens.

Ackman’s Microsoft thesis centres on the argument that the market has not yet priced the roughly 27% economic interest in OpenAI into the stock, valuing that stake at approximately $200 billion against a $3 trillion market capitalisation, a framing that makes the two structural risks analysed here even more consequential: if the OpenAI relationship deteriorates, both the infrastructure growth story and the embedded asset value unwind simultaneously.

For investors evaluating a position, three monitoring priorities follow logically:

- Assess concentration risk in Azure growth attribution by tracking any disclosure changes around OpenAI’s share of AI workloads or backlog

- Monitor agentic AI adoption signals in enterprise, particularly any survey data showing reduced Microsoft 365 seat counts or SKU-tier downgrades

- Watch for any change in OpenAI’s infrastructure diversification, including disclosed partnerships with competing cloud providers

These are speculative and subject to change based on market developments and company performance.

Two structural risks at different points on the horizon

The two risks operate on different timescales. OpenAI dependency is a nearer-term, more quantifiable concern: Azure’s 40% growth rate in Q3 FY26 is the metric most directly sensitive to any change in that relationship, and the doubled capex programme amplifies the consequences. Agentic AI disruption of Microsoft 365 is longer-dated and more structural; Microsoft 365 seat counts and SKU-tier trends are the metrics to monitor, though meaningful signals may not emerge for several years.

Set against these risks is a business generating $71.6 billion in annual free cash flow, operating at 46% margins, with embedded enterprise relationships that span decades. Microsoft’s own hedging strategies, particularly embedding Copilot inside the Microsoft 365 bundle, are strategically coherent.

Alphabet’s structural risks offer a useful comparison for investors evaluating how unresolved regulatory and competitive pressures interact with strong reported results: Search revenue grew 19% in Q1 2026 even as short-query volume fell 12% year-over-year, a surface-strength-masking-latent-risk dynamic that parallels Azure’s headline growth rate and the concentration questions underneath it.

| Risk | Monitoring signal | Threshold that should shift the thesis |

|---|---|---|

| OpenAI dependency | Azure growth deceleration; OpenAI cloud diversification disclosures | Azure growth falling below 30% with no offsetting first-party AI workload growth |

| Agentic AI disruption | M365 seat counts; enterprise survey data on agent-driven tool switching | Measurable decline in M365 renewal rates or SKU-tier downgrades attributed to agent adoption |

Neither risk has materialised in reported results. Both rest on mechanisms that are structurally credible. At a base-case return of approximately 10% annually, the current valuation leaves limited room for optimism to be wrong. Microsoft’s OpenAI stake, estimated at $100-$200 billion contingent on future IPO pricing, does not materially alter the calculus at a $3 trillion market capitalisation.

The investment question is not whether Microsoft is a strong business. It is whether two unresolved structural risks are adequately compensated at today’s multiple.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.