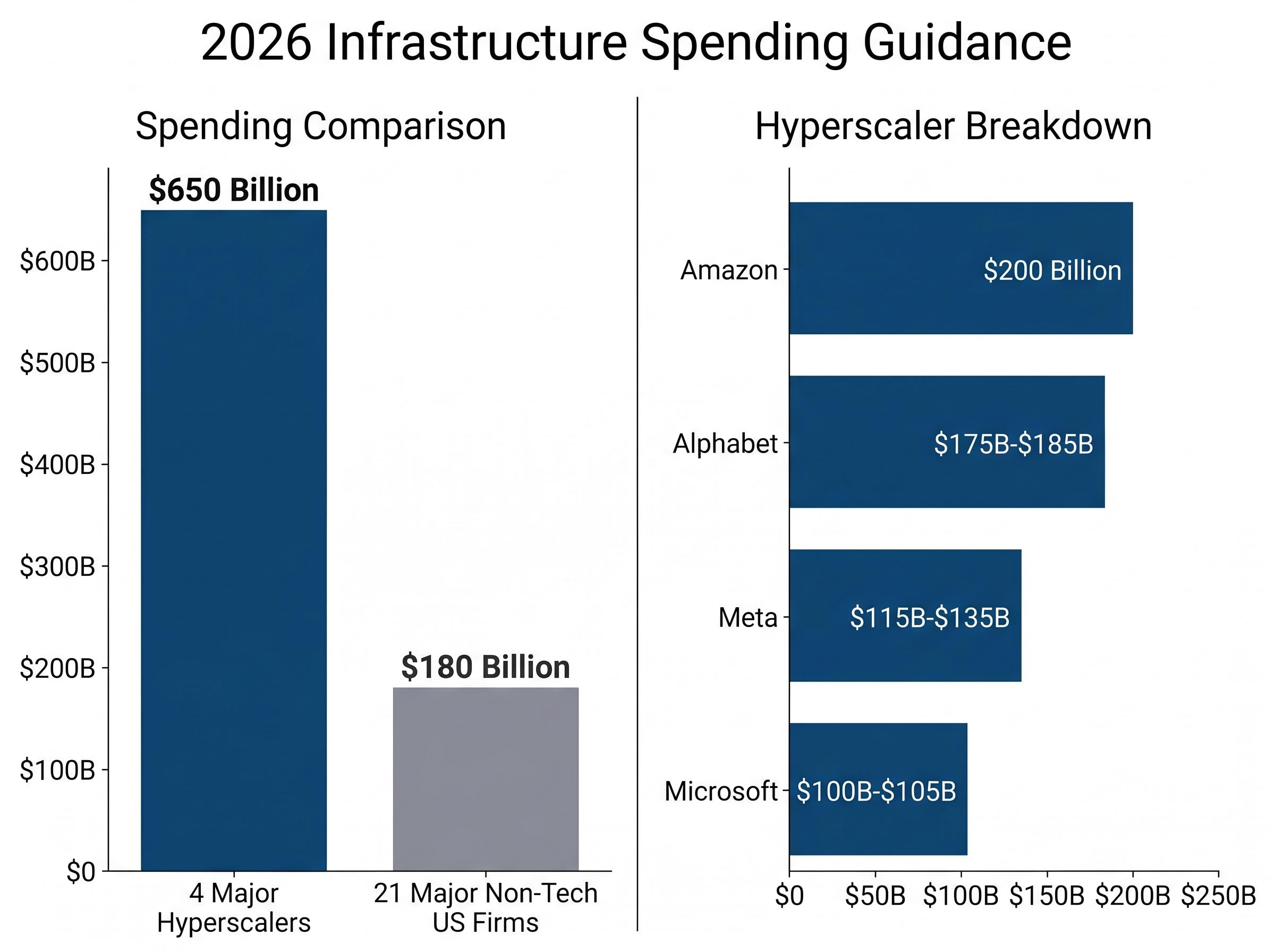

Four major technology hyperscalers are projected to spend a collective $650 billion on infrastructure throughout full-year 2026, dwarfing traditional corporate budgets. This unprecedented AI capital expenditure currently acts as the primary engine for broader United States market growth, validating the acceleration of the computing arms race. The gap between these massive corporate commitments and the broader economy reveals how investor capital is aggressively clustering around artificial intelligence development. These forecasts build on massive previous investments, with megacap spending tracking above $405 billion in 2025. The sheer scale of these outlays requires commercial investors to recalibrate their valuation models for the current financial year. What follows is a clear analytical framework for understanding how these massive corporate investments directly dictate hardware manufacturer revenues and influence semiconductor index valuations.

Mapping the 2026 Hyperscaler Spending Trajectory

The unprecedented financial gravity of the current cycle emerged rapidly through specific financial guidance released in January 2026 and February 2026. Microsoft, Meta, Amazon, and Alphabet outlined commitments that firmly established the aggregate $650 billion total for the year. This ongoing infrastructure build represents an accelerating trend rather than a temporary spike, easily surpassing earlier industry forecasts.

To contextualise this market concentration, these technology giants vastly outspend the broader United States corporate sector. A comparative analysis shows that 21 other major non-technology United States firms combined represent only roughly $180 billion in expenditures. For Amazon alone, forecasted spending on artificial intelligence, chips, and robotics totals $200 billion. Alphabet provided guidance of $175 billion to $185 billion for its own deployments.

These individual company projections align closely with Bridgewater Associates aggregate capex estimates, confirming that a handful of major players now dictate the overall trajectory of corporate infrastructure spending.

Investors must grasp the absolute scale of this concentration, as the spending decisions of just four companies now heavily dictate the trajectory of the broader S&P 500 index. The strategic posture of these corporations indicates no signs of infrastructure delays or shifts to alternate priorities.

| Company | Publication Date | Recent Actual/Quarterly Figure | Full-Year 2026 Guidance |

|---|---|---|---|

| Meta | 29 January 2026 | Prior full-year implied ramp-up | $115 billion to $135 billion |

| Microsoft | 28 January 2026 | Q2 FY2026 CapEx was $37.5 billion | ~$100 billion to $105 billion |

| Alphabet | 4 February 2026 | Exceeded analyst estimates | $175 billion to $185 billion |

| Amazon | 5 February 2026 | Not explicitly broken down in quarterly | $200 billion |

When big ASX news breaks, our subscribers know first

Understanding the Capital Return Timeline for Next-Generation Infrastructure

Evaluating whether current market anxiety regarding delayed profitability is justified requires understanding how capital expenditures function in the technology hardware space. The transition from initial investment to cloud service revenue follows a specific, multi-year timeline that separates expenditure from monetisation. A dollar spent today funds facility construction and advanced chip procurement, laying the physical groundwork for future computational capacity.

The ongoing expansion of these physical data centres aims to solve severe AI infrastructure constraints, which currently threaten to compress margins for even the most well-funded industry leaders as they hit computational bottlenecks.

Once the hardware is secured, the timeline shifts toward service deployment, software integration, and finally enterprise customer adoption. This prolonged cycle creates a projected shift in operating cash generation requirements over the coming years as companies fund the build-out phase.

“Financial forecasts project capital outlays expanding,” according to market projections published by Barclays and BCA Research.

Enterprise Adoption and Realised Value

The infrastructure timeline concludes when commercial end-users successfully deploy these computing systems to extract tangible economic value. Current enterprise goals focus heavily on operational efficiencies, representing 34% of strategic targets, and productivity enhancements at 33%. Recent commercial data indicates that 74% of the economic value generated within top organisations is now driven directly by these new technological deployments.

Hardware Suppliers and the Semiconductor Valuation Surge

The locked-in infrastructure budgets of the leading hyperscalers serve as a guaranteed revenue floor for hardware sellers, shifting market momentum toward physical component providers. This direct correlation actively drives semiconductor index valuations upward, providing suppliers with a layer of immunity against broader economic pressures. Commercial readers must recognise that the safest financial position in the current cycle has historically been the infrastructure suppliers rather than the software developers.

While analysts increasingly model rising US recession probability driven by energy shocks, the locked-in capital expenditure commitments from major technology firms allow semiconductor revenues to remain relatively insulated from consumer downturns.

This dynamic was particularly evident throughout early 2026, demonstrating the resilience of hardware manufacturers despite occasional sector volatility. The momentum in United States semiconductor indices highlights how investor capital rotates toward hardware beneficiaries when massive corporate expenditures are announced. According to market reports, a designated 50-enterprise technology portfolio recorded a 27.2% valuation boost between late March 2026 and April 2026.

Specific metrics from the Philadelphia SE Semiconductor Index capture the scale of this hardware surge:

Year-to-date growth reached approximately 41.68% as of late April 2026, climbing from a year-open baseline near 7,083 points. The index experienced a major session surge of 4.32%, demonstrating significant buying pressure from institutional investors. * This surge occurred alongside a sustained streak of 18 consecutive winning sessions, cementing the hardware sector’s dominance.

Balancing Massive Outlays Against Wall Street Revenue Demands

A structural conflict has emerged between long-term technology development timelines and modern quarterly earnings expectations. The sheer scale of the January 2026 and February 2026 guidance announcements triggered immediate negative equity reactions from investors seeking near-term profitability. Post-announcement share price tumbles affected Microsoft, Alphabet, and Amazon as markets demanded proof of sustainable revenue generation to justify the hardware expenditures.

Corporate leaders face increasing pressure to prove immediate financial returns on their facility investments. However, the initial investor anxiety contrasts sharply with the tangible, accelerating revenue metrics now emerging from hyperscaler cloud divisions. These metrics provide evaluators with the exact data needed to determine if the hyperscalers are succeeding at monetising their enormous capacity increases.

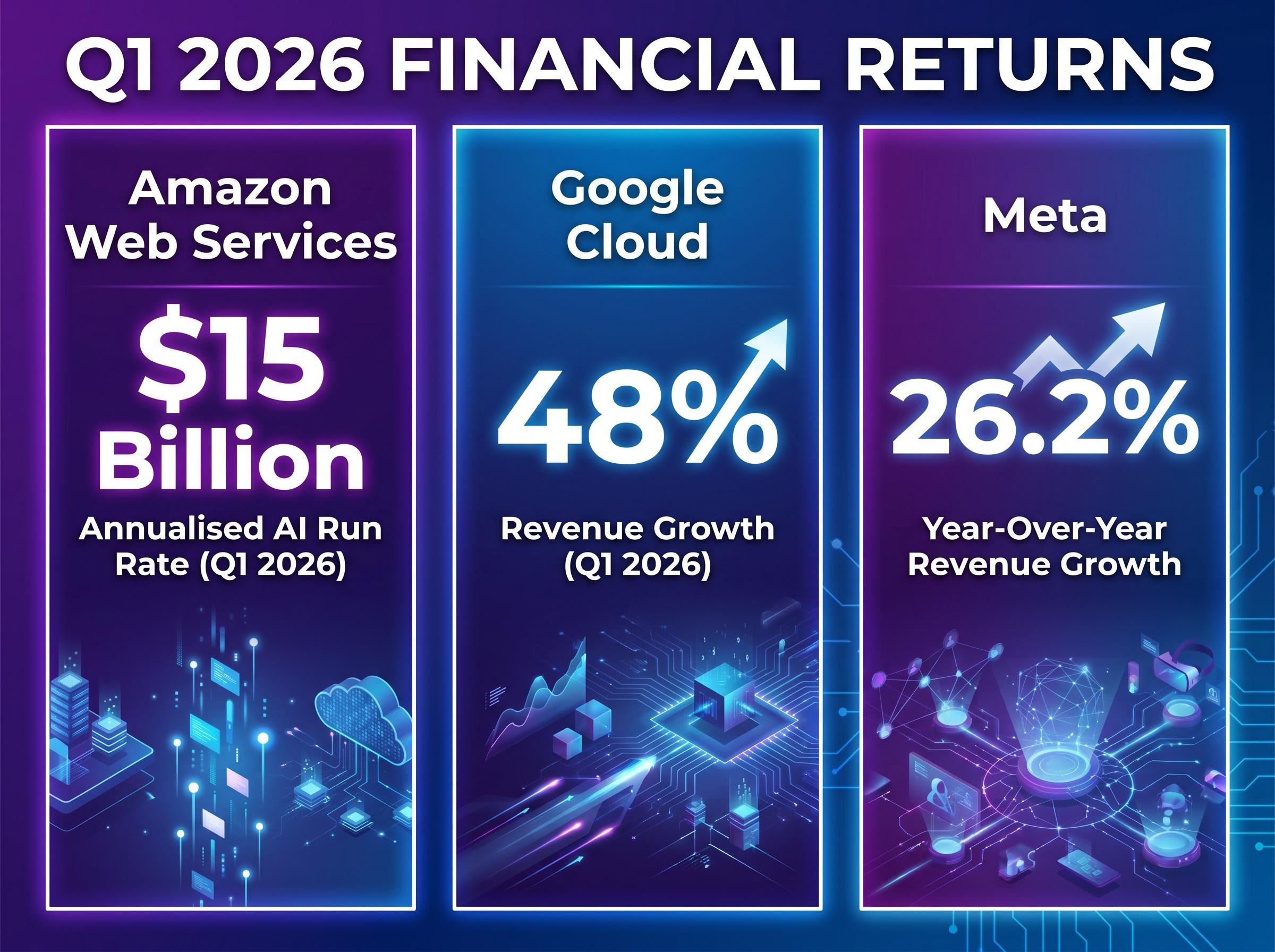

Early Proof Points in Cloud Monetisation

Cloud service integrations are currently driving unprecedented year-over-year growth for the leading platforms, validating the underlying hardware strategy. The specific commercial successes achieved by the major technology players include:

- Amazon Web Services reaching a $15 billion annualised artificial intelligence run rate in Q1 2026, accelerating sharply from the previous year.

- Google Cloud achieving revenue growth of 48% in Q1 2026, heavily supported by new enterprise service integrations.

- Meta recording a 26.2% year-over-year revenue growth, driven primarily by advanced algorithmic advertising gains.

Measuring Supply Chain Vulnerability and Equity Volatility

Projecting the current trajectory forward exposes the structural risks inherent in the computing supply chain. According to financial analysts, a systemic risk is created by having just four companies constitute 17% of the overall S&P 500 index composition. According to market data, the combined valuation of Alphabet, Amazon, Meta, and Microsoft now exceeds $10 trillion, concentrating enormous market influence within a narrow group of decision-makers.

Derivative markets clearly anticipate severe single-day equity valuation fluctuations following financial disclosures from these specific entities. According to trading data, options contracts anticipate a 4% valuation shift for Amazon and a 7.1% change for Meta Platforms immediately post-announcement. Historical context validates this volatility, as Meta experienced average adjustments over the previous dozen reporting periods.

Traders and commercial evaluators gain actionable foresight into post-earnings volatility by examining the underlying fragility of hardware supplier order books. A potential supply chain catastrophe could emerge if these leading technology firms suddenly reduce their infrastructure deployment targets. The hardware manufacturers that currently benefit from guaranteed revenue floors remain entirely dependent on this concentrated spending pattern holding steady.

For readers wanting to understand the broader implications of this market fragility, our full explainer on S&P 500 stock market risk explores how heavy index concentration and elevated valuations could trigger severe drawdowns if macroeconomic conditions worsen.

Strategic Posture for the Next Investment Cycle

The relationship between hyperscaler spending patterns and semiconductor valuations defines the current United States equities environment. While early revenue signs from cloud divisions are highly positive, the extraordinary scale of the 2026 investments requires ongoing monitoring of enterprise usage metrics. Commercial investors must continuously weigh the immediate infrastructure momentum against the structural supply chain risks of heavy market concentration.

This ongoing evaluation must also account for rising energy-driven inflation, which has effectively eliminated anticipated interest rate cuts and removed a crucial policy buffer for broader equities.

Hardware suppliers remain the primary beneficiaries of this expenditure cycle, yet their future performance relies entirely on the major technology platforms sustaining their capital commitments. Past performance does not guarantee future results, and financial projections are subject to rapidly shifting market conditions and supply chain risk factors. These forward-looking statements remain speculative and subject to change based on broad market developments and individual company performance.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.