Two Microsoft Stock Risks Missing From the Bull Case

37 mins ago

CSL’s share price has shed roughly 58% over the past year, returning the stock to levels last seen in 2016 and erasing nearly a decade of investor gains in a single deterioration cycle. The decline accelerated on 23 April 2026 when interim CEO Gordon Naylor delivered the company’s fourth guidance downgrade in approximately 15 months, cutting FY26 NPATA guidance to A$3.1bn and triggering a single-day fall of roughly 16%. That announcement confirmed what many shareholders had feared: the Vifor acquisition has been a costly misfire, the dialysis business has required a A$900m pre-tax writedown, Iran market exposure has added unexpected drag, and US plasma collection costs remain stubbornly elevated. Against that backdrop, CSL is now trading at a price-to-earnings multiple and dividend yield not seen since its growth-stock ascent began. The question for Australian investors is whether the combination of factors driving the selloff is cyclical and recoverable, or structural and permanent, and what the current valuation implies for long-term position decisions.

The fourth downgrade did not arrive in isolation. It was the final entry in a sequence that began in early 2025 and accelerated through each subsequent quarter, each revision citing a different cause, each one compounding the credibility damage of the last.

On 23 April 2026, CSL cut FY26 revenue guidance to approximately A$15.2bn (constant currency), down from approximately A$15.8-16.0bn, and NPATA guidance to A$3.1bn, down from approximately A$3.4-3.5bn. Management cited four distinct causes:

What converted a disappointing result into a credibility event was the timing. Management had reaffirmed guidance approximately three months before the fourth downgrade.

The single-session market cap destruction on 11 May 2026, when CSL shed approximately A$9.48 billion in a 15.96% collapse to a nine-year closing low, underscores how quickly credibility deficits can translate into shareholder wealth loss when guidance cuts arrive without a credible recovery narrative attached.

“A more realistic assessment of FY26 conditions.” — Gordon Naylor, interim CEO, CSL

The table below shows the progression across the four downgrades. Earlier guidance figures are based on available reporting from ASX filings and broker notes; precise prior ranges should be confirmed against CSL’s original releases.

| Downgrade | Approximate Date | Revenue Guidance (CC) | NPATA Guidance | Primary Cited Cause |

|---|---|---|---|---|

| 1st | Early 2025 | Trimmed from prior range | Reduced | IL-12 R&D setback, early cost pressures |

| 2nd | Mid-2025 | Further reduction | Lowered | Plasma cost inflation, inventory build |

| 3rd | Late 2025 | ~A$15.8-16.0bn | ~A$3.4-3.5bn | Iran exposure, Vifor underperformance |

| 4th | 23 April 2026 | ~A$15.2bn | A$3.1bn | All four factors combined |

Nine-month revenue to 31 March 2026 grew approximately 6% year-on-year in constant currency, and plasma collections rose by high single digits. The volumes were there. The costs were the problem.

CSL completed the Vifor acquisition approximately three years ago, paying a significant premium for exposure to renal care, iron deficiency therapies, and an expanded European commercial presence. The deal thesis was straightforward: diversify beyond plasma into adjacent specialty markets with growing patient populations, add higher-margin products to the portfolio, and expand the addressable market at a time when plasma growth alone could not sustain the valuation multiple investors had awarded.

The thesis has not materialised. US and European uptake of dialysis-adjacent products has been slower than the acquisition underwriting assumed. Regulatory pricing pressure on certain renal therapies has compressed margins. The A$900m pre-tax impairment announced on 7 May 2026 (approximately A$630m after tax, largely non-cash) is a concrete acknowledgement that management’s original valuation of the deal was materially wrong.

“A necessary kitchen-sink reset under the interim CEO.” — Goldman Sachs, 29 April 2026

The writedown does not appear in NPATA, and the impairment is largely non-cash. But the cost is real in a different sense: it represents capital that could have been deployed elsewhere and signals that the strategic assumptions underpinning CSL’s largest acquisition in a decade were flawed. For investors, this connects to the R&D disappointments that preceded it, including the IL-12 project failure that contributed to an earlier earnings miss. The pattern is not a single misjudgement. It is a question about capital allocation discipline.

CSL has signalled it will “prioritise higher-return opportunities” but has not announced a disposal of the underperforming dialysis assets. The business remains a strategic anchor: contributing lower margins than the core plasma franchise, absorbing management attention, and leaving an unresolved drag on the portfolio. If management mispriced one large acquisition, investors are right to apply a higher risk premium to the next strategic move.

A transformation programme targeting A$500-550 million in annualised savings by FY28, flagged alongside the guidance cut, represents the financial recovery thesis that management is now asking investors to underwrite, though the credibility of that figure depends heavily on who leads the execution.

The global plasma-derived biologics market remains an oligopoly. Three companies, CSL, Takeda, and Grifols, dominate collection, fractionation, and distribution. No large-scale entrant has materially disrupted that structure in 2025 or 2026, and the barriers that protect it have not changed: regulatory requirements for collection and manufacturing are onerous, building a plasma centre network takes years and hundreds of millions of dollars, and scale economics in fractionation favour incumbents.

Morningstar reaffirmed CSL’s wide economic moat rating on 10 May 2026, citing three structural advantages:

Neither of CSL’s two major rivals is positioned to press an advantage during this period of weakness. Grifols is leverage-constrained, targeting net debt/EBITDA below 4x by 2027 after asset disposals and following scrutiny from Gotham City Research’s short-seller report in January 2025. Aggressive expansion is off the table. Takeda, at its March 2026 investor day, signalled “mid-single-digit revenue growth” and a focus on upgrading existing centres rather than opening new ones.

| Company | Strategic Posture | Capacity Expansion Stance | Key Constraint or Risk |

|---|---|---|---|

| CSL | Resetting expectations, tightening capital allocation | Collections growing but at elevated cost | Credibility damage, leadership vacuum |

| Takeda | Disciplined growth, productivity-led | Upgrading existing centres, not aggressively expanding | Donor cost inflation in US |

| Grifols | Deleveraging, slower expansion | Modest net centre growth, capacity optimisation | Leverage constraint, transparency scrutiny |

The moat, by all independent and broker assessments, is intact. The genuine uncertainty lies elsewhere: structurally elevated US donor compensation and labour costs may mean CSL’s historical peak margins do not return even if oligopolistic pricing power persists. All three major players are signalling more disciplined capital spending, which reduces the risk of overcapacity but does not resolve the cost question. The franchise is not in decline. The profitability of that franchise, however, may have permanently shifted.

Peer-reviewed research on US plasma donor compensation cost trends documents a 40.7% increase in the cost per litre of plasma collected in the United States between 2017 and 2022, providing empirical grounding for why broker and management commentary on structurally elevated collection costs carries more weight than a single-cycle phenomenon.

Gordon Naylor was appointed interim CEO in February 2025. More than 15 months later, the role remains unfilled. The board, chaired by Brian McNamee, described the permanent CEO search as “well advanced” on 24 April 2026, with executive search firm Spencer Stuart engaged and an appointment targeted before the end of calendar 2026.

Gordon Naylor’s interim appointment in February 2025 was framed by the board as a continuity play, drawing on his 33 years of internal experience including a turnaround role at Seqirus, but that framing has grown harder to sustain as the credibility events have accumulated beneath his watch.

The vacancy is not a governance footnote. It is a valuation mechanism.

“The absence of a permanent CEO after four downgrades in quick succession will weigh on sentiment and justify a de-rated multiple until credibility is rebuilt.” — UBS, 24 April 2026

UBS downgraded CSL to Neutral on the same date, explicitly linking the leadership vacuum to the credibility discount investors are applying. Macquarie framed the other side of the trade on 8 May 2026, arguing that “resolution of the CEO search with a high-calibre external or clear internal successor could be a catalyst for re-rating.” Morningstar acknowledged the elevated uncertainty but concluded it does not threaten CSL’s long-term moat, assuming a competent successor is appointed within the signalled timeframe.

Named internal contenders include Paul McKenzie (head of CSL Behring) and Bill Campbell (then head of CSL Seqirus), according to AFR Street Talk on 26 April 2026. External candidates from Takeda and Novartis have been reported but not confirmed.

Across broker research, four catalysts are consistently identified as the events most likely to unlock a re-rating:

The CEO appointment is the only one with a defined timeline. It is also the one that determines the credibility with which investors will receive the other three.

Four arguments converge. The plasma oligopoly is intact and competitors are not positioned to exploit CSL’s weakness. The four downgrades may now be priced in at approximately 13x earnings. A margin recovery pathway is visible if US collection costs normalise through FY27. And the CEO appointment remains a pending catalyst with a defined timeline.

Approximately 98% of CSL’s revenue is generated offshore, making the stock a natural AUD/USD hedge for Australian portfolios, a consideration that adds structural appeal for domestic investors regardless of the near-term earnings picture.

The conditions are specific. A permanent CEO must be appointed. FY26 NPATA guidance of A$3.1bn must be delivered. Plasma collection costs must normalise rather than remain structurally elevated. No further Vifor-related impairments can surface.

Goldman Sachs has flagged the risk that “CSL’s historic 25-30x PE regime does not return.”

If the market permanently re-rates CSL as a mid-teens PE stock rather than restoring its growth premium, the maths of the bull case look materially less compelling even with earnings recovery. At 13x earnings, a stock that recovers to 18x delivers a different return profile than one that recovers to 28x. The PE regime question is the structural risk that sits beneath every cyclical recovery argument.

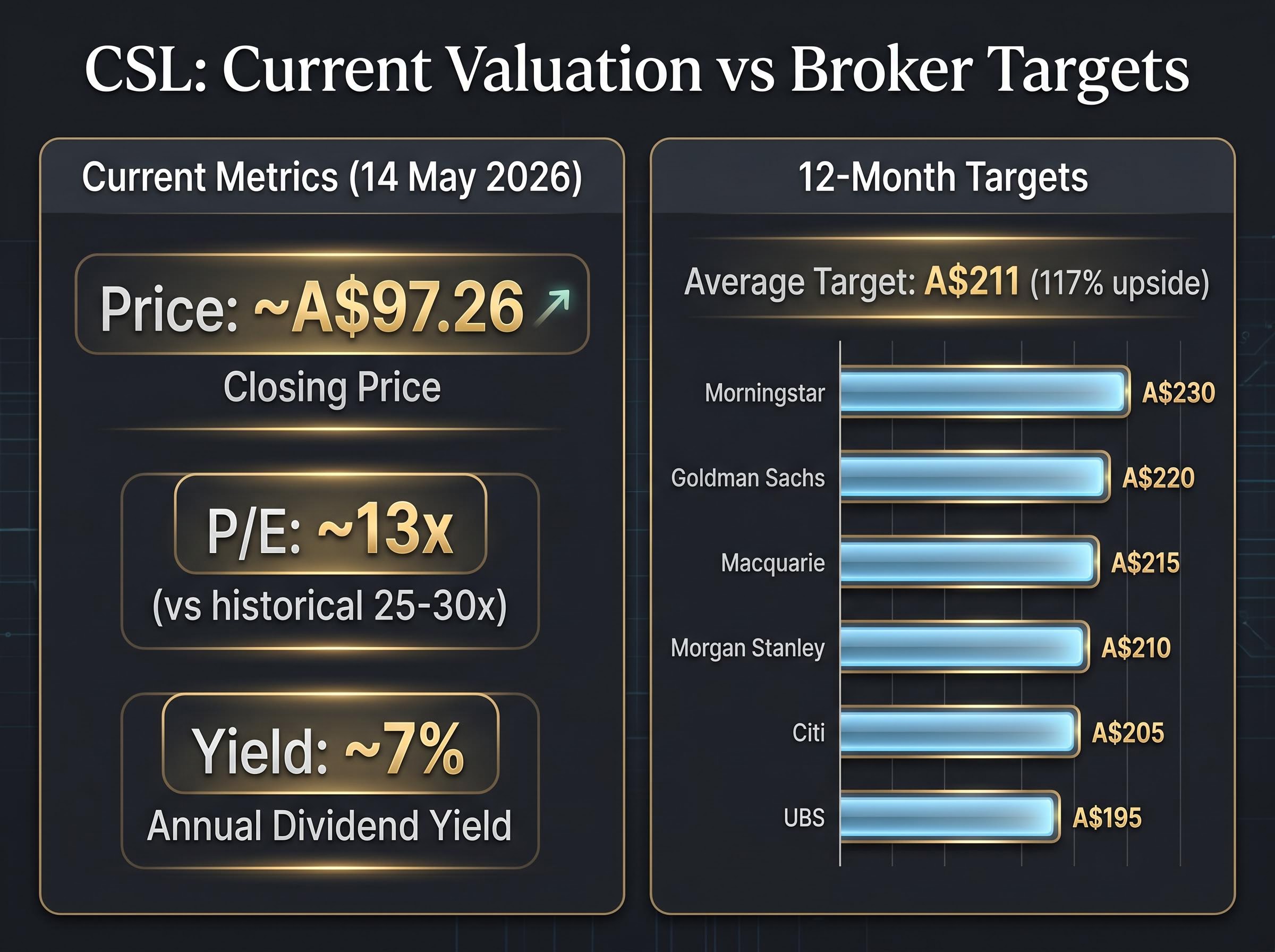

At the 14 May 2026 close of approximately A$97.26, CSL carries a market capitalisation of approximately A$47.2bn, enterprise value of approximately A$67bn, and debt of approximately A$11.5bn (debt-to-EBITDA approximately 2x). The trailing dividend yield sits near 7% at this price, close to an all-time high for the stock, with negligible franking credits due to predominantly offshore earnings. The price-to-earnings ratio of approximately 13x compares with a historical range of 25-30x.

| Broker | Date | Rating | 12-Month Target | Key Thesis |

|---|---|---|---|---|

| Goldman Sachs | 29 April 2026 | Buy | A$220 | Kitchen-sink reset; attractive at ~10x FY27 EV/EBITDA |

| Macquarie | 8 May 2026 | Outperform | A$215 | Cyclical and execution-related; contrarian entry |

| Morgan Stanley | 2 May 2026 | Overweight | A$210 | Multiple repair, not immediate re-rating |

| Citi | 25 April 2026 | Buy | A$205 | Clearing event for value investors |

| UBS | 24 April 2026 | Neutral | A$195 | Credibility event; higher bar for outperformance |

| Morningstar | 10 May 2026 | 4-star (undervalued) | A$230 (fair value) | Wide moat intact; short-term missteps |

The average broker 12-month target sits at approximately A$211, per InvestorDaily consensus from 9 May 2026. At the current price, that implies upside of approximately 117%, a figure that itself demands careful interpretation: either the market is pricing in risks that brokers are underweighting, or the stock is deeply mispriced. There are no Sell ratings among major brokers.

Four arguments converge. The plasma oligopoly is intact and competitors are not positioned to exploit CSL’s weakness. The four downgrades may now be priced in at approximately 13x earnings. A margin recovery pathway is visible if US collection costs normalise through FY27. And the CEO appointment remains a pending catalyst with a defined timeline.

Approximately 98% of CSL’s revenue is generated offshore, making the stock a natural AUD/USD hedge for Australian portfolios, a consideration that adds structural appeal for domestic investors regardless of the near-term earnings picture.

The selloff has two distinct layers. The first is cyclical and likely to reverse: inventory overhang, interim CEO uncertainty, near-term margin compression from elevated collection costs. These are the problems that broker consensus believes are already being addressed and that FY27 trading should begin to resolve.

The second layer is genuinely unresolved: whether CSL’s capital allocation discipline has been structurally impaired and whether the historical PE multiple will return. No amount of Q3 trading data answers that question. It requires a permanent CEO to demonstrate strategic direction, a clean FY26 result to rebuild credibility, and early FY27 evidence that the plasma margin structure is recovering rather than settling at a permanently lower level.

The risk factors divide accordingly:

Morgan Stanley on 2 May 2026 described the period ahead as “a period of multiple repair rather than immediate re-rating.” Morningstar characterised the issues as “short-term demand/supply imbalances and portfolio missteps rather than a structural decline in CSL’s competitive position.” No major broker describes the plasma moat as broken.

The next 12-18 months are the decisive window. Approximately 98% of revenue is generated offshore, making currency exposure a material consideration for Australian portfolios alongside the earnings recovery question.

For investors wanting to stress-test the bull case against specific checkpoint milestones, our dedicated guide to the CSL re-rating thesis examines four concrete inflection points — including the Seqirus demerger timeline and H2 FY26 Behring revenue recovery — that will determine whether the discount closes or widens from here.

The structural moat case is credible. Independent research supports it. Broker consensus supports it. No major analyst house has issued a Sell rating, and the implied upside from the average target is substantial. That body of evidence is real.

So is the credibility damage. Four downgrades in 15 months, a A$900m writedown on an acquisition completed three years ago, and a leadership vacuum that has persisted for over a year represent a different kind of risk than a single bad quarter. Patient investors should require more evidence before treating the discount as self-evidently attractive.

Three concrete events will determine whether the bull case materialises:

At approximately A$97 with a near-7% yield and no meaningful franking credits, CSL is offering a value proposition it has not offered at any point in the past decade. Whether that proposition reflects temporary dislocation or a permanently different business is the question every Australian investor considering the stock must answer for themselves.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

CSL's share price has declined approximately 58% over the past year due to four consecutive guidance downgrades in roughly 15 months, a A$900m pre-tax writedown on the Vifor dialysis acquisition, Iran market disruptions, and persistently elevated US plasma collection costs.

NPATA stands for Net Profit After Tax and Amortisation, a non-GAAP measure that excludes amortisation of acquired intangibles, which CSL uses because large acquisitions like Vifor generate substantial amortisation charges that can obscure underlying business performance.

Brokers and analysts consistently identify four catalysts: the appointment of a permanent CEO, delivery of FY26 NPATA guidance of A$3.1bn, early FY27 evidence of plasma collection cost normalisation, and a clear signal of capital allocation discipline around the underperforming Vifor dialysis assets.

At approximately A$97, CSL trades at roughly 13 times earnings, compared to its historical range of 25-30 times, representing the lowest valuation multiple the stock has carried since its growth-stock ascent began.

CSL operates within a global plasma-derived biologics oligopoly alongside Takeda and Grifols, and Morningstar reaffirmed its wide economic moat rating in May 2026, citing CSL's unmatched collection network scale, high regulatory barriers to entry, and fractionation capacity that competitors cannot quickly replicate.