Starbucks Builds AI Tools to Drop Microsoft, IBM and Oracle Apps

3 hrs ago

A drone strike on the UAE’s sole nuclear power plant on May 17, 2026 was intercepted before reaching the core facility, but its impact on global energy markets was not so easily contained. With Brent crude at approximately $111 and WTI above $103, the Middle East conflict has crossed from a geopolitical risk into a confirmed, persistent inflationary force. The escalation has been running for more than two months, and the combination of fresh attacks on Gulf energy infrastructure, stalled diplomatic efforts, and elevated supply-risk premiums is now driving real economic decisions from Tokyo to Frankfurt.

What follows traces the full economic chain: from the strike itself, through what triple-digit oil actually costs the global economy, to how governments and central banks are being forced to respond, and what comes next if the conflict remains unresolved. The traditional separation between oil market analysis and geopolitical risk analysis has collapsed. Both are now the same variable.

The confirmed facts of the May 17 strike are narrow in scope:

The physical damage was contained. The market reaction was not.

On May 18, 2026, Brent crude rose approximately $1.98 (+1.81%) to around $111.24. WTI climbed approximately $2.32 (+2.30%) to around $103.34. A nearly 2% single-session move on a strike that caused no operational disruption signals something beyond damage assessment: the market is pricing the damage that could occur, not the damage that did.

OCBC analysts characterised the pattern of fresh attacks on UAE and Saudi targets, combined with a presidential ultimatum and a scheduled high-level security meeting, as significantly elevating the probability of renewed large-scale conflict.

The Barakah strike was not an isolated event. It was one data point in a pattern of escalation that the oil market is now treating as a persistent signal rather than a one-off disruption.

The Barakah strike is best understood against the backdrop of the Hormuz triple lock that has been reshaping global energy flows since late April, a convergence of US naval blockade operations, Iranian toll enforcement, and the near-total withdrawal of commercial war-risk insurance that has removed millions of barrels per day from seaborne circulation even when no physical engagement was occurring.

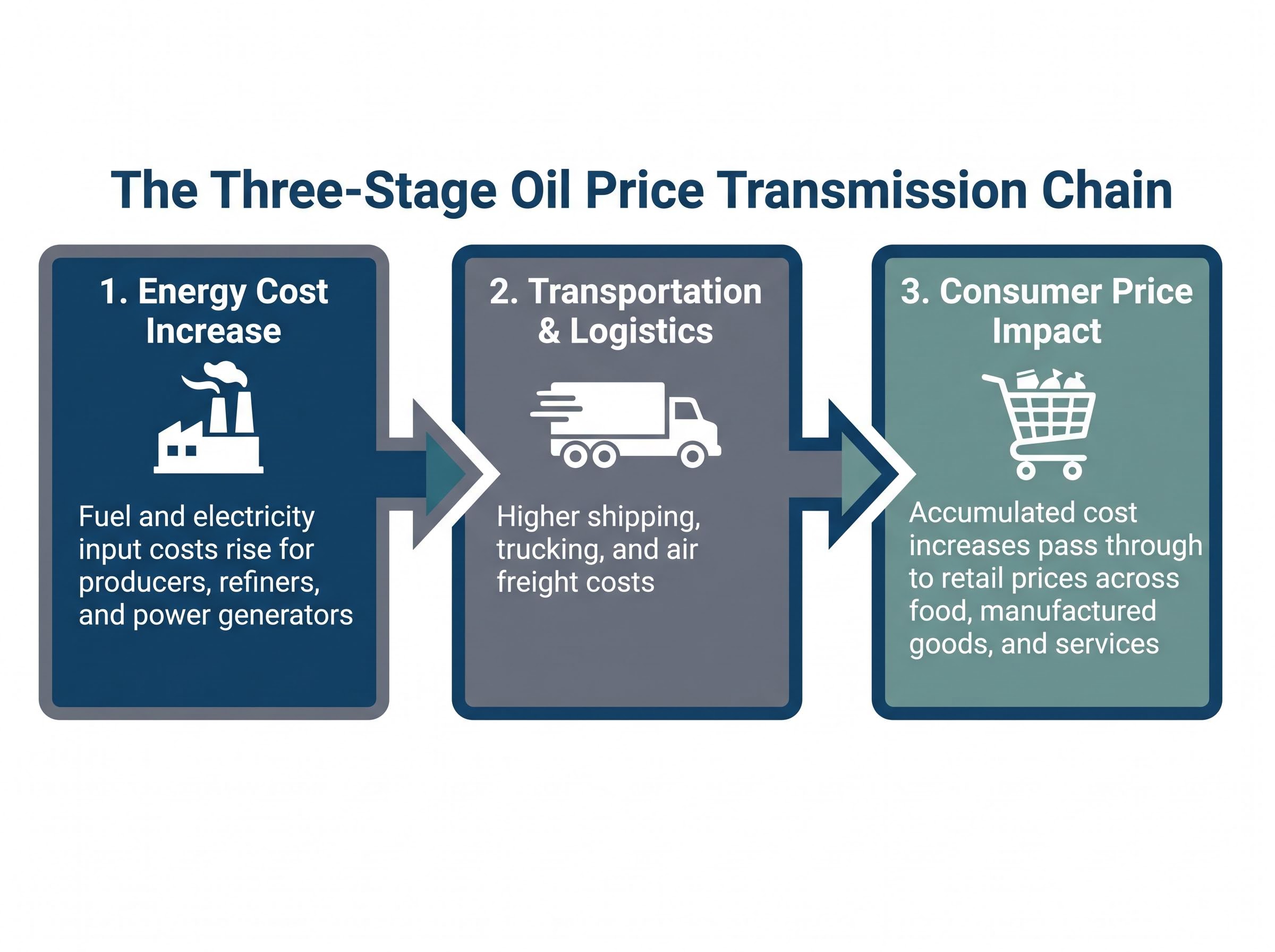

Triple-digit oil does not arrive at the consumer as a single price shock. It multiplies through the supply chain in a three-stage transmission process:

No freshly quantified 2026-specific Consumer Price Index (CPI) pass-through coefficients have been published in publicly accessible sources. IMF and World Bank 2026 surveillance documents identify sustained higher oil as an upside risk to global inflation and a threat to ongoing disinflation progress, though they stop short of attaching a precise number.

IMF World Economic Outlook projections published in April 2026 explicitly link Middle East supply disruptions to upside inflation risks, noting that sustained higher energy costs threaten to reverse disinflation progress in both advanced and emerging market economies, a risk the article’s three-stage transmission analysis reflects.

Analyst commentary referenced in media reporting during May 2026 suggests sustained higher oil could add some tenths of a percentage point to inflation in advanced economies, and potentially more in oil-importing emerging markets.

The impact is not uniform. Advanced economies retain partial insulation through strategic petroleum reserves, domestic production capacity (particularly in the United States), and energy policy tools that can absorb a portion of the shock before it reaches consumers.

Oil-importing emerging markets face sharper exposure. Weaker fiscal buffers, greater dependence on imported fuel, and limited subsidy capacity mean the pass-through from wellhead to consumer is faster and less filtered. The distinction matters beyond the countries directly affected: if emerging market consumers face severe cost-of-living pressure, the demand contraction feeds back into global trade volumes, creating a secondary drag on the world economy.

A geopolitical risk premium is the portion of the oil price above what supply-demand fundamentals alone would justify. It reflects the market’s probability-weighted expectation of supply disruption: the higher the perceived risk that conflict will interrupt physical oil flows, the larger the premium.

No precise dollar-per-barrel decomposition of this premium is available in public sources. However, IEA Oil Market Reports for April and May 2026 treat geopolitical tension in the Middle East as a persistent upside risk to prices rather than a transient spike. The framing is telling.

The IEA’s April and May 2026 Oil Market Reports identify Middle East geopolitical tension as a key upside risk to oil prices, treating the premium as structural for the current period rather than a short-duration event.

The IEA’s framing of geopolitical tension as a persistent upside risk rather than a transient spike is consistent with the structural risk premium argument: even a ceasefire announcement would not immediately restore commercial insurance coverage or supply chain normalcy, meaning the premium embedded in current prices is likely to decompress slowly over months rather than unwind in a single session.

Past oil price spikes tied to single, discrete events (a facility strike, a tanker seizure, a brief military exchange) tended to self-correct once the immediate threat passed. The current conflict has been running for more than two months as of May 18, 2026, with no confirmed diplomatic progress. Attack patterns have escalated rather than subsided.

If the premium is structural rather than transient, the relevant question shifts. It is no longer about when oil retreats to pre-conflict levels. It is about what sustained triple-digit prices do to economic planning horizons, fiscal capacity, and monetary policy settings, which is the thread the following sections pick up.

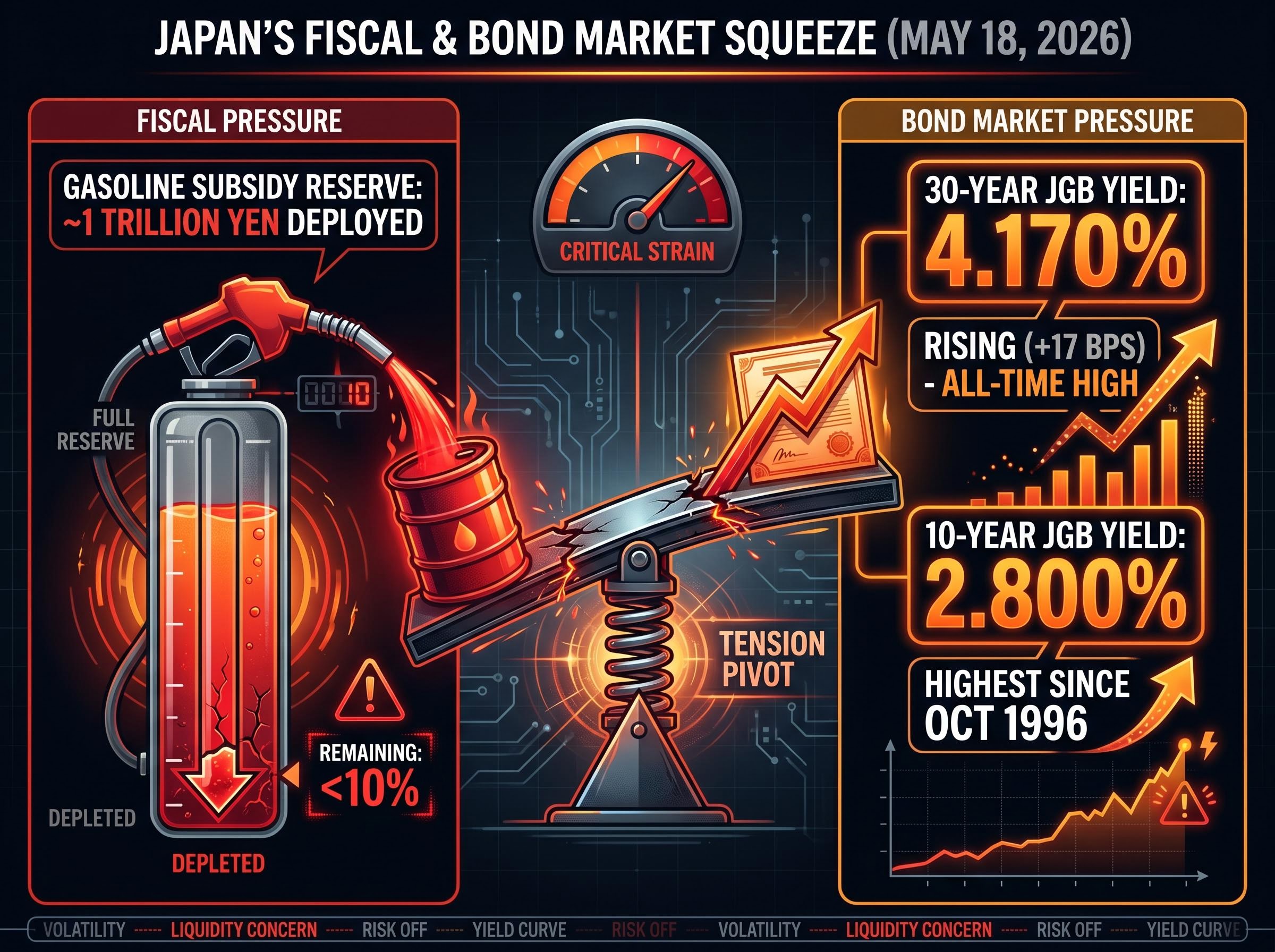

As of May 14, 2026, the Japanese government was actively compiling a supplementary budget for FY2026 to cushion the impact of elevated oil prices and living-cost pressures arising from the conflict. An existing reserve of approximately 1 trillion yen had already been deployed for gasoline subsidies, with the new package under discussion due to the risk of that reserve being depleted.

The formal size, debt instrument types, and full spending breakdown of the new supplementary budget had not been publicly confirmed as of May 18, 2026.

What is confirmed is the fiscal environment into which this spending would land. Japan carries one of the world’s highest public debt-to-GDP ratios. On May 18, 2026, the 30-year Japanese government bond (JGB) yield surged 17 basis points to an all-time high of 4.170%. The 10-year JGB yield touched 2.800%, its highest level since October 1996.

| Fiscal element | Status as of May 2026 | Key uncertainty |

|---|---|---|

| Existing gasoline subsidy reserve | Approximately 1 trillion yen deployed | Depletion timeline unclear |

| New supplementary budget | Under active discussion | Total size not confirmed |

| JGB yield environment | 30-year at all-time high 4.170% | Borrowing cost trajectory uncertain |

The bind is precise: the conflict forces additional fiscal spending, but the bond market is simultaneously making that spending more expensive. Each yen of oil-related stimulus now carries a higher interest cost than it would have six months ago.

Japan’s debt levels make this tension most visible, but the structural pressure is not unique. Oil-importing governments across Asia, Europe, and emerging markets face the same dynamic: forced energy subsidy spending arriving at the same time as rising borrowing costs. The balance sheets differ; the bind does not. The question is whether monetary policymakers can help, or whether their own dilemma makes the situation worse.

Emerging market sovereign spreads have widened by approximately 150 basis points since February 2026, a signal that the oil shock’s fiscal damage is not evenly distributed: oil-importing developing economies face the compounding pressure of higher borrowing costs and higher energy import bills simultaneously, with Morningstar warning that prolonged disruption could push EM sovereign debt losses into double-digit percentage territory.

Oil-driven inflation is cost-push rather than demand-pull. Rate increases suppress demand without addressing the supply-side cause of rising prices. Tightening into a cost-push shock risks the worst of both outcomes: persistent inflation alongside weakening economic activity.

Yet market pricing as of May 18, 2026 shows investors expect tightening regardless.

| Central bank | Current rate direction signal | Key data point | Timing expectation |

|---|---|---|---|

| Federal Reserve | Hike probability rising | Over 50% probability of increase by December 2026 (CME FedWatch) | By year-end 2026 |

| European Central Bank | Potential hike priced in | Market pricing indicates possible move | As early as June 2026 |

| Bank of England | Multiple hikes anticipated | Markets anticipate approximately two increases | Within 2026 |

The bond market is already reflecting this repricing. The 10-year US Treasury yield reached 4.6310%, its highest since February 2025. The 30-year yield hit 5.1590%, a one-year high.

Charu Chanana, Chief Investment Strategist at Saxo, framed the outlook as rates remaining “elevated for an extended period,” reflecting the persistent nature of the inflationary signal from oil markets.

Rate decisions driven by oil inflation rather than overheating demand represent a materially different risk environment. Borrowing costs rise, equity valuations face compression from higher discount rates, and government debt servicing costs climb at precisely the moment fiscal spending is being forced higher. The feedback loop tightens with every week that oil remains above $100.

The economic damage from this conflict is not linear. Extended duration compounds the problem through three reinforcing channels: inflation expectations embed more deeply into wage negotiations and pricing behaviour; accumulated fiscal spending narrows the room available for future responses; and rising debt service costs make each additional dollar of stimulus more expensive than the last.

Three variables will determine whether the situation improves or deteriorates:

Strategic reserve limitations are more binding than the headline release figures suggest: approximately 280 million barrels in combined SPR and IEA releases have failed to halt inventory drawdowns running at 8.5 million barrels per day in Q2 2026, a pace that leaves the usable buffer JPMorgan estimates at roughly 800 million barrels exposed to depletion well before any diplomatic resolution materialises.

European sovereign debt is absorbing the shock alongside US Treasuries. German bund futures and French OAT futures each declined approximately 0.4% in early trading on May 18. The US 2-year Treasury yield reached 4.1020%, a 14-month peak, signalling that short-term rate expectations have reset.

OCBC analysts characterised the probability of renewed large-scale conflict as significantly elevated. The structural conditions, high debt, rising yields, oil above $100, and stalled diplomacy, point to a constrained range of favourable outcomes rather than a clear path to resolution.

The chain traced across this analysis runs in a single connected line: a drone strike on a nuclear facility perimeter moves oil prices by 2% in one session; sustained triple-digit oil feeds inflation through fuel, logistics, and consumer prices; governments like Japan are forced into emergency fiscal spending at the same time their borrowing costs are surging; and central banks face a cost-push inflation problem that rate increases cannot solve cleanly.

What the available evidence cannot confirm is equally important. The precise dollar value of the geopolitical risk premium in current oil prices remains unquantified in public sources. Exact CPI pass-through coefficients for 2026 have not been published. Japan’s final supplementary budget size is pending. These gaps are not analytical failures; they are features of an economic environment defined by uncertainty.

The forward question is which pressure releases first: diplomatic progress that de-escalates the conflict, an OPEC+ production response that eases supply fears, or a demand-side slowdown triggered by the very tightening the conflict has forced. Each path leads to a different inflation and rates environment. None is assured.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A geopolitical risk premium is the portion of the oil price above what supply and demand fundamentals alone would justify, reflecting the market's probability-weighted expectation that conflict will disrupt physical oil supply flows.

Triple-digit oil transmits through three stages: rising energy input costs for producers, higher transportation and logistics costs across supply chains, and finally increased retail prices for food, manufactured goods, and services paid by consumers.

Oil-driven inflation is cost-push rather than demand-pull, meaning rate increases suppress economic activity without addressing the supply-side cause, risking persistent inflation alongside a weakening economy simultaneously.

Japan had already deployed approximately 1 trillion yen in gasoline subsidies and was compiling a further supplementary budget as of May 2026, while borrowing costs simultaneously surged, with the 30-year JGB yield hitting an all-time high of 4.170%.

The three critical variables are diplomatic progress toward a ceasefire, whether OPEC+ increases production to offset supply disruptions, and whether central bank tightening tips oil-importing economies into recession before inflation is brought under control.