Alphabet’s stock surged nearly 30% in 30 days following its Q1 2026 earnings beat, yet the company still draws less AI-investor attention than Nvidia. The gap between the two reveals as much about market psychology as it does about Alphabet itself. With Q1 2026 revenue reaching $109.9 billion (up 22% year-over-year) and Google Cloud growing at 63% annually, this is not a quiet story. It is an AI story that spans search, cloud, autonomous vehicles, and quantum computing simultaneously. As investors build AI exposure in 2026, the choice between a pure-play hardware leader and a diversified AI integrator deserves serious analytical attention. This analysis works through each of Alphabet’s AI-driven business segments, benchmarks the investment case against Nvidia’s, and lays out the risks that any investor must weigh before reaching a conclusion.

The earnings print that reframed Alphabet as an AI growth story

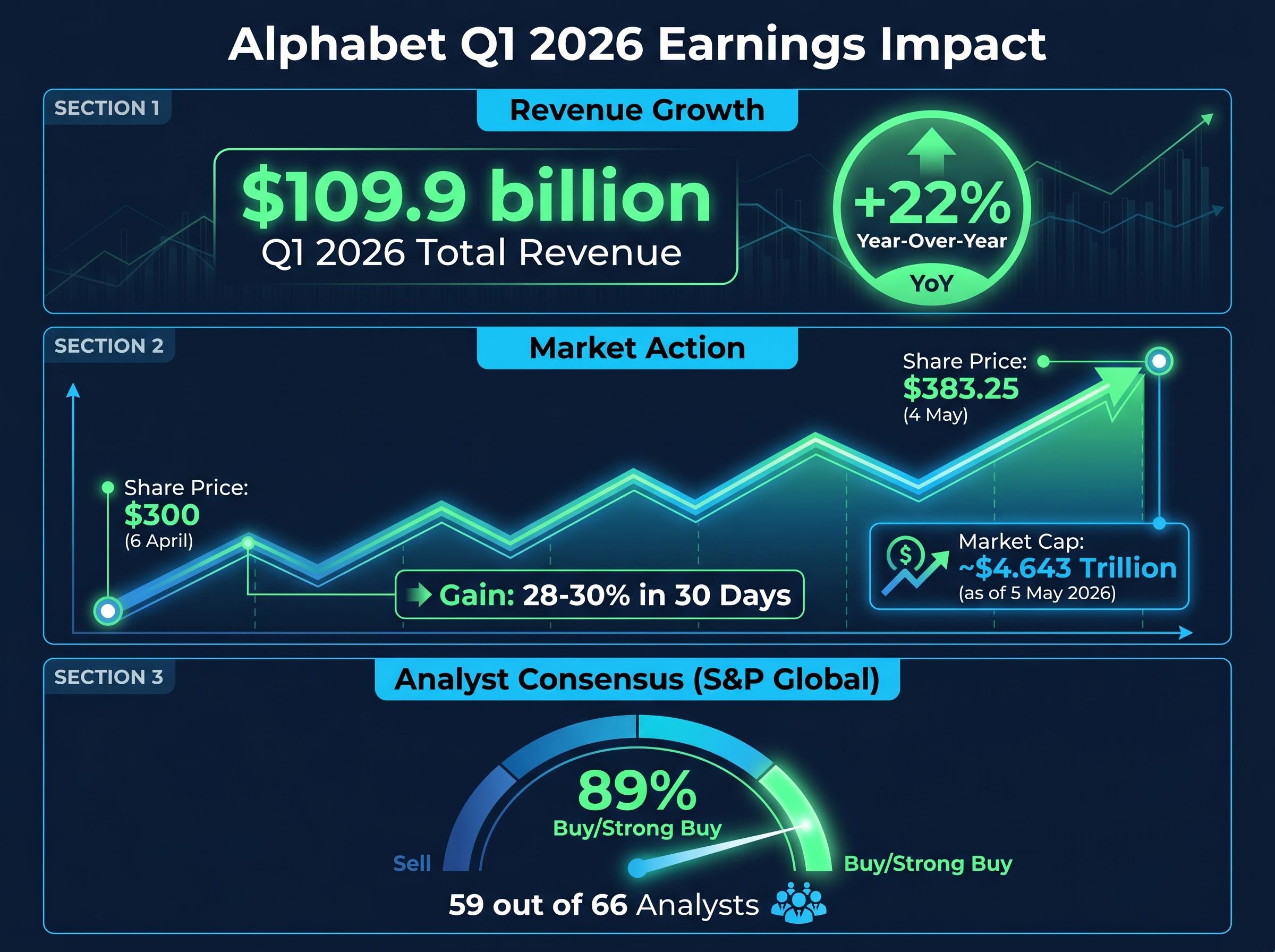

The scale of the Q1 2026 earnings surprise caught even bullish analysts off guard. $109.9 billion in quarterly revenue, up 22% year-over-year, was not a narrow beat driven by a single business line. The growth was broad-based, spanning advertising, cloud, and subscription revenue in a quarter where most mega-cap peers posted mid-single-digit gains.

The market’s response was proportional. Alphabet’s share price moved from approximately $300 on 6 April to $383.25 by 4 May, a gain of roughly 28-30% in a single month. That is not a routine post-earnings drift. It is a re-rating, one that pushed the company’s market capitalisation to approximately $4.643 trillion and placed Alphabet firmly within the 52-week range of $147.84 to $387.38.

The core Q1 2026 metrics tell the story concisely:

- Total revenue: $109.9 billion, up 22% year-over-year

- Share price appreciation: approximately 28-30% in 30 days

- Market capitalisation: approximately $4.643 trillion as of 5 May 2026

- 52-week range: $147.84 to $387.38

Analyst consensus: 59 out of 66 analysts surveyed by S&P Global assigned a buy or strong buy rating, representing approximately 89% of the coverage universe.

For investors who had categorised Alphabet as a mature advertising business, the Q1 print is evidence that the AI transition is already generating revenue at scale.

When big ASX news breaks, our subscribers know first

How Google Cloud became Alphabet’s fastest-moving AI engine

Google Cloud posted $20 billion in Q1 2026 revenue, a 63% year-over-year increase that made it the fastest-growing major cloud provider by growth rate. That growth figure sits meaningfully above the rates reported by Amazon Web Services and Microsoft Azure in the same period, even as Google Cloud remains third in absolute market share behind both.

The growth differential matters more than the market share ranking for investors making a forward-looking decision. Enterprise adoption of Gemini-powered tools and Vertex AI services has driven the acceleration, pulling AI workloads onto Google’s infrastructure at a pace that compressed the gap with larger competitors.

The AI capital expenditure cycle powering Google Cloud’s acceleration operates on a multi-year monetisation timeline: hyperscaler infrastructure spending typically translates into proportional cloud revenue growth within approximately 12 months, a lag that helps explain why Google Cloud’s 63% growth rate reflects investment decisions made well before Q1 2026.

| Metric | Google Cloud (Q1 2026) | Competitive context |

|---|---|---|

| Quarterly revenue | $20 billion | Third by absolute share |

| Year-over-year growth | 63% | Fastest among major providers |

| Operating margin | 32.9% | Improving as scale increases |

The unit economics case for sustained margin expansion

The 32.9% operating margin is where the story shifts from topline momentum to structural profitability. Cloud infrastructure carries high fixed costs. As utilisation scales, per-unit infrastructure costs decline, meaning the current margin may represent a floor rather than a ceiling as enterprise AI adoption compounds.

Gemini integration across Vertex AI creates a form of AI-specific lock-in that differs structurally from commodity cloud compute. Enterprises building applications on Gemini-native tooling face meaningful switching costs, a dynamic that supports both retention and pricing power over time.

What Gemini and Waymo add to the investment case that cloud alone cannot

Gemini and Waymo operate in different markets, serve different customers, and monetise through different mechanisms. Together, they illustrate why Alphabet’s investment case extends well beyond cloud infrastructure.

Gemini has reached 750 million monthly active users, a scale that creates two distinct monetisation pathways. On the consumer side, subscription revenue reached $1.2 billion in 2025. On the enterprise side, Gemini’s integration across Google Search, Workspace, Cloud (via Vertex AI), and Android positions it as a platform-level upsell engine rather than a standalone product.

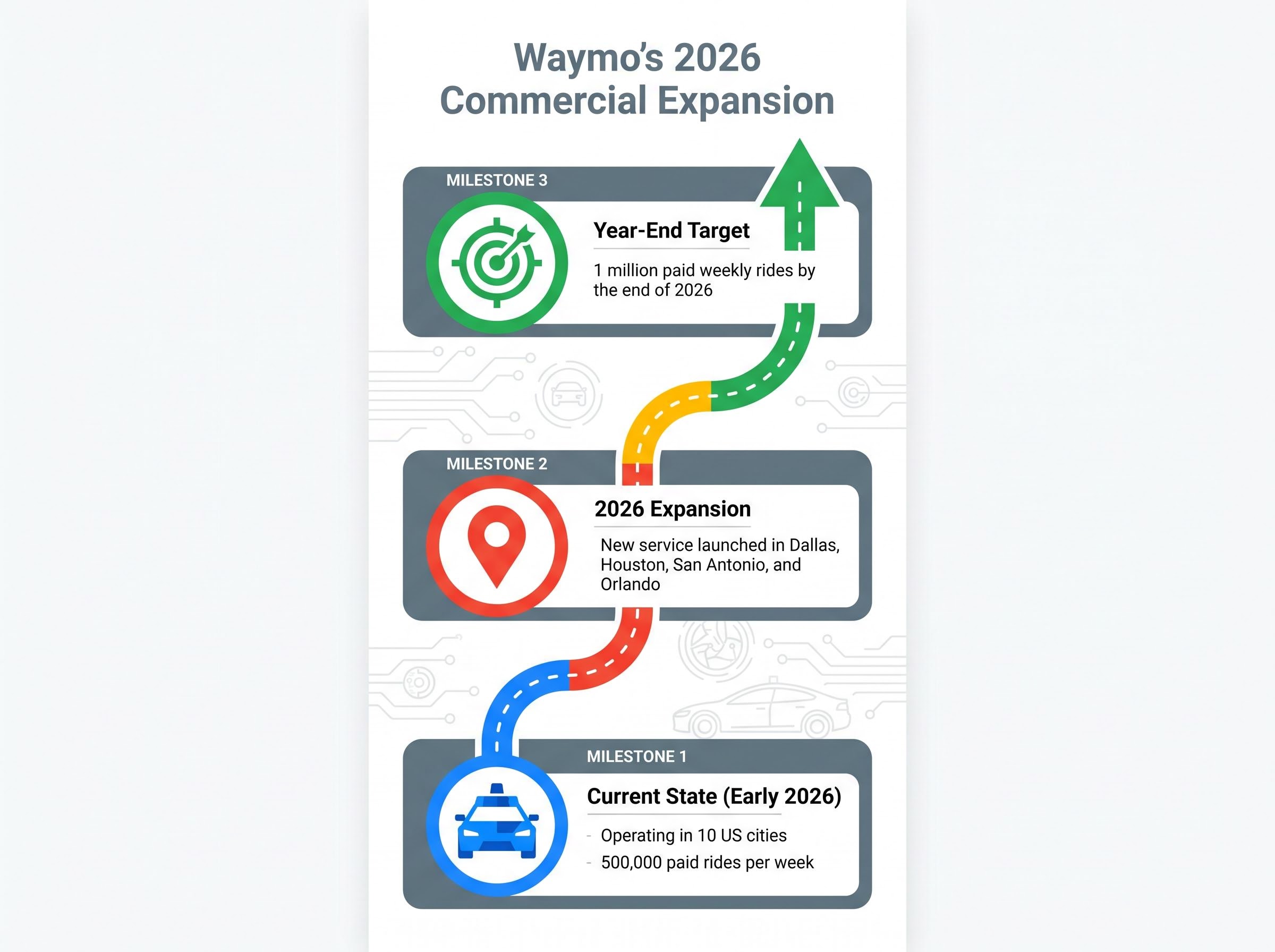

Waymo’s commercial expansion tells a different story, one measured in city-by-city scaling rather than user counts. The trajectory is concrete:

- Current state: operating in 10 US cities, delivering 500,000 paid rides per week as of early 2026

- 2026 expansion: new service launched in Dallas, Houston, San Antonio, and Orlando

- Year-end target: 1 million paid weekly rides by the end of 2026

Commercial milestone: Waymo is currently providing 500,000 paid robotaxi rides per week, positioning it as one of the most commercially advanced autonomous vehicle operations globally.

Investors who frame Alphabet purely as a search and cloud business are underpricing optionality. Gemini’s user base and Waymo’s ridership curve represent two additional large-market revenue stories that do not require new customer acquisition from scratch.

Understanding why Alphabet built the foundations of modern AI

Most investors know Alphabet as a company that uses AI. Fewer recognise that the technology architecture powering virtually all current large language models, including ChatGPT and Gemini itself, originated inside the company.

Google Brain (now merged into Google DeepMind) developed the Transformer architecture, the foundational machine learning framework that underpins every major large language model in production today. A Transformer processes language by weighing the relationship between every word in a sequence simultaneously, rather than reading words one at a time. This approach enabled the step-change in AI capability that launched the current investment cycle. The fact that Alphabet’s own research team built it reframes the company’s position from AI adopter to AI architect.

The 2017 paper Attention Is All You Need, published by Google Brain researchers, introduced the Transformer architecture that now underpins every major large language model in commercial deployment, a lineage that positions Alphabet as a founding contributor to the current AI cycle rather than a late entrant.

DeepMind continues to function as Alphabet’s primary AI research organisation, with its work directly feeding Gemini model development and scientific AI applications. Key milestones include:

- Development of the Transformer architecture (via Google Brain, now DeepMind)

- Ongoing Gemini model advancement and scientific AI research

- 105-qubit Willow chip from Google Quantum AI

- Published five-stage quantum computing roadmap

- Active research into neutral atom computing technologies

Quantum computing: a long-horizon position within a near-term AI stock

Google Quantum AI’s milestones, including the Willow chip and the five-stage roadmap, are signals of technical credibility rather than near-term commercial revenue guidance. The broader quantum computing market is projected to reach approximately $3 billion by 2026, a figure that provides a scale anchor for the opportunity while making clear that this remains a pre-commercial position for Alphabet.

For investors, quantum computing functions as asymmetric optionality embedded within a holding that already generates returns from nearer-term AI businesses.

Alphabet versus Nvidia: two different AI bets, not two versions of the same one

The instinct to compare Alphabet and Nvidia as competing AI investments is understandable. Both sit at the centre of the AI spending cycle. Both command multi-trillion-dollar valuations. Both carry overwhelming analyst support. The comparison, however, obscures more than it clarifies because the two companies occupy structurally different positions in the AI value chain.

Nvidia is the dominant AI hardware vendor. Its GPUs power the training infrastructure that hyperscalers, including Alphabet itself, are building at scale. The investment case is concentrated: demand for AI training and inference hardware remains the primary revenue driver, and Nvidia’s gross margins reflect the pricing power that comes with near-monopoly positioning.

Alphabet occupies the other side of the same cycle. It is an AI integrator and monetiser, converting hardware-level infrastructure into revenue across search, cloud, consumer products, autonomous vehicles, and research. The diversification is the point: no other single holding offers simultaneous exposure to this many large AI-addressable markets.

| Metric | Alphabet | Nvidia |

|---|---|---|

| Market capitalisation | ~$4.643 trillion | ~$4.8 trillion |

| Gross margin | 60.43% | 71.07% |

| Analyst buy/strong buy rate | 89% (59/66) | 95% (56/59) |

| Consensus 12-month upside | Not specified | ~24% |

| Primary AI exposure | Ecosystem monetisation | Hardware infrastructure |

Analyst commentary, including framing from Motley Fool and similar publications, has positioned Alphabet as the stronger growth-to-value mix for 2026, citing its diversified monetisation pathways against Nvidia’s hardware concentration. Notably, Alphabet is itself an Nvidia customer, meaning the two are not purely zero-sum alternatives in a portfolio context. The choice between them is a portfolio construction question, not a stock-picking contest.

Nvidia’s valuation mechanics reveal an important asymmetry in the comparison: Nvidia trades at approximately 24.5x forward earnings, roughly half the Magnificent Seven peer average, despite projected free cash flow exceeding $400 billion across 2026-2027, a gap that Bank of America analysts argue a capital return policy shift could close independent of the AI demand story.

The risks that make the Alphabet investment case genuinely complicated

The bull case for Alphabet is persuasive precisely because it rests on multiple independent revenue vectors. The bear case draws its force from the same structure: the risks are not peripheral. They are embedded in the same business decisions that drive the upside.

- Antitrust exposure: Alphabet faces active DOJ antitrust scrutiny across search dominance and its ad technology stack. Potential remedies could affect core revenue streams that still generate the majority of the company’s cash flow.

- Capital expenditure commitment: The planned $175 billion to $185 billion in AI-related capex for 2026 approximately doubles prior-year levels. This investment is broadly viewed as competitively necessary, but it compresses near-term free cash flow and raises legitimate questions about return timelines.

- Search share pressure: AI-native competitors, including OpenAI-integrated products and Microsoft Copilot, are creating structural pressure on Google’s search market share. Alphabet’s own AI Overviews and Gemini integration into Search have been credited with driving incremental volume, creating a genuine analytical debate rather than a one-sided headwind.

- Cloud market position: Despite 63% year-over-year growth, Google Cloud remains third in absolute market share behind AWS and Azure, requiring sustained aggressive investment to maintain momentum.

Alphabet’s $175-185 billion figure sits within a broader coordinated infrastructure buildout: hyperscaler capex commitments across Amazon, Microsoft, Alphabet, and Meta reached $130 billion in Q1 2026 alone, with full-year 2026 combined guidance reaching approximately $725 billion and a $1 trillion annual run rate trajectory emerging for 2027.

The DOJ antitrust remedies against Google, confirmed in a September 2025 Department of Justice ruling, target the search monopoly and ad technology stack that together underpin the majority of Alphabet’s current cash flow generation.

Capex commitment: Alphabet’s planned AI capital expenditure of $175 billion to $185 billion in 2026 represents one of the largest single-year infrastructure investments in corporate history.

The core tension is this: the scale of investment that creates the long-term upside is simultaneously the source of near-term financial risk. Investors who accept the bull case must also accept that the capex, the regulatory exposure, and the competitive dynamics in search are not separate from the thesis. They are part of it.

Alphabet in 2026: an AI stock that rewards patience over pattern-matching

No other single holding offers simultaneous exposure to AI search monetisation, cloud hypergrowth at 63%, a consumer AI platform with 750 million monthly active users, an autonomous vehicle business delivering 500,000 paid rides per week, and the research organisation that built the architecture underlying the current AI cycle. That breadth is Alphabet’s defining characteristic as an investment.

The risks are real. Antitrust scrutiny, $175 billion to $185 billion in capex, and competitive search pressure are not background noise. The thesis requires tolerance for complexity and a multi-year investment horizon. With 89% of analysts assigning a buy or strong buy rating at a $4.643 trillion market capitalisation, the professional consensus appears to reflect conviction that the diversified AI portfolio is not yet fully priced.

The due diligence question for investors is whether to evaluate Alphabet’s ecosystem-adjusted valuation against pure-play AI peers, rather than against its own historical advertising multiples. If the AI integrator thesis holds, the search-company discount may represent the remaining opportunity.

For investors building AI exposure through index funds or broad tech allocations, megacap concentration risk is a structural consideration that sits alongside individual stock selection: four megacap tech firms now represent over 19% of the S&P 500, meaning passive investors already carry substantial Alphabet weighting before adding any direct position.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.