Asian equities surged on 15 June 2026 as traders repriced a risk that had weighed on the region since Iranian forces closed the Strait of Hormuz in early March: the possibility that the world’s most critical oil chokepoint might stay shut for months. A preliminary memorandum of understanding between the United States and Iran, announced over 14-15 June 2026, commits both sides to a cessation of hostilities and a reopening of Hormuz to commercial shipping. For oil-import-dependent economies across Asia, the deal functions as an unexpected terms-of-trade improvement. For global oil markets, it strips away at least part of the war premium that had kept crude elevated since the conflict began. What follows explains what the MOU actually contains, which Asian markets moved and why, how lower oil prices flow through to corporate earnings and government finances, and why the deal’s retained escape clauses mean sustained optimism carries real risk.

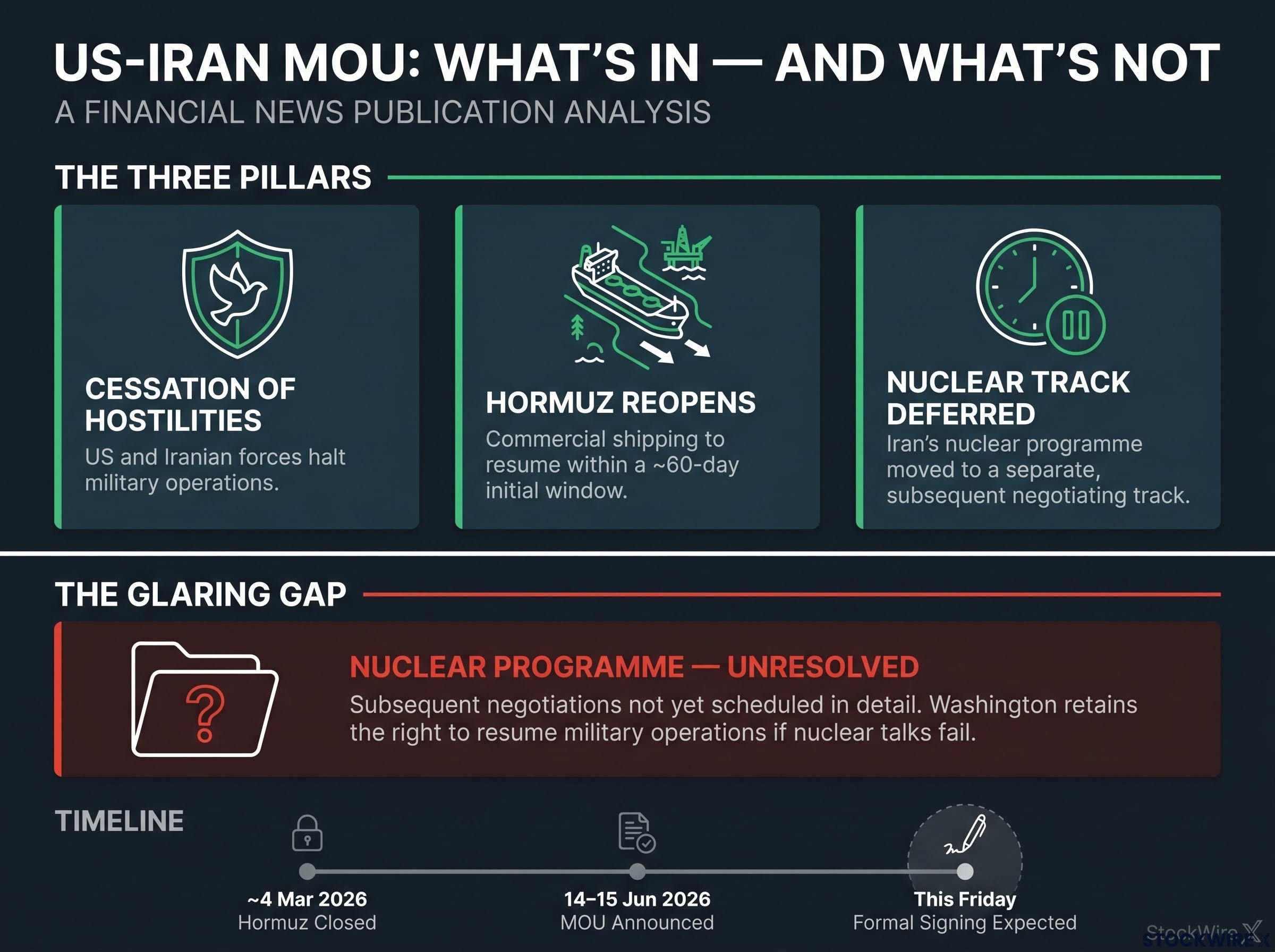

A ceasefire framework built on three pillars, with one glaring gap

The MOU reported over the weekend rests on three commitments:

- Cessation of hostilities between US and Iranian forces.

- Reopening of the Strait of Hormuz to commercial shipping within an initial, time-limited window of roughly 60 days.

- Deferral of Iran’s nuclear programme to a separate negotiating track, to be addressed after the ceasefire and reopening are formalised.

A formal signing is expected by Friday of this week. Press accounts describe a framework designed to de-escalate quickly while buying time for the harder diplomatic work ahead.

What the deal does not settle

Iran’s nuclear programme remains the central unresolved issue. The MOU explicitly defers it to subsequent negotiations that have not yet been scheduled in detail. Washington’s reserved right to resume military operations if those nuclear talks fail is not rhetorical; it is an operational condition embedded in the framework itself. The gap between “ceasefire MOU” and “resolved conflict” is precisely where the residual risk sits.

The CFR backgrounder on the Iran nuclear deal outlines the technical verification requirements and sunset clauses that defined the 2015 JCPOA, illustrating why nuclear file negotiations are categorically more complex than a ceasefire and shipping-lane framework.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz sits at the centre of Asian energy security

Roughly 20% of all globally traded oil transits the Strait of Hormuz, the narrow channel connecting the Persian Gulf to open sea lanes.

That global figure understates Asia’s exposure. The region’s major importers source a disproportionate share of their crude from Gulf producers, and virtually all of it passes through Hormuz. The economies most exposed include:

- Japan, which imports nearly all of its oil, with a heavy Gulf weighting.

- South Korea, a near-total crude importer and major refining and petrochemical hub.

- India, the world’s third-largest oil importer, with chronic current-account sensitivity to crude benchmarks.

- China, a large net importer despite some domestic production and state reserves.

- Singapore, a regional trading, storage, and refining hub where freight, insurance, and financing costs are directly tied to Gulf shipping risk.

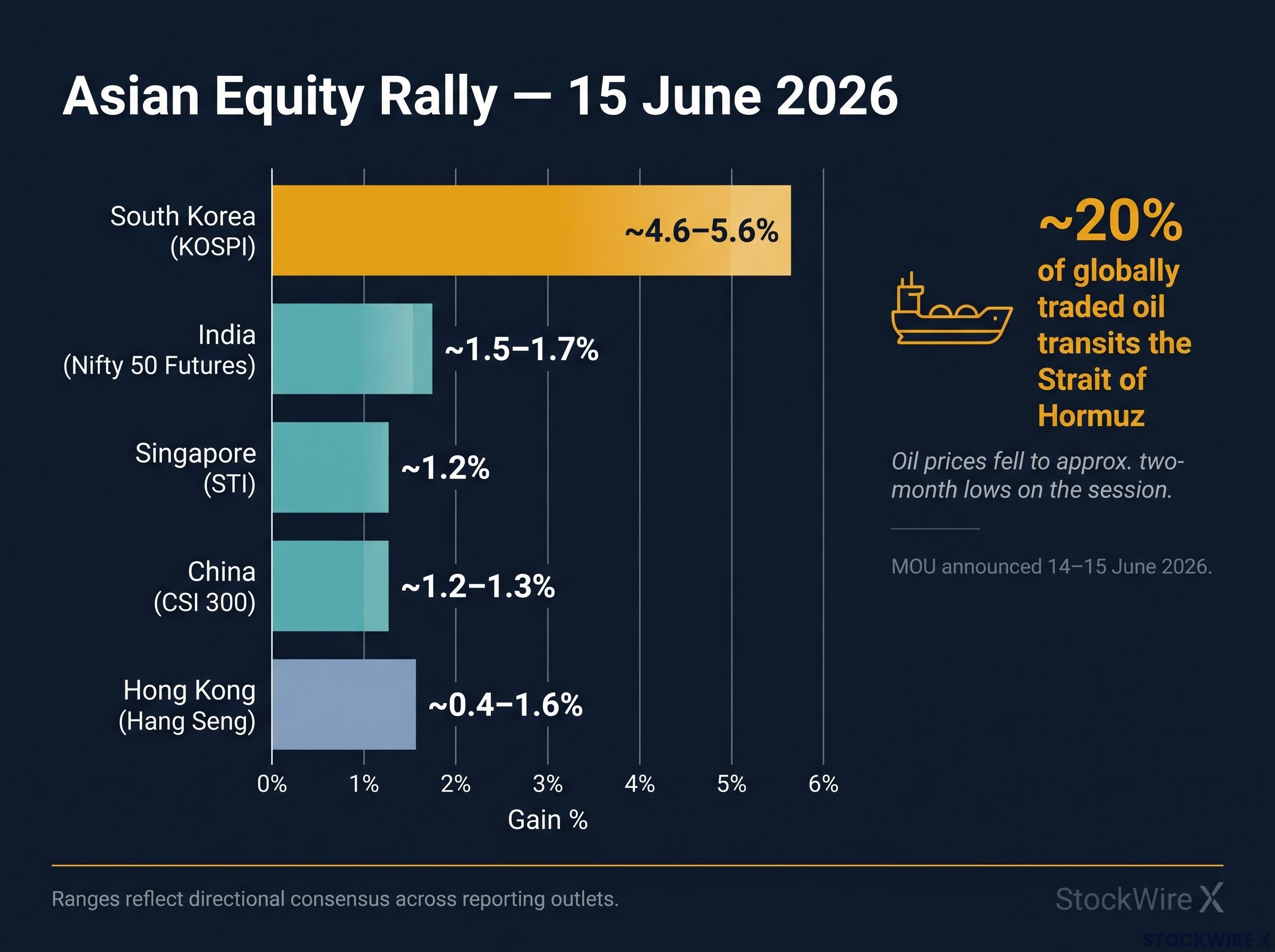

Analysis of past disruption scenarios shows that even a 30-day loss of Gulf shipments can cut US GDP by 0.4-0.5% and spike inflation; for oil-dependent Asian importers with less domestic production, the effects are magnified. Iranian forces declared Hormuz closed on approximately 4 March 2026. The economic stress that followed is the backdrop against which this agreement was reached, and it explains why the same headline produces a larger equity rally in Seoul than in Frankfurt.

The rally on 15 June is best understood against the scale of what preceded it: the effective closure of Hormuz in early March triggered a 57% surge in Brent crude, from roughly $70 per barrel to above $110, as nearly 11 million barrels per day were removed from global circulation with no immediately viable bypass alternative.

The Asian market scorecard on 15 June 2026

The pattern of gains across the region maps closely onto each economy’s structural dependence on Gulf oil imports. Korea, with near-total crude import reliance, led. China, with more diversified supply and state reserves, lagged.

| Market | Index | Reported Gain | Key Driver |

|---|---|---|---|

| South Korea | KOSPI | ~4.6-5.6%* | Near-total crude importer; energy-intensive export base |

| India | Nifty 50 futures | ~1.5-1.7%* | Third-largest oil importer; fiscal and current-account relief |

| Singapore | STI | ~1.2% | Regional energy trading and logistics hub |

| China | CSI 300 / Shanghai Composite | ~1.2-1.3% / ~0.9% | Large net importer, but diversified supply cushions exposure |

| Hong Kong | Hang Seng | ~0.4-1.6%* | Broader regional optimism; tempered by local structural issues |

*Source figures conflict across reporting outlets; ranges reflect directional consensus. Oil prices fell to approximately two-month lows on the session.

The dispersion is not noise. It is the market’s real-time map of energy dependency. Traders treated the MOU as an energy-security event, not a generic risk-on trigger, and the variation in gains confirms that reading.

How cheaper oil actually moves through Asian economies

The equity rally reflects more than sentiment. Lower crude prices, if sustained, flow through oil-importing economies via four distinct channels:

- Lower input costs for manufacturers, logistics operators, and agricultural producers, directly widening margins.

- Softer headline inflation, giving central banks more flexibility to hold rates or ease, rather than tighten in response to energy-driven price pressures.

- Improved trade balances and currency stability, as the import bill shrinks relative to export earnings.

- Higher expected corporate earnings, particularly in energy-intensive sectors such as airlines, shipping, petrochemicals, and heavy industry.

Oil-driven inflation had already forced emergency fiscal responses across the region before the MOU was announced, with Japan deploying approximately 1 trillion yen in gasoline subsidies and facing all-time highs in its 30-year JGB yield simultaneously, illustrating the compounding fiscal bind that cheaper crude now begins to ease.

A durable deal that includes sanctions relief could also raise Iranian export volumes, adding further downward supply pressure on crude benchmarks.

India as the clearest case study

India illustrates how these channels compound. As the world’s third-largest oil importer, elevated crude had strained the government’s fiscal balance through fuel subsidies and widened the current account deficit simultaneously. Cheaper oil reverses both: the subsidy bill falls, easing fiscal pressure, while the import bill shrinks, narrowing the external deficit.

Lower fuel prices also feed through to consumer price inflation, which in turn gives the Reserve Bank of India more room to hold or cut rates. Easier monetary conditions further support equity valuations. For India, the transmission is not a single channel but a reinforcing loop.

Three reasons the optimism could unravel quickly

The rally prices in a smooth diplomatic path. The historical record suggests that path is far from guaranteed.

- The nuclear file is unresolved. Iran’s nuclear programme requires technically complex and politically sensitive negotiations. Past US-Iran diplomacy, including the 2015 Joint Comprehensive Plan of Action, shows large gaps between preliminary frameworks and durable final agreements. Hardline factions in Iran and congressional opposition in the US both constrain what negotiators can credibly offer.

- The US military option is explicit, not rhetorical. Washington’s reserved right to resume operations if nuclear talks fail places a permanent cap on how far the geopolitical risk premium can fall. This is not a diplomatic courtesy; it is an operational policy commitment embedded in the framework.

- Implementation carries its own risks. Physically reopening Hormuz requires naval repositioning, coordinated shipping lane protocols, and insurance market adjustments. Each step creates windows for miscalculation, proxy disruption, or isolated incidents that could threaten the ceasefire before a formal agreement is signed.

The Hormuz risk premium embedded in crude prices is not expected to decompress quickly even under a best-case diplomatic outcome; the IEA projects a two-year supply chain recovery timeline, and VLCC daily hire rates, running at approximately $110,000 per day at the peak, are a physical market signal that often lags geopolitical headlines by weeks.

The Brookings Institution timeline of Iran nuclear diplomacy documents how preliminary frameworks in past US-Iran negotiations routinely took years to translate into binding agreements, with multiple near-collapse moments along the way, a pattern directly relevant to assessing how much weight to place on the current MOU.

A single-session market move assigns a high implied probability to a diplomatic outcome that history suggests is far from guaranteed.

What happens next will be determined by these four signals

The coming days and weeks will test whether the risk repricing holds. Four signals matter most, in priority order:

- Formal signing. Does the agreement get signed on schedule this week, and does the final text match the reported ceasefire-plus-reopening framework? A clean signing would anchor at least part of the equity and currency gains.

- Oil prices and shipping flows. Do Brent and WTI continue to trade near two-month lows, or does the war premium creep back? Ship-tracking data and freight rates will confirm whether physical traffic through Hormuz is actually normalising.

- Nuclear talk headlines. Early signals on scope, timelines, and red lines from both capitals will feed directly into oil and currency volatility.

- Gulf security incidents. Any renewed missile, drone, or naval activity around the Gulf would instantly challenge the peace narrative and re-price risk across the region.

The cross-asset repricing triggered by earlier rounds of US-Iran diplomacy in May 2026 showed that durable market gains required three unmet conditions: a formal agreement with verifiable terms, confirmed normalisation of strait traffic over multiple weeks, and sustained Brent pricing below the crisis-era range, none of which the current MOU has yet delivered.

The bottom line for investors

If the truce holds and evolves into a broader settlement, Asian oil-importing economies stand to gain through lower structural energy costs, improved external balances, and easier financial conditions. If it falters, the 15 June rally is vulnerable to a rapid unwind. A starting point and a conclusion are not the same thing.

A genuine inflection point, but diplomacy still has the final word

The MOU represents the most meaningful de-escalation in the US-Iran conflict since hostilities began in early 2026, and its potential upside for Asian economies is structurally grounded. Beyond the financial markets, a genuine ceasefire reduces the immediate threat to lives and to regional stability. The next test arrives with the formal signing and the first session of nuclear talks. Markets will be watching both with unusual intensity.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding the diplomatic process and market outcomes are speculative and subject to change based on geopolitical developments.